helen89

Introduction

Before we start breaking down BJ’s (NASDAQ:BJRI) first quarter 2024 results, I would like to highlight that this is an analysis intended to place greater emphasis on short-term operational patterns. Therefore, if you are interested in a more complete analysis, which aims to closely investigate both profitability, capital structure and other factors, I recommend reading my latest analysis of BJ’s.

For those who remember, I recommended “Buy” in my last review of BJ’s Restaurants, mainly expecting an improvement in margins, along with the establishment of successful cost containment programs. What we had in the first quarter of 2024 was, perhaps, something more than that, since not only have costs been contained and improved significantly since the pandemic, but also a favorable outlook for the brand’s geographic expansion into new markets.

The development of a leaner unit model, which costs 15% less, corroborates the attractiveness generated by the successful implementation of the Brookfield unit and suggests that the brand will be able to grow organically in states where they do not have a presence.

Due to the favorable outlook, expectations of increasing earnings, in addition to the prospect of expanding the brand organically, I reiterate the “Buy” recommendation for BJ’s. Remember, this recommendation is based on long-term prospects, so they may not correspond to short-term changes in the share price.

First Quarter 2024 Developments

Despite weaker demand in January, BJ’s recovered for the remainder of the quarter

Initially, we will understand how revenue behaved in the first quarter of fiscal year 2024 at BJ’s Restaurants and then measure the impacts of optimizing processes with the aim of improving margins on the quarterly return.

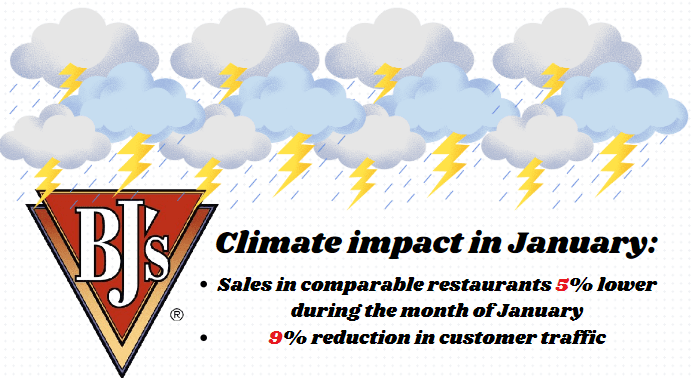

First of all, it is worth highlighting that part of the operations were interrupted or impacted by winter storms that hit the Midwest and Southern United States in January.

How the weather impacted BJ’s in January (Author)

The impact of these storms affected comparable restaurant sales in relation to the first quarter of 2023, which were 5% lower than the same period last year, also impacting customer traffic, which fell by around 9% when compared to the same period. Based on the developments presented during the months of February and March, BJ’s was able to present a measure of comparable restaurant sales that was only 1.27% lower. This indicates that, if not for January 2024, comparable restaurant sales would be slightly higher or at least very similar to the first quarter of 2023.

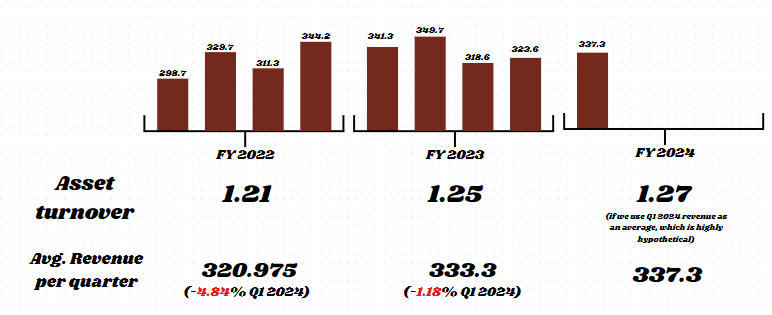

Revenue in recent quarters (Author)

Note that the revenue indicated in the first quarter of 2024 exceeds the average revenue of the two previous calendar years per quarter. Furthermore, there are signs of improvement in asset turnover, which will tend to grow as revenues become stronger (which is very likely to happen, given that revenues have grown on an annual basis every year since the effects of COVID- 19 were mitigated).

