OlekStock/iStock via Getty Images

Performance Assessment

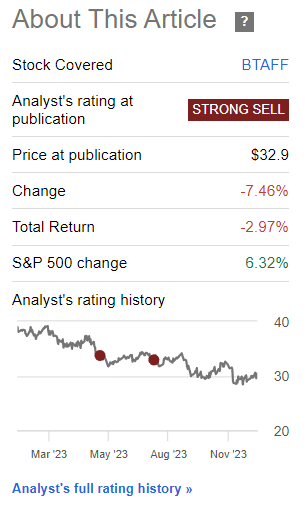

For two consecutive times, I’ve been the only bear on Seeking Alpha on British American Tobacco (NYSE:BTI) (OTCPK:BTAFF). I’ve issued a ‘Strong Sell’ rating on both of these occasions. My latest piece was entitled, “Consensus Bulls May Be Wrong Again“. The market has ruled in my favor yet again as the stock has generated -2.97% in total shareholder return compared to the S&P 500 (SPY) (SPX), which has gained +6.32% in the same period. This implies an alpha of +3.35% for the Strong Sell view compared to a long position in the market index.

Performance since Hunting Alpha’s Last Coverage of British American Tobacco (Seeking Alpha)

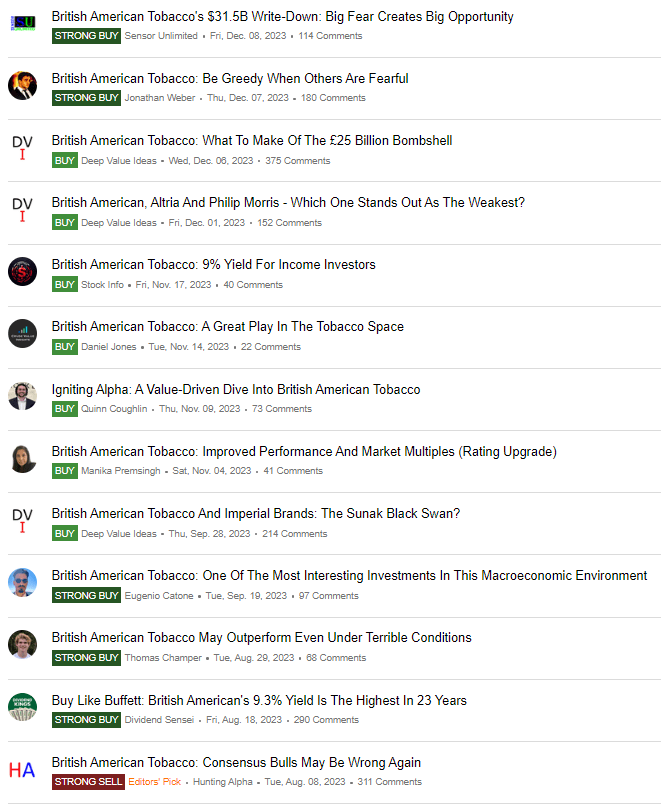

So clearly, the results show that I’ve been the only analyst who has had this right yet again as everyone else has been overwhelmingly bullish on the stock:

Consensus Bullish Views on British American Tobacco by Other Seeking Alpha Analysts (Seeking Alpha)

Thesis

In the comments section of my previous article on BTI, I’ve been asked if I had any changes in my view after the stock underperformed and fell as expected. I have consistently replied that I retain the bearish bias. Well, the same statement applies even now with a slight moderation; instead of a ‘Strong Sell’, I now declare BTI a ‘Sell’. Please see the last section of this article to understand how to interpret the difference in these stances.

