z1b

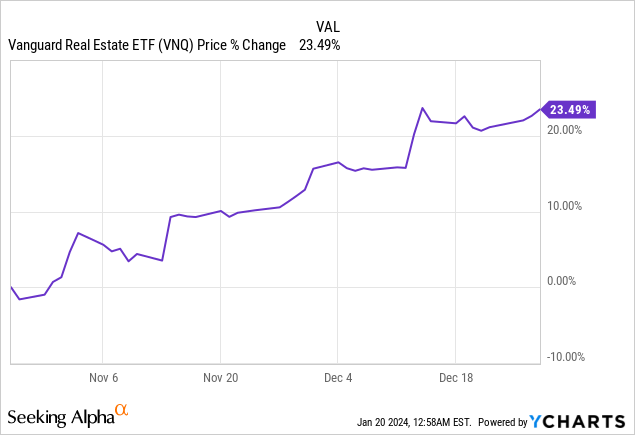

REITs (VNQ) rallied strongly in late 2023 when the Fed indicated that we would have at least 3 interest rate cuts in 2024:

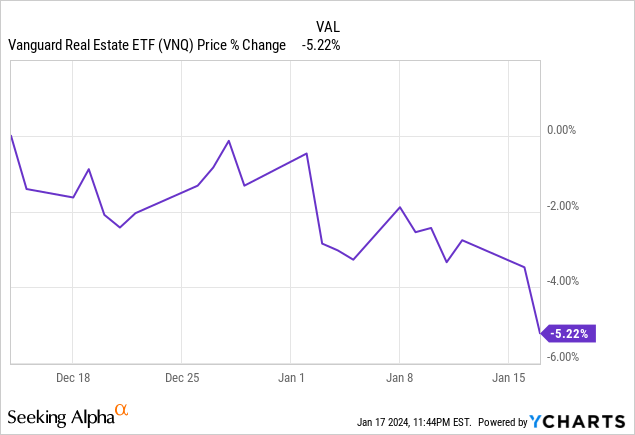

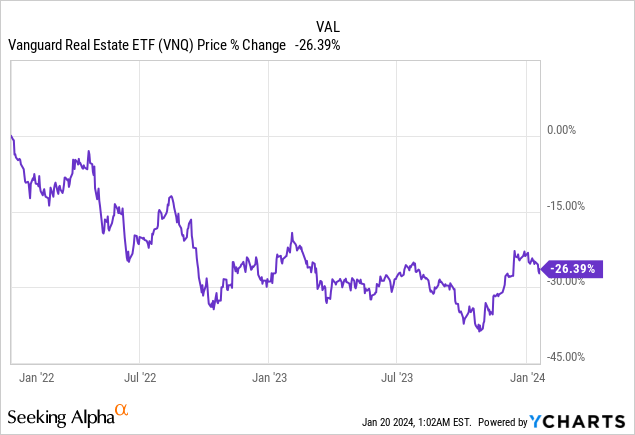

But since then, REITs have dipped back to lower levels, and in some cases, the dip has been quite significant:

