champc

Introduction

I’m constantly looking for undervalued microcap companies, and recently I came across BGSF (NYSE:BGSF). It’s a US consulting and staffing solutions firm which has been focusing on improving margins over the past few years, and the adjusted TTM EBITDA stands at $23.9 million. BGSF has a dividend yield of $6.3 million and the balance sheet looks strong, with net debt at $66 million on October 1. I’m putting BGSF on my watchlist and my rating on the stock is a speculative buy. Let’s review.

Overview of the business and financials

BGSF was established in 2007 and specializes in the provision of consulting, managed services, and professional workforce solutions to various industries. The company has a network of 89 offices across the USA and operations in 44 states. The business has a client retention rate of about 86% and is split into two segments – Property Management, and Professional. The Property Management focuses on office and maintenance field talent solutions for apartment communities and commercial buildings. The Professional segment, in turn, offers specialized talent and business consultants for IT, managed services, finance, accounting, legal, and human resources.

BGSF

There is some seasonality in the business of BGSF, as revenues of the Property Management workforce solutions business are typically higher in the summer due to increased turns in multifamily units due to the summer break. In addition, the company’s cost of services usually rises in the first quarter of the fiscal year as a result of the reset in payroll taxes.

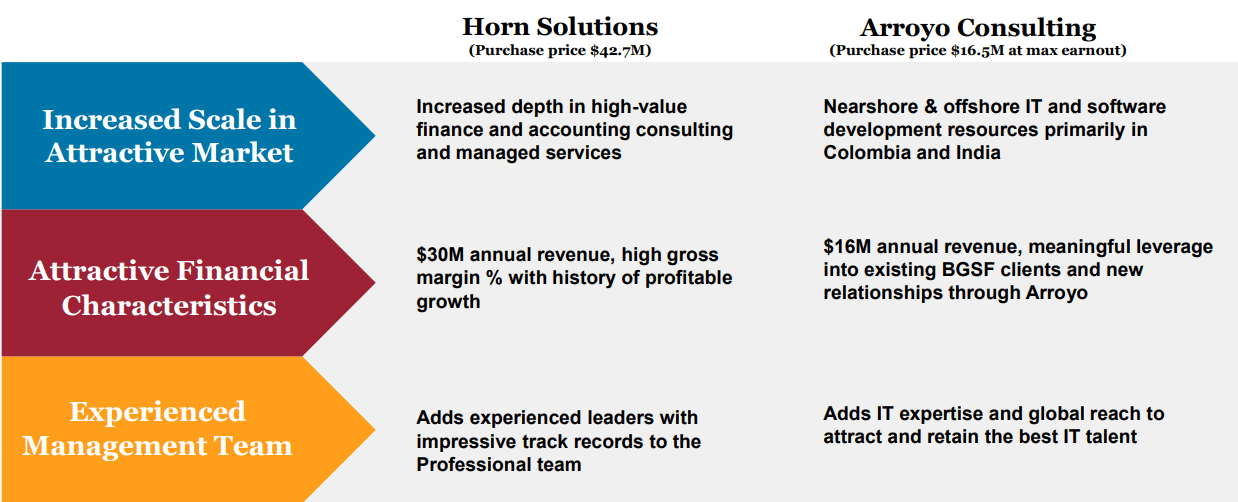

BGSF has been pivoting to high-end, specialized consulting services over the past few years, and its growth strategy includes both organic growth and acquisitions. The latest two acquisitions included Texas-based Horn Solutions and Arroyo Consulting. Horn Solutions was bought in December 2022 for $42.7 million and added revenues of about $30 million. Arroyo Consulting, in turn, was acquired in April 2023 for $6.8 million and added $16.2 million in annual revenues.

