Spencer Platt

In recent months, I have turned more bullish on the outlook for fixed income, particularly as the Fed has signalled peak rates have been achieved and markets look forward to policy rate cuts in 2024.

I came across the BlackRock Flexible Income ETF (NYSEARCA:BINC) while screening for bond funds with strong 2023 returns in order to uncover funds that may perform well in 2024.

The BINC ETF is a newly launched active ETF from BlackRock with a flexible mandate that allows its star manager to invest in various fixed income sectors like CLOs and Emerging Market bonds. So far in its short history, the BINC has outperformed peers by betting on outperforming sectors like CLOs. However, given the reliance on its star manager to make differentiated sector bets, I am hesitant to recommend the BINC without more data.

Fund Overview

The BlackRock Flexible Income ETF is a newly launched active bond ETF managed by Rick Rieder, the star bond portfolio manager at BlackRock who was named as Morningstar’s Outstanding Portfolio Manager of 2023.

Strategy

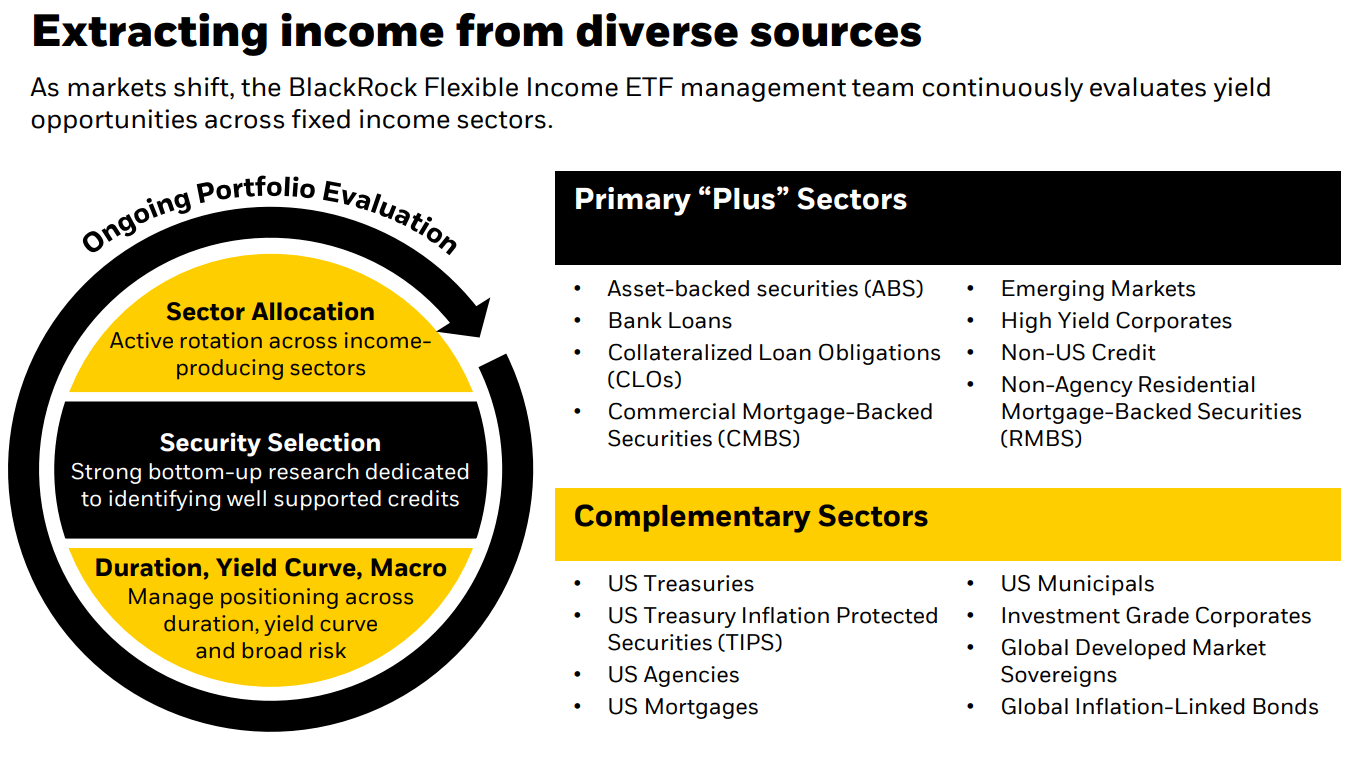

The BINC ETF is designed to maximize income by offering exposure to hard-to-access fixed income sectors and leverages the experience of BlackRock’s investment team, led by Mr. Rieder (Figure 1).

