kerkla

Investment Thesis

Builders FirstSource (NYSE:BLDR) has been a very good holding for me, but now has come the time to say our teared-eyed farewell, bon voyage, and good luck departure.

Ultimately, as an inflection investor, you are always unpopular. You are unpopular with buying the stock when nobody sees what you see. And you are unpopular when you recommend exiting the stock, as you don’t believe the risk-reward is compelling looking ahead.

More specifically, according to my estimates, BLDR is now priced at 16x forward free cash flow. A multiple that I do not believe is enticing enough for new investors looking at this stock with free cash flow.

Therefore, I’ve called it a day on this name.

Rapid Recap,

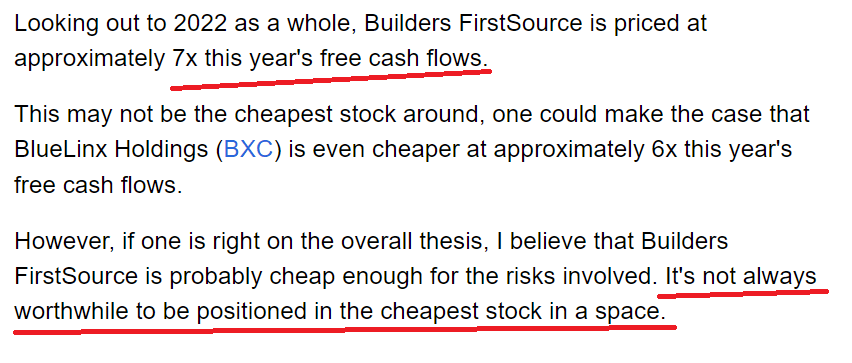

When I first recommended BLDR to you, 2 years ago, it was priced at 7x forward free cash flow, see below.

Author’s work on BLDR Author’s work on BLDR

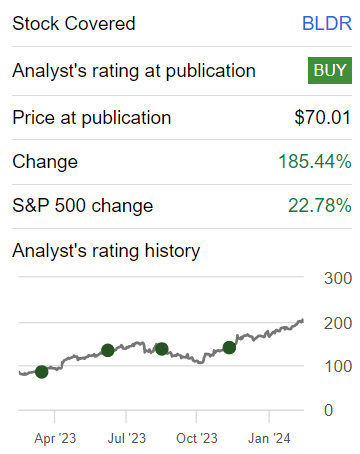

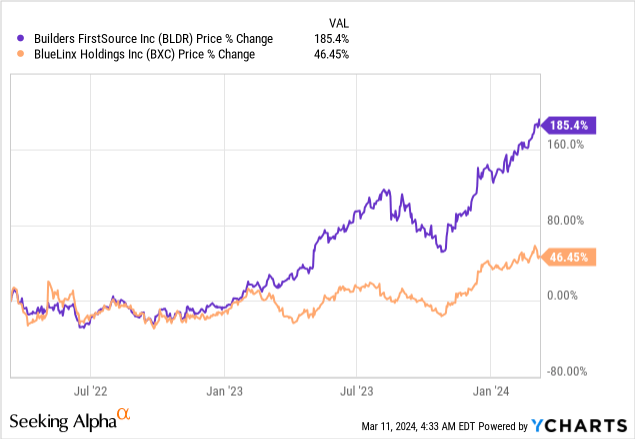

Since I’ve been bullish on this stock, it’s up 185% versus the S&P500 which is up 23%.

In fact, I was right on two occasions. I was not only right to recommend (and own) BLDR rather than BlueLinx (BXC), but even with BXC, investors would have done well.

But as you know, you can’t invest in hindsight. So, without any hindsight, I made more than 150% in two 2 years in BLDR.

But what’s next? Why am I calling it a day here? That’s what we’ll discuss next.

Why Builders FirstSource? Why Now?

Builders FirstSource is a leading supplier of building materials and construction services in the United States, catering to both residential and commercial construction projects. The company offers a comprehensive product portfolio, including lumber, trusses, doors, windows, and value-added solutions, with a focus on supporting the construction industry with quality products and services.

Its recent results, Q4 2023, demonstrate resilience in the face of a challenging operating environment. The commitment to being the easiest to do business within the industry are likely to contribute to maintaining a competitive edge.