BGSF

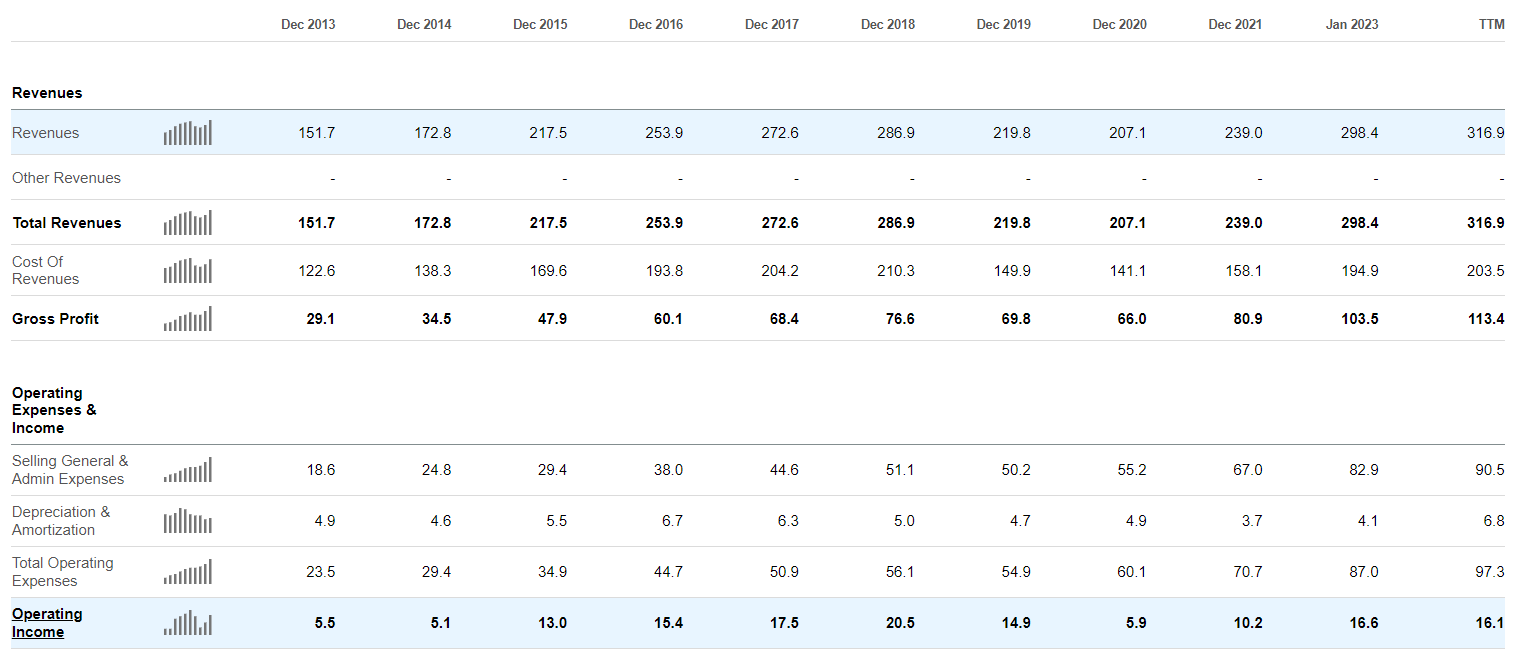

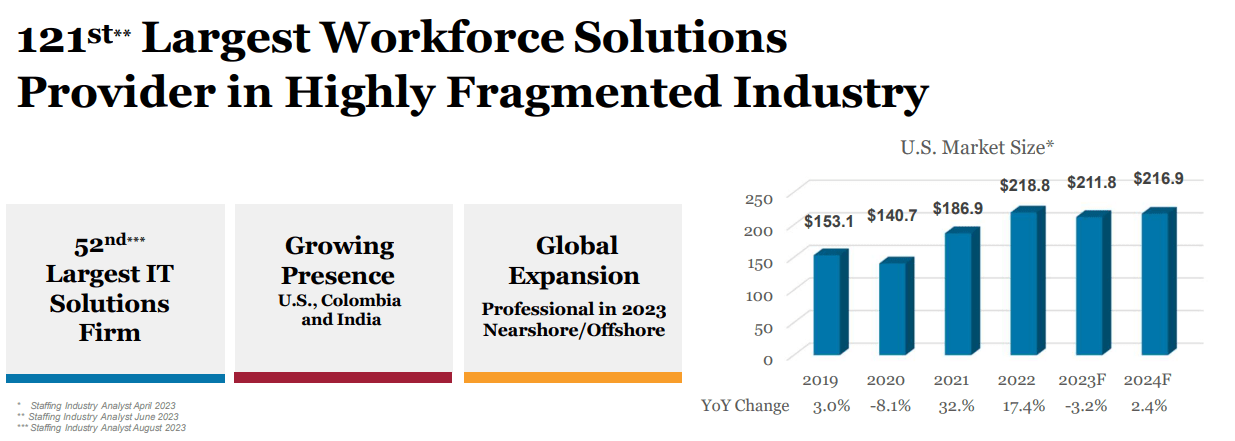

As you can see in the table below, annual revenues have grown by almost $110 million since the end of 2020 while the operating income margin has improved to 5.1% from 2.8%. In my view, this is a market with low barriers to entry and tight margins, and having a national footprint gives BGSF a decent moat. There are currently about 25,000 staffing firms in the USA and around 200 of them have revenues of over $100 million per year (see slide 7 here). With low-margin businesses in fragmented industries, economies of scale are crucial for profitability.