Figure 1 – BINC overview (blackrock.com)

The BINC ETF actively rotates across income producing sectors, with primary weights invested in Asset-Backed Securities (“ABS”), Bank Loans, Collateralized Loan Obligations (“CLOs”), Commercial Mortgage-Backed Securities (“CMBS”), Emerging Markets, High Yield bonds, and Non-Agency Residential Mortgage-Backed Securities (“RMBS”). In addition, the BINC ETF can also invest in other complimentary sectors like treasuries and Agency MBS.

In effect, the BINC ETF is a fixed income hedge fund managed by Mr. Rieder offered in an ETF Wrapper. The BINC ETF currently has $490 million in assets and charges a net expense ratio of 0.40% after fee waivers, effective until June 2025.

Portfolio Holdings

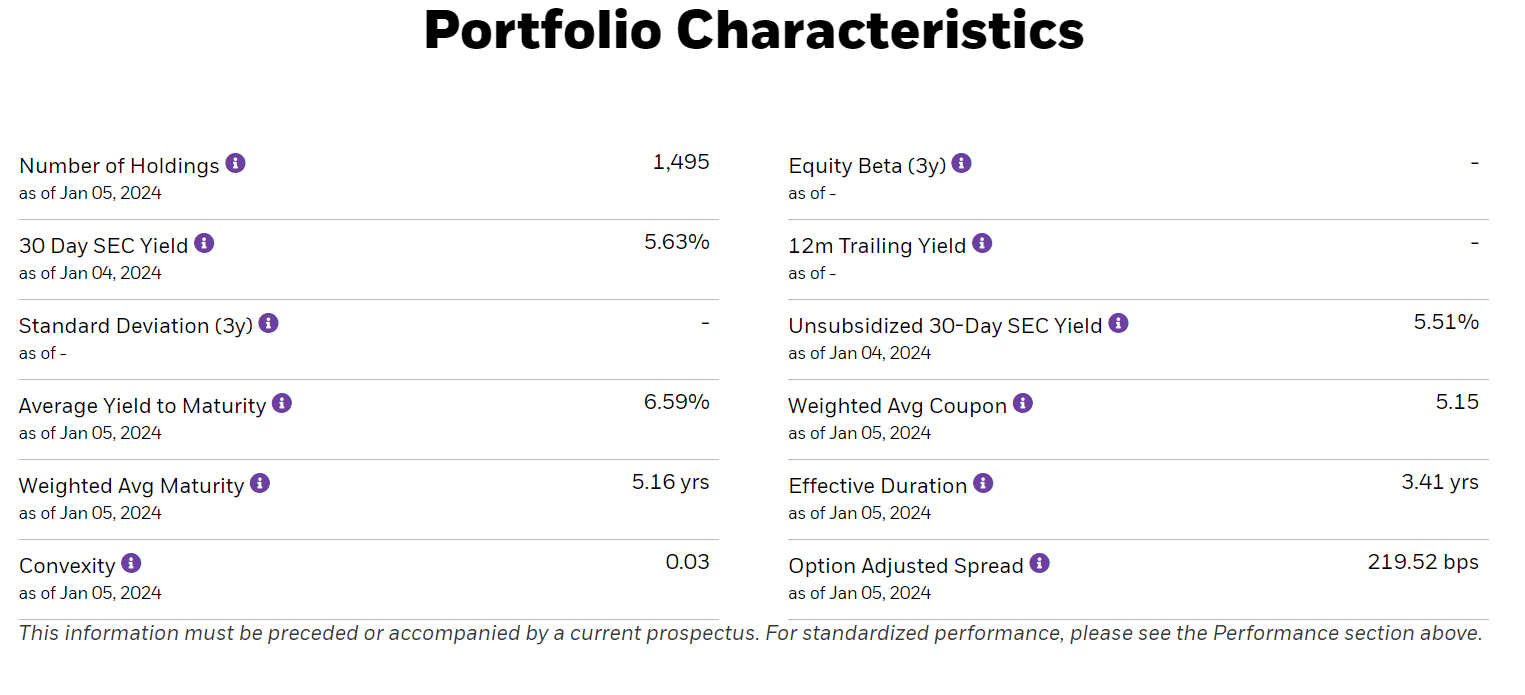

Figure 2 shows BINC’s overall portfolio characteristics. The BINC ETF currently has close to 1,500 securities with a portfolio effective duration of 3.4 years.

