champpixs

Growth and innovation stocks are one of my favorite plays in 2024. Many of them have seen a complete cycle of boom and bust and are recovering again. Lower rates and a dovish Fed should provide a positive backdrop which could last several years.

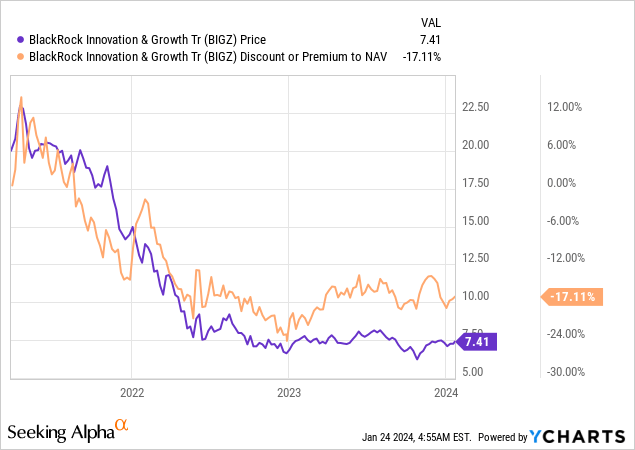

I’ve been searching for ways to position for a possible rally and one of the most interesting vehicles I have found is the BlackRock Innovation and Growth Term Trust (NYSE:BIGZ). This Closed End Fund fell 73% as the growth/innovation bubble burst and only bottomed in October 2023. It has recovered slightly, but prices are still subdued and there is an opportunity to get in right at a potential bottom. Best of all, it is trading at a -17% discount to NAV.