Furthermore, its acquisitions, coupled with a disciplined capital deployment strategy, depict Builders FirstSource’s dedication to long-term value.

Despite the optimistic outlook, Builders FirstSource also faces challenges. For instance, the normalization of gross margins could end up being a drag on profitability in 2024, as the multifamily business experiences a pullback.

Given this background, let’s now discuss its fundamentals.

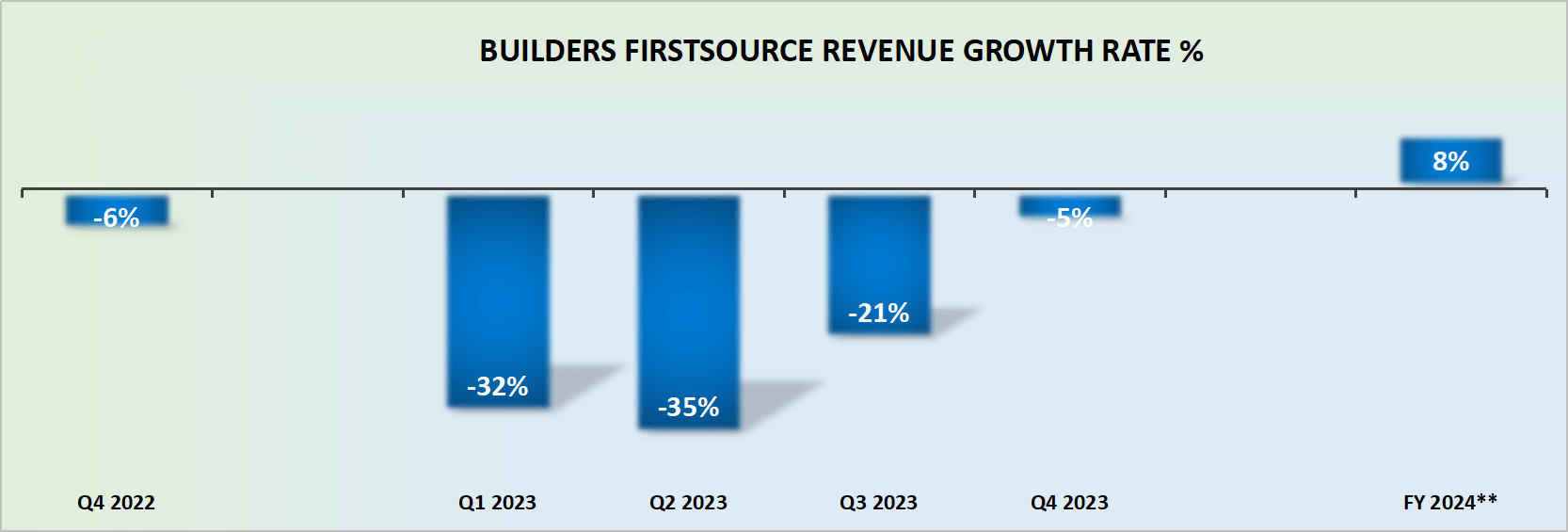

Revenue Growth Rates Point to Mid-Single Digits

BLDR revenue growth rates

BLDR’s comparables with the prior year are set very low. This means that 2024 was always expected to deliver some growth. Consequently, the fact that 2024 points to 8% CAGR is to a large extent already priced into its share price.

SA Premium

The problem with investing is that it’s not so much about the growth being better in one year compared with the previous year, but rather everything boils down to what investors were expecting. It’s all about expectations.

