Daniel Grizelj

We previously covered BYD Company Limited (OTCPK:BYDDF) in October 2023, discussing its bright prospects as one of the top-selling automakers in the far future, thanks to its profitable growth trend and robust domestic/ international demand.

Combined with its depressed valuations and low cost vertically integrated supply chain, we had maintained on Buy rating for the stock.

In this article, we shall discuss how BYDDF has performed against Tesla (TSLA) in FY2023, with the Chinese based automaker emerging as the king of EVs based on the FQ4’23 production/ sales number.

The management has also demonstrated why it will be able to maintain its highly competitive ASPs and decent automotive profit margins ahead, thanks to its expanding footprint in Latin America and Hungary.

As a result of these developments, we maintain our Buy rating, with us upgrading our long-term price target with the lifting market sentiments and thawing geopolitical tensions likely to trigger the upward rerating in its P/E valuations ahead.

The BYDDF Investment Thesis Is Even More Tempting Here

For now, BYDDF has reported an excellent FY2023 production of 3.04M (+62.5% YoY) and deliveries of 3.02M (+62.3% YoY), with FQ4’23 bringing forth an excellent annualized production of 3.72M (+64.6% QoQ/ +36% YoY) and deliveries of 3.77M (+68.3% QoQ/ +36.2% YoY).

These are new milestones for the Chinese-based automaker indeed, with it trumping TSLA as the largest EV/ PHEV producer globally.

For context, TSLA produced 494.9K units (+14.9% QoQ/ +12.5% YoY) and delivered 484.5K in FQ4’23 (+11.3% QoQ/ +19.5% YoY), or the equivalent annualized total of 1.97M and 1.93M units, respectively.

Anyone concerned about BYDDF’s hybrid approach may be rest assured, since the Chinese based automaker reported pure EV production of 518.96K units (+18.2% QoQ/ +59% YoY) and sales of 526.4K units in FQ4’23 (+21.8% QoQ/ +60% YoY), clearly exceeding TSLA’s numbers over the same time period.

With TSLA expecting to deliver 2.2M units in 2024, it appears that BYDDF may very well retain the honor of being the EV King ahead, based on its annualized FQ4’23 production/ delivery numbers.

It is also unsurprising that BYDDF remains the most popular EV in China with an average ASP of 136K Yuan, compared to TSLA’s Model 3 at 260K Yuan and Model Y at 310K Yuan.

The Chinese consumer demand for EVs has yet to abate as well, with 2023 bringing forth 9.4M in overall EVs sold (+36.2% YoY) and 2024 projected to grow to 11.5M units (+22.3% YoY), with BYDDF likely to emerge at the top again.

Therefore, while BYDDF has yet to announce FQ4’23 earnings results, we believe that the quarter may bring forth excellent growth on a QoQ/ YoY basis.

This will build upon the top/ bottom line expansion we have observed in its FQ3’23 earnings, with 822,094 units delivered (+16.9% QoQ/ +64.2% YoY), 162.15B Yuan of sales (+15.8% QoQ/ +38.5% YoY), and 3.58 Yuan per share in EPS (+52.3% QoQ/ +82.5% YoY).

At the same time, BYDDF’s aggressive global expansion has been paying off, with it exporting 97.23K units in FQ4’23 (+36.5% QoQ), demonstrating why its affordable offerings are highly popular despite the higher import taxes.

Much of its tailwinds is attributed to the management’s strategic launch in North and Latin America, with four models already sold in Mexico, namely Dolphin hatchback at approximately $31K, Han sedan at $81K, Tang SUV at $82K, and Yuan Plus crossover at $47K, based on the foreign exchange at the time of writing.

While the rest may be notably expensive, BYDDF’s Dolphin may be a game changer in North America, with it still cheaper than many other legacy/ start up automakers’ EV offerings at an average of ASPs of $50K, despite the hefty 27.5% import taxes.