Boom and Bust

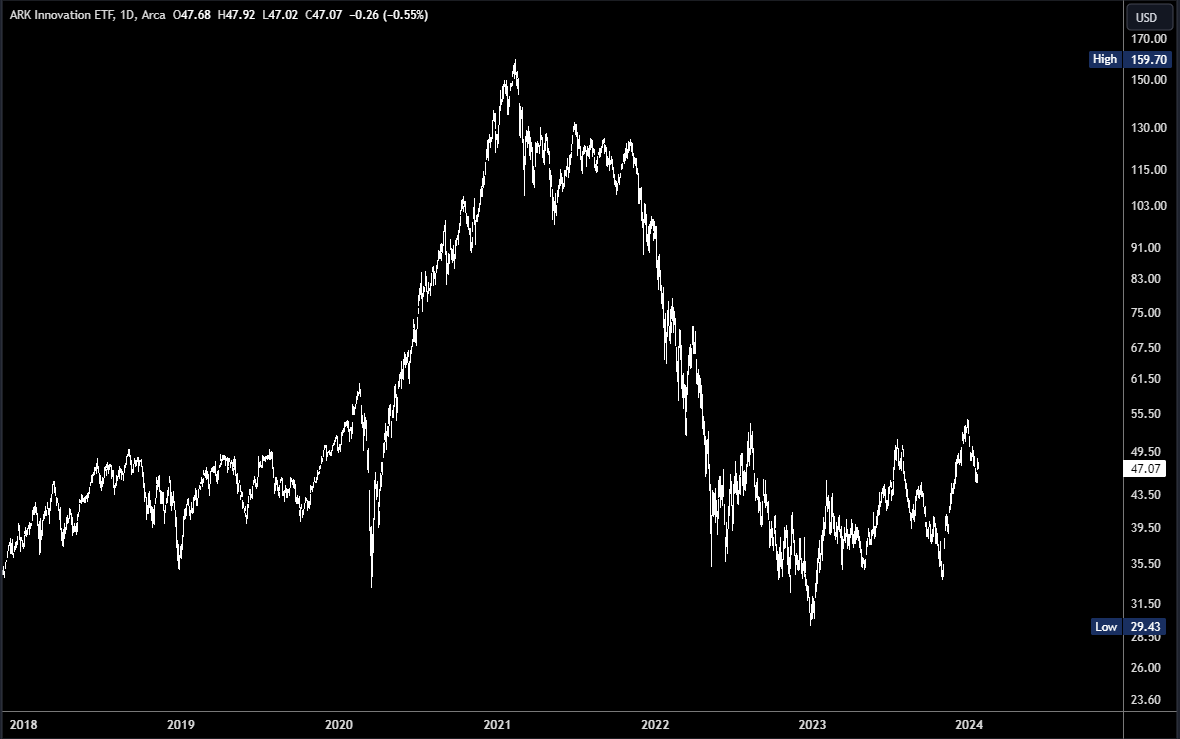

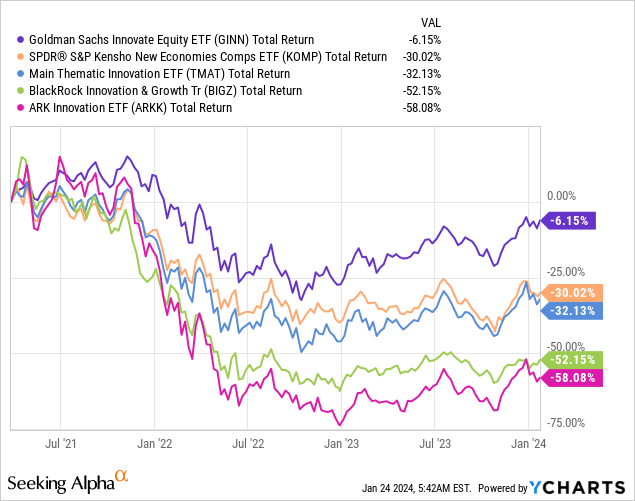

The boom and bust cycle in growth and innovation stocks is best illustrated by the ARK Innovation ETF (ARKK), actively managed by Cathie Wood. This could do no wrong in the post-pandemic era of ZIRP, but the bubble popped in early 2021 and the entire rally has been unwound.

ARKK Boom and Bust (Tradingview)

Dropping from $159.70 to $29.43 reset the frothy valuations and it looks like a bottom was made in late 2022. There has been a tentative recovery but I think there should be much more to come as yields have almost certainly topped and the Fed have signalled rate cuts are on the way this year. High duration growth stocks should benefit.

