With the S&P 500 index up more than 25% over the past year and 6.5% so far in 2024, it’s time to look beyond the usual suspects and toward stocks that haven’t participated in the rally so far this year. Whirlpool (WHR 1.10%) and Owens Corning (OC 0.93%) match this description and I think they have the potential to do well through the year. Here’s why.

Why Whirlpool stock is a buy

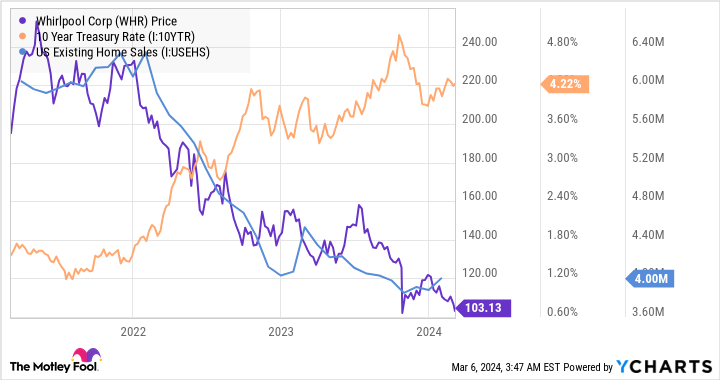

As you can see below, the housing market (expressed here in terms of sales of existing homes) doesn’t like higher interest rates, and Whirlpool’s share price doesn’t like a declining housing market.

As such, the uptick in interest rates (which push up mortgage rates) in 2024 on the back of hotter-than-anticipated inflation data is not good news for Whirlpool or, rather, sentiment over its stock.

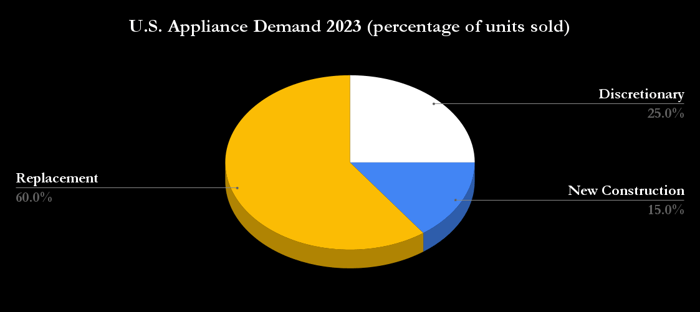

During a recent presentation to investors, management outlined that a quarter of demand for appliances in the U.S. comes from discretionary demand guided by existing home sales, and a further 15% is from the construction of new homes. In other words, 40% of end demand is guided by housing market conditions.

Chart by author. Data source: Whirlpool presentations.

As such, sentiment over the stock is going to be guided by interest rate movements. However, long-term investors should focus on the underlying improvement in the business coming from refocusing on its core North American market. Whirlpool is about to combine its European business with a subsidiary of a Turkish company, Arcelik, while taking a 25% stake in the new company — a deal that will pull it out of Europe directly. Whirlpool also cut costs by $800 million in 2023, with a further $300 million to $400 million expected in 2024.

Moreover, history suggests that the interest rate cycle will turn, and so will the demand for housing. That will help management achieve its aim of growing earnings before interest and taxation (EBIT) margin to 9% in 2026 from 6.8% in 2024. In addition, management thinks it can hit free cash flow (FCF) of $1.1 billion in 2026, representing 19.5% of the current market cap. If it gets anywhere near that figure, the stock will appreciate significantly.

Why Owens Corning stock is a buy

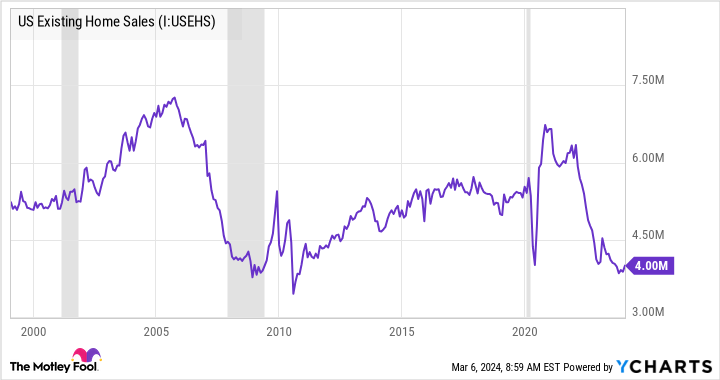

Whirlpool’s management believes that the slump in existing home sales and housing starts in the U.S. means the industry is set for a multiyear expansion.

US Existing Home Sales data by YCharts

If so, then investors should take a close look at roofing, insulation, and composites company Owens Corning, because its management has decided to double down on the U.S. housing market by agreeing to acquire interior and exterior door manufacturer Masonite International for an enterprise value of $4 billion.

While the deal comes at a hefty 38% premium to Masonite’s share price, it makes sense for Owens Corning. It will strengthen its exposure to U.S. housing, making it a market leader in residential building materials. Owens Corning and Masonite sell to the same types of customers (builders, contractors, distributors, home centers, homeowners, etc.), so there’s an obvious opportunity to generate revenue synergies — meaning the combined company can make more sales than the two would as individual entities.

However, since it is harder to make assumptions about revenue synergies, acquiring companies usually outline cost synergies (e.g., sharing sourcing and supply chain and sales, general, and administrative costs), and here Owens Corning believes it can generate $125 million in cost synergy by the end of the second year.

Including those synergies means Owens Corning is buying Masonite at a value of 6.8 times earnings before interest, taxation, depreciation, and amortization (EBITDA) rather than the 8.6 times estimated Masonite 2023 EBITDA at the time of the deal.

Moreover, management believes the cash flow generated by the new company will enable it to reduce its net debt-to-EBITDA level to just 2 times EBITDA at the end of 2024. In the meantime, the company is conducting a strategic review of its industrial-focused glass reinforcement business, a move that could signal the sale of a non-core business.

Image source: Getty Images.

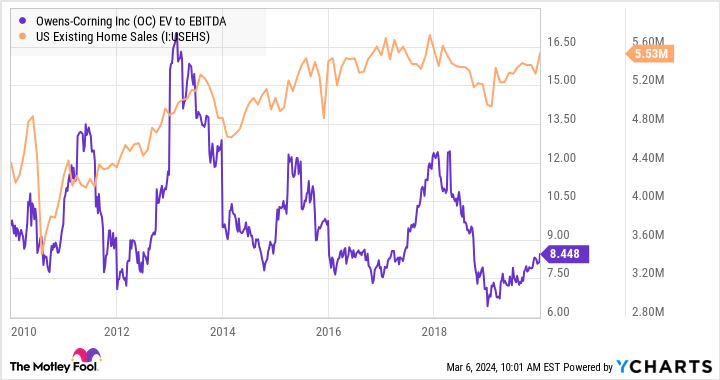

If Owens Corning is right and the new company hits $2.9 billion in EBITDA, and the housing market returns to more normal conditions, such as in 2010-2020, the stock could have significant upside if it returns to the kind of enterprise value (market cap plus net debt) to EBITDA levels achieved in that period.

OC EV to EBITDA data by YCharts

For example, 8 times EBITDA of $2.9 billion would give the combined company a market cap of $23 billion compared to the $13 billion that Owens Corning currently trades at and the enterprise value of $4 billion its paying for Masonite.

All told, Whirlpool and Owens Corning are highly attractive stocks for investors who believe a bull market in housing is coming around the corner.

Q2 2024 Earnings Call Transcript")