NoDerog/iStock via Getty Images

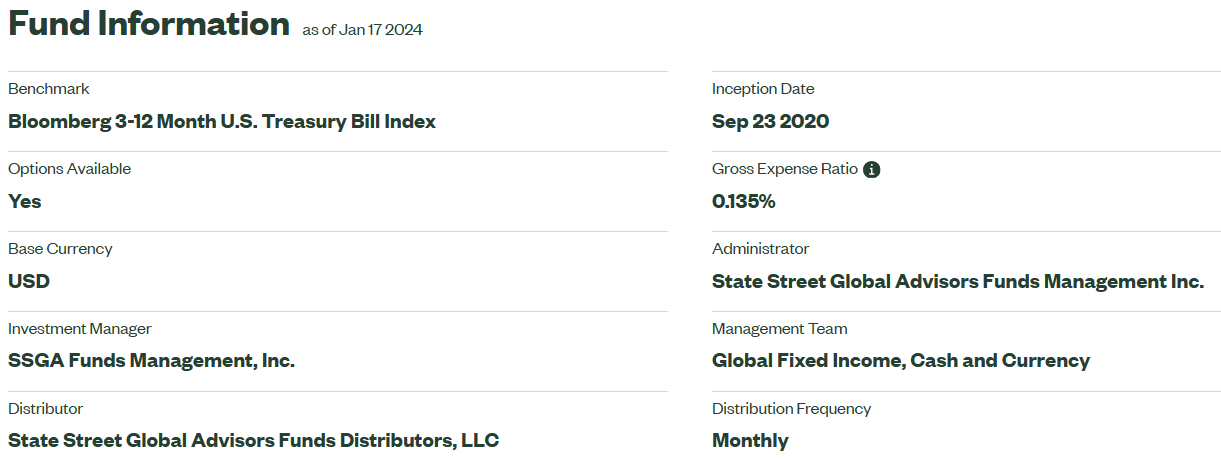

The Bloomberg 3-12 Month U.S. Treasury Bill Index comprises United States Treasury Bills with between 3 to 12 months left to maturity. The fund that we will be discussing today, SPDR® Bloomberg 3-12 Month T-Bill ETF (NYSEARCA:BILS), tracks this index. The description of the index on the fund website has a few redundancies, namely, that these bills are investment grade, denominated in USD, and have a fixed rate. The fund started in September 2020, has an annual expense ratio of 0.135% and makes distributions to its unitholders on a monthly basis.

BILS Website

Also noted on the fund website, is that the fund “seeks to provide investment results that, before fees and expenses, correspond generally to the price and yield performance” of the index. The part about the fees and expenses is significant when investors measure the fund’s success in tracking the performance of its benchmark index. This is because the index does not have any expenses, and the fund does not enjoy the same luxury. Comparing the performance of the two since the fund’s inception, we can say that the fund did meet its objective.

BILS Website

The fund lags slightly in each of the time periods, and that can be more or less explained by its 0.135% annual expense ratio. Let us look at the process followed by the fund to earn these results.