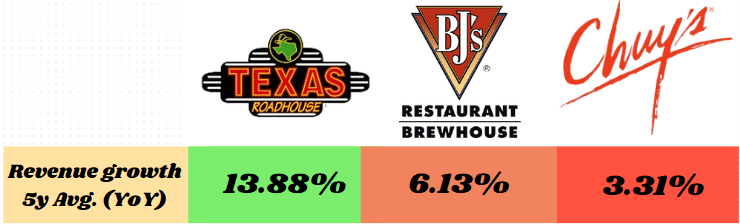

For the long term, management has established a base scenario of sales growth of 8% to 10% per year. We need to remember that BJ’s five-year average revenue growth is around 6.13%, which is definitely not weak growth when compared to companies in the casual dining sector. As I will discuss later in this analysis, the success of the new unit entering the Wisconsin market suggests that the company will continue to expand the brand’s presence geographically, perhaps being the vector of sales growth. Even more so when we consider the new prototype unit, which costs approximately almost 15%.

Average revenue growth for BJ’s and other casual dining restaurants (Author)

Due to the substantial improvement in margins, as a result of the partnership with the activist investor PW Partners and the commitment expressed by management in the search for operational efficiency (as I had already predicted in my last analysis of BJ’S Restaurants, which you can find here), we saw a movement to contain the price increases that the company was practicing throughout the entire fiscal year 2023.

In January, for example, there was a 1% increase in menu prices, around 200 basis points than in January 2023. Therefore, from a marketing point of view, it is clear that management intends to prioritize customer retention (aiming at a long-term relationship and organic growth in both revenue and the business as a whole) rather than simply aggressively increasing the price of the menu in seeking to increase profitability by overcoming fixed costs.

Another positive development was the normalization of alcohol sales volume to pre-pandemic levels. As BJ’s brewery segment is quite impactful in terms of its value proposition, it seems that the company is succeeding in its central proposition, offering casual dining with a “premium” experience. In this vein, craft beers can very well be included in strategies to maximize the check per customer, as they are an item commonly associated with a higher perceived value. The variation in blends and flavors can lead to the consumption of multiple units, even more so when facilitated by promotional times or combined discounts.

The long-awaited impact on margins has arrived

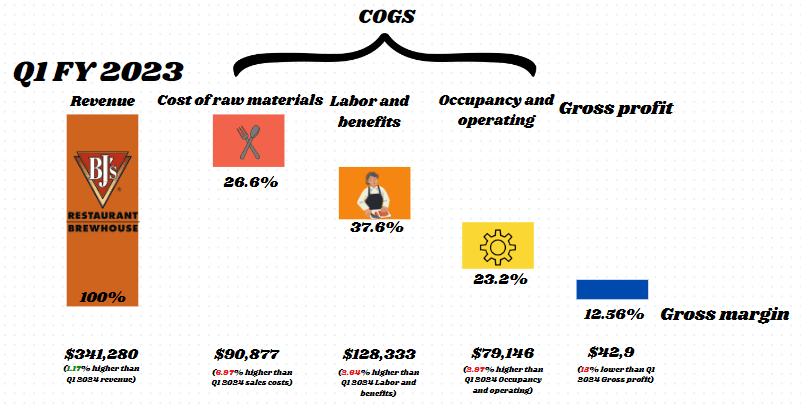

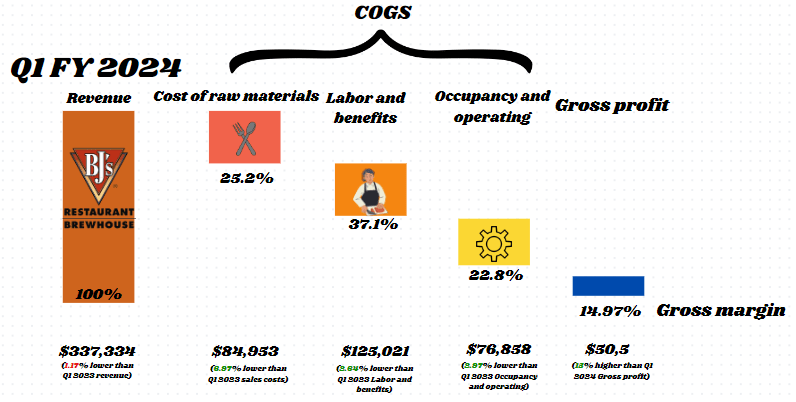

From now on, let’s talk about BJ’s Restaurants’ margins and the long-awaited improvement in operational efficiency. Below, I have broken down the company’s COGS into three major cost centers: Cost of raw materials, Labor and benefits and Occupancy and operations. The first graph refers to the first quarter of the 2023 fiscal year, and the second refers to the last quarter:

Composition of operating costs in Q1 2023 (Author) Composition of operating costs in Q1 2024 (Author)

Note that, in addition to the negative pressure felt on revenues due to the factors mentioned above, which were: reduction in customer traffic and comparable restaurant sales in January, milder than normal increases in menu prices in the first quarter of 2024 and an increase in traffic In restaurants at night (night traffic has a lower check per customer at BJ’s), all groups of operating costs were positively affected.

