georgeclerk

Written by Nick Ackerman.

BlackRock, Inc. (NYSE:BLK) posted its latest quarterly results along with its full-year results as well. The company was able to exceed the bottom line estimates but came in line with the top line expectations.

The company has a history of beating results, with 15 of the last 16 quarterly reports beating expected EPS. Revenue has been a bit more hit or miss – with some slight misses 3 out of the last 16 quarters. That said, perhaps analysts are just better at estimating the revenue number, as the last four quarters in a row essentially were right in line throughout 2023.

In the latest quarter, the asset manager has once again regained the $10 trillion assets under management, or AUM, mark. This was helped along with a total 2023 net flow of $289 billion, $96 billion of which was in Q4.

For the year-over-year AUM flows, retail clients saw total net outflows for the year, but ETFs contributed massively as they garnered nearly $186 billion for the year. Institutional active strategies also saw net inflows of over $87 billion. However, that was partially offset by the index strategies, which saw net outflows of $55.125 billion.

With that said, market changes also contributed significantly year-over-year, as that added over $1.073 trillion back to AUM – mostly with a strong rebounding market from 2022’s down year.

While they posted some decent results overall, the more exciting news would have to be that they are acquiring Global Infrastructure Partners. In their own words, “Creating a World Leading Infrastructure Investment Platform.”

Adding To The Infrastructure Roster

The GIP acquisitions further drive their dive into both equity and debt investments in the infrastructure space, but more specifically, adding to the private markets – noting that the acquisition pushes the combined platform to over $150 billion in AUM.

That might not seem all that impressive as the company once again reached the threshold of over $10 trillion in total AUM. As the world’s largest, it is definitely difficult to move the needle these days, but it’s also a decent position to be in, with its reach everywhere.

Further, infrastructure is a particularly advantageous area of the market. Human society relies on these hard assets in our everyday lives, even if we don’t think about it. It allows societies to survive and thrive. Infrastructure probably isn’t something most think about when it is functioning properly, but we definitely know when it isn’t working.

BlackRock gains an expert team in this field with this acquisition. More importantly, this further adds to their fee-based AUM and generates bottom-line earnings. This is a business, after all, and that’s the goal. Fee-related earnings (“FRE”) are particularly attractive when we start to look into the private space.

The combination will mark a transformational change in our private market scale and growth. GIP is the world’s leading independent infrastructure manager with current client AUM of over $100 billion and fee-based AUM of over $60 billion. The acquisition will create a highly complementary pro forma $150 billion infrastructure platform post-closing tripling BlackRock’s infrastructure client assets. The integration will nearly double our private markets management fees to over $1.5 billion and add over $400 million in post-tax annual FRE [(fee-related earnings)] with FRE margins above 50%.

Additionally, it is even more attractive when you consider it can be illiquid assets they are taking custody of.

GIP has generated really strong performance as well as FRE growth. I’m not going to comment on the 2023, it will let the 2024 speak for itself. But we continue to see great growth opportunities in terms of being able to expand fee paying AUM across the illiquid alternatives platform with the infrastructure as a priority as well as growing base fees in a way that adds to our 5% organic growth objective through the cycle.

When operating private funds, there are often limits on what can be withdrawn in terms of redemptions. We just have to remember Blackstone’s (BX) BREIT continually hitting redemption limits. Private funds often have to have these sorts of features because of their illiquid nature; they cannot just liquidate positions into an open market, as can be done with publicly traded securities and those liquid securities with an active secondary market.

Of course, this isn’t a free transaction. The price tag for this acquisition does come at a fairly hefty $3 billion-plus 12 million shares of BLK. With BLK at around $800 right now, we are looking at about $9.6 billion worth.

That’s certainly out of my league, but the market reaction was rather neutral. I think that reinforces that this deal can make sense as often, when an acquisition is announced, shares of the acquirer can move lower.

In the Q4 earnings call, they further highlighted that they bought the iShares asset from BGI, and it had under $300 billion. Today, that’s climbed to $3.5 trillion. They also highlighted when they acquired First Reserve when it had around $3 billion in AUM. They noted that they “tripled its assets in a number of years in terms of infrastructure.”