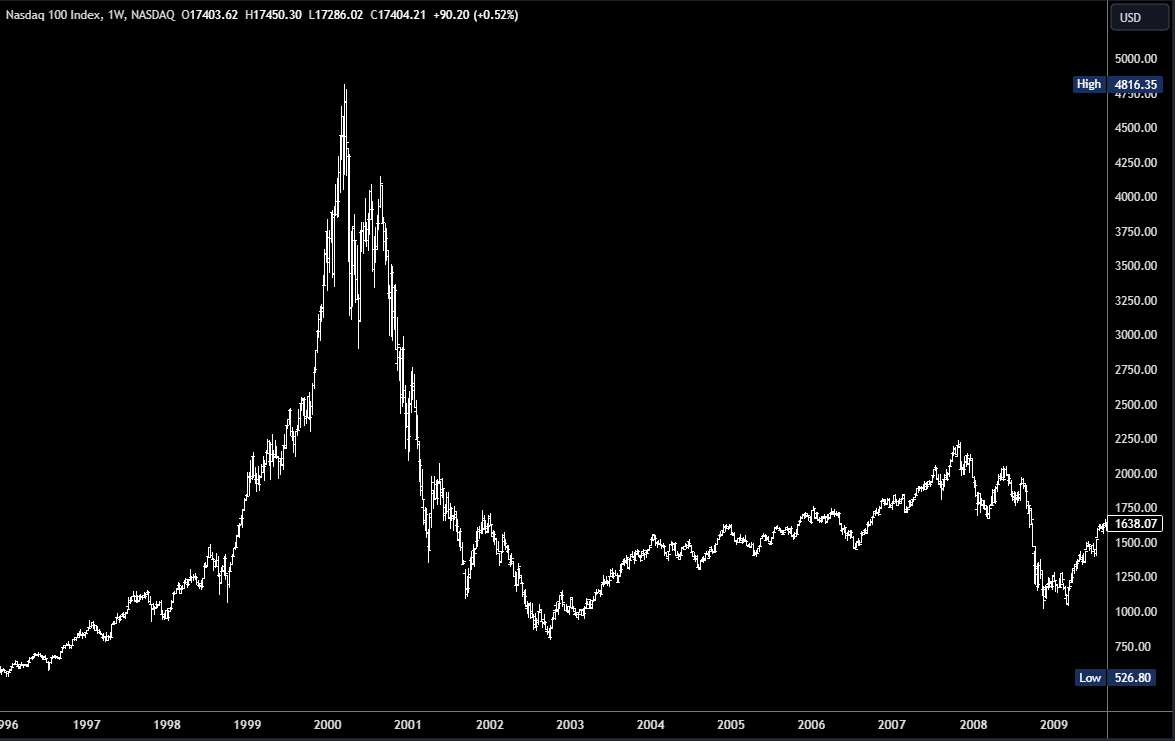

There are various scenarios that could play out following the boom and bust cycle. In individual stocks the company may actually go bust. However, in commodities, indexes and funds, this can’t really happen. The worst that could happen in a closed end fund like BIGZ is the assets (stocks) are sold and paid to the shareholders. A slow recovery is much more likely and the Nasdaq (QQQ) pattern from the 1990s-2000s boom and bust is similar to what we see in ARKK now.

Nasdaq Boom and Bust (Tradingview)

The recovery may look weak due to the size of the preceding drop, but there was still a +172% rally from the 2002 low into the 2007 top, and of course, much more later. Buying after the bust phase can lead to huge gains.

Why BIGZ?