At the same time, the Chinese automaker has embarked on new growth opportunities in Brazil, attributed to the R$3B investment in three factories in Bahia from H2’24 onwards, for the production of electric buses/ trucks, hybrid/electric cars, and processing of lithium/ iron phosphates.

Readers must note that the Latam region has the world’s largest deposits of both copper and lithium, both of which are critical to the electrification cadence through the next few decade.

The region is also the home base to many of the world’s largest commodity mining operations, including Albemarle Corporation (ALB), Sociedad Quimica y Minera de Chile S.A. (SQM), BHP Group Limited (BHP), and Rio Tinto (RIO).

ABVE, the Brazilian Association of Electric Vehicle, already expects sales of EV/ PHEVs in Brazil to grow drastically by nearly +60% YoY to 150K units in 2024, building upon the robust +91% YoY growth reported in 2023.

This is on top of BYDDF’s first European EV factory in Hungary, where the hourly labor costs are drastically lower at €10.7 compared to Germany at €39.5. This implies its ability to maintain its low production costs more efficiently than TSLA’s Berlin operations.

These developments naturally demonstrate BYDDF’s highly successful vertically integrated supply chain from raw materials and finishing of battery packs in multiple regions, further underscoring why it has been able to produce highly affordable EVs with modest profit margins.

This may also be significantly aided by the moderating lithium spot prices, with the volatile WTI crude oil prices likely to accelerate the price parity between EV and ICE vehicles. For now, Goldman Sachs already expect this to occur by mid-2026, implying that BYDDF’s export numbers may further grow from current levels.

So, Is BYDDF Stock A Buy, Sell, or Hold?