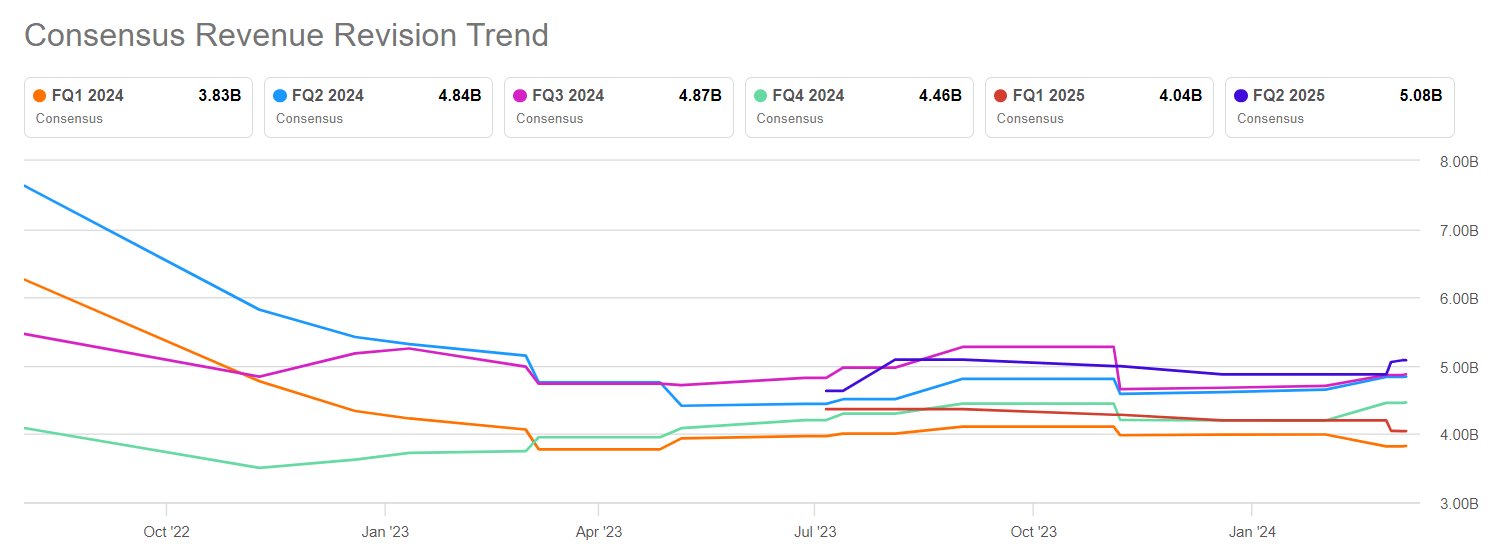

As you can see above, while I was recommending BLDR, analysts were consistently reducing their revenue estimates for BLDR. Nevertheless, I could see that analysts were too bearish and that’s why I was long this stock.

To be honest, I normally recommend that investors don’t fight the Street. By this I mean, don’t go long a stock, where analysts are lowering their revenue estimates. That’s a recipe for disaster.

And I recommend that investors don’t follow that style of investing, apart from the occasional exception. And I believe that BLDR was that one-off rare expectation. But that insight has now been priced in, therefore, the risk-reward of staying with this stock isn’t as attractive as it once was.

BLDR Stock Valuation — 16x Forward Free Cash Flow

BLDR is being super conservative with its lumber prices of $440 mbf. This will naturally allow BLDR to deliver more than $1.2 billion of free cash flow. Hence, for the sake of our discussion, let’s say that BLDR delivers $1.5 billion of free cash flow in 2024, higher than the $1.2 billion BLDR presently forecasts.

This leaves BLDR priced at 16x forward free cash flow. Clearly, that’s far from a shocking valuation, particularly when we look elsewhere in the market.

But at the same time, I have to keep in mind that BLDR already holds more than $3 billion of net debt. So, while in the past, its debt levels didn’t bother me as much, today I have to pay a high multiple to free cash flow, on top of a restrictive balance sheet.

Finally, this free cash flow estimate implies that in 2024, we’ll see BLDR’s free cash flow compressing by approximately 20% y/y. In sum, it doesn’t make sense to pay an exaggerated valuation on a stock, that’s priced as if the sky is the limit when the underlying fundamentals are starting to deteriorate ever-so-slightly.

The Bottom Line

My decision to part ways from BLDR stems from an evaluation of the current valuation and the associated risk-reward dynamics. With BLDR priced at 16x forward free cash flow and an anticipation of a 20% year-over-year compression in free cash flow in 2024, the stock seems less appealing for new investors. And if I can’t imagine new investors buying into my stock, then I shouldn’t be holding it either.

Despite the company’s past successes, a slightly deteriorating fundamental outlook could see the stock giving back a lot of my gains.

An investor is always forced to look ahead to where a business is going, not look back from where it came.

Q2 2024 Earnings Call Transcript")