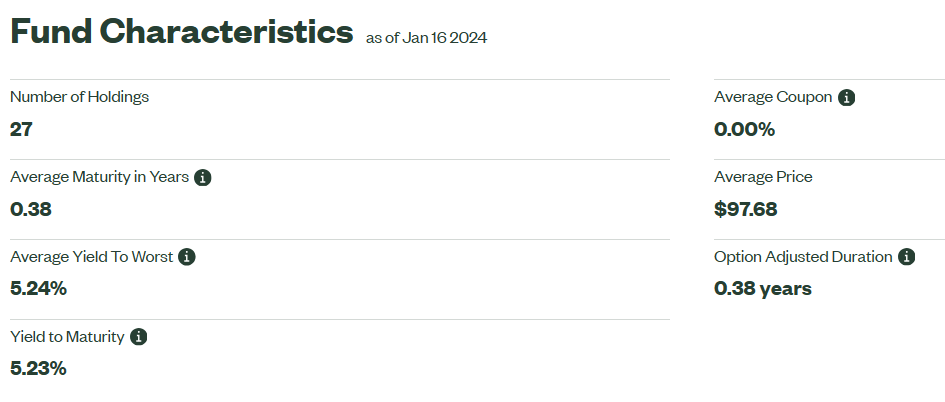

BILS builds its portfolio using the sampling methodology, i.e., it selects securities from the index that embody the risks and characteristics of the index as a whole. Depending on the market conditions and the total assets under management, the fund advisor has the leeway to switch to replicating the index i.e. buying all securities of the index proportionate to their weight in it. Typically, at least 80% of the fund assets are invested in securities from the index or those that are deemed to have “economic characteristics that are substantially identical” to the index securities. The balance assets can be held in cash or money market assets. At last count, BILS has 27 securities in its portfolio, and collectively they have a term to maturity of a little less than 4 months.

BILS Website

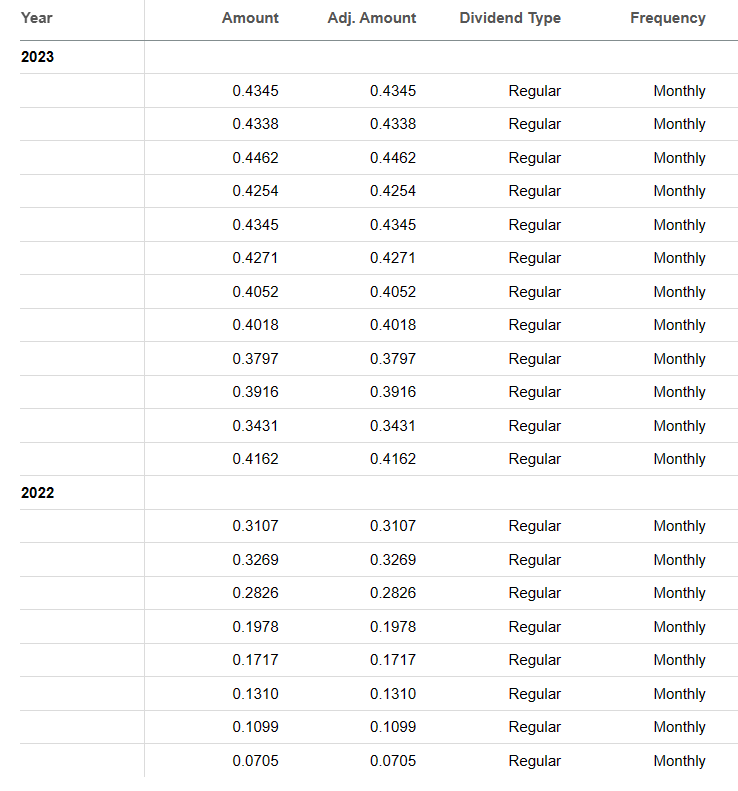

The average yield to maturity of the portfolio is 5.23%, and considering the annual expenses, the take home income is around 5.10%. As noted in the “Fund Information” graphic at the beginning of this piece, BILS distributes on a monthly basis. This amount has been trending upwards since June 2022.

Seeking Alpha

Fun fact, unitholders did not get any distributions prior to June 2022, which considering the interest rates at the time, makes sense.

