Michael M. Santiago/Getty Images News

British American Tobacco (NYSE:BTI) reported a disappointing trading update on Wednesday, with the stock taking a 9% hit as we write.

A few highlights (or rather lowlights)

– Revenue growth will be at the low end of their 3-5% organic revenue growth range. The company reported losing combustible market share of 100 basis points to 18.2%. Japan and Italy were cited as especially competitive markets. In the US, the first half was stable but in the second half management said that volumes weakened.

– Organic revenue and EPS growth in 2024 is now expected to be low single digits. With Street estimates of 3% revenue and EPS growth next year, earnings will get revised down. Management is accelerating their investments in US products and growth. Along with continued inflation, EPS growth will be limited.

– The California menthol ban has led to 80-90% retention rates (that is 80-90% of menthol smokers have opted for other products). This is a bit lower than we expected. A full US ban of menthols is still on the table at some point and has been an overhang for months now.

– Goodwill will be impaired by £25 billion, an eye-popping figure that has garnered a lot of headlines. This mostly related to the company’s Reynolds acquisition in 2017. Total intangible assets were £122 billion as of June 2023, with Reynolds accounting for £37.18 billion. Last year, management maintained that their Camel and Newport brands intangibles should be kept on the balance sheet indefinitely. Now, BTI will amortize these over 30 years. While a perhaps worrisome statement that these brands have a finite life, the incremental amortization expenses can be used to reduce their taxes and so is beneficial to free cash flow.

– The US FDA continues to withhold approval for BTI’s flavored vaping products. These have been shown as the most effect with which to convert smokers. The company expects little action in 2024 on this front however.

Ok, with the bad news out of the way, there were several positives.

– EPS growth guidance remains intact this year and likely ends up around £3.77, or $4.77 in US dollar terms at current exchange rates.

– Leverage will be 2.7x on a debt/EBITDA basis by year end. With a goal of 2.5x, the company should be able to resume share buybacks in 2024 in the second half per our model.

– Non-combustibles have improved from £1.1 billion in losses and now are “expected to be breakeven in 2023.” These products could easily be higher margin once scaled given the generally lower excise taxes on them compared to cigarettes.

– Combustibles outside the US are performing well.

– The company continues to target 100% of net income convertible into free cash flow. With a payout ratio of 58%, we see little risk to the dividend.

– The company aims to have 50% of its revenue from non-combustibles by 2035. Vuse, Glo and Velo are growing by 25% approximately.

ITC Corporation Stake

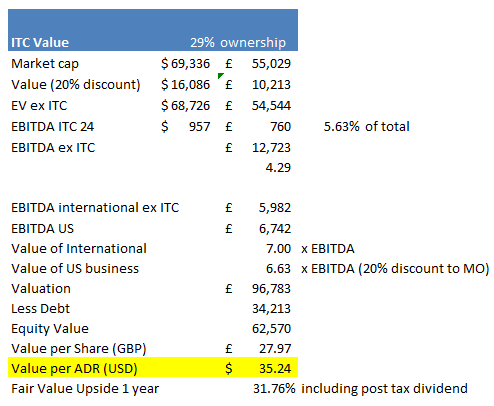

Finally, management alluded to looking at disposing “non-strategic geographies” which we think is a clear reference to monetizing their 29% stake in ITC (ticker ITC IN in Bloomberg).

ITC has a £55 billion market cap implying £16 billion of value there to BTI (and only about £760 net of EBITDA on 2024 estimates, or about 6% of BTI’s total). Any divestiture would be complicated by Indian regulations (notably foreign direct ownership laws on tobacco stakes), but a partial monetization to a local Indian company seems quite doable in time. Importantly, can BTI use their £25 billion goodwill write offs against a £17 billion gain on a divestiture? We would love for any tax specialist to weigh in here.

The net valuation in a spin/sale implies that BTI is trading at 4.3x on an EV/EBITDA basis proforma. MO trades at 7.8x 2024 EBITDA and PM trades at 11.8x. We included a 20% discount to their stake for tax leakage/liquidity discount.

That seems really cheap, more below.

Market In reject

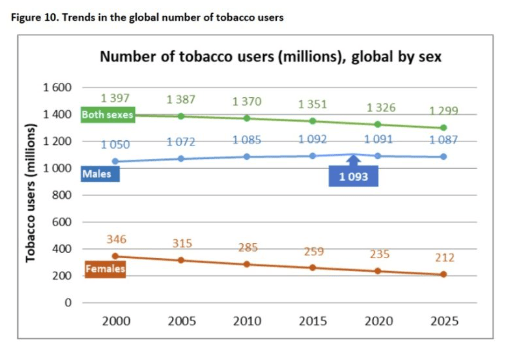

Clearly volume pressures have worsened in the US in 2023. The California menthol ban, lost market share and macro pressures are taking a toll. According to BTI management, there are 1 billion users of tobacco globally, with 100 million of these using non-combustibles. 60% of non-combustible users vape and the other 40% use heat not burn products or pouches. BTI seems to be having more success on the vaping side.

Below are global trends from 2000 to 2025 (estimated of course).

Health policy watch

Overall though, as we eyeball the above chart, we are not seeing any step change in global usage (down 0.26% annually from 2000 to 2020).

