Richard Drury

We previously covered British American Tobacco p.l.c. (NYSE:NYSE:BTI) in January 2024, discussing the management’s great success in renewing its tobacco portfolio, with the New Categories segment boasting an accelerated top-line growth well-balancing the secular decline of the conventional cigarettes segment.

With the worst of the secular decline baked in and the October 2023 bottom holding post-write-down, we believed that the discounted levels offered a highly attractive forward yield for dividend-oriented investors looking to buy and hold indefinitely.

Compared to the wider market at +12.8%, BTI has moderately recovered by +4.2% since the painful write-downs, as we examine its detailed financial performance in FY2023.

For now, BTI has exceeded expectations by reporting the first year of positive margins for the New Categories segment, further aided by the growing Free Cash Flow generation and healthier balance sheet.

We believe that it is only a matter of time before the stock’s valuations are upgraded, triggering a great upside potential. For now, thanks to the rich forward yields, investors may simply dollar cost average while being paid to wait.

BTI Continues To Offer A Compelling Investment Thesis For Opportunistic Tobacco Investors

For now, BTI continues to offer a compelling tobacco play, attributed to its successful transition from conventional cigarettes to the non-combustible segment thus far, especially observed in its highly definitive FY2023 earnings results.

As discussed in our previous article, we maintain our belief that the massive combustible write down has revitalized its balance sheet while highlighting the management’s confidence about its New Categories segment.

For example, BTI reported robust growth in the New Categories segment revenues at £3.34B (+17.8% YoY) and increasing volumes sold for the Vapour product at +7% YoY, Heated Products at +11.6% YoY, and Modern Oral at +34.4% YoY in FY2023.

These numbers naturally balance the secular decline observed in the Combustible revenues at £22.84B (-0.8% YoY) and volumes at -4.8% YoY, as more “smokers continue to switch to smokeless products.”

BTI’s New Categories segment has also achieved Profit from Operations of £17M (+104.6% YoY) with positive margins of 0.5% (+14.2 points YoY), two years ahead of its original target.

While there is still a great distance from its top/ bottom line driver, the Combustible segment at Profit from Operations of £12.54B (+4.5% YoY) with positive margins of 52.3% (+3.9 points YoY), it is apparent that the cash burn is behind us.

This has naturally triggered the company’s overall Profit from Operations of £12.78B (+3.1% YoY) with margins of 45.6% (+0.4 points YoY).

The most important metric of all, BTI’s Free Cash Flow generation, remains robust at £8.36B (+3.9% YoY before dividends) with expanding margins of 37.6% (+1.9 points YoY), implying its ability to consistently return value to existing shareholders while paying down debt.

For context, the tobacco company has reported a lower long-term net debts of £33.94B (-10.9% YoY) and healthier balance sheet with moderating net-debt-to-EBITDA ratio of 2.6x in FY2023, compared to 2.9x in FY2022 and 3.5x in FY2019.

This is compared to its peers, Phillip Morris (PM) at 2.68x, Altria (MO) at 1.86x, and the average tobacco industry at 2.47x.

With BTI still guiding a cumulative Free Cash Flow generation of £40B before dividends over the next five years, we believe that its dividend investment thesis remains robust, significantly aided by the immense upside potential given its inherent undervaluation.

Finally, the management is notably lifting a page from MO’s playbook, in selling the ITC stake to potentially resume its share repurchases, which has been relatively minimal since the last big repurchase at $2.09B in FY2022.

As a result of the recovering market sentiments, we believe that BTI has promising prospects for the future.

