Jamie Grill/The Image Bank via Getty Images

Thesis

Black Stone Minerals (NYSE:BSM) was handed a lump of coal for Christmas. On Christmas Eve, one of its largest natural gas producers, Aethon, announced that it was exercising a “time-out” clause in its drilling contracts with BSM in the Haynesville shale. In response, BSM announced that this would not meaningfully impact 2024 financials thanks to a pipeline of 30 wells that are already in progress. The company expects these wells will be completed on schedule regardless of the time-out.

While BSM is technically correct that 2024 should be able to produce a relatively flat natural gas production profile, it does not adequately explain the embedded risks to investors for 2025. The characteristics of the Haynesville shale could result in a rapid decline in natural gas volumes in 2025 if replacement inventory is not developed. This could result in an eventual cut to the dividend as cash flows decline.

This conclusion has resulted in my downgrade from a Buy in September 2023 to a Hold.

Time Out

2023 and the start of 2024 has been horrendous for natural gas prices. There really is no other way to say it. After two very mild winters in a row, the industry sits in early February with spot natural gas prices flirting with $2/MCF. It is no surprise that natural gas producers are challenged in this environment.

This challenge is even larger in the Haynesville shale, which has one of the highest break-even costs in North America. Drilling costs are more than double on a per foot basis than the Marcellus, resulting in breakeven prices approaching $3/MCF in this basin.

South Western Energy (SWN Investor Presentation)

As a result, Aethon, the top producer in Haynesville is scaling back its production. The private producer announced on December 23, 2023, that it was declaring a “time-out” on its production agreement with BSM. Under this agreement, Aethon was contractually required to drill at least 27 wells per year on its Haynesville acreage in San Augustine and Angelina counties. BSM was able to arrange such a contract by offsetting a portion of the development costs to 3rd parties in exchange for a portion of the royalty rate. While this was excellent deal making on BSM’s part, at current prices, the deal no longer makes economic sense.

In the associated press release, BSM stated that it anticipates Aethon to complete the 30 wells that are currently in progress and the financials for 2024 will be largely unaffected. While I can reasonably conclude that this estimate is accurate, it also does not tell the entire story. This announcement means that the pipeline for future production is essentially stopped.

Under the current clause of the contract, Aethon is permitted a total of 18 months of “time-out” over a 48-month period, with a maximum time-out period of nine consecutive months. Now that we are in the backstretch of winter, we are without any real economic drivers for natural gas prices for several quarters. It is hard to imagine what would drive natural gas prices back up into the profitable range to inspire enough confidence to warrant further investment on Aethon’s behalf. Therefore, in the absence of a market disruption, I assume this production pause will last the full nine months that is permitted by the agreement.

Under this scenario, Aethon would not resume drilling until the beginning of Q4 of this year. BSM has stated that it takes roughly 10 months to get a well to sale from the onset of drilling. As a result, any new well will not begin flowing until Q3 of 2025.

The press release by BSM only discusses 2024 from a siloed perspective. Based on well performance characteristics of the Haynesville, this “time-out” creates a 9-month gap in production that could result in a sharp decline in natural gas volumes.

Understanding Type Curves and Their Importance

Many investors understand that the highest levels of production for a well occur in the first few months of operation. Daily production declines rapidly, and then enters a gradual decay. This behavior is typically shown in what is called a type curve.

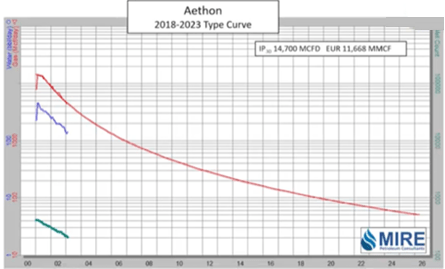

The shape of the type curve for Haynesville wells is much more drastic than those of the Permian basin. These wells are characterized by extremely high initial production rates followed by a stunning decline. The decline rates are so severe, that after 6 months of production, daily output falls to only 10% of peak rates. After one year of operation, daily production falls to roughly 2% of the initial rate.

The graph below displays well performance over the last several years produced by Aethon in the Haynesville shale. This chart was developed by MIRE consultants who studied that basin across multiple operators. It is extremely important to note that this graph is displayed on a logarithmic scale and thus is exponential in nature. This graph shows that while initial production rates are nearly 15,000 MCF/d, at the 6-month mark, rates have fallen to just over 1,000 MCF/d or 9% of the initial rate.

