baona

Dear readers,

Branicks (OTCPK:DDCCF), formerly known as DIC Asset, is a relatively small German company which essentially operates as a combination of a REIT and an asset management business.

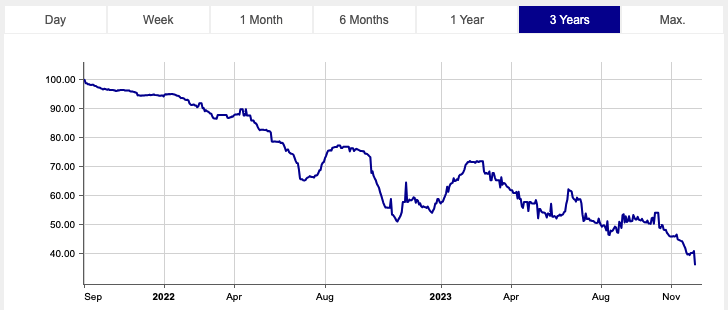

I’ve covered the stock before (here), explaining the basics and calling the investment “Speculative, but potentially rewarding“. Since my last article in April, there have been several (mostly bad) developments, which have resulted in a advocate sell off and the stock now trades at just EUR 3.50 per share.

The stock is priced at a substantial discounted to book value and its 2026 bonds trade at just 35 cents on the dollar, suggesting that bankruptcy is a real threat here.

Frankfurt Stock Exchange

I continue to see a way out of this for Branicks, but recognize that the situation is serious and there isn’t a lot of time left for Branicks to raise the liquidity it needs to address its debt maturities.

The stock has recently been downgraded by S&P Global to B+ and advocate downgrades are possible if management doesn’t deliver on their forecast of EUR 200-300 Million of inflows.

The business

Recall that Branicks operates in two business segments, that can each be valued individually and that complement each other quite well.

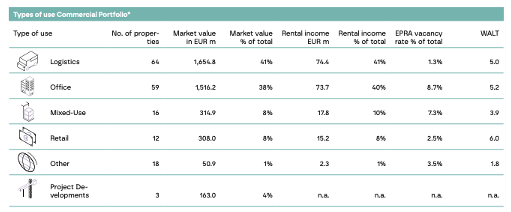

The first is a traditional commercial portfolio, which Branicks owns outright and operates. The portfolio has a book value of around EUR 4 Billion and consists of 41% of recently acquired logistics space, followed by 38% of office space, 8% of retail and 8% of mixed-use.

The portfolio continues to perform well with high occupancy – 98.7% for logistics and 90%+ for office. Moreover, leasing over the first three quarters of the year has been decent and rents have increased by 3.5% YoY, primarily due to inflation-related indexation.

Branicks Presentation

I appreciate most of the properties in the portfolio, but I have a problem with the EUR 4 Billion valuation. Management expects the book value to drop by 4-7% as a result of year-end revaluation, but I actually think that the current fair value is much lower than that.

The reported book value assumes very aggressive cap rates of around 4% for both the logistics space and office. With the 10-year USD treasury yield at 4.50% and the EUR yield at 3.35%, I find it hard to preserve such aggressive cap rates. If we use cap rates that are in line with what peers such as Prologis (PLD) or Boston Properties (BXP) trade at, we get fair value of the commercial portfolio of (at most) EUR 2.5-3 Billion.

Moving to the asset management business, this segment provides major synergies for the commercial portfolio, because it essentially allows Branicks to offload properties that it doesn’t want to own out-right. Therefore, it allows Branicks to raise liquidity. This is a key reason why I continue to believe that Branicks can create the liquidity it needs, despite the transactional market still quite frozen. And it’s not just theoretical, either. As of earlier this year, Branicks offloaded nearly half a Billion of retail properties into the asset management business.

Assets under management, which consist almost entirely of institutional money, have been fairly stable at EUR 10 Billion and so have base management fees that average about 0.5%. Because of low transaction volumes, however, Branicks’ performance and transaction fees have been zero so far this year.

The asset management segment has its place in the business model, and I quite appreciate that management clearly stated that it has no plans of selling it. But from a fair value standpoint, I assess that the segment is only worth about EUR 0.5 Billion, because of very high OPEX which consumes nearly all base fees and because of low performance fees.

I assess the fair value of Branicks’ assets around EUR 3-3.5 Billion, which is about EUR 300-800 Million in excess of net debt.

Obviously, because Branicks is so heavily leveraged, any sort of improvement in cap rates will translate into huge gains in the value of equity and therefore the stock price. But high leverage comes at a cost.

Risks

Branicks is a risky bet.

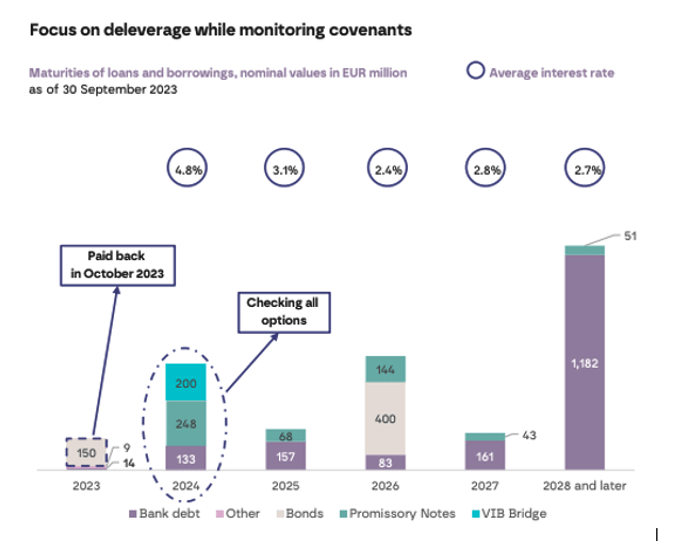

The company has about EUR 120 Million in cash and will have to cover debt maturities of EUR 600 Million next year alone. And while it may be able to refinance (at least part of) the bank loans worth a total of EUR 133 Million, it’s very unlikely that it will be able to refinance the rest.

That means that Branicks needs a significant liquidity boost soon.

Branicks Presentation

There are several solutions here.

Firstly, the company can (and will most definitely try to) sell some of its real estate assets on the open market or to the asset management business. Though these sales would likely take place below book value, it would allow Branicks to create the liquidity it needs and still be a (big) net positive for shareholders.

Secondly, with a market cap of just EUR 250 Million, Branicks is a potential target for a buy-out. The assets are worth more that the debt, so a much bigger player could come in, take over Branicks and repay the debt.

It remains to be seen whether management will handle to steer the situation or not.

Bottom Line

Branicks has been a speculative investment for me from the start. And there are significant risks here if Branicks fails to raise liquidity over the next 6 months. At the same, the potential reward if they do is massive (think 3x).

I rate the stock a HOLD and propose that anyone interested in Branicks common shares considers also the bonds, which furnish 300% upside to par value and rate higher in the capital structure compared to common shares.

Note that we are currently working on a more detailed review of Branicks for High Yield Landlord.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")