phive2015

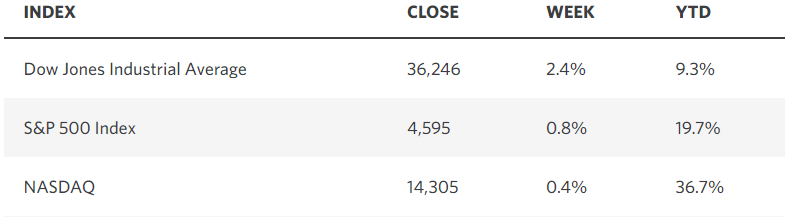

For months I have recommended that investors focus on what the Fed does and not what its officials say because the statements are designed more to supervise expectations than furnish specific policy guidance. This has been a trap for bears who for the past year have interpreted Fed rhetoric, which is typically hawkish, in a literal sense. It has been particularly painful over the past five weeks, as the S&P 500 (NYSEARCA:SPY) and Dow Jones Industrials (DIA) hit new closing highs for the year on improving breadth. Breadth was the missing ingredient until this latest surge in stock prices, which now has the equal-weighted S&P 500 up more than 7% on the year. The consensus of investors is now recognizing what I have been preaching all year long, which is that inflation is falling as fast as it rose, while the rate of economic growth is decelerating under the weight of tighter financial conditions but not to the point that a recession is on the horizon.

Edward Jones

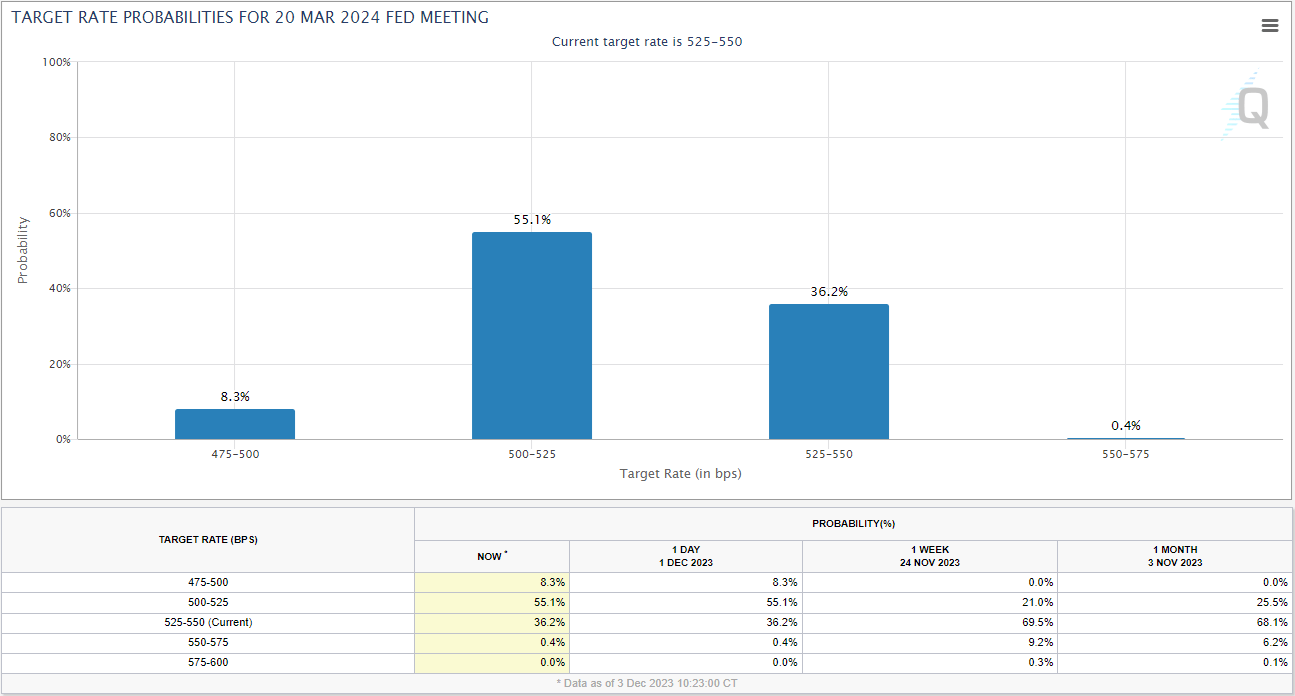

As expected, Chairman Powell tried to temper the rally on Friday by suggesting that the Fed may have to raise rates advocate if appropriate and that speculating about rate cuts was premature. Investors are not buying that anymore. One week ago, I stated that I expect to see the Fed start cutting interest rates much sooner than the consensus expects with the first coming as soon as the March meeting. After inflation numbers for November were reported on Thursday, investors raised the probability of the first rate cut coming in March from 21% to 55%.

