Editor’s note: Seeking Alpha is proud to welcome DT Invest as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Leon Neal/Getty Images News

My thesis

As mostly a growth investor, I seek for industries expected to grow over the long-term. The electric vehicles (EV) market looks especially interesting after valuations moderated since the 2020-2021 craze. I am not a risky investor and I prefer to invest in market leaders with strong strategic positioning. After beating Tesla (TSLA) in 2023 as the largest EV manufacturer, BYD (OTCPK:BYDDF) became an undisputed EV industry leader. My analysis of the company’s business and its financials reveals several bullish signs. From the business perspective, I like BYDDF’s ability to ramp up quickly enough to address growing demand. The strategy of targeting price-conscious consumers also looks sound considering the average residual income of Chinese households. From the financial perspective, I like that the revenue growth results in improving profitability. It means that there is high probability that the expected revenue growth will lead to more profits. What is also essential is that the intrinsic value is substantially below the current market capitalization. All these factors make the stock a Buy and I plan to add the stock to my long-term portfolio at current share price levels.

BYDDF: business perspective

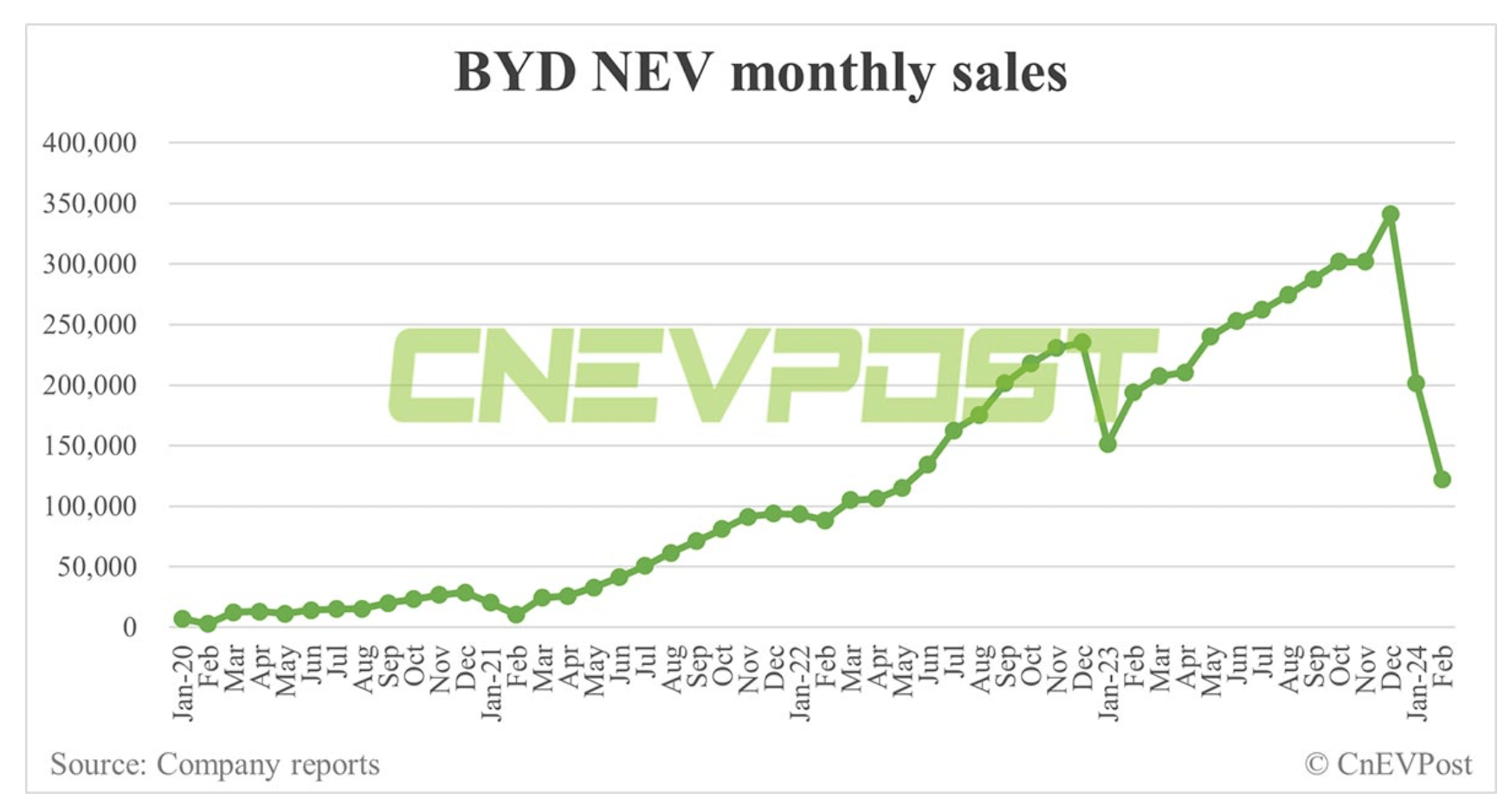

As mentioned in the introductory paragraph, BYD is now the world’s largest EV manufacturer. The company produced more than three million electric vehicles in 2023, about 66% more than Tesla did in the same year. The dynamics looks mixed in 2024 as BYD recorded a 64% YOY production increase in January accompanied by a 48% increase in sales, but recorded falling volumes in February. I think that the mixed picture in 2024 is due to peculiarities with every year’s shifts in holiday dates due to the Chinese New Year (Lunar New Year). For example, in 2023 Lunar New Year holidays were between January 22 and February 5, while in 2024 holidays were between February 10 to February 17. Therefore, I expect the dynamic to become more fair and smooth in March 2024, and this will be an important data I will be looking at. According to the below chart, in March 2023 BYD sold around 200 thousand EVs, which is approximately January 2024 levels. Since company had several months of delivering far above 200 thousand vehicles per month in 2023, beating March 2023 levels looks doable, in my opinion.