I am still bearish BTI due to these views:

- US Combustibles continues to post disappointments

- BTI is at the mercy of slow-moving and unaligned regulatory bodies

- BTI has a poor diversification strategy that forces it to swim against powerful currents

US Combustibles continues to post disappointments

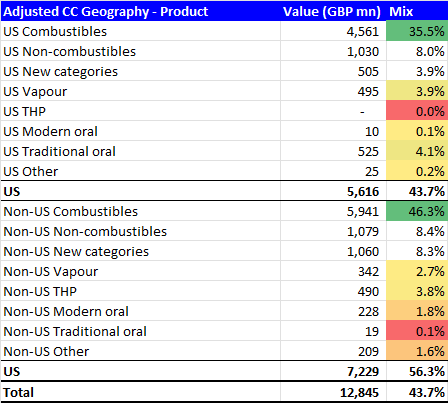

British American Tobacco – Key Revenue Drivers (Company Filings, Author’s Analysis)

As a reminder, US combustibles make up almost 36% of the overall revenue mix. In the H2 FY23 Pre-Close update, the company took a £25 billion ($31.5 billion) impairment charge on acquired US combustible brands as they cut down the useful life assumptions on these assets:

mainly relates to some of our acquired U.S. combustibles brands, as we now assess their carrying value and useful economic lives over an estimated period of 30 years.

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall

Following this was a revenue guidance update pointing toward the lower end of the previous range:

due to the continued weakness of U.S. combustibles, we now expect to deliver group organic revenue growth at the low end of our 3 to 5% guidance range.

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall, Author’s bolded highlights

From a microeconomic market share perspective as well, BTI’s woes continue as they admitted to combustibles value share dropping 40bps in H2 FY23. This was only partially offset by stronger performance in non-US combustibles. Partially, not fully. So overall, management is saying they lost value market share in their main market of combustibles.

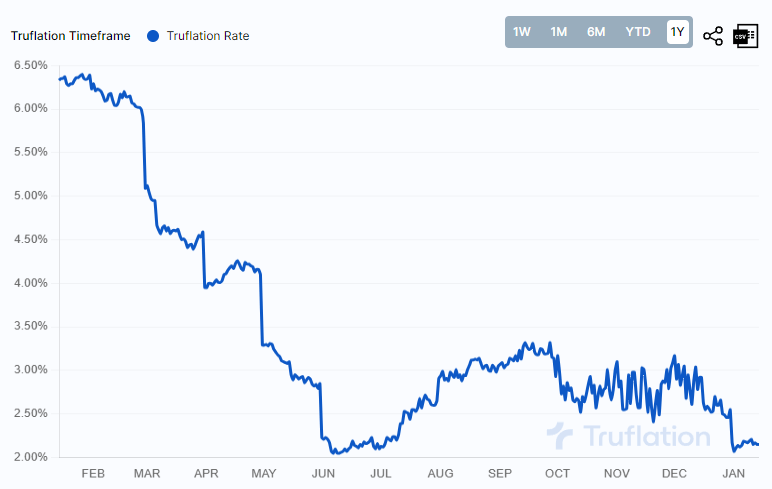

Why have US combustibles performed poorly? Well, last time management blamed inflation:

And at the same time with massive inflationary pressures that put a lot of pressure in terms of consumer purchase power.

– CEO Tadeu Marroco in the H1 FY23 earnings call

Incrementally, data shows that inflation has not changed so much since H1 FY23:

US Inflation Rate YoY – Real-time estimate (Trueflation)

The inflation data reported by Trueflation is arguably a more real-time measure of the inflation rate in the US economy.