Outlook & Comparatives

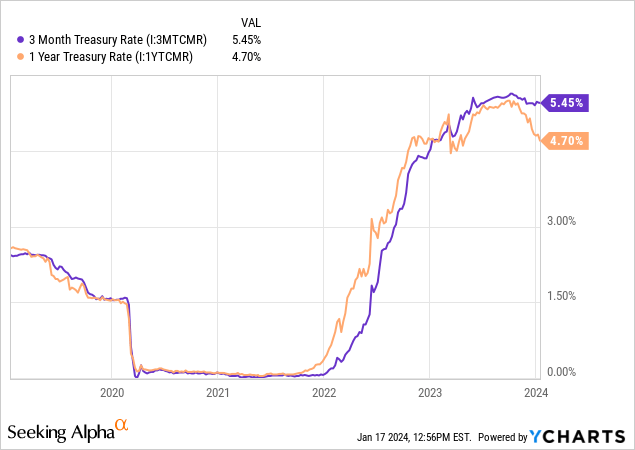

Coming back to the present day, based on the most recent distribution and the current price of $99.32, BILS yields 5.25%. While the average yield to maturity net of expenses for BILS comes to around 5.10% (explained earlier in this piece), the fund’s last distribution yielded higher than that. This is because the distributions lag the net earnings. Just like we saw a rising trend in the distributions from 2022, in conjunction with the rise in interest rates, the distributions will dip in the future to line up with the lower net earnings. The depth of the dip will depend on magnitude of cuts by the Federal Reserve. The guy at the helm believes the rates at the short end of the curve will be 4.6% at the end of this year.

The appropriate level [of the federal funds rate will be 4.6% at the end of 2024″ if the Fed’s economic projections hold up, Fed Chair Jerome Powell said during a conference call to discuss December’s decision.

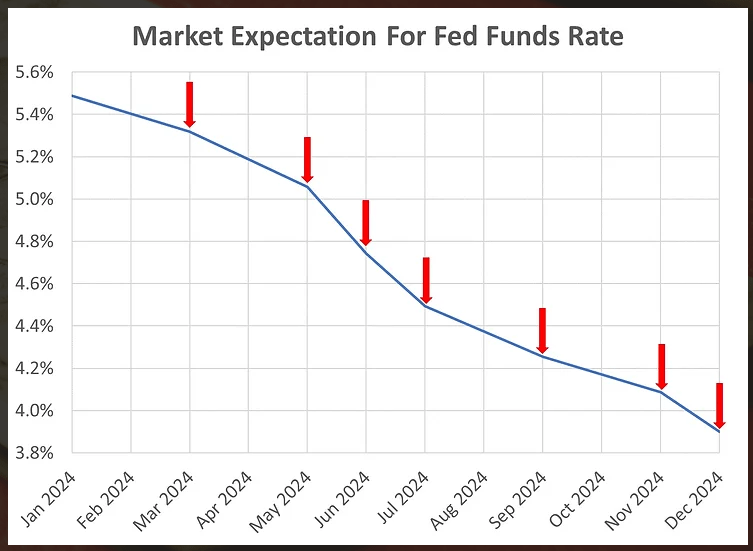

The market is more optimistic and has priced in 7 cuts in 2024, with the year ending at 3.9%.

AllQuant

Of course, the last time they cut rates 7 times was in 2008, and we all know what that was like. So “optimistic” might not be the correct word here. BILS is well positioned for this on a relative basis, especially if the rate cuts don’t pan out. It is sticking to the short end of the duration curve, even within its mandated range. As a result, it is not buying bills which have heavily priced in these cuts. So the SPDR® Bloomberg 3-12 Month T-Bill ETF remains a decent choice for those that believe that rate cuts of this magnitude will not occur. For those that concur that these rate cuts will occur, they should be indifferent to holding either BILS or a 1-year Treasury ETF.

Finally, for those thinking that even these rate cuts forecasted understate what will actually happen, may want to buy 2-year Treasuries (US2Y). Those 2-year Treasuries are paying you almost exactly the same as the 30-year Treasuries (US30Y).

The last two times the spread “uninverted” were extremely “exciting” times. Maybe we will have threepeat. SPDR® Bloomberg 3-12 Month T-Bill ETF is a good place to hide out regardless, and the only way you do significantly better in the 2-year Treasury is if we hit full-on Armageddon.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Q2 2024 Earnings Call Transcript")