Stanley Druckenmiller bets on themes. Well, he does a lot of other things, but when he invests in individual stocks, he typically buys because of a multi-year secular theme. It can pay to listen to the legendary investor and former right-hand man to George Soros, too, as he has put up phenomenal stock returns over the long haul. In the 30 years of running outside money for Duquesne Capital Management, he has averaged a 30% annual return while never having a down year.

Today, Druckenmiller is only managing his own capital through the Duquesne Family Office. But he is still investing the same way. As of his latest 13-F filing, the family office had a concentrated portfolio, mainly of technology stocks. Two of his largest positions — Nvidia and Microsoft — have been highly profitable bets on the growth of artificial intelligence (AI) and cloud computing. Nvidia is his largest position, while Microsoft is his third. Both make up over 10% of the family office’s portfolio.

These two stocks are recognizable names with market capitalizations of over $1 trillion. But Druckenmiller’s second-largest position is small and not even operating in the United States, his home country. The stock is Coupang (CPNG -2.71%), the largest e-commerce operator in South Korea with plans to expand in East Asia. What does Druckenmiller see in Coupang stock? Let’s find out.

Why Coupang?

According to CNBC, Druckenmiller became an investor in Coupang years before it went public in 2021. Since its debut on the public markets, Druckenmiller has held on to most of his position, indicating he is still bullish on the stock after all these years.

So what has him so bullish? I think a few things. First, the company is operating in a fast-growing sector: online shopping in South Korea. Coupang’s revenue has gone from essentially zero 10 years ago to over $20 billion today. It is rapidly gaining market share in its home country, with a long runway for reinvestment ahead. The Korean commerce market (both offline and online) is approximately $500 billion. If Coupang keeps gaining market share in e-commerce while more and more shoppers shift from in-person to online shopping, the company still has many years left to grow.

Second, the company has a fantastic founder running the business named Bom Suk Kim. Kim started Coupang and still runs the business as CEO today, overseeing its domination of the South Korean market. Founder-led businesses have been shown to outperform the average stock. Investors should want Bom Suk Kim to stick around at Coupang for many, many years.

Expanding into Taiwan

Coupang started out with an intense focus on its home market, South Korea. Now, it is slowly expanding to other countries in East Asia. First is Taiwan, an island nation with a similar geographic density to South Korea. On the latest earnings call, Coupang’s management said it was increasing its investment in Taiwan after seeing rapid growth in the region. The Coupang mobile app is projected to be the most downloaded app in all of Taiwan for 2023.

In the short run, heavy investments into Coupang may lead to widening losses. Coupang’s “developing offerings” business segment saw its adjusted loss of earnings before interest, taxes, depreciation, and amortization (EBITDA) loss widen to $160 million compared to $44 million in 2022. But over the long run, it will expand Coupang’s revenue and earnings potential. Investors interested in Coupang will want to track revenue growth from the developing offerings segment to validate the Taiwan expansion. Last quarter, segment revenue grew 41% year over year.

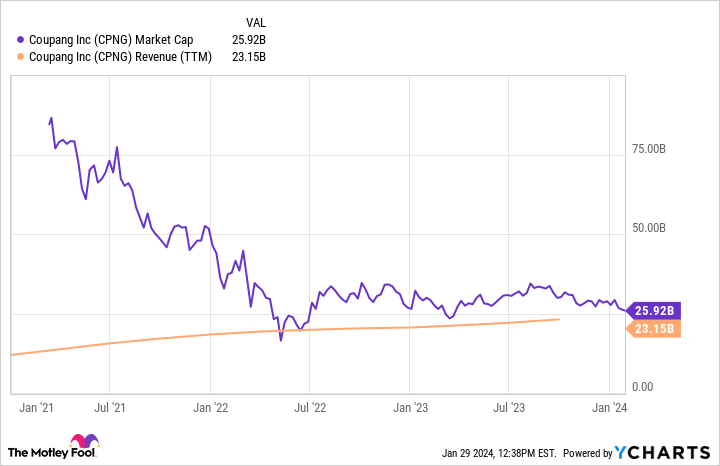

CPNG Market Cap data by YCharts

The stock looks dirt cheap

Lastly, Druckenmiller is likely still attracted to Coupang because the stock looks cheap. Shares are down 71% from all-time highs, and its market capitalization is now just $26 billion.

In 2023, Coupang should generate close to $25 billion in revenue, depending on the currency fluctuations of the Korean won and U.S. dollar. Over the long term, management expects the business to hit around 10% profit margins. The company is already showing progress in this regard, with net income hitting a margin of 1.5% last quarter despite the heavy losses coming from the Taiwan expansion. Its core produce commerce segment had an adjusted EBITDA margin of 6.6% last quarter.

A 10% profit margin on $25 billion in revenue is $2.5 billion in bottom-line earnings. Compared to a market cap of $26 billion, that gives Coupang a forward price-to-earnings ratio (P/E) of 10.4. For a company growing revenue at a fast rate (21% year over year last quarter) and with such a large market opportunity ahead of it, Coupang stock looks undervalued at these levels.

The time is right to bet along with Druckenmiller. Today looks like a great buying opportunity in Coupang stock for investors who plan to hold on to their shares for many years.

Brett Schafer has positions in Coupang. The Motley Fool has positions in and recommends Coupang, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")