This improvement in cost management is truly commendable, even more so when we put into perspective that many companies in the casual dining segment and, especially its “half-brother” fast-casual, are suffering really serious pressure on costs, especially when it comes to labor costs. BJ’s managed to reduce this group by approximately 2.64%, reducing its importance in the operational cost matrix by 0.5 percentage points.

Speaking of which, all operating costs decreased in importance in the first quarter of 2024, with the one that benefited most being raw materials, which was almost 7% lower on an annual comparison basis and decreased its total importance by 1.4%. Specifically regarding the cost of inputs, BJ’s has been carrying out some new processes since the beginning of the last quarter to ensure efficiency in its production chain.

An example of this is its new meat supply program and the reformulation of certain sauces, prioritizing certain types of ingredients that help contain costs. With these advancements, the company has more than offset the inflationary costs of items like salmon, wings and steaks.

Now, when we talk about labor costs and benefits, BJ’s is using a method already widely used by large restaurant chains, which is the AI-based sales forecasting tool. This model was one of the pivots responsible for reducing labor costs, as it boosted productivity per employee to pre-pandemic levels.

And anyone who thinks that the use of AI tools for process management, in the case of BJ’s, is only focused on the labor aspect, is mistaken, as the company has already been using a similar system for inventory management. And remember, inventory and operational cycle management is extremely important for companies in the restaurant sector as a whole, as they have little or no net working capital and need to finance their operations from current resources. This is only possible with a well-parameterized cash cycle with cash needs and optimal management of receivables. From these efforts, we saw in the first quarter of 2024 a cost almost 3% lower than in the first quarter of 2023.

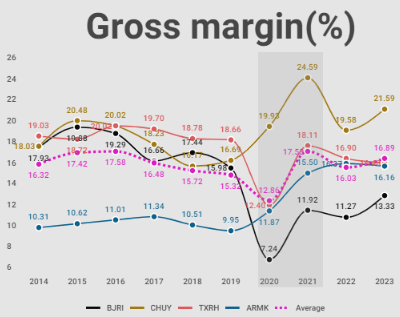

The result of this improved cost management was a gross profit 15% higher than that of the first quarter of 2023. The gross margin presented in today’s BJ’s results is 14.47%, which puts the company back on track to achieve pre-pandemic levels. Observe how BJ’s improves its gross margin since the very weak result in 2022:

Annual Gross margin in perspective (Author)

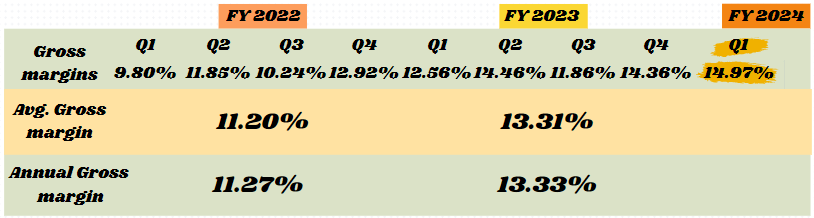

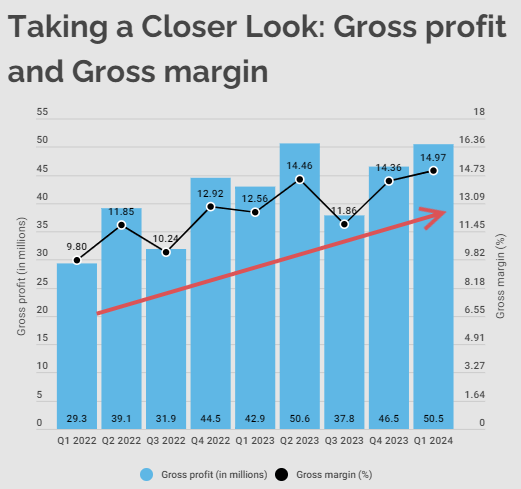

How about we take a closer look at BJ’s gross margins over the past few quarters?

Gross margin in recent quarters: notice how they have improved since 2022 (Author)

Note that the gross margin presented by BJ’s in the first quarter of 2024 exceeds all of the last eight quarters. It is interesting to mention that the fourth quarter of 2023 had already presented a very satisfactory gross margin, which, in my opinion, indicates a clear trend towards operational efficiency.