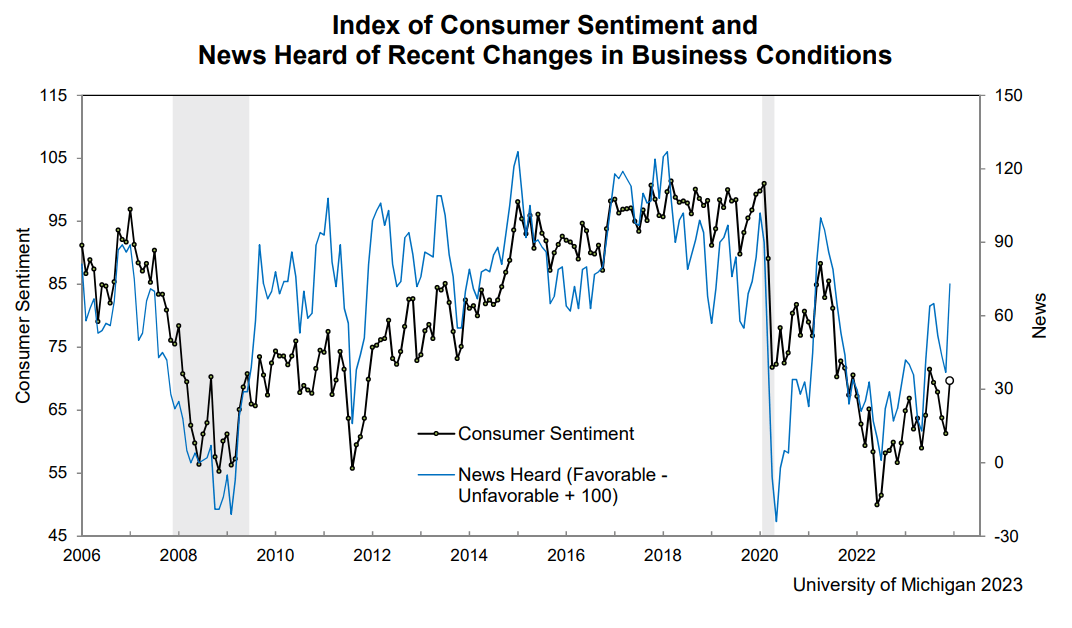

This time, they point to other macro drivers such as high interest rates and consumer confidence:

…the scenario will now improve once the macroeconomics get better, which means interest rates and such coming down, consumer confidence starts to go up, and then it will be anybody’s guess when this will start happening – some people are saying that is more towards the second half of 2024. That’s why I’m also saying that we expect that most of the year we’ll be seeing still a lot of pressure from the consumable point of view, and we start seeing some green shoots more towards the end of ’24.

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall, Author’s bolded highlights

Let’s employ some critical thinking here: will higher interest rates really influence consumer behavior so much for a low-ticket addictive product like nicotine? Keep in mind that BTI is positioning itself more and more on the value end of the cigarette spectrum as well. As for consumer confidence, the data actually shows it to be rebounding quite strongly:

University of Michigan Consumer Sentiment Index (University of Michigan)

So I am still skeptical about the macros being such a big reason for underwhelming US combustibles performance. I believe changes in consumer buyer patterns are a big driver as people either quit smoking or move to substitutes such as e-cigarettes. Indeed, management indicated that the illicit disposable e-cigarette category is cannibalizing regular combustibles:

These illicit modern disposals though is having more and more impact on Combustibles as well.

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall

In any case, these macro-related headwinds and substitution effects would impact the entire combustibles market, not just BTI. So it does not explain why BTI lost market share. I hope management expands on this in the H2 FY23 earnings call.

So far, the outlook is not a bright one for US combustibles:

While returning our U.S. Combustibles business to consistent value growth will take time, we are confident that the actions we are taking will strengthen our portfolio over the longer-term.”

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall, Author’s bolded highlights

I question what longer-term actually means here as this is clearly a sunset industry.

BTI is at the mercy of slow-moving and unaligned regulatory bodies

Vapour e-cigarettes make up the largest piece in the New Categories segment of BTI, contributing a 6.5% mix to overall revenues as of H1 FY23. This market is facing heavy pressure from the supply of illicit products. For example, more than 60% of vapour revenue is estimated to come from illicit disposable e-cigarettes in the US. And BTI is at the mercy of the US Food & Drug Administration (FDA) to do something about this:

…enforcement from the FDA on these modern disposables because, if this happens, it will not just help with the Vapour glo system where were are present, the legal part of vapour, let’s put it that way, it will open up a big white space because, today, we believe that £6bn out of £10bn Vapour revenue, more than £6bn is coming from these modern disposables

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall, Author’s bolded highlights

However, a saving grace from the FDA is unlikely according to industry experts:

The FDA moves at a ponderous pace and the industry knows that and exploits it… Time and again, the vaping industry has innovated around efforts to remove its youth-appealing products from the market.”