CnEVPost

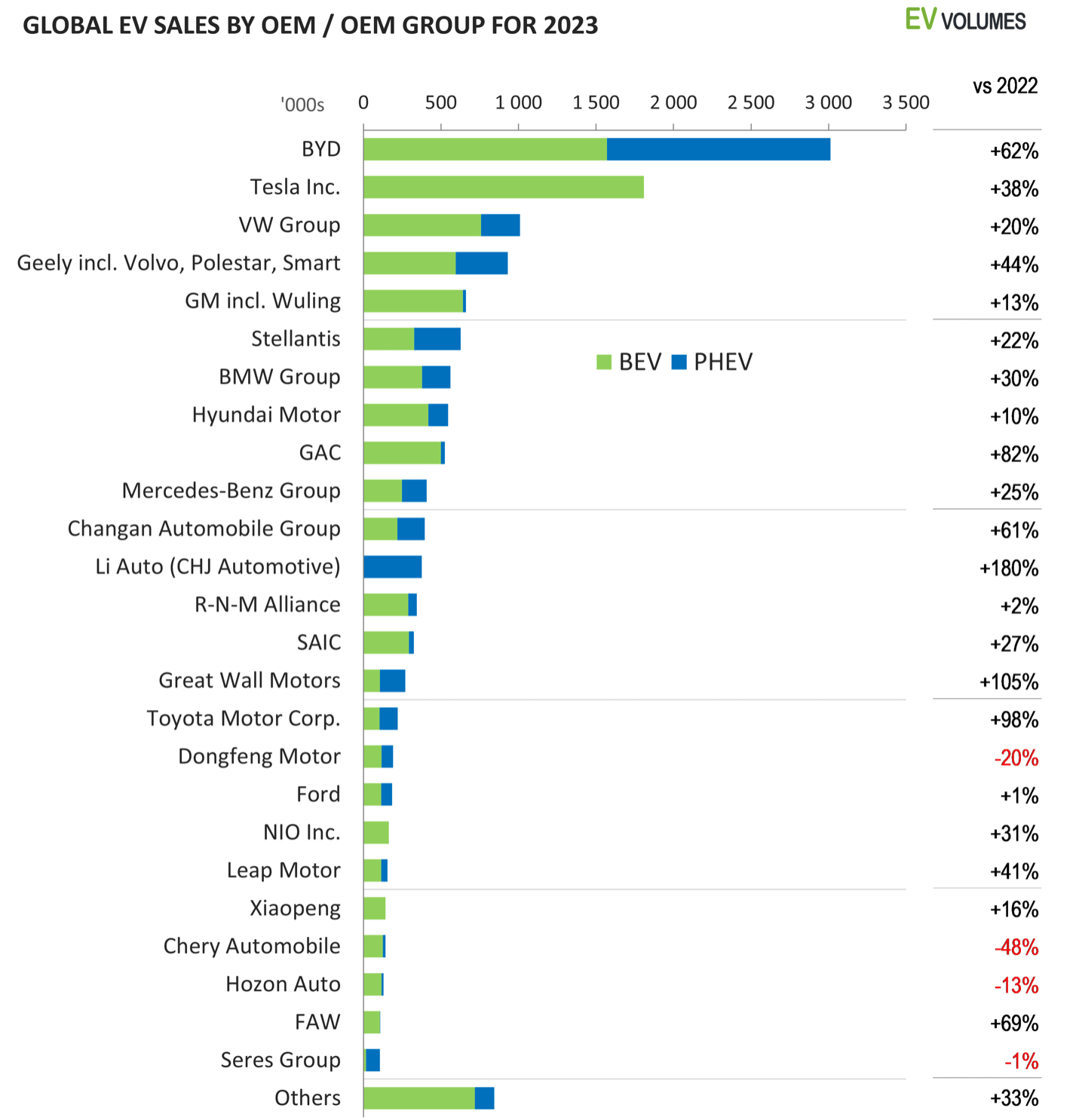

BYD is an indisputable global EV leader in terms of production and deliveries volume. I have already mentioned that 2023 sales were around 66% higher than the second spot, Tesla. Third place, Volkswagen (OTCPK:VWAGY) sold around one million EV’s in 2023, three times less than BYD. Figures demonstrated by companies below Volkswagen are much lower, and the gap between BYD and all other players is a solid advantage for the company. Despite the largest volume, BYD also demonstrated the biggest percentage growth in 2023 compared to 2022, another indication of the company’s strength.

EV-Volumes

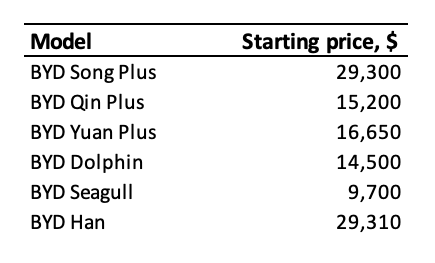

BYD’s strength compared to its closest rivals, Volkswagen and Tesla, is explained by the fact that the company targets lower budget consumers with its cheap models like Seagull, which starts even below $10,000 at the moment. Apart from the Seagull model, there are five more BYD models in the top-10 best-selling EVs in 2023. As shown below, none of the model starts above $30,000. Meanwhile, Tesla’s cheapest option of Model 3 starts at around 246,000 RMB, which is approximately $34,000. Volkswagen’s ID.4 model is cheaper and starts at slightly above $20,000, but still BYD has four models which are cheaper.

Compiled from public sources