Author

Other operating expenses, non-operating expenses and net profit

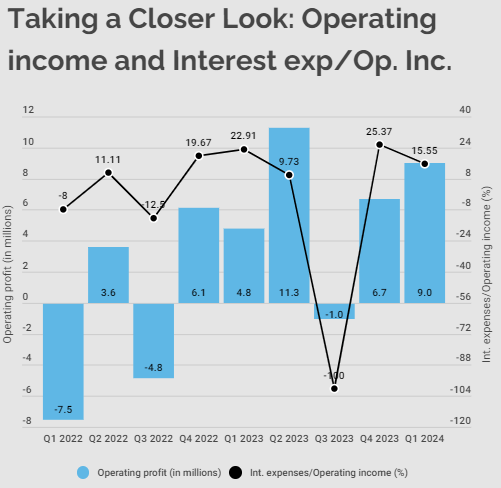

Below, I will compile how much BJ’s earns in operating profit and how much of that operating profit is spent on interest expenses.

Author

When we exclude non-monetary expenses, BJ’s effectively has no problem paying interest on what it earns from its operations. However, in some quarters, we see that this relationship presents itself with a little more volatility. With the continuous improvement in margins in the coming quarters, the tendency is for BJ’s to be able to maintain this relationship between interest expenses and operating profit continuously below 15%, in fact, we would already see a relationship of this type if the month of January was not impacted by climate.

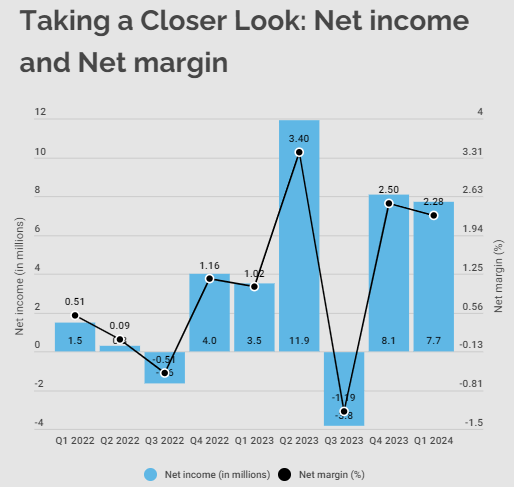

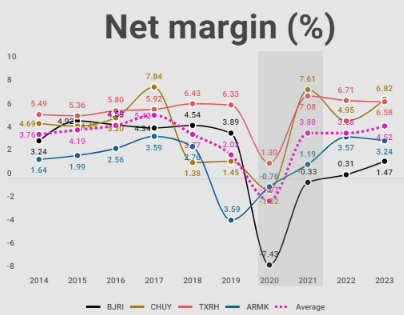

Author Annualized net margin in perspective with other companies (Author)

Note that despite having historically low net margins, since 2023 BJ’s has been increasingly approaching the sector average. The fourth quarter of 2023 and the first quarter of 2024 already exceed all annualized net margins from the pre-pandemic period. BJ’s first goal is to return to the margins presented between 2015 and 2018, approaching 5%, slightly above the sector’s historical average.

For the year 2024, a margin greater than 2.5% would already represent a significant advance for BJ’s profitability. Everything indicates that, if no catastrophic event occurs by the end of the year, management will most likely achieve this result, since the company is committed to developing processes that improve operational efficiency.

Openings, new prototype and remodelings

Material proof of BJ’s ability to touch new markets and take advantage of unexplored potential is the new unit in Brookfield, Wisconsin. This unit marks BJ’s entry into the state, and it seems to have arrived on the right foot, presenting very strong results since opening.

There are remodeling initiatives in the markets in which the company already operates. By the end of the year, BJ’s plans to remodel 23 of its restaurants, using lighter colors, remodeling the bar and a 130-inch television as a focal point. Following the paradigms implemented to operate with high efficiency, for the next two openings in 2024, BJ’s will use the new prototype unit, which costs around $1 million less than the current model. The current model costs around $7 million to get ready to operate.

In this context of brand expansion, we can paraphrase Greg Levin, President and CEO of BJ’s, “This is our first restaurant in Wisconsin and is off to a very strong start, demonstrating the broad appeal of the BJ’s concept in several regions of the United States, which reinforces our belief that there is room for further expansion to 425 or more restaurants, approximately double our current number of restaurants.”

We are seeing firsthand why adapting this new restaurant prototype is so important for BJ’s, and it is not just a matter of increasing the rate of return on its investments in the short term, but rather the rehearsal for expansion across the country. I mean, if this new prototype proves profitable in the short term, and still proves to be quite profitable along the lines of the new unit in Brookfield, demonstrating organic growth in new regional markets, this will probably be the expansion model in a broader context.

