D. Lentz

Above: The Vegas downtown market BYD properties are doing well but have been disrupted by construction. That is mostly past now.

The massive proliferation of data and constant hash and rehash of metrics and analysis that accompany the coverage of securities today compels savvy investors to extend their need for more diverse sources to support decisions. Add to that the oncoming rush of AI applications to further speed and refine stock data and you have the danger of TMI blurring it all to confusion. The state of play then needs what is already available from bulge analysts, to notable investing gurus and data generated from companies earnings releases for certain.

With such a plethora of data available to so many people at the same time, investors need a much broader information base to discover for themselves, alphas that may lie outside the traditional sources of stock data.

With that in mind, we often stress that our reports on stocks in the two main sectors we cover: casinos/sports betting and media entertainment always bring another dimension – appraisals of management quality or lack of same.

The best analogy we can think of lies in professional sports. You place your bets on a game based on odds constructed out of the prior wins and loss records of the teams. You place higher value on teams with proven rosters of the best players position by position. You consider offense, defense and overall past performance under pressure.

And then you toss into the calculation the presence of the head coach or manager. You build a betting thesis as to whether that leadership will contribute to the possibility of a win and to what extent it will do so. The truth as we have learned is that of the four major professional sports, the one where a superior head coach can really make a difference on what happens on the field, is the NFL head coach. Not in MLB, NBA or NHL does the coach factor in the outcome anywhere near what it does in pro football.

Having been part of senior management in the gambling business for over 35 years I have come to understand the complexity of skills what ultimately comprises a casino that over performs. And there is where higher valuations of their shares are born and pose stronger returns for investors.

Over these many decades in the business, I have concluded that the difference between a meh, conventional management skill set vs. one with smarts across the strategic and operational decisions is worth at least +15% in an upside or (15%) downside value of a gaming stock.

Boyd Gaming: Superior top management smarts centered in how they have allocated and continue to allocate capital

Boyd Gaming (NYSE:BYD) is a company sprung out of the gene pool of early entrepreneurs of Nevada who began their businesses out of an instinctive grasp of how to make gamblers happy. Most of them came to Las Vegas because in the early days of the 1960s and 1970s they saw visions of what would happen in the decades ahead once the town had publicly traded casinos and had rid itself of its early nefarious founders.

Among them was Mr. Sam Boyd and his heirs who started with Sam’s Town in 1975 and over time built a consumer friendly operation that eventuated in the multi-billion dollar company we know today. Central to its core strategy has been a discipline in the allocation of capital mixed between being opportunistic and prudent at the same time. Not easy.

BYD archives

Above: Signature property that was the foundation of an empire remains among the best marketers in the Vegas locals market.

It is this central reserve of savvy that in our view is the heart and soul of the success of BYD and why we believe in this current market its stock remains a great value at $62.28.

google

Above: The stock is quietly on the move toward July high.

BYD’s track record shows win after win in smart asset deployment The Borgata AC success confirms this thesis

Early in the 2000s, I was part of a group of senior executives in the AC casino industry who were invited by a team from BYD to a presentation of their plans for the Borgata project. What they had to say was refreshing, if not outright revolutionary. They planned to break every rule of conventional marketing wisdom accumulated from 22 years of operations. In brief they said, no mass bussing or promos, total dependence on drive in, demos light years younger than the proven AC golden slot play grey hair contingents. Simply put the dramatically superior property itself would be the core marketing tool.

The presentation provoked many skeptical questions from our group in the Q&A that followed. One listener suggested that their neighbor to be, Harrahs, was drive in first, but still ran big bus programs. Another saw that meeting as a teaching moment for the BYD guys: He said AC customers were spoiled with comps and bus deals. It was part of the East Coast player DNA, he said.. Another executive suggested that their approach was too much Vegas, a different world from AC.

BYD understood all of the chin scratching. Yet BYD maintained that it was confident that its $1b sunk cost would be money well spent for it and its 50% partner MGM.

The Borgata opened in 2003. It met and exceeded all forecasts by rapidly becoming the top revenue producer in the market. Its demo was indeed materially younger. Its property was brilliantly executed to immerse players and tourists in a real Vegas touch outside of the AC environment.