Aiming the most price-conscious audience looks like the primary factor fueling BYD’s success since per capital annual disposable in China in 2023 equaled around 39,000 RMB, which is approximately $5,400. This is around ten times lower compared to USA, which emphasizes that there are much more price conscious consumers in China than in the U.S. BYD does not try to match Tesla’s technological advantage (FSD, safety), but instead differentiates itself as a cost leader and looks successful in its niche.

BYDDF: financial perspective

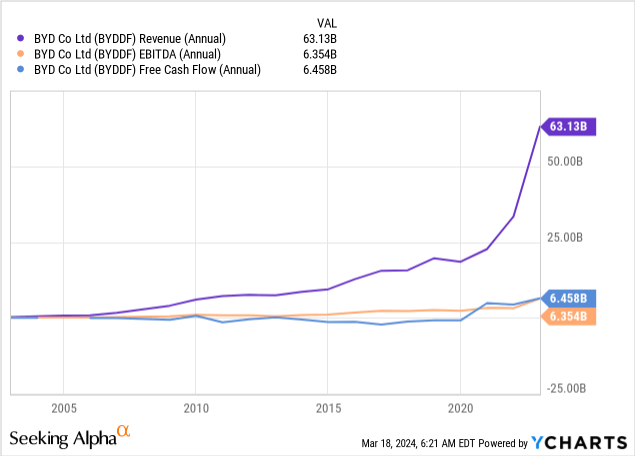

Production and deliveries growth together with solid strategic positioning is good, but at the end of the day it has to be converted into profits and free cash flow. BYDDF’s revenue grew dramatically in recent years, but the free cash flow is lagging in growth pace. This is explained by substantial investments into business, required to match the high demand for the company’s vehicles. Overall, the EBITDA and free cash flow dynamics are positive and BYDDF generated more than $6 billion free cash flow in the last fiscal year.

Profitable growth means that the company is able to accumulate more resources which can be either reinvested into business or distributed to shareholders. Since the business experiences strong growth momentum, I think that it is more reasonable to allocate more financial resources into reinvesting.