Haynesville Well Decline Rate (MIRE Consultants)

This rate of decay makes these wells comparable to bottle rockets. While no basin is perfect, other basins can contribute approximately 20% of initial production after being online for 12 months. This bottle rocket behavior has the potential to set 2025 up for rapid declines in natural gas volumes if replacement activity for the Aethon wells is not found. All of the 30 in-progress wells turned online in 2024 will essentially be exhausted by the time the calendar flips to 2025.

NOTE: MIRE Consultants has an interesting YouTube channel for those interested in learning more about oil and gas production.

Total Impact

At this point, it may seem like the sky is falling. Fortunately for BSM, 63% of its revenue came from oil and condensate sales in Q3. This provides a very strong backstop to mitigate the potential consequences of the decline in the natural gas segment. Adding to its financial strength is its debt-free balance sheet and cash balance of $56 million to weather a few rainy days.

Without finding methods to replace the Aethon volumes, BSM will have a few rainy days ahead of it that may result in draining its cash funds to sustain the current dividend. In Q3, the company recorded a revenue of $110 million while paying out $94.5 million in distributions.

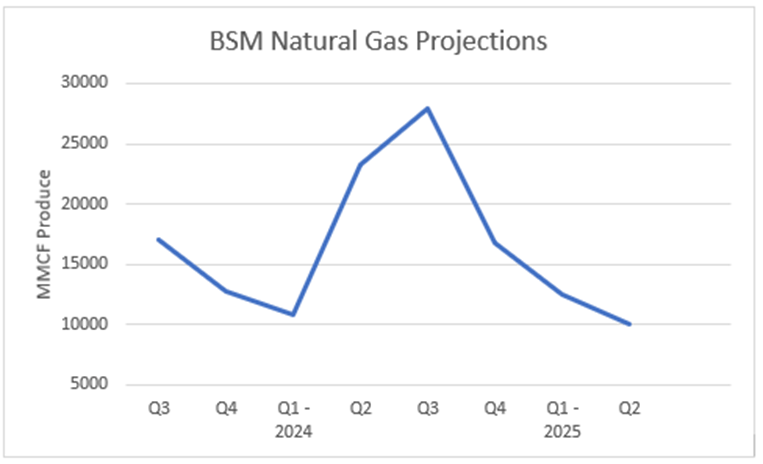

Using the previously mentioned type curves I modeled the company’s production profile. I project a 25% decrease in natural gas volumes beginning in Q1 of 2025 compared to Q3 of 2023. At a $2.75/MCF strip, this results in a loss of $12 million in revenue. The subsequent quarter would endure a subsequent 20% reduction in volumes, resulting in an additional $7.5 million in lost revenue.

Projection for Natural Gas Production (Author Modeling)

BSM simply doesn’t have the margin to accommodate these losses. Fellow Seeking Alpha analyst, Elephant Analytics, previously modeled BSM’s cash flow using $75 oil and $3.75 for natural gas as inputs to the model. In his model, the distribution coverage was approximately 1.0x. Experiencing steep production declines in 2025 will require the company to start drawing on its cash reserves to maintain the current distribution.

What To Do

Management’s commentary in Q4 is critical in my view. If it sells the narrative that 2024 will be fine and that’s all it has to say on the matter, I have a huge concern. It should at least be straight with investors as the risk factor for the stock has certainly increased. As a result of this, part of me wanted to recommend a sell for BSM. There are a few reasons why I maintained my HOLD rating.

1. The risks are far enough in the future that management has time to develop a solution. The partnership is also in a net cash position to help weather minor cash shortfalls.

2. Long-term unit holders may have a low-cost basis and invoke high tax implications on a panic sell. Since BSM is a partnership, the tax implications are different compared to a standard C-Corp. I recommend consulting a tax professional to under the implications of any sell decision.

3. There is reason to believe that the 5 BCF/d of projected demand additions for LNG exports will raise the price floor of natural gas. This will help offset losses from production declines and will correspond with the “time-out” expiring. There may very well be lucrative times after a 6-to-9-month rough patch starting in Q4 of 2024.

Summary

In this article, we looked beyond the headline to understand the long-term implications of disrupting the Aethon production pipeline. The rapid decay nature of Haynesville wells has the potential to rapidly reduce natural gas production starting in Q4 of 2024 until production can resume mid-2025.

I withheld from recommending a sell rating as a result of the financial health of the partnership while also accounting for potential tailwinds developing in mid-2025. I believe these strengths warrant giving BSM a ‘wait and see’ approach but investors should be cautious in the near term to see how the situation develops. A distribution cut is certainly a possibility if management cannot pivot.

Q2 2024 Earnings Call Transcript")