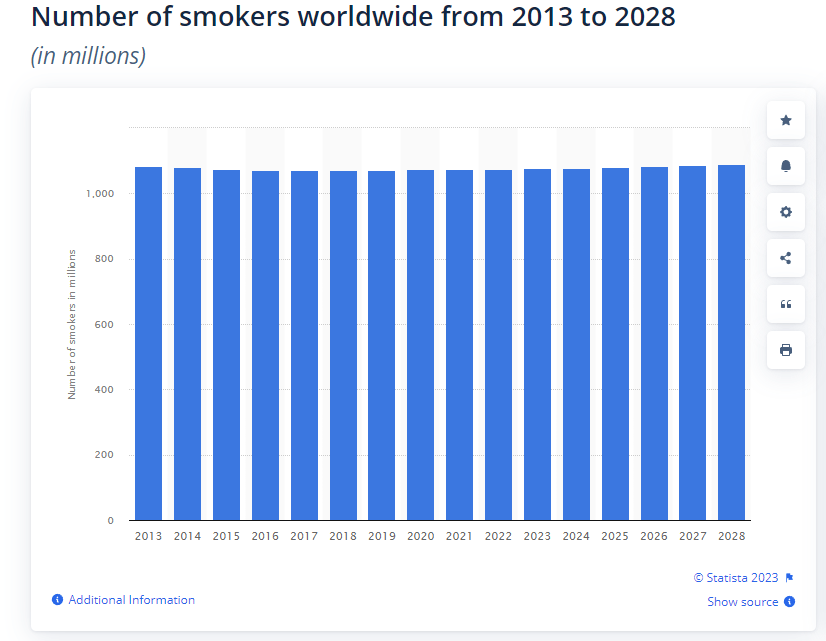

Statistica forecasts growth in tobacco usage through 2028. This chart is dated July 2023.

Statistica

While we have no idea where volumes end up, we are not seeing a dying/decaying business worthy of trading at 6x earnings.

Today, BTI has 17% of its revenue from non-combustibles and Philip Morris International (PM) has 35%.

The business may be under pressure, particularly in the United States. But we see a lot of people who admire to consume nicotine and probably will continue to do so. With safer methods of administering nicotine, there arguably will be a steady state level of consumption reached even in the US at some point.

Globally many forecasters think we are already there but our view is that investors will likely see pressures in the US for the next year or two before easing. There should be a US menthol decision next year.

Valuation

PM trades at 15x forward earning and is expected to grow 6% next year. Altria (MO) trades at 8x forward earnings and is expected to grow 2.1% next year (which figure probably gets cut as Altria is all US based). BTI at 1-2% growth resembles MO, but with overseas exposure should in the long run help its growth and valuation (as volume and regulatory pressures are highest in the US).

So BTI, with about half of its profits overseas and half in the US, arguably should be worth some kind of blended multiple. But with the cut to growth guidance, perhaps a MO multiple is the best we can expect here.

Below is the sum of the parts math assuming a monetization of ITC.

Author spreadsheet

Note the discounts we used above, with the US business valued at 6.6x EBITDA (20% cheaper than MO given potential menthol headwinds).

We also discounted BTI’s ITC stake by 20% for liquidity reasons/tax leakage.

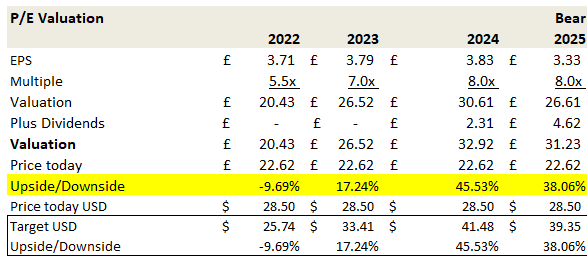

Should BTI be able to reach their 3-5% organic revenue growth target in 2026, with tough menthol ban comps lapsed, the stock could easily rate back to 8-10x earnings.

Author spreadsheet

At 10x, BTI would be worth in the mid $40s on the ADRs, close to where it traded just 18 months ago.

Should the US enact a full menthol ban, we calculate that retentions rates at 85% would result in lost profits of £850 million, a 10% hit to EPS. At 6x, BTI could fall to the mid $20s. With that uncertainty behind the company, however, a higher multiple seems likely. Said differently, this could already be priced in and most already expect a US ban at some point. But a 10-15% drop on an outright ban with no flavored vaping product approval could be possible.

Conclusion

We struggle to see material downside to BTI from current levels, but do worry about a menthol ban. While it seems priced in to the stock, the uncertainty looms. In the near term, the company also mentioned that the first half will be weaker than the second half next year, so the penalty box could be rather elongated for BTI.

Furthermore, volume or market share losses could mean that 2024 earnings miss their preliminary guidance for the year. The jury is also still out on their new CEO, Tadeu Marroco who started last May. Perhaps the goodwill impairment and reduced guidance is his way of kitchen sinking expectations.

More likely, the transition to non-combustibles amidst inflation and heightened US regulatory actions have taken a toll on growth. In time, these likely will ease. Marroco was considered a pretty solid CFO for the two years in that role, and he has been at the company since 1992.

All this being said, we still consider Philip Morris to be the highest quality tobacco name. With better geographic exposure and product mix, it is obvious in the valuation and organic growth figures that it is the first name that an investor should consider in the space.

But at $28, there is certainly a place for the patient investor to own a position in BTI. With a 9% yield that is well covered, we don’t need capital appreciation to relish solid returns. We put a $24 to $45 range on BTI shares in the next 3 years.

Q2 2024 Earnings Call Transcript")