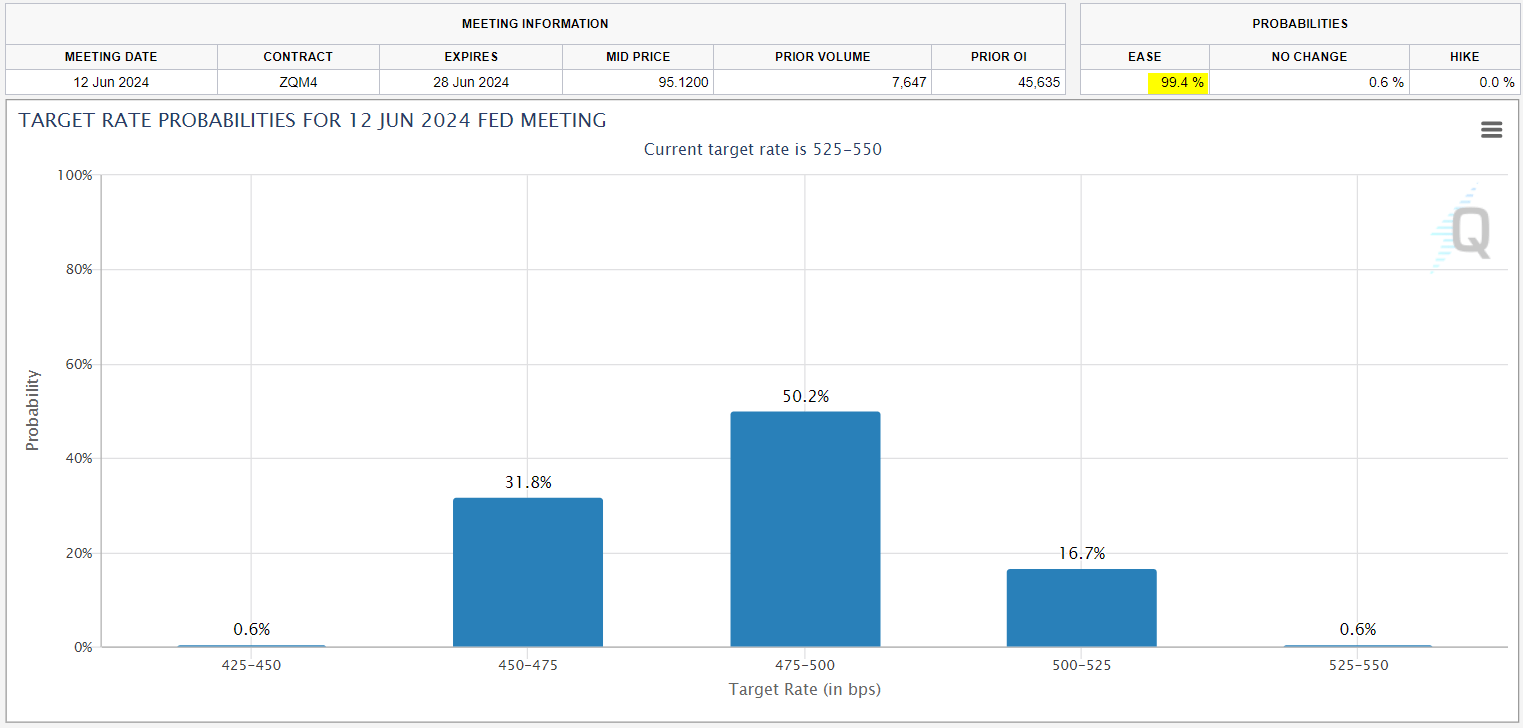

I believe that this is an opportunity because the expectations for lower interest rates haven’t changed. In fact, the FedWatch tool now pricing a 99.6% chance of at least one rate cut by June:

FedWatch

Therefore, the dip didn’t occur because of a change in the outlook. Rather, it seems that short-sighted investors are taking profits, failing to realize that REITs remain heavily discounted even following the recent rally.

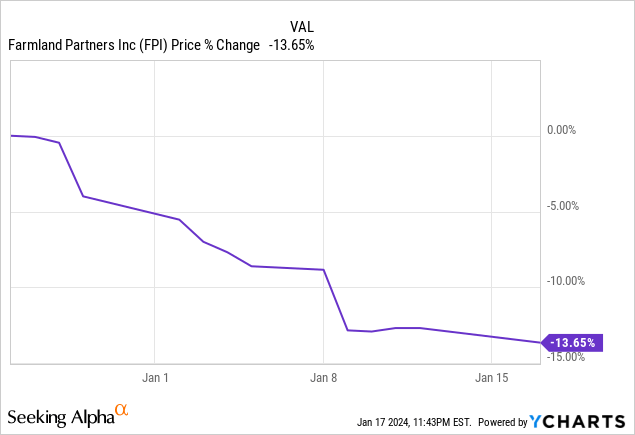

Right now, REITs are still down 26% over the past two years, and that’s despite growing their cash flows by 5-10% since then. I would add that this is just the average. Many individual REITs are down much more than that:

The reason why REITs are down so much is because a lot of investors are today still comfortably hiding in money market funds, earning them a 5%+ yield. But as interest rates are cut, I expect a lot of that money to come right back into REITs and other high-yielding equities that suffered in recent years.