BYD had invested ~$500m for half end of the cost, a considerable jump given its size and financials in Nevada at the time. After 13 years of runaway success BYD sold its half to MGM for $990, Its share of profits over the years more than justified their investment. And the sale proceeds enabled BYD to walk away with net proceeds of $600m.

google

Above: The property that broke all the conventional wisdom rules of AB marketing and rose to the top in profits and revenues. It still leads.

Many in our and industry questioned why BYD would walk away from its share of the AC honey pot. The answer according to my industry colleagues in the know was this: They felt AC had reached near a peak and worried about new competition from Pennsylvania and New York. Instead they liked the growth numbers better at their home Nevada market.

So they took around $250m from their cash out and bought two locals properties in Las Vegas, seeing better returns over a longer term. Both have been accretive to earnings since.

In 2018, after the SCOTUS sports betting decision, BYD made a deal that opened its 28 properties in 10 states for its Fan Duel live sports books. In exchange, BYD got a 5% equity position in the FD parent. If this isn’t among the smartest example of deal making in the sector I don’t know what is.

Near six years later, Fan Duel is now the dominant part of parent FLUT’s present and future. At writing it shows a $29.3b market cap. BYD’s market cap is $6.3b, implying a theoretical value to the BYD position in the FLUT stock of $1.45b, or ~15% of the total. Moreover we have a PT on FLUT early in its trading on the NYSE from its price at writing of $211 to $245 by 2Q24. Fan Duel is now the #1 sports betting platform in the US holding ~40% of the market. Our expectation is that FD and its close rival DraftKings (DKNG) will together hold ~76% of the US sports betting market as far as the eye can see.

At minimum we are looking for US sports betting to haul in ~$35b in revenue by 2030. Maintaining a 40% share of market FD revenue to reach $14b. Forecasting long range where the stock may be trading at that point is a fool’s errand of course. Yet it is clear that the BYD equity piece could rise to a value of at least $2.6b by then. So prospects for BYD to grow both in brick and mortar casinos as well as a thickening digital presence. (BYD also bought betting tech operator Pala Interactive in 2022 for $175m assuring its presence in social games, cutting edge monitoring technology and data.

Guidance for investors contemplating opening a position in the gambling sector: You want to be in business with BYD- period.

google

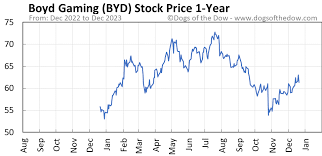

Above: The trajectory of the BYD shares has been north since 2021 and has since fattened. But the company has outperformed. Its sustained strong results since could well be about to trigger a breakthrough.

The price of our SA call on BYD 7/12/22: $49.67.

Frankly given the catalysts, superior management initiatives and healthy operational policies, the shares deserved a far more generous valuation in my opinion. But as usual, Mr. Market has a mind of its own. All too often we see stocks that appear to some investors to be a screaming buy while others shrug and keep in hot pursuit of rocket rides elsewhere. And sometimes there is sentiment that assigns dog with fleas status to any stock, regardless of its virtues, that has a long range sluggish trading range unrelated to performance.

We thought we saw breakthrough last summer when the stock moved up to $72 on news that was pretty much the excellent performance over the last 36 months. Yet it fell back again.

Over time, BYD has been strongly supported by analysts as either a BUY or STRONG buy. Yet the shares have been dead pooled around the 60’s far too long. It has been ready to break through based on rising quarterly results over 3 years. But it doesn’t. That may relate to waning interest in the sector of course. But my own view is that the consumer discretionary sector in general is still in the throes of worry about the game changing impact long range of covid.

The numbers could not produce a more bullish scenario IMHO.

BYD Intrinsic value analysis from alpha spread:

Base case: $92.39

Worse case: $63.84-stock is trading there now.

Best case: $148,49

DCF value: $74.50

Our PT taking post-covid solid recovery into consideration plus the company’s long and successful savvy asset allocation decisions we see $85 by mid-year.