Figure 2 – BINC portfolio characteristics (blackrock.com)

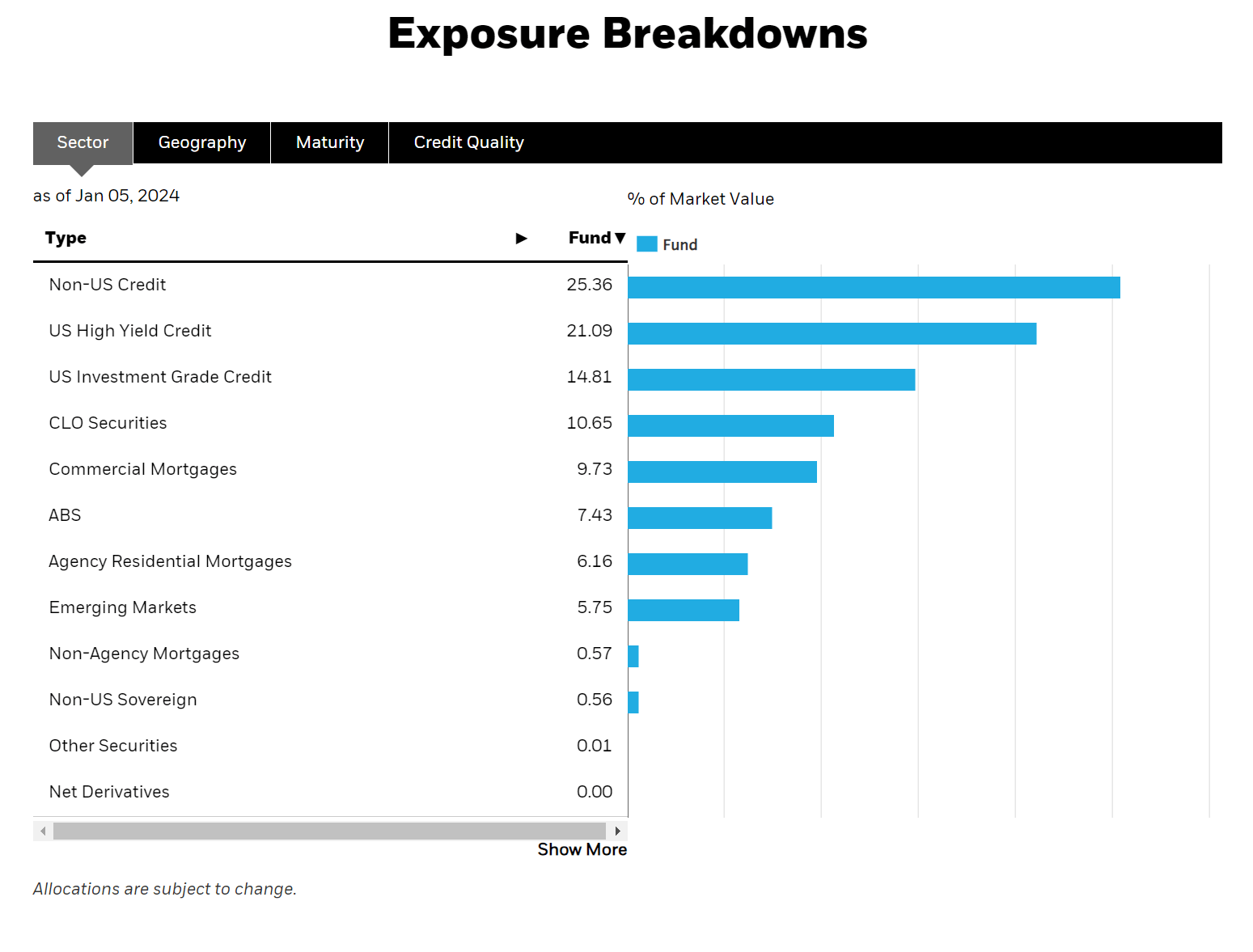

In terms of sector allocation, the BINC ETF has 25.4% of its portfolio allocated to non-US credit, 21.1% allocated to U.S. high yield credit, 14.8% in U.S. investment-grade credit, 10.7% allocation to CLOs, and 9.7% allocated to commercial mortgages (Figure 3).