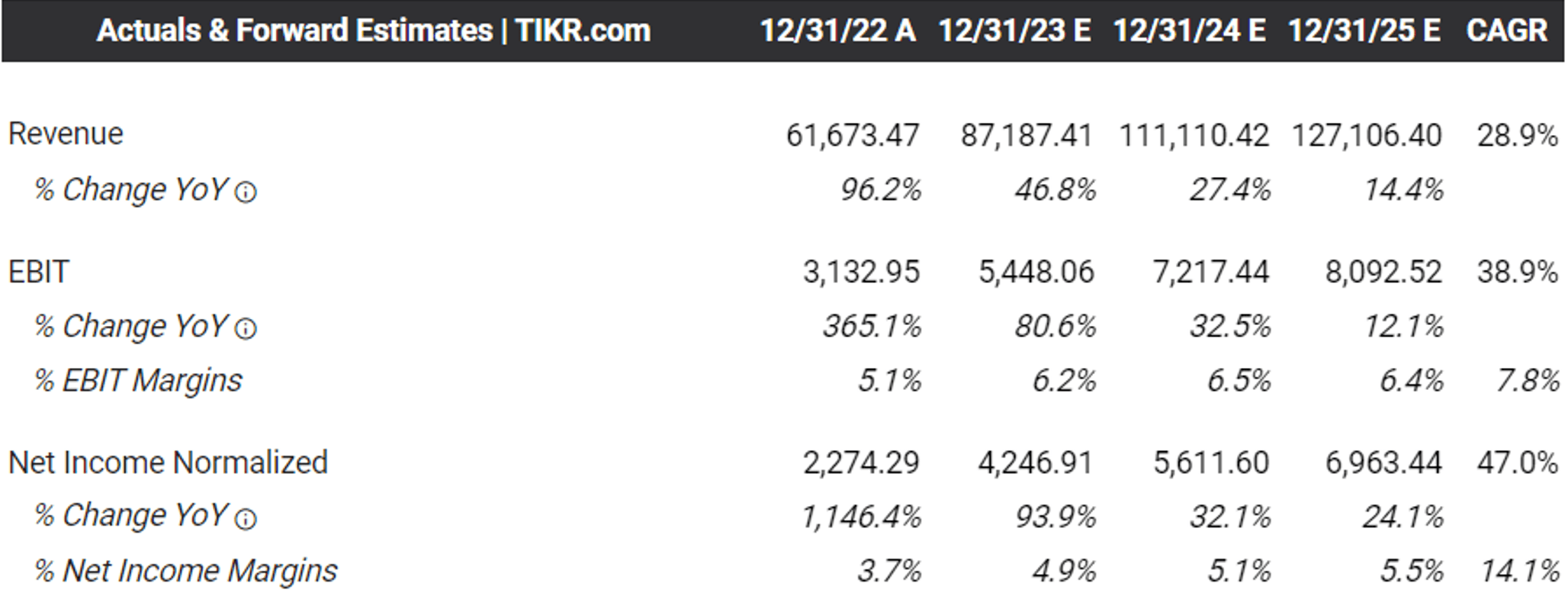

The Consensus Forward Estimates

Tikr Terminal

For now, the consensus estimates that BYDDF may keep its EBIT margins steady at approximately ~6% through FY2025, implying the increased likelihood of the automaker lowering ASPs as its production scale improves, which in turn drives consumer adoption as EV parity nears.

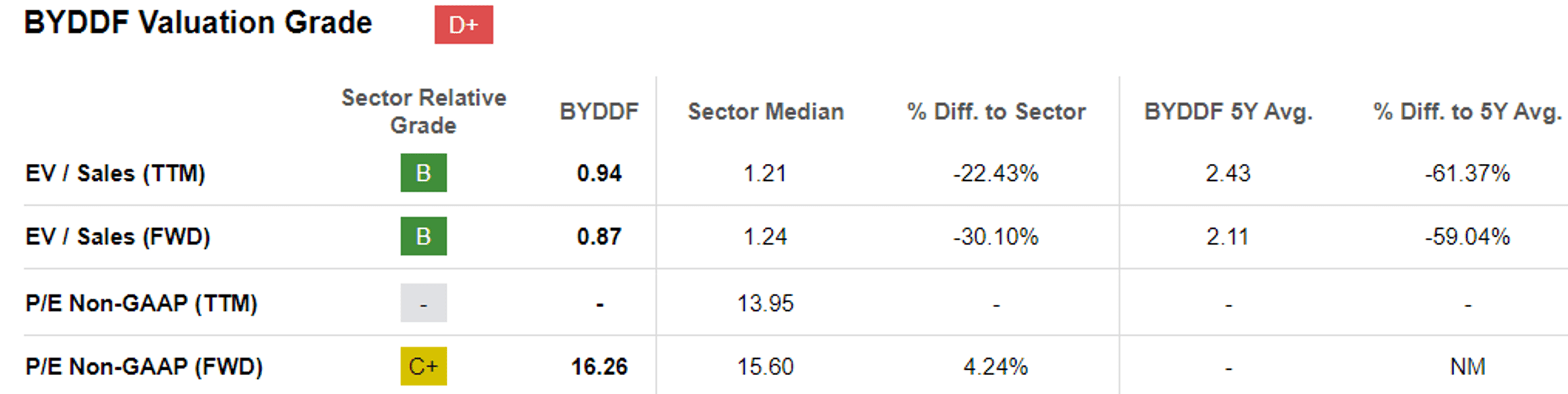

BYDDF Valuations

Seeking Alpha

These factors are why we believe that BYDDF’s FWD P/E valuation of 16.26x is very attractive here, with it comparatively undervalued compared to TSLA’s 74.63x.

While geopolitical concerns remain valid and thus explaining its depressed valuations, we believe that an upward rerating is very likely after the headwinds lift and macroeconomic outlook normalizes.

If anything, the meeting between President Biden and President Xi in November 2023 marked the potential thawing in the ongoing trade war, with the BYDDF likely to be upgraded nearer to TSLA ahead.