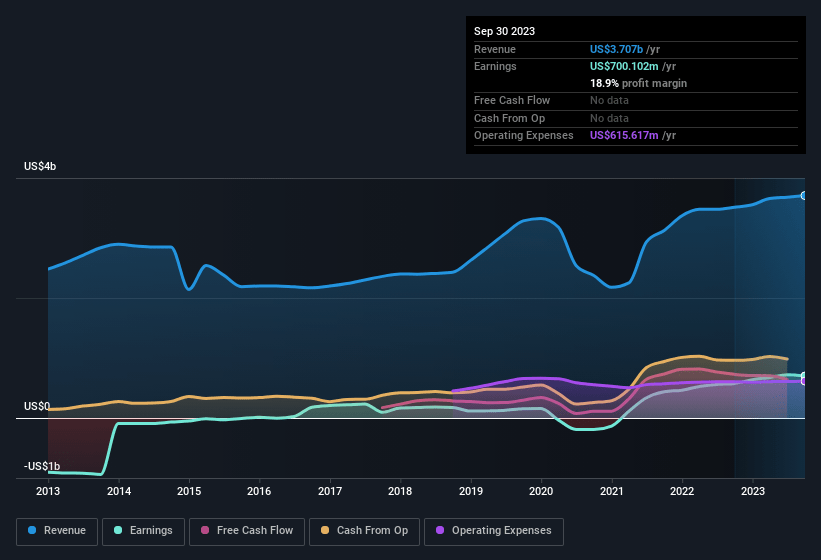

ROC as of 3Q23: 15%, a direct proof of BYD’s asset management skills over the past 10 years.

The gold standard metric to me that trumps all others in valuing casino stocks is EV/EBITDA. BYD sits at 13.10. The average S&P stock is at 14.20. But in the casino sector this augers a very solid operating performance.

The Durango challenge: Wait and see but there is a pattern

Last December 3rd, BYD competitor Red Rock Resorts (RRR) opened a 200 room luxury property that geographically and thematically appears as a potentially significant poacher of BYD locals properties. It is aimed at the upper segments of the locals market with a top shelf product. There was persistent Q&A about Durango by analysts at the most recent BYD earnings call. Executives were asked to weigh the possibilities of market share loss to the new properties. Their responses were candid, neither worrisome nor panglossian.

In brief, management said it’s too early to tell just what kind of impact BYD properties will feel when the Durango ramps up. We believe there could be some holders seeing this as a headwind. And others not yet in the stock, be getting wary of opening a position even off the solid performance of BYD.

We have a history of observing the impacts of new supply in gaming markets all over the world, including the Las Vegas locals market. What we have found is a classic 18-month cycle in the solidification of market share in a new competitor.

Here’s what our archived studies show:

First six months: Considerable trial both in established customers of competitors as well as what we call lookie loo business among curious tourists who all want to see new places. Durango is in a good area, with a cordon of 5 miles of no competitors. In this period poached business can move from 3.5% to 5.7% away from existing properties in the market. Phase two, 6 months to 12 months there is solidification. The merely curious are gone. Foot traffic settles into a predictable flow.

Aggressive marketing programs kick in as management now has a stronger handle on where the customers most likely to return come from and what they like and dislike about the new property. And then 6 months after the year two developments. The new properties have found their core players based on preferences in amenities and ease of access via roads. In other words they are more likely to be players who live closer to the property.

Secondly, on the average about 75% of the trial play that came from existing properties returns.

The bottom line: What the new property owners have really bet on is the longer term growth arc of the market in general.

RRR’s bet is made on the Vegas of tomorrow based on the rapid growth of population in Clark County, the #1 job growth metro area in the US and above all, visitation to Las Vegas. In 2023 the town climbed back to arrivals of 41m up 5% y/y. We expect that number to rise at least by 5.3% CAGR over the next five years. In three years Vegas visitation could reach 43m.

Conclusion regarding Durango: There could be some short term revenue loss to BYD but they have faced new supply issues before. They will have their marketing tools at hand to hold share and not overreact.

In short I do not think the arrival of the Durango will have any lasting major impact on BYD’s revenue flow from the area,

Overall takeaway

BYD is among the best of breed in the sector by any measure. Continuing revenue and EBITDA beats ahead, a keen eye on opportunities to deploy capital for above average returns and a management with a customer service DNA I like a lot as a veteran of the industry. And I think its 5% equity on Fan Duel is a real alpha not yet fully baked into its price.

At its current price, stagnated in the $60s I think it’s getting near a break through by mid year to well above $80.

Q2 2024 Earnings Call Transcript")