Figure 3 – BINC sector allocation (blackrock.com)

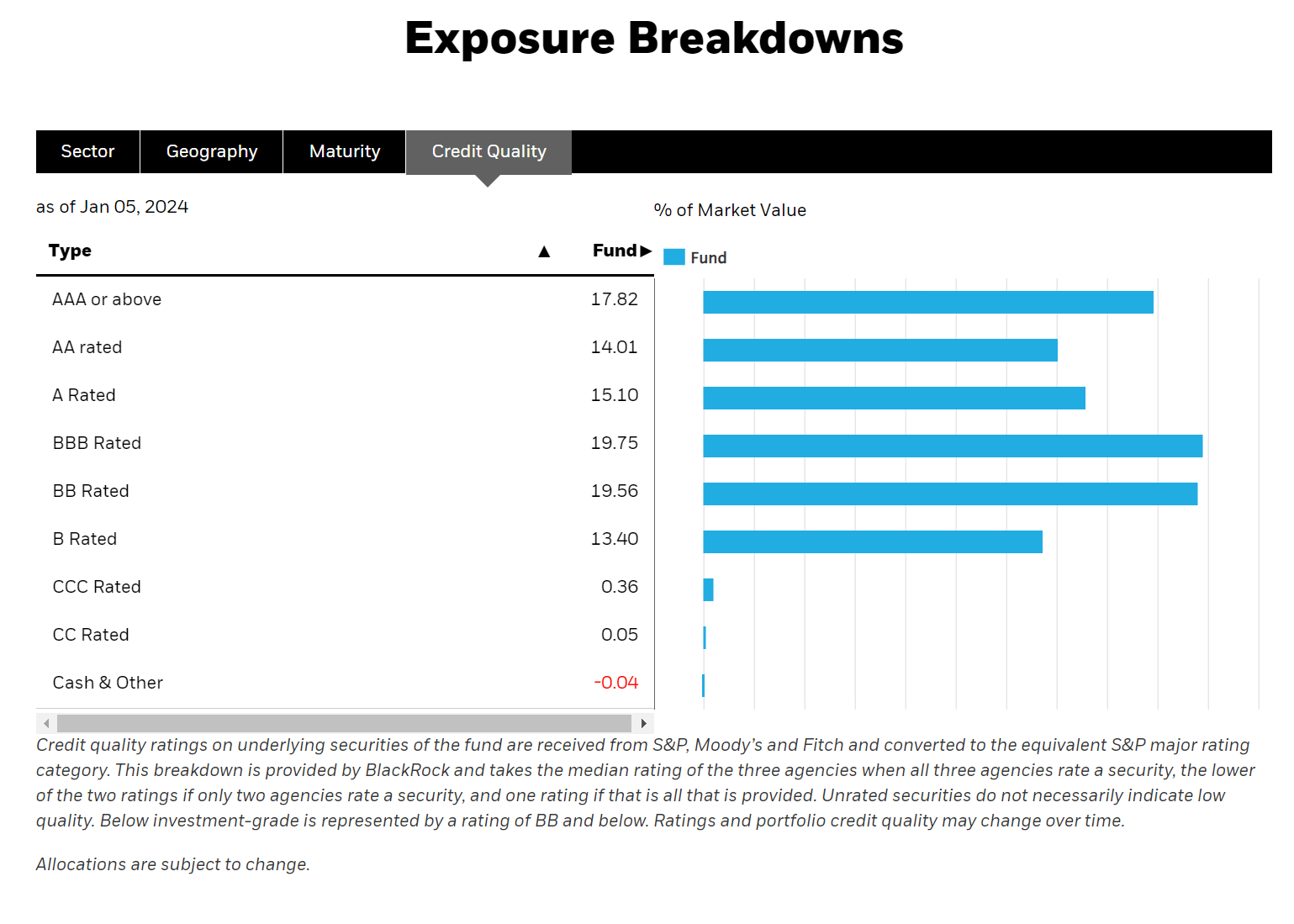

Credit quality-wise, the BINC ETF appears to be primarily investment grade, with BBB-rated to AAA-rated securities accounting for 66.7% of the portfolio while non-investment grade credits (BB-rated and below) account for 33.4% (Figure 4).