For this reason, I continue to accumulate more REITs, especially following the recent dip.

Here are two of my favorite “Buy The Dip” opportunities at the moment:

Farmland Partners (FPI)

After briefly recovering all the way to $13 per share… Farmland Partners is now back in the low $11s:

I believe that FPI is a compelling purchase at $11 per share because we estimate its net asset value to be right around $18.

Put differently, it is currently priced at a ~40% discount to its net asset value.

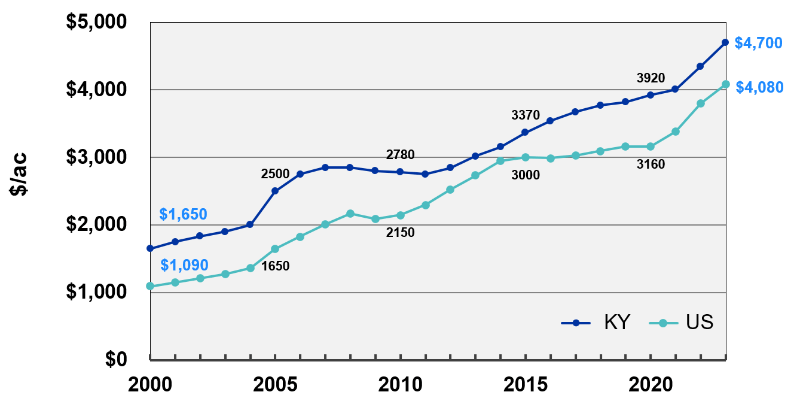

The reason why it got so cheap is that its share price declined with the rest of the REIT sector even as farmland kept appreciating in value. In fact, today, farmland is more valuable than ever before:

University of Kentucky

Farmland Partners

The interesting thing here is that the management is actively taking advantage of this disconnect between public and private markets by selectively selling properties at premiums to their book value and buying back shares at large discounts to their fair value.

Last year alone, they announced $120 million worth of sales with an average 15% gain, and these proceeds were then used to buy back shares and pay off debt.

That’s very significant for a company with a $550 million market cap.

In addition to that, the chairman and former CEO of the REIT also bought another million worth of stock with his personal money, and that’s despite already having the bulk of his net worth tied down to the stock:

Openinsider

He is bullish because he likes the idea of buying farmland equity at 60 cents on the dollar and so do we.

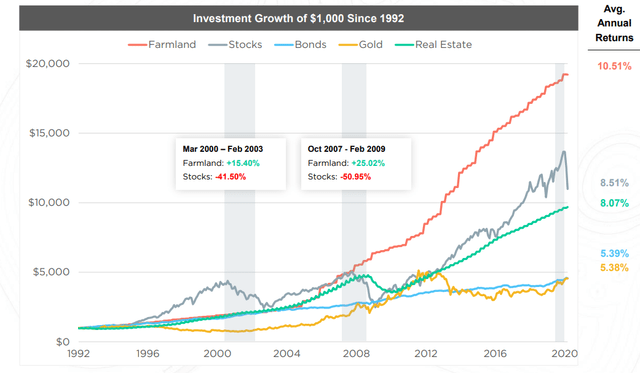

Farmland has consistently been one of the best investments over the long run, generating even higher returns than those of the S&P 500 (SPY):

Farmtogether

Bought at a large discount, it of course becomes an even better investment.

I think that as interest rates return to lower levels, investors will again regain confidence in REITs, and this should be particularly beneficial to lower-yielding REITs like FPI, which have been shunned by investors in recent years.

I expect 30-50% upside in a future recovery as its share price returns closer to its net asset value. If it doesn’t, they will simply keep selling assets to buy back shares, and eventually, it wouldn’t surprise me if they decided to sell the entire company to unlock its value. After all, the insiders are heavily invested in the stock and their patience will eventually run out.