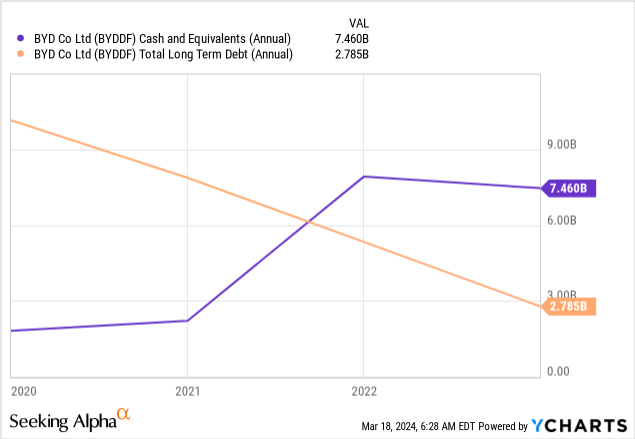

Due to the positive free cash flow, the company improved its cash position in recent years compared to 2020 and the total long-term debt declined dramatically. Both trends are positive for investors and indicate improving financial position of BYDDF.

Since the company drives profitable growth and is backed by a solid financial position, there is a high probability that BYDDF has solid position to continue successfully executing its long-term strategy.

Intrinsic value calculation

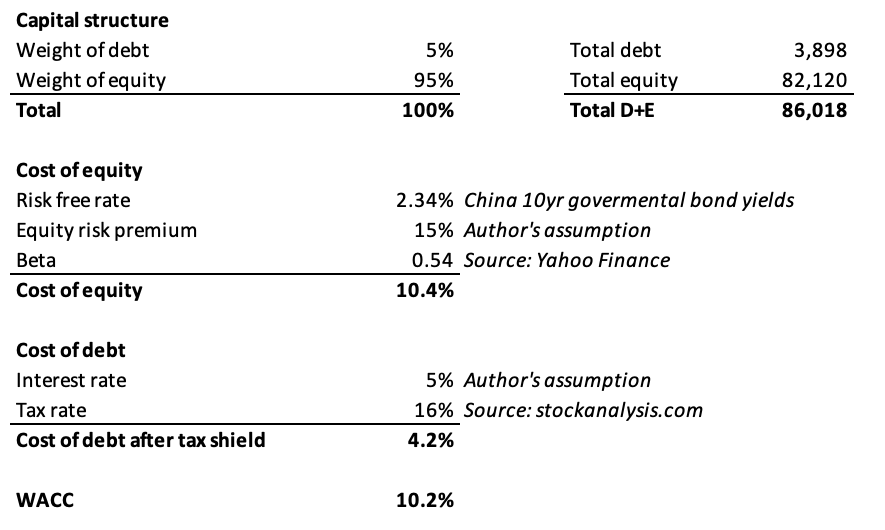

Discount rate plays crucial role in my valuation analysis since the intrinsic value will be calculated by discounting cash flows (DCF). I use a classical CAPM approach to derive the discount rate, or the WACC. According to my working below, BYDDF’s WACC is 10.2% and I will use it as a discount rate for my DCF.