I say this because organic growth without the need for very intensive capital is a sign that BJ’s will be able to penetrate new markets without the need to acquire another regional brand, for example. And this is extremely important for BJ’s expansion plans.

From this perspective, we can infer that each of BJ’s 217 restaurants operating after the first quarter of fiscal year 2024 generates an average of $1,554 million per quarter in revenue. That’s approximately $129,500 in sales per week per restaurant.

Using the operating margin, in order to evaluate the profitability of the average unit, without focusing on non-recurring expenses or interest expenses, for example, which are more relevant at corporate levels than operational levels, we have the average profit per unit of BJ’s in the first quarter of 2024 was approximately $41,336.4. If we assume constant results for the next three quarters, we will have revenue of $6,216 million and an operating profit of approximately $165,345 per year at each unit on average.

Using the operating cash flow margin, when we add back the non-cash items into the equation, we have a margin of 9.54%. This means that following this metric, BJ’s earns approximately $593,000 per year, very different from when we use the operating margin.

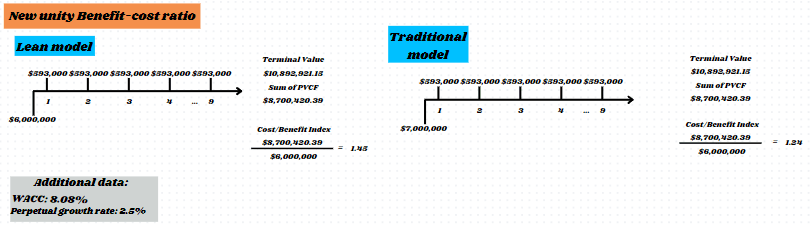

Cost/benefit index of each model using simplified values and averages (Author)

This means that a change in the unit’s establishment value (let’s say the values remain constant) from $7,000,000 to $6,000,000 for a unit with average revenue and operating margins, would impact about 1.24 to 1.45 with respect to the project’s attractiveness index. That’s an improvement of approximately 17%. This would greatly assist the establishment of new units. Remembering that the numbers I used here are static representations of values that change a lot, I just wanted to demonstrate the cost of implementing the leaner unit would impact the expansion project.

Very short term: what do we expect from BJ’s at the beginning of the second quarter?

Statistically, the second quarter is the strongest for BJ’s. After a new round of price increases in the second quarter of 2024, a small drop in comparable sales was noticed, along the lines of the first quarter (between 1% and 2%). Despite this, traffic is gradually improving, with April being the month with the highest traffic so far.

This situation probably occurred due to an increase in customer traffic during the night shift. Therefore, as customers who frequent BJ’s at night have a smaller check on average, sales end up suffering decreasing pressure in terms of volume. It will be up to management to pay attention to how to increase the check per customer during the evening hours.

Will this greater customer traffic continue to frequent BJ’s after this new round of price increases? These will be developments that we need to pay attention to during the release of the second quarter results. If demand remains resilient even after successive rounds of price increases, this will imply that the company has some type of competitive advantage that will provide a certain elasticity for price increases and, consequently, margin expansion.

What we are seeing is management observing “how far they can stretch the string without it breaking”, how far they can increase their pricing without significantly affecting demand. This will depend on the differentiation of its value proposition, and BJ’s will also need to continue working on these management issues in parallel.

Therefore, management expects Q2 2024 comparable sales to be slightly lower than Q2 2023. That is, customer timing preferences appear to be well established, and there is a long way to go before an increase in the check medium in an organic way. But this is not a problem, as long as BJ’s continues to improve its processes, costs and expenses, in order to present increasing margins throughout the year, in the same line as the most recent advances are pointing to.

Conclusion

Given recent developments, both in margins and brand positioning, I reiterate my “Buy” recommendation for BJ’s Restaurants. What I see both in statements and in actions that are materialized by the results is a management committed to improving margins and operational efficiency, and for what did not give a vote of confidence in the fourth quarter of 2023, the first quarter of 2024 brings favorable airs to the performance of the action.

Thus, the share price soared after the release of the results on 05/03, precisely after the materialization of these positive results and a glimpse of expansion into other American states after a successful establishment in Brookfield.

We also need to monitor, in addition to those pricing strategies according to the segmentation of night-time customers, the establishment of a lean restaurant model, which could pivot the brand’s growth across the country. This model offers savings of around 15% in restaurant establishment costs and, consequently, will make many projects viable, and even very attractive depending on the flow of customers, as observed in my restaurant viability analysis.

We will continue to periodically monitor the company. Any relevant upcoming developments and quarterly demonstrations, I will follow with you here on Seeking Alpha.

Q2 2024 Earnings Call Transcript")