Figure 4 – BINC credit quality allocation (blackrock.com)

However, judging by BINC’s mandate, investors should be prepared to see fairly high turnover and movements in the fund’s sector and credit allocations, as the BINC ETF is designed to be ‘nimble’ and take advantage of opportunities as they arise.

Distribution & Yield

The BINC ETF has paid a monthly distribution with a trailing yield of 3.2%, according to Seeking Alpha (Figure 5).

Figure 5 – BINC distribution yield (Seeking Alpha)

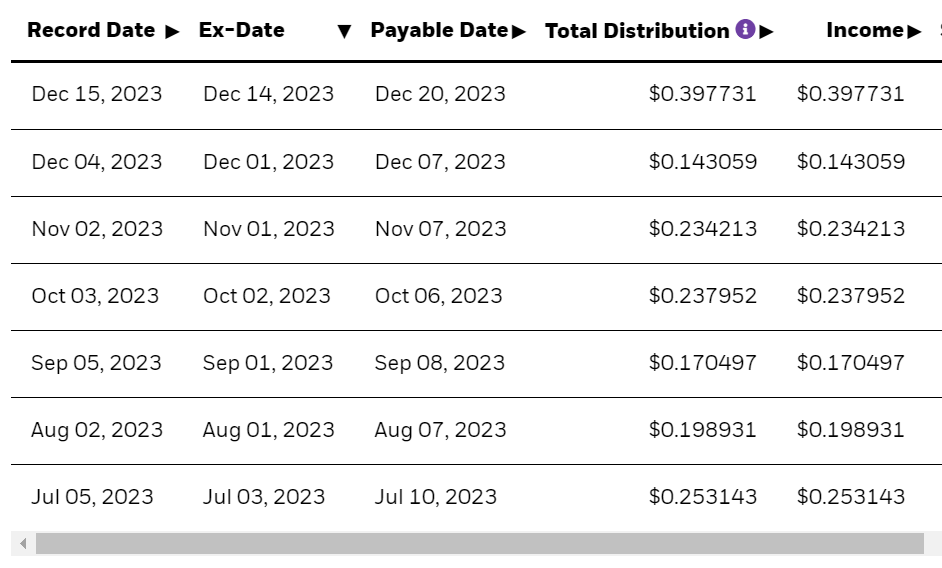

However, I believe this yield calculation is misleading as the BINC ETF only began operations in May 2023 so it has not paid a full year of distributions. Looking at actual distributions paid, the BINC ETF has averaged a monthly distribution of $0.206, plus a special distribution of $0.398 / share declared in December (Figure 6).

Figure 6 – BINC actual distributions (blackrock.com)

Hence BINC’s distribution yield is closer to ~5%. Officially, the BINC ETF has a 30-Day SEC yield of 5.6%.