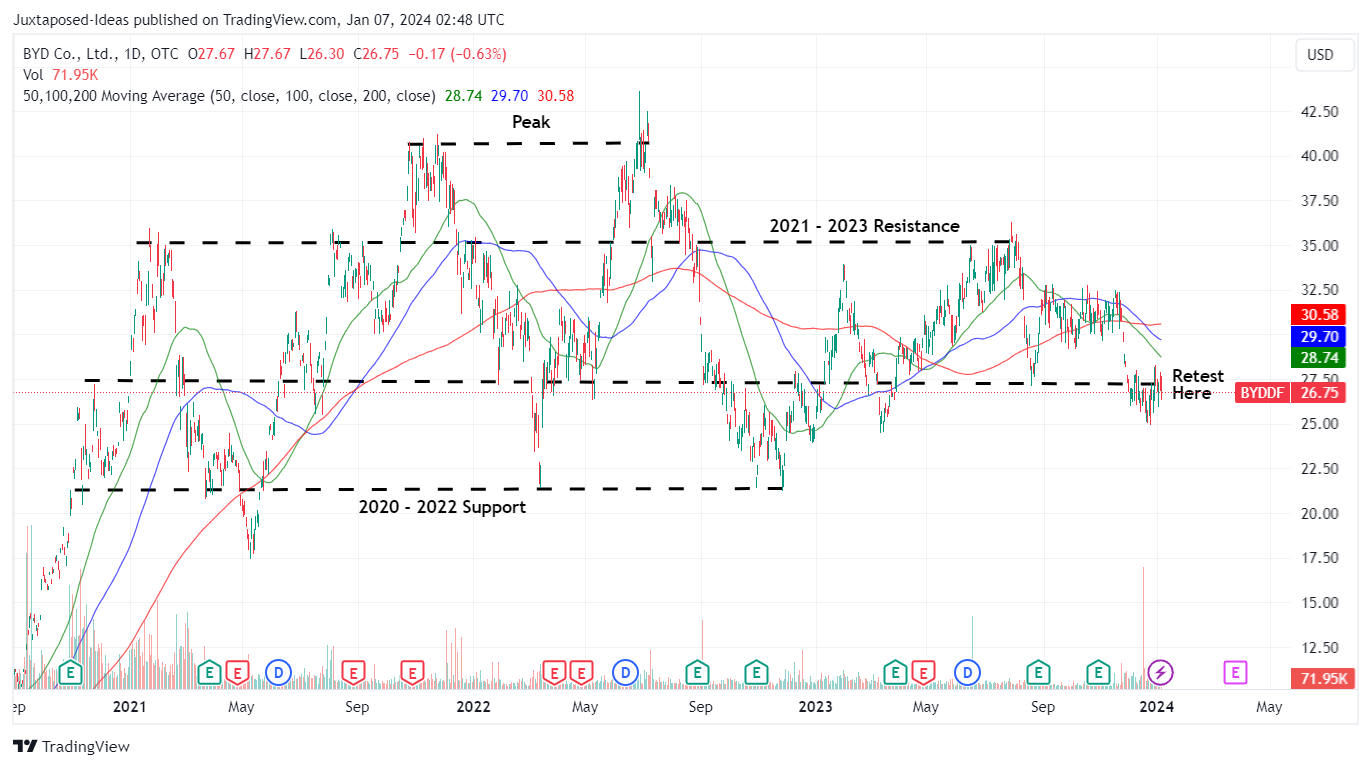

BYDDF 3Y Stock Price

Trading View

With BYDDF now well-supported at the $20s through the bottoming of the stock market in October 2023, we believe that these levels offer a highly attractive risk reward proposition for value oriented investors with higher risk appetite.

Based on the consensus FY2025 adj net income estimates of $6.96B and its FQ3’23 share count of 2.9B, we are looking at an approximate adj EPS of $2.40. Combined with its FWD P/E of 16.26x, we are looking at a base case long-term price target of $39, implying an excellent upside potential of +45.7% from current levels.

However, we are confident that BYDDF’s upward rerating to its pre-pandemic P/E mean of 37x may eventually occur, suggesting an even more bullish long-term price target of $88.80, with it offering an impressive +231% upside potential.

As a result, we maintain our Buy rating on the BYDDF stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")