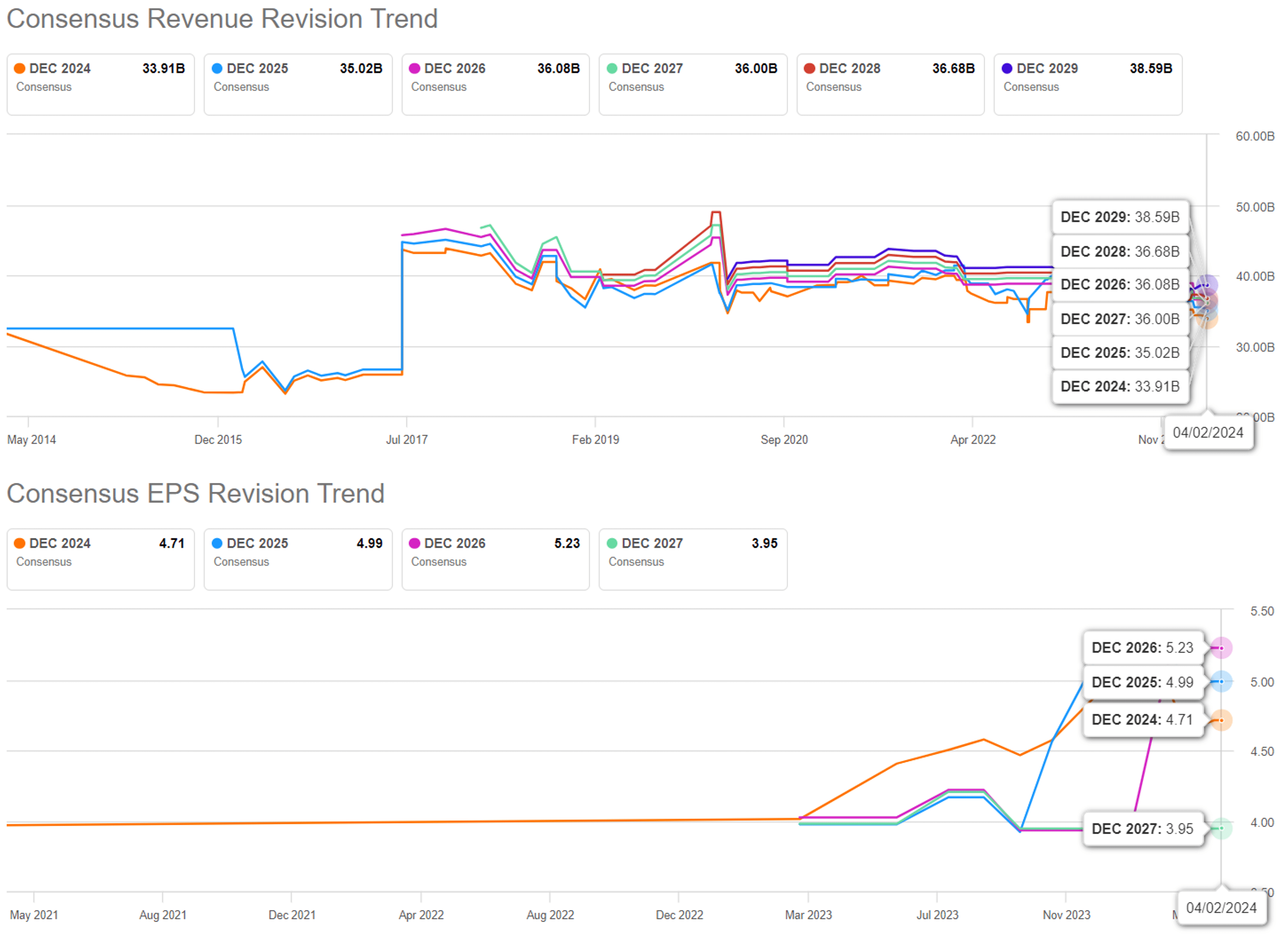

The Consensus Forward Estimates

Seeking Alpha

The same optimism has been reflected in the consensus forward estimates, with BTI expected to generate an accelerated bottom line expansion at a CAGR of +3.3%, despite the slower projected top-line growth at +1.8%.

This is compared to the previous top/ bottom line estimates of +4.6%/ -6%, while building upon the historical growth of +9.2%/ +6.2% between FY2016 and FY2023, respectively.