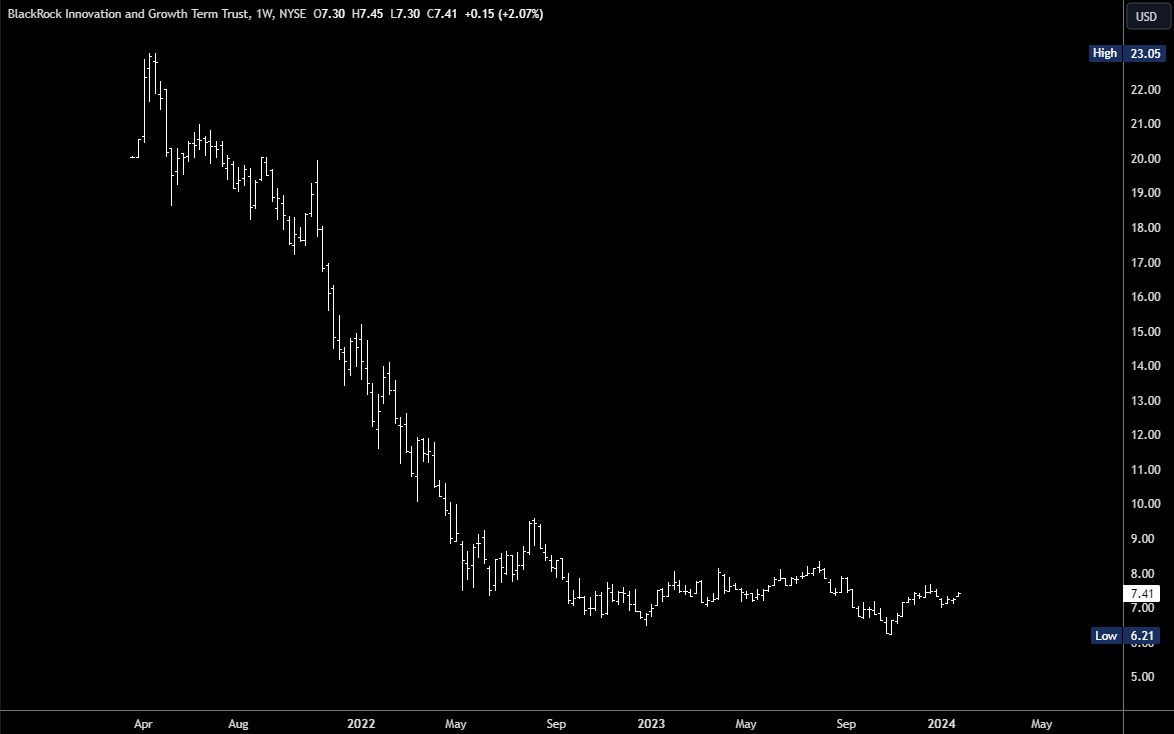

While the likes of ARKK should do well in the coming years, it is already over 60% above the bottom made in 2022. BIGZ bottomed much later in October 2023 and is only around 20% from its low. This provides an opportunity to get in near a multi-year low before the herd arrives and pushes up prices.

BIGZ Weekly Chart (Tradingview)

Admittedly, this shows BIGZ is relatively weak, and I will investigate the possible reasons later. This weakness is also reflected in the large discount to NAV of 17%.

BIGZ was unlucky to IPO in March 2021 just as the growth/innovation bubble was popping. It lost 68% of its value in under two years. This was a sector-wide downtrend rather than anything specific to BIGZ and it would have been almost impossible to populate a growth and innovation fund without taking heavy losses. That said, BIGZ did take fall further than most other growth / innovation funds.

BIGZ has been consistently underperforming, and this is concerning. It certainly merits further investigation.

A Closer Look at BIGZ

BIGZ is an actively managed closed end fund with around $2B in AUM. As per the fund’s page,

The Trust will invest primarily in equity securities issued by mid- and small-capitalization companies that the Trust’s adviser believes have above-average earnings growth potential. In selecting investments for the Trust, the Trust’s adviser focuses on mid- and small-capitalization growth companies that are “innovative.” These are companies that have introduced, or are seeking to introduce, a new product or service that potentially changes the marketplace. companies that have introduced, or are seeking to introduce, a new product or service that potentially changes the marketplace.

So far, so clear, but this is far from an ordinary fund. The Prospectus and other documents from the fund’s page, reveals some important characteristics.