CME

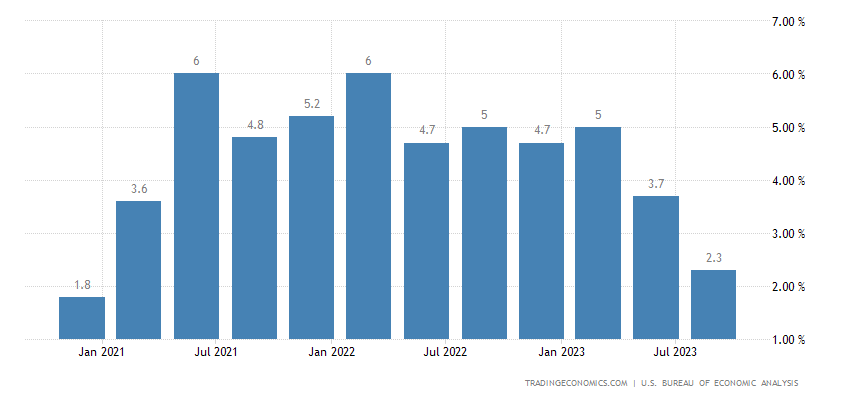

Powell’s words were ineffectual in deflating expectations for rate cuts because the writing was on the wall. The core personal consumption expenditures (PCE) price index report for October, which was released on Thursday, showed that the Fed’s preferred measure of inflation decelerated advocate to 3.5%. Furthermore, this measure increased just 2.3% from the second quarter to the third, which means we are within the goalposts of the Fed’s target already. This is why the Fed can and should start to regularize rates.

TradingEconomics

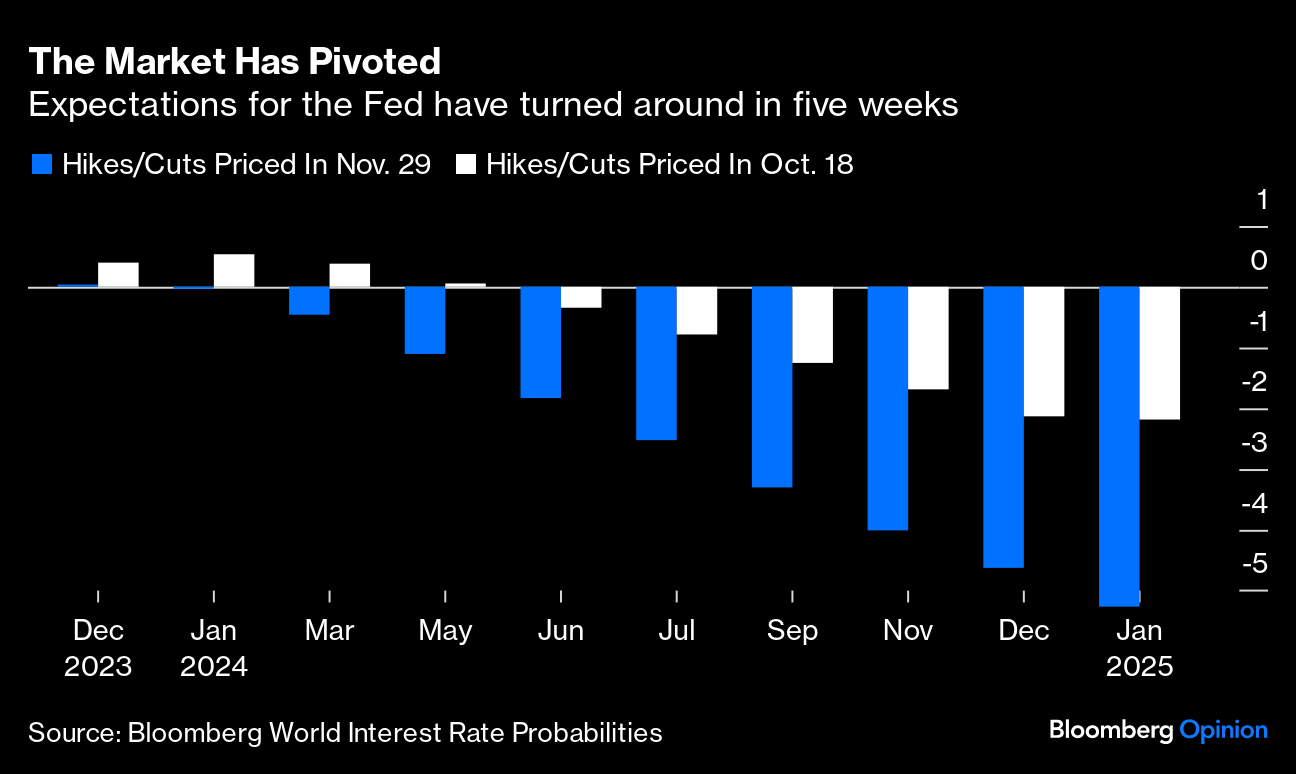

This is why the Fed can and should start to regularize rates soon unless it wants to make the same mistake twice by waiting too long to react to the underlying trend. The Fed was far too slow and too late in raising rates during the surge in prices, failing to confess the impact fiscal stimulus would have on consumer demand for goods and services. It needs to recognize that the delayed impact of its rate hikes will be felt as it reaches its inflation target ahead of plan. Growth is likely to decelerate below trend during the first half of the year, which is why the market has gone from pricing in just two rate cuts a few weeks ago to five now. I think once the Fed starts reducing rates, it will not stop until it reaches a neutral policy rate closer to 3%.