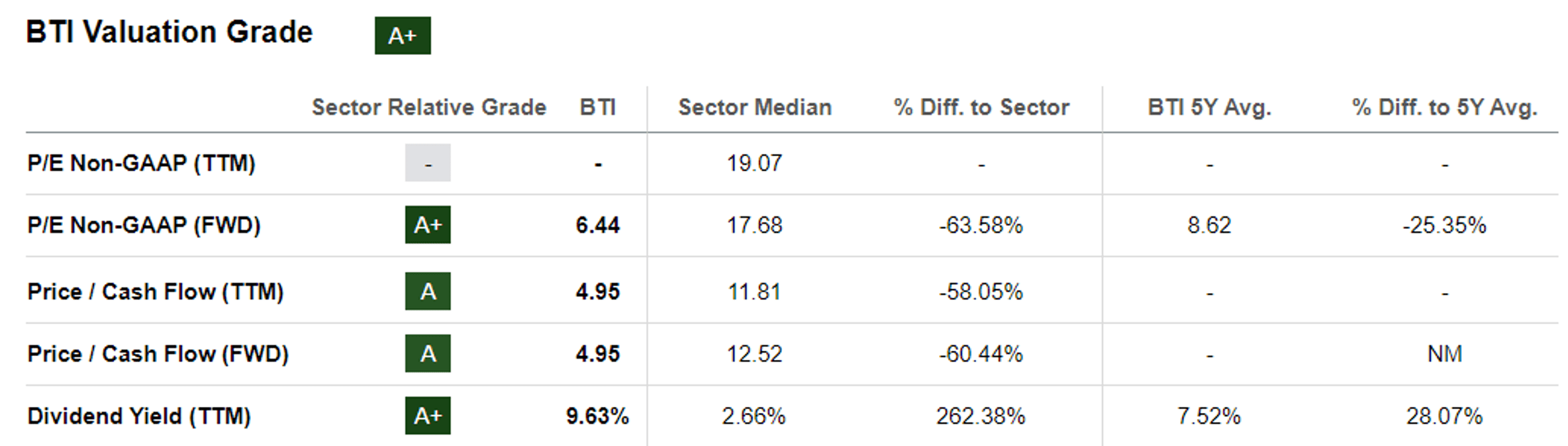

BTI Valuations

Seeking Alpha

And it is for this reason, that we believe BTI is currently trading at discounted valuations of FWD P/E 6.44x and FWD Price/ Cashflow 4.95x, compared to the post write-down levels of 6.92x/ 4.92x, its 2022 mean of 8.44x/ 7.10x (pre-write-down), and 3Y pre-pandemic mean of 13.02x/ 12.51x, respectively.

The same is observed when compared to its tobacco peers, such as PM at 14.41x/ 12.70x and MO at 8.55x/ 8.49x, respectively, offering interested investors with a great upside potential assuming an upward re-rating in BTI’s valuations.

We believe that the market is getting wrong with this one in creating this buying opportunity, since BTI has already achieved positive contributing margins for the New Categories segment, as the second runner up to PM with MO still far behind.

For context, PM reports successful monetization in the smoke-free segment, with it already accretive to its profitability at “over 40% of gross profit, with the adjusted gross margin rate on smoke-free surpassing combustibles for both the quarter and year.”

With BTI already achieving this break-even goal two years earlier than expected, we believe that the same bottom-line outperformance may be expected ahead, especially with Vuse is still leading the US market at 42.2% (+0.2 points MoM) for the four weeks ending February 24, 2024.

However, readers may want to monitor the potential risks from PM’s IQOS 3 launch in the US from Q2’24 onwards and the IQOS ILUMA from 2025, since it may trigger headwinds to BTI’s dominance in the vaping market.

This is given PM’s global expertise in the smoke-free approaches, with growing sales volume as the management completes “the global rollout of ILUMA” with the last market being the US, after the recent settlement between PM/ BTI and the reassignment of the US IQOS rights from MO.