Holdings in Private Companies

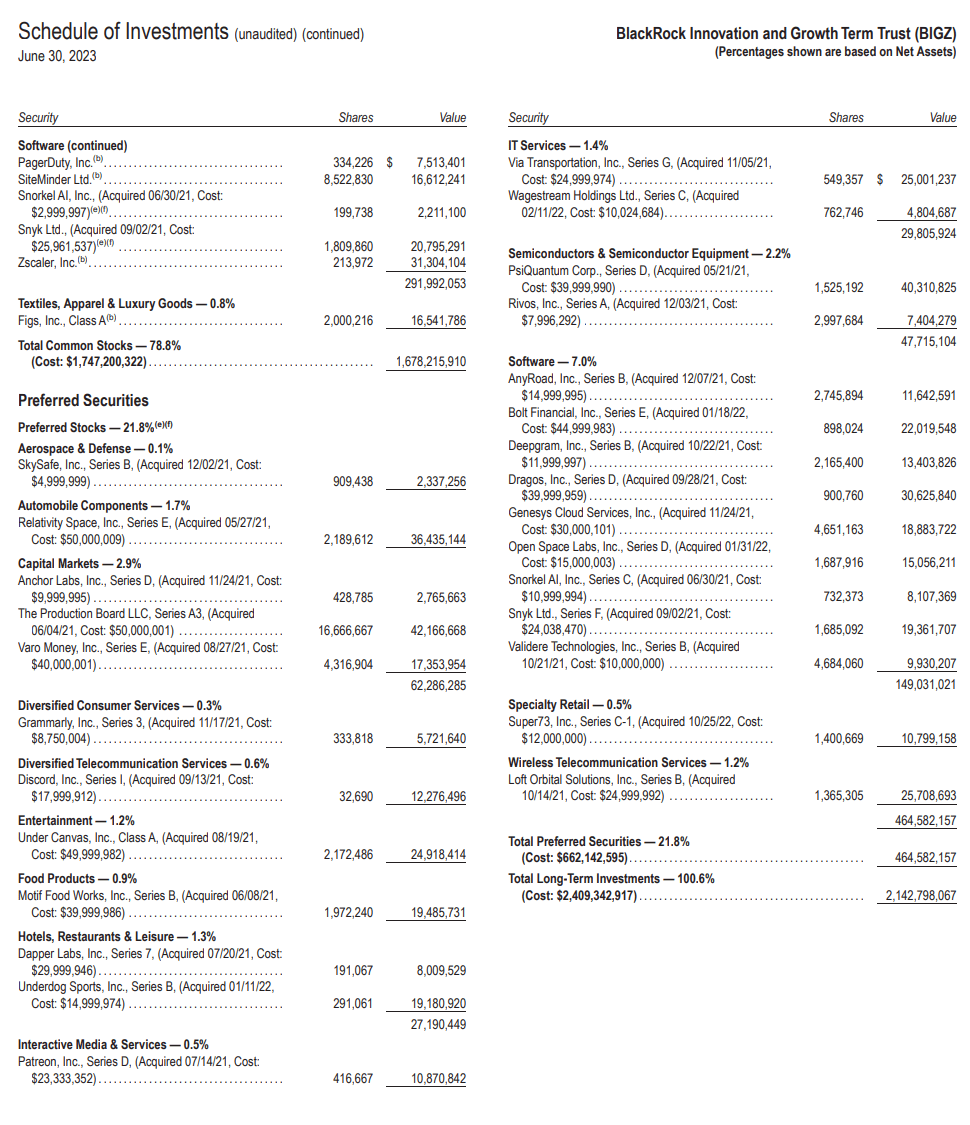

While the top 10 holdings contains some recognizable mid-cap names such as Axon Enterprise (AXON), BIGZ also invests in small private companies.

The Trust may invest in shares of companies through initial public offerings (“IPOs”). The Trust may also invest, without limit, in privately placed or restricted securities (including in Rule 144A securities, which are privately placed securities purchased by qualified institutional buyers), illiquid securities and securities in which no secondary market is readily available, including those of private companies. Issuers of these securities may not have a class of securities registered, and may not be subject to periodic reporting, pursuant to the Securities Exchange Act of 1934, as amended. Under normal market conditions, the Trust currently intends to invest up to 25% of its total assets, measured at the time of investment, in such securities.

Basically, it is up to 25% venture capital. The 2023 annual report is not yet available with a full list of investments, but the 2022 semi-annual report shows the holdings under “preferred securities.”

Preferred Securities (BIGZ Annual Report)

The value of these shares are hard to evaluate as they are not decided by markets. The value of BIGZ, however, is decided by the market and is consistently below the NAV it reports. That could be partly due to sentiment and lack of buyers in this beaten down sector, but it also shows the market believes the NAV is inflated or inaccurate.

Holdings Outside the US

BIGZ currently holds 93% of its investments in the US, with the UK second at 2.14%. It is worth noting, however, that,

The Trust may invest up to 25% of its assets in securities of foreign companies, including companies located in emerging markets. Foreign securities in which the Trust may invest may be U.S. dollar-denominated or non-U.S. dollar-denominated.

Leverage

There is no leverage yet on its books, perhaps as rates are high, but the fund has the option to take on sizeable debt.

The Trust currently does not intend to borrow money or issue debt securities or preferred shares. The Trust is, however, permitted to borrow money or issue debt securities in an amount up to 33 1/3% of its Managed Assets (50% of its net assets), and issue preferred shares in an amount up to 50% of its Managed Assets (100% of its net assets). “Managed Assets” means the total assets of the Trust (including any assets attributable to money borrowed for investment purposes) minus the sum of the Trust’s accrued liabilities (other than money borrowed for investment purposes). Although it has no present intention to do so, the Trust reserves the right to borrow money from banks or other financial institutions, or issue debt securities or preferred shares, in the future if it believes that market conditions would be conducive to the successful implementation of a leveraging strategy through borrowing money or issuing debt securities or preferred shares.