Returns

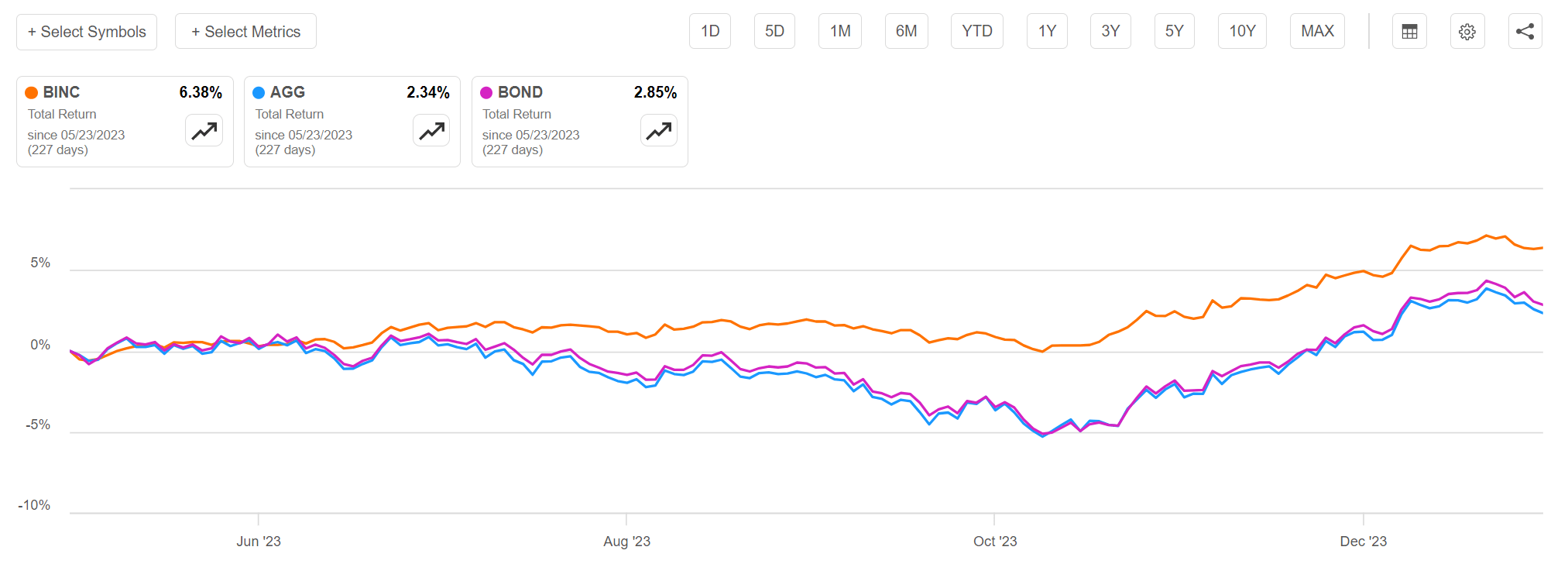

As the BINC ETF was only launched on May 19, 2023, there is not a lot of historical performance to analyze. However, from its limited history, BINC’s performance since inception has been strong, with the BINC ETF returning 6.4% compared to 2.3% for the iShares Core U.S. Aggregate Bond ETF (AGG) and 2.9% for Pimco’s Active Bond ETF (BOND) (Figure 7).

Figure 7 – BINC’s performance since inception has been strong (Seeking Alpha)

Impressively, BINC had minimal drawdowns during the June-October bond-market swoon, whereas AGG and BOND both suffered significant declines.

Why Bonds May Be A Buy?

As I have written in several recent articles, with the Fed “likely at or near the peak rate for this cycle”, according to Fed Chairman Jerome Powell at the December FOMC press conference, investors are betting that policy rates will decline in 2024, providing a boost to bonds in general.

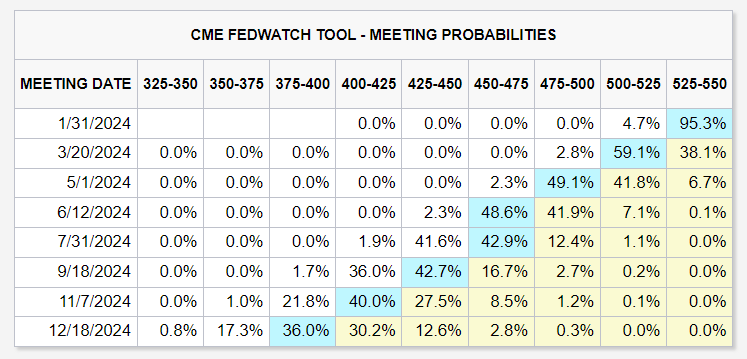

In fact, looking at the Fed Funds futures market, traders are betting that rate cuts will begin as early as March, with 6 cuts priced into 2024 (Figure 8).

Figure 8 – Traders have priced in 6 rate cuts (CME)

While expectations appear aggressive compared to the Fed’s forecast for 3 rate cuts in its December Summary of Economic Projections, a dovishly positioned Fed is a tailwind to bonds, so I believe the BINC ETF should perform well in the coming quarters.

Risks To BINC

However, the BINC ETF is not without risks. In general, I am hesitant to invest in rockstar managers, as they rely on a single individual to make differentiated macro ‘calls’ to generate outperformance.

This approach of ‘swinging for the fences’ is inherently unsustainable, as discussed in a recent article by Howard Marks titled “Fewer Losers, More Winners?”. By taking big swings, BINC’s star-manager approach may introduce returns volatility. As noted by Mr. Marks, “most investors aiming for top-decile performance eventually shoot themselves in the foot.”