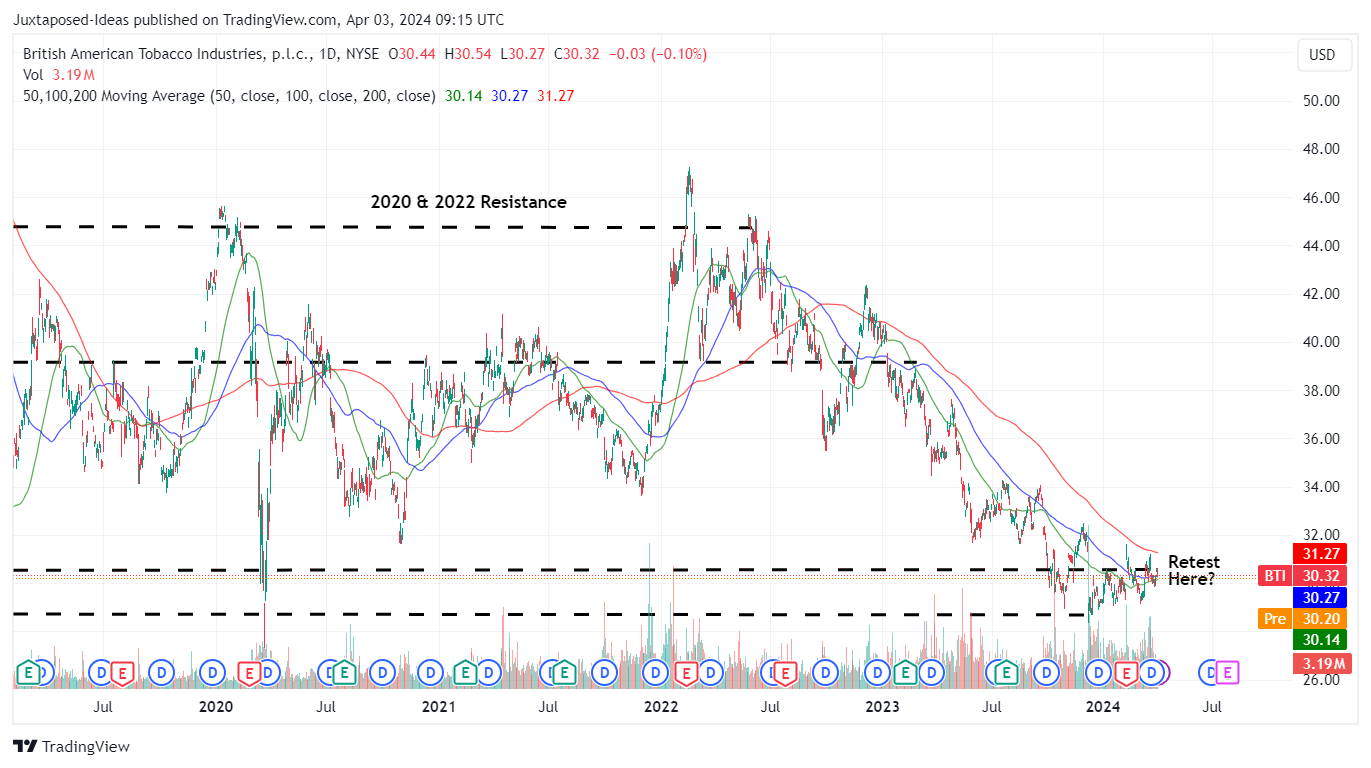

So, Is BTI Stock A Buy, Sell, or Hold?

BTI 5Y Stock Price

Trading View

For now, BTI has moderately recovered by +4.2% since the painful write downs, with the stock appearing to retest its previous resistance level of $30s.

Based on the FY2023 adj EPS of $4.74 and the FWD P/E valuations of 6.44x, the stock appears to trading near our fair value estimates of $30.50.

At the same time, we are confident about BTI’s potential upward re-rating in P/E valuations to the 2022 mean of 8.44x (pre-write-down), given the successful monetization of its smoke-free approaches and the accretive impact to its overall profit growth.

Based on the consensus FY2026 adj EPS estimates of $5.23 and an upward re-rating to its 2022 P/E mean of 8.44x (pre-write-down), there seems to be an excellent upside potential of +46.4% to our long-term price target of $44.10 as well.

This is on top of BTI’s expanded forward dividend yield of 9.63%, compared to its 5Y mean of 4.81%, PM at 5.66%, and MO at 9.13%, thanks to its discounted valuations, the recent correction, and the recently raised payouts by +6.1%.

As a result of the dual pronged returns through (prospective) capital appreciation and dividend incomes, we are maintaining our Buy rating for the BTI stock here.

Be paid to wait the great upside.

Q2 2024 Earnings Call Transcript")