Camden Property Trust (CPT)

Camden Property Trust is one of our favorite apartment REITs.

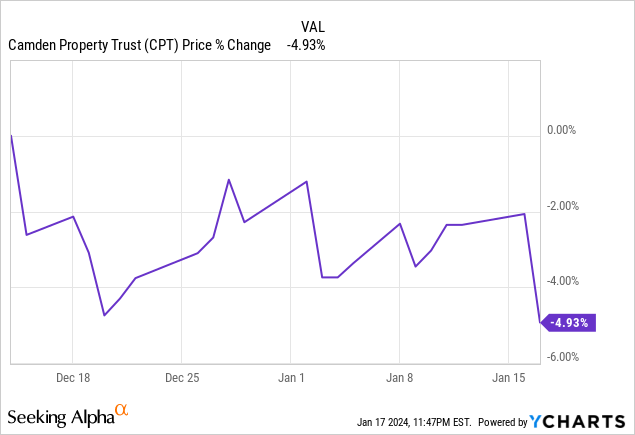

It didn’t drop as much as Farmland Partners, but it didn’t rise as much in the first place either. It is down 5% nonetheless, which is in line with the broader REIT market, despite not recovering as much in the previous months:

I believe that the main reason for this recent underperformance is that loan delinquencies are on the rise in the apartment sector.

A lot of private equity landlords are today overleveraged in the face of rising interest rates. They commonly use 60-70% and lots of variable debt, which is putting great pressure on them, especially now that rent growth is slowing down.

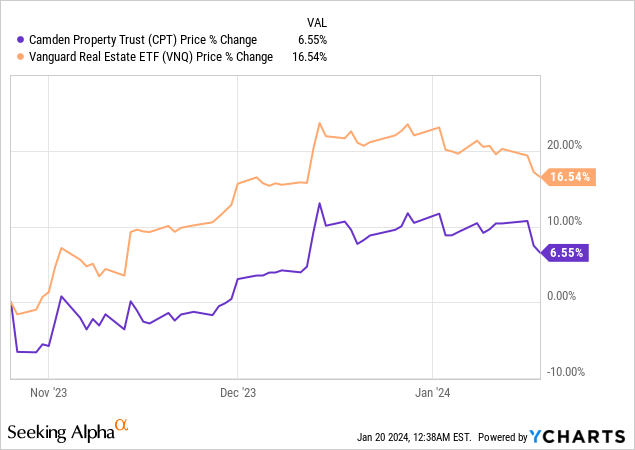

Camden Property Trust

But there’s a tradeoff here for the well-capitalized apartment REITs like Camden Property Trust.

Its LTV is just around 30% and it has the balance sheet strength to buy properties from distressed sellers at low prices. Mid-America (MAA), another apartment REIT, already closed one such deal in Q3 at a great price.

Therefore, we actually think that the recent loan delinquencies are a net positive for REITs like Camden Property Trust. Sure, it could hurt property values a bit in the near term, but Camden has an A-rated balance sheet, which will allow it to pick up the pieces at discounted prices, benefiting shareholders over the long run.

Camden Property Trust

Even then, the market has priced Camden at a ~35% discount to its net asset value, which is quite exceptional considering that this is a blue-chip apartment REIT with a fortress balance sheet and a long track record of significant outperformance.

We expect the weakness of the apartment sector to last for another year or two, but the silver lining is that this has put new development projects on halt and growth should therefore reaccelerate in 2025-2026.

As rent growth reaccelerates and interest rates return to lower levels, I expect Camden to reprice at closer to its net asset value, unlocking 30-50% upside from here. While you wait, you earn a 4% dividend yield and the company will keep acquiring new assets to create value and grow its cash flow.

Closing Note

If you missed the REIT buying opportunities in 2023, now is your second chance to buy discounted REITs following their recent dip.

But the window of opportunity is now closing… As interest rates return to lower levels, I expect REITs to recover a lot higher.

Q2 2024 Earnings Call Transcript")