– Dr. Robert Jackler of Stanford University, who has studied the rise of disposables

Recently, the US is moving toward a ban on menthol cigarettes in an effort to control illicit supply. This is harmful for legitimate players such as BTI too. Note how BTI CEO laments the ban:

It seems that they have taken a right blank approach in terms of menthol, denying all products, they haven’t approved any products of menthol, which is very frustrating to say the minimum because this goes against even their belief in terms of risk continuing and migrating consumers out of cigarettes, they just make this more difficult.

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall, Author’s bolded highlights

This is clear proof that BTI is powerless and at the complete mercy of regulatory authorities’ decisions, which go against their interests. The bad news for BTI continues as there is recent talk about the banning of flavored e-cigarettes by the World Health Organization (WHO). This will pose a serious threat to BTI’s entire diversification strategy:

BTI has a poor diversification strategy that forces it to swim against powerful currents

BTI’s has its main business is in combustibles, which is a declining industry fraught with many regulatory hurdles and challenges. Given this, I can’t see how diversifying into related and arguably only a bit less unhealthy, but overall still harmful products is a good idea. It doesn’t address the root cause, which is nicotine, and the world’s ever-growing negative sentiment toward it.

Hence, it is not at all surprising that BTI is facing the exact same challenges relating to changing consumer preferences and fighting regulatory challenges every step of the way. With a poor diversification strategy that forces it to always swim against the currents, I predict that we will see a lot more of these kinds of comments in BTI going forward:

challenging the Marketing Denial Orders received for Vuse menthol variants, including most recently for Vuse Alto

– CEO Tadeu Marroco in the H2 FY23 Pre-Close Concall

What should BTI have done instead?

I think we can look toward the Indian cigarette market leader ITC as a fine example of what successful diversification looks like; ITC had 87% of its revenues coming from cigarettes in FY16. Now over the LTM, this has almost halved as the mix stands at 47%. The company has successfully diversified into FMCG, agricultural commodities, hotels, and the packaging industry. These are attractive growth areas, particularly in India and importantly, there is no fight against regulation every step of the way in these markets. BTI has a >25% stake in ITC but it has not managed to adopt a similarly successful diversification strategy.

Of course, such diversification into new categories unrelated to the nicotine business may have been very difficult to achieve. In this case, I think the next best thing would have been to ride out the combustibles for as long as possible and return even more capital to shareholders. This may have been a better capital allocation decision for shareholders since BTI’s return on invested capital has fallen from a healthy 16.6% to below 8% over the last 10 years.