Writing Options

BIGZ utilizes an option writing (selling) strategy in an effort to generate gains from options premiums. In the semi-annual report nearly $16m of options were listed as liabilities on its books.

Distributions

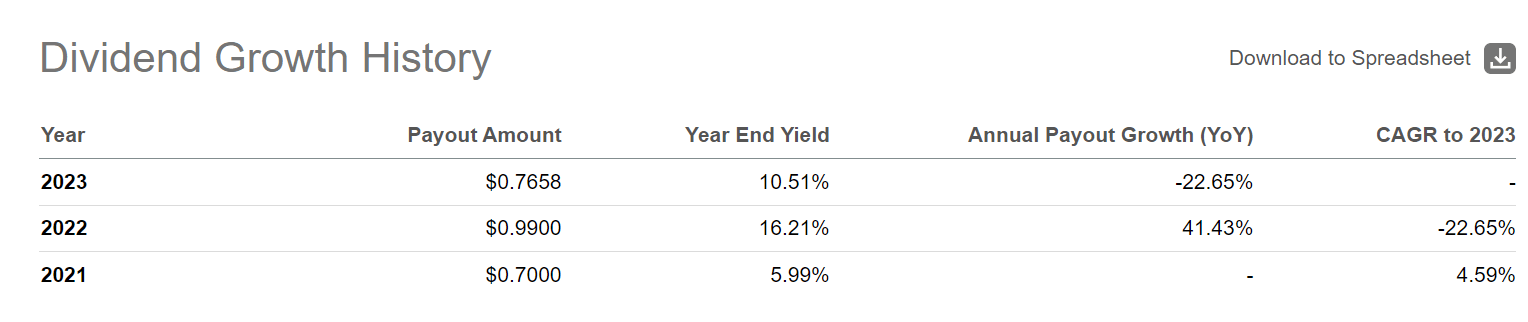

I was surprised to see BIGZ pays out a monthly dividend with a yield (FWD) of 7.24%. Obviously this isn’t coming from its holdings and as per the latest distribution document from January 2024:

The Fund estimates that it has distributed more than its income and net-realized capital gains in the current fiscal year; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the shareholder’s investment is paid back to the shareholder.

The pay-out varies greatly. Quite clearly, this is not a fund to hold for reliable passive income.

BIGZ Distributions (Seeking Alpha)

Share Buybacks

Since the initial Repurchase Program’s inception in 2016, BlackRock has repurchased approximately $1.3 billion in shares across the closed-end fund complex. This intends to enhance shareholder value by purchasing Fund shares trading at a discount from their NAV.

It has so far repurchased 18,909,732 BIGZ shares for $176,860,365.

Other Considerations

As an actively managed fund, the expense ratio is quite high at 1.35%. However, given the volatility, this isn’t a major consideration.

Liquidity, on the other hand, is always a concern. With 1,124,330 shares traded on average, this shouldn’t be much of an issue.

One last consideration is BIGZ is a “term trust” with a 12-year limited term, subject to extension. I guess this depends on whether or not the fund is successful over its first 12 years.

Conclusions

BIGZ has big potential as the growth and innovation sector could make a comeback in 2024. It has underperformed its peers and trades at a big discount to NAV, mostly due to its holdings in private companies.

The fund provides the management with the capacity to invest in almost anything “innovative” in any country, use leverage, write calls, buyback shares and issue dividends. It places a lot of trust in the management, and so far, this approach has led to underperformance.

BIGZ is always going to be a high risk, high reward play, but I would need to see more evidence of relative strength and outperformance to be confident in this fund and consider buying.

Q2 2024 Earnings Call Transcript")