Bloomberg

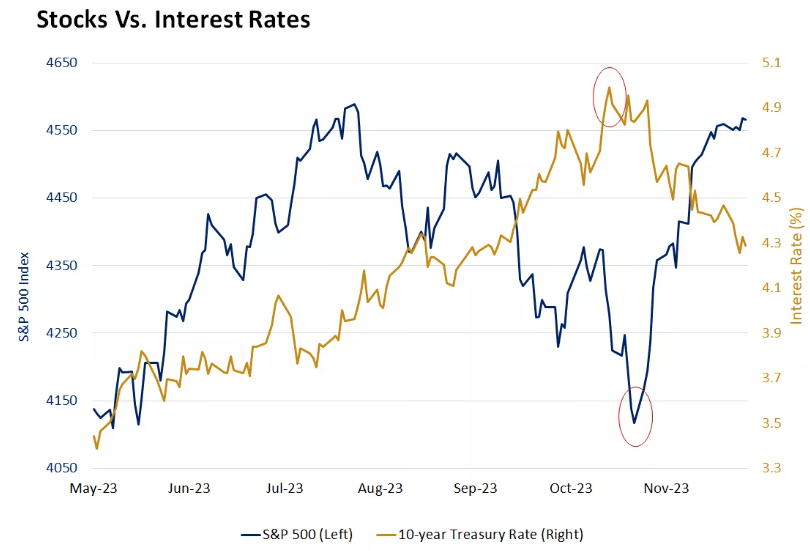

The rapid reject in long-term interest rates is what powered the five-week rally in stocks and bonds after the 10-year yield peaked at 5%. Short-term rates are falling as well, which tells us that the Fed will be cutting rates sooner than it is willing to admit. Short rates are likely to fall faster than long rates, steepening the yield curve once the 2-year falls below the 10-year yield. That normalization is no reason for alarm, but bears are bound to suggest it means recession is on the horizon.

Edward Jones

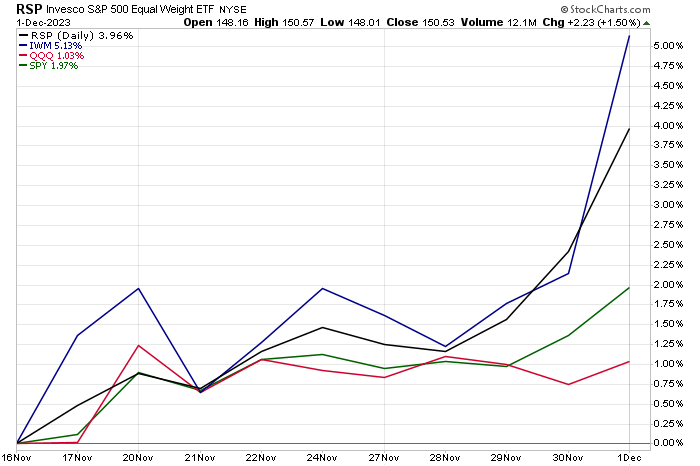

An important development over the past two weeks, which is one I’ve been anticipating for some time, is the rotation from the Magnificent 7 members of the S&P 500 to the remaining 493, as well as the rest of the broad market’s constituents. The evidence is gradually strengthening market breadth and the near-term leadership change between major market indexes. While it is early, it is very encouraging. Note below that over the past two weeks, the Nasdaq 100 (QQQ), which is home to the Magnificent 7, has risen just 1%. Meanwhile, the S&P 500 has risen nearly 2%, while the equal-weighted version has risen nearly 4%, and the Russell 2000 small-cap index is up more than 5%. This is hugely important from the standpoint of the strength of the November rally and sustainability of the bull market. The market may be extremely overbought in the near term, but recent market action suggests that pullbacks should be bought for new all-time highs in 2024.

Stockcharts

It is also important to note that this rotation is occurring in the face of declining long-term interest rates. The 10-year yield has fallen 30 basis points from 4.5% to 4.2% over the past two weeks, but that is no longer fueling gains in the largest growth stocks. This suggests to me that valuations for the Magnificent 7 are getting stretched, which is why we should see more value-oriented names direct moving forward.

The next leg up to new all-time highs will be fueled by the $6 trillion that sits comfortably for now in money markets yielding more than 5%. As the Fed lowers the Fed funds rate early next year, those lucrative yields will gradually reject, and the $6 trillion will be looking for a new home in stocks and bonds. I think companies that are paying sustainable dividends with yields of 4% or more will be magnets for the outflows from money market funds by investors who have been underinvested in stocks.

Q2 2024 Earnings Call Transcript")