While Mr. Rieder is currently the man of the hour having won Morningstar’s Outstanding Portfolio Manager award for 2023, history is replete with feted managers delivering poor performance.

Instead of a single star manager, I would be more comfortable investing in a proven investment process or a team of managers, as outperformance there may be more repeatable.

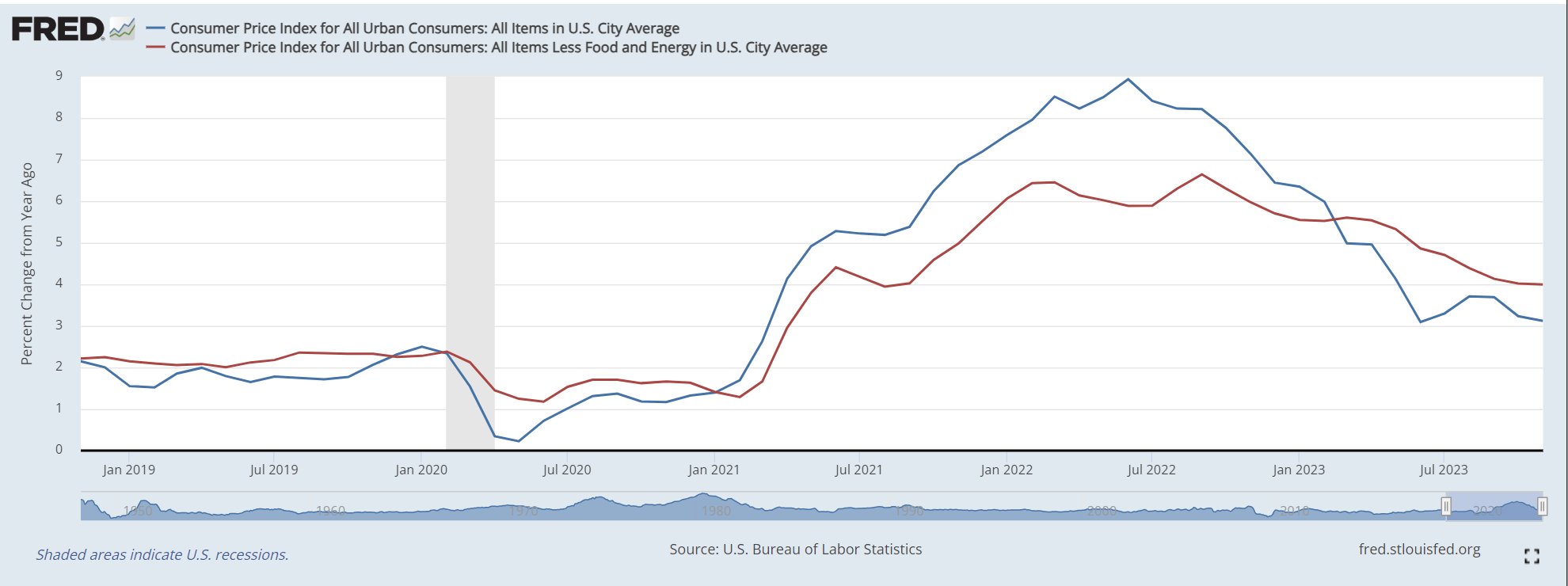

Another risk to BINC is if market expectations for a soft landing’ is incorrect and inflation makes a comeback, then the Fed may have to restart raising interest rates, which could put pressure on fixed income investments. Although headline CPI inflation has been moderating, with a 3.1% YoY rate in November, core inflation has been stickier, hovering around 4% (Figure 9).

Figure 9 – Core inflation stickier and may make a comeback (St. Louis Fed)

Conclusion

The BlackRock Flexible Income ETF is a recently launched actively managed ETF managed by star manager, Rick Rieder. The BINC aims to provide exposure to difficult-to-access fixed income sectors and is essentially a fixed income hedge fund.

So far, the BINC has delivered impressive returns in its short history, outperforming peer active bond funds like the Pimco Active Bond ETF. However, since BINC relies on its star manager to make differentiated macro ‘calls’ to select outperforming sectors, I am hesitant to recommend the fund without more performance data to analyze. I rate the BINC ETF a hold and will reassess the fund in future quarters.

Q2 2024 Earnings Call Transcript")