DT Invest

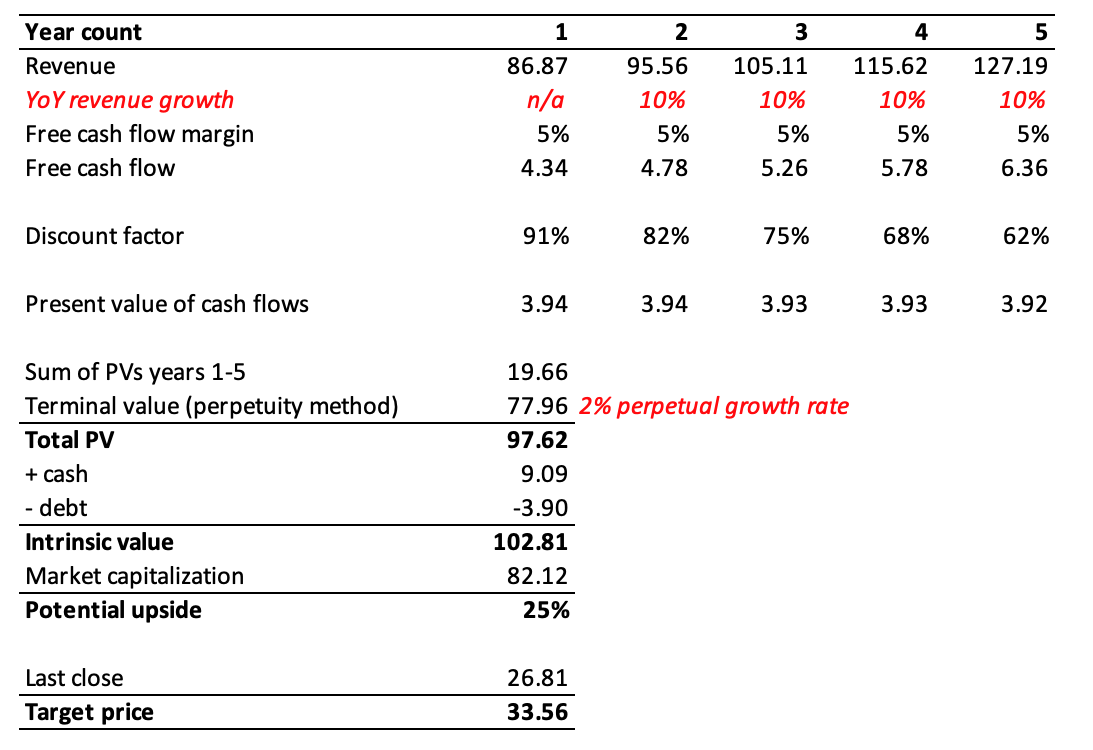

With WACC figured out I now can move on to the intrinsic value calculation. All my assumptions can be seen in the below working, to be more understandable I will explain the logic behind my assumptions. Year 1 $86.87 billion revenue is the projection provided by Seeking Alpha with the reference to consensus. Searching the internet for the Chinese EV market growth projection gives multiple resources with very different long-term CAGR projections varying between 6% and 16%. In this situation I prefer to seek somewhere in the middle and a 10% CAGR looks like a safe choice to me. A 5% free cash flow margin is an average between the sector median and BYDDF’s last five years average, both figures provided by Seeking Alpha. I am using a very modest growth rate for the perpetuity method used to derive the terminal value.

Based on all the above assumptions and my WACC calculations, the intrinsic value of the company is $103 billion. The intrinsic value is 25% higher than the market capitalization, meaning that the target price is $33.56. I arrived at this figure by multiplying the last close by the potential upside plus 100%.

DT Invest

What can go wrong with my thesis?

My thesis is bullish and based on the general idea that BYD will continue successfully ramping up at least in line with the growing Chinese EV market. But the level of competition in the Chinese EV industry is very intense and crowded by numerous ambitious local brands like NIO (NIO), Li (LI), XPeng (XPEV), Voyah, Zeekr, and even consumer electronics giant, Xiaomi (OTCPK:XIACF). Let’s also not forget that major western automotive companies are also present in the country. Tesla’s gigafactory Shanghai, which ramped up with impressive pace in recent years, is quite well-known due to the big interest around Tesla. But I was surprised to find out that the European giant, Volkswagen, has 33 plants in China which in total produce around 4 million vehicles annually. Therefore, the competition is tough and my thesis is likely to go wrong if BYD fails to protect its market share.

The risk might look remote today in early 2024, but Tesla already announced its plans to build by 2025 a cheaper EV which will be priced at about $25,000, codenamed “Redwood”. Volkswagen also has plans to build a 20,000 Euro model, partnering with Renault.

Let’s also not forget that BYDDF is a Chinese company, meaning it faces a myriad of country risks. The most apparent one is the foreign exchange risk since the company operates in Chinese currency (RMB), while my intrinsic value calculation is in U.S. dollars. Fluctuations in foreign exchange rates might have unfavorable effect in BYDDF’s financial performance measured in USD, which is a risk. Another country risk is the perpetuity of power, since the general secretary of the Chinese Communist Party (CCP), Xi Jinping, is in charge for more than a decade and has a mandate until 2028. The longer the country’s leader is in charge, the higher the risk of concentrating too much power in one hands which can lead to sharp shifts in policies, laws, and regulations. This might not be necessarily adverse for BYDDF, but investors should be aware about the high level of political uncertainty the company faces. Last but not least, the current state of tense relationships between China and the West might limit export potential of BYDDF and the company will be unable to realize its full potential.

Summary

I think that trends BYD demonstrates both from the business and financial perspectives suggest that the company’s dominance in the EV industry is sustainable. The stock is attractively priced compared to the intrinsic value and considering all pros, I consider BYDDF as a very good investment opportunity to add to my portfolio.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")