Certainly, that bodes well for the world’s largest asset manager to continue its successful trend. That said, it’s quite clear that the iShares ETF platform is notably different in terms of its reach and scope.

Small Dividend Bump

While the acquisition news was certainly the most noteworthy for the quarter, we also got the annual dividend increase we’ve come to expect around this time. That said, this raise was likely a big disappointment to most investors as it was another small 2% bump this year – similar to where it was last year.

This had once been a rapid dividend grower and contributed meaningfully to my own dividend income growth over the last several years.

BLK Dividend History (Seeking Alpha)

At first, I was fairly disappointed as well. However, aside from putting free cash flow (“FCF”) into something like a sizeable acquisition in private infrastructure, this is also reflecting some prudent management.

For the year, the company generated adjusted EPS of $37.77. Next year, earnings estimates are expected to reach $39.50. The annualized rate being raised up to $20.40 now means an EPS payout ratio of around 54% or a forward payout ratio based on expected earnings of nearly 52%. The FCF payout ratio is tighter but not in danger territory, as it is around an 80% FCF payout ratio.

So, no matter how you slice it, the company has earnings and really enough cash flow that it could be further paying out to investors.

That said, these earnings posted last year haven’t topped peak earnings hit in 2021. 2022 was a rough year, and in 2023, while we saw a recovery, it took most of the year to get back to where we were. We aren’t expected to see those 2021 earnings topped until next year, and that’s if the market cooperates.

BLK Earnings History and Forward Estimates (Portfolio Insight)

Similarly, and really about what we would expect, FCF has been under similar pressure.

BLK FCF History (Portfolio Insight)

Therefore, given the acquisition and looking at earnings and FCF trends, I believe it makes sense to be fairly prudent.

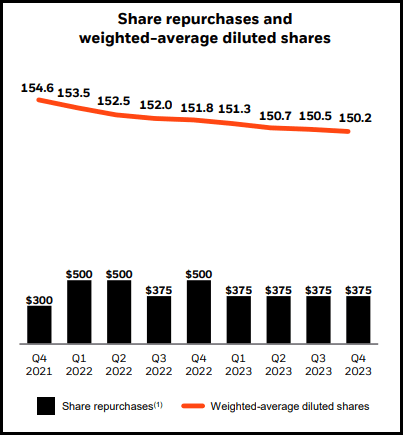

Additionally, the company has been steadily repurchasing shares. They noted that along with dividends, share repurchases saw $4.5 billion returned to shareholders. So, it isn’t as though the only returned capital is coming through the dividend alone. Shares outstanding have been steadily declining.

BLK Share Repurchases (BlackRock)

This brings up another point that circles back to the acquisition and being prudent. With another 12 million shares going to be added, it could make sense that they turn to more aggressive share repurchases rather than dividends. After all, those 12 million more shares will also require being paid the dividend in the future. That said, they also noted that they expect the acquisition to be “modestly accretive to AUM.” Meaning, those new shares should pay for themselves.

Conclusion

BlackRock, Inc. posted some decent results, and their AUM has recovered from the 2022 market swoon, thanks to both a rebound in the broader market and continuing to see positive net inflows. Acquiring a private infrastructure investment platform can further add to their capabilities going forward – adding both further AUM and, more specifically, fee-earning AUM that can be relatively sticky.

All this said, shares of BLK aren’t cheap like they were just a few short months ago or throughout most of 2023. Based on their fair value historical P/E range, we are in the upper half.

BLK Fair Value Range Estimate (Portfolio Insight)

With earnings expected to grow going forward, the share price could sit still, and it would eventually become cheap once again. For a longer-term investor, being so picky probably isn’t necessary, and the company can likely still deliver strong returns in the future, even at these levels. That said, a more patient investor who can be prudent with their own capital could consider BlackRock, Inc. shares to come down closer to at least around $765 or ideally lower before ultimately looking like you are getting shares at least at fair value.

Q2 2024 Earnings Call Transcript")