Seeking Alpha

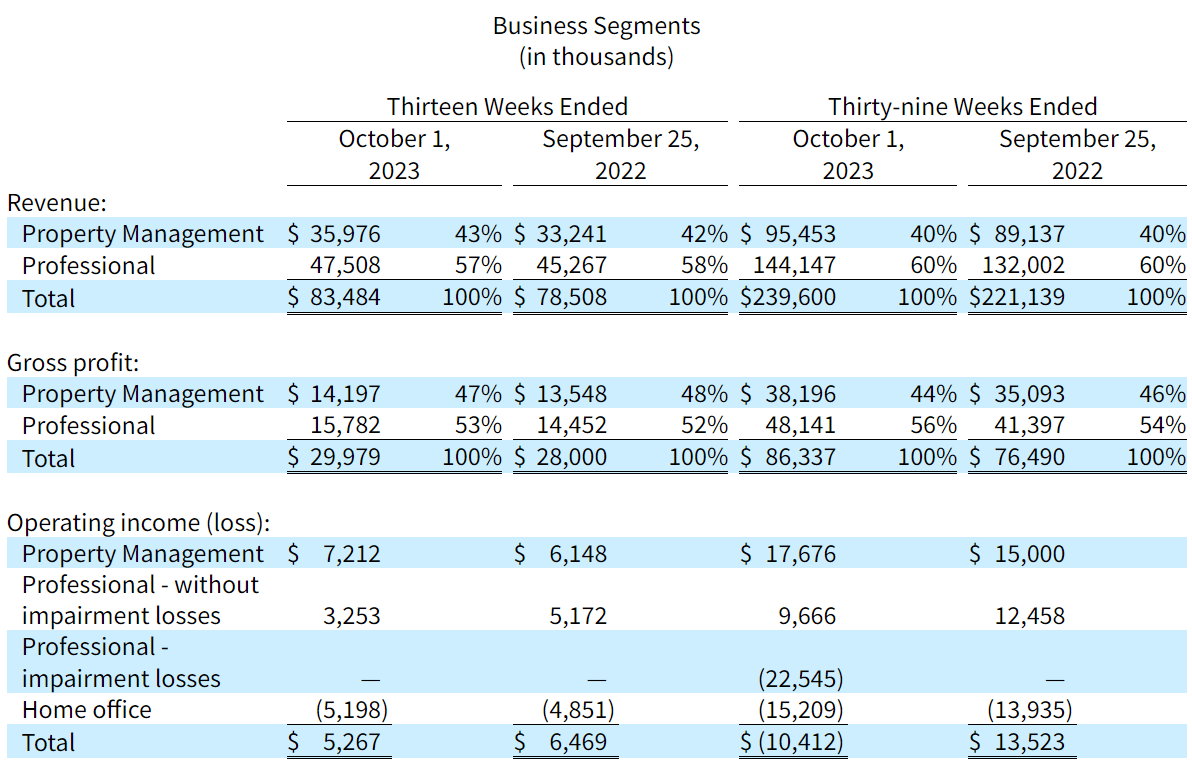

Turning our attention to the latest available quarterly financial results, we can see that both the Property Management, and Professional segments experienced decent growth in Q3 2023 as total revenue went up by 6.3% to $83.5 million. The revenue of the Property Management business rose by 8.2% to $36 million as BGSF increased billing rates. The Professional segment, in turn, booked a 5% increase in revenues to $47.5 million. I find this growth disappointing considering Horn Solutions and Arroyo Consulting added revenues of $11.6 million (see page 28 here). The soft demand in this segment also shrank the operating income of BGSF by 18.6% year-on-year to $5.3 million.

BGSF

Looking at the balance sheet, we can see that the situation has improved since the start of 2023 despite the purchase of Arroyo Consulting and keeping the quarterly dividend at $0.15 per share. The net debt decreased from $66.7 million on January 1 to $66 million on October 1 as operating cash flow for the period was $13.1 million (see page 4 here).

Overall, I think this was a mixed quarter for BGSF. On one hand, the Property Management business had good organic growth and the strength of the balance sheet is improving. On the other hand, demand in the Professional segment was soft. Yet, I think the dividend here is safe. Considering the quarterly dividend payments are just $1.6 million, I think that the dividend payment is unlikely to be slashed in the near future.

Turning our attention to the valuation, I think that BGSF seems undervalued at the moment from a fundamentals standpoint. The company has an enterprise value of $169.7 million as of the time of writing, while the TTM adjusted EBITDA from continuing operations stands at $23.9 million. This translates into an EV/EBITDA ratio of 7.1x. In my view, BGSF has a high dividend yield, a decent moat, a solid balance sheet and improving margins and should be trading at about 8x EV/EBITDA. This is equal to $11.57 per share, or an upside potential of 21.1%.

Looking at the downside risks, I think the major one is that a cooling off in the US labor market could create headwinds for the staffing industry, pushing down revenues and margins for most of the companies in it. This tight labor market has boosted the size of the sector since 2021, and I’m concerned that it could fall to 2020 levels in a few years.

BGSF

I’m not too concerned about the weakness in the Professional segment yet. As BGSF explained during the Q3 2023 earnings call, it was a tough comparison as the segment benefitted from macro tailwinds in Q3 2022 and its revenues rose by 14.9% year-on-year back then. That being said, it’s worth keeping an eye on the matter.

Investor takeaway

BGSF is a relatively large consulting and staffing solutions firm that has managed to improve its operating margins over the past few years. It has a high dividend yield and a strong balance sheet, and I think that the mixed financial results over the past few quarters have opened a buying opportunity here. The market capitalization has decreased by over 37% in the past year, and BGSF is trading at just 7.1x EV/TTM adjusted EBITDA from continuing operations.

Q2 2024 Earnings Call Transcript")