Valuation

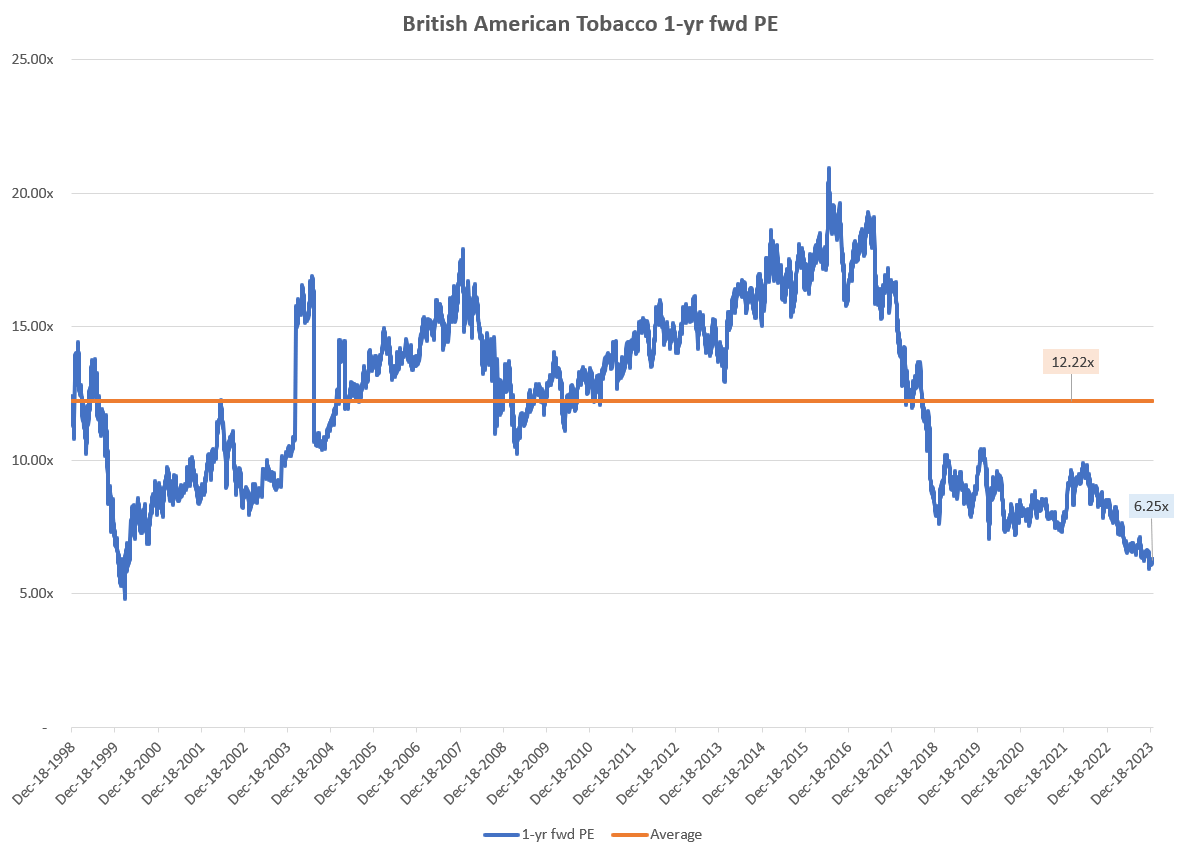

BTI 1-yr fwd PE (TradingView, Author’s Analysis)

Trading at a 6.25x 1-yr fwd PE, The discount to the longer term 1-yr fwd PE multiple of 12.22x now is still large at 48.8%. But the discount was around the same levels at 46.1% in August 2023. Yet, the stock continued to not only underperform the S&P 500 but generate a negative total shareholder return. I think this is clear evidence of what I had contended earlier: BTI is a value trap. I don’t see a compelling case for buys until a small miracle happens, which I discuss now:

Key Risks and Monitorables

I don’t think BTI will find meaningful support from the buyers unless regulatory bodies start to meaningfully help curb illicit e-cigarette sales, lifting the bans and allowing companies such as BTI to sell their products. This is the key incremental driver that may provide BTI with some relief from the selling pressure and allow for a short-term rally in the stock.

Takeaway

I’ve been the only Seeking Alpha analyst who’s been right on British American Tobacco 2 times out of 2, with a high conviction ‘Strong Sell’ rating each time. Since the publication of my last article on the stock, BTI has generated -2.97% in total shareholder return compared to the S&P 500, which has gained +6.32% in the same period. This implies an alpha of +3.35%.

I am still bearish on the stock as the main business of combustibles, especially in the US, continues to post disappointments prompting lower-end guidance revisions by management. From a market positioning perspective, BTI is losing out on value share.

The illicit supply of e-cigarettes is a major headwind for BTI’s New Categories. Here, the company is at the mercy of slow-moving and unaligned regulators for getting more desirable operating conditions.

I think BTI’s diversification strategy into other nicotine products is poor as it forces the company to continually encounter resistance and fight regulatory bodies every step of the way. Indian cigarette maker ITC is a beautiful exemplar of successful diversification for a nicotine-related company.

As I had expected in my last article, the stock remains a value trap. I don’t anticipate the sell inertia to change unless, by some small miracle, regulatory bodies start to align and aid BTI’s interests. For now, I rate the stock a ‘Sell’. This is a slight change from the ‘Strong Sells’ earlier since I believe a lot of bad news and headwinds have already hit the stock.

I understand many BTI shareholders hold it for the dividends. I focus on total shareholder return as I believe that is what matters to overall net worth. However, for dividend-focused plays, I believe Annaly (NLY) and SCHD (SCHD) are better options.

Rating: ‘Sell’

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher-than-usual confidence

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher-than-usual confidence

The typical time horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")