Yossakorn Kaewwannarat

Welcome to another installment of our BDC Market Weekly Review, where we converse market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the second week of December.

Market Action

BDCs had another good week with a total NAV return above 1% – the best across the broader income market. A reversal in the recent drop in short-term rates supported the sector.

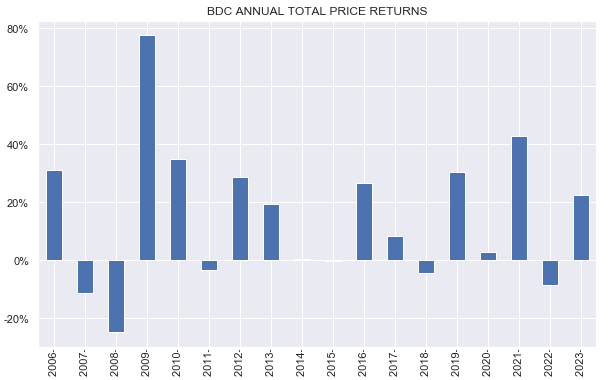

So far this year BDCs have generated a total return north of 20% which more than offsets their loss in 2022.

Systematic Income

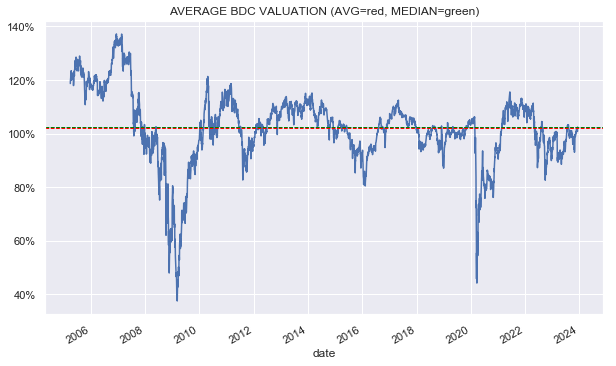

A consequence of this is that the sector is no longer as cheap as it has been for most of its time since 2022. In fact, it’s trading in line with its historic average over the last 20-odd years and near its highest valuation since the initial drawdown in 2022.

Systematic Income

Market Themes

This week we received several questions from readers about our price targets on various securities. In theory price targets sound pretty intuitive – you may not admire a security at the current price but you would buy it, say, 3-5% below where it trades.

However, the reality is, annoyingly, more complicated. The fact of the matter is that if the given security drops by 5%, the rest of the world will not stand still. Other securities could drop by more and they could be even more attractive.

Two, significant price drops don’t typically happen ex nihilo, so to speak. They happen either because the macro picture has worsened (i.e. for systemic reasons) or because there is a problem with the stock (i.e. for idiosyncratic reasons). Mechanically buying a stock only because the price is lower requires investors to switch off their higher-order thinking.

Three, for BDCs there are two reasons a price could drop – due to the drop in the NAV and/or the widening in the discount. If the NAV drops by 5% because of a big loss in the portfolio, it’s not at all obvious that the stock would all of a sudden be a buy when it hits the price target whereas a widening in the discount could very well make it a buy. The particular situation has to be analyzed at the time. The same price drop could be a buy or not – it depends.

Finally, markets tend to co-advance and price drops tend to be more violent than price rises. This means that when a price target on a given security is reached, most other price targets in the portfolio could easily be triggered as well. And, unless you have unlimited capital to put to work, price targets don’t actually make the allocation choice any easier since you still need to go and see which of the many hit price targets you want to follow. This obviates the need for the price target in the first place.

Overall, price targets have a comforting precision about them but they don’t account for the fact that the world is more complicated and that some things should not be oversimplified.

Market Commentary

Oaktree Specialty Lending (OCSL) had a decent Q3 with a +3.2% total NAV return which was in line with the average though below the median so far. Net income stayed flat for the third quarter in a row (the rest of the sector continued to see rising net income) which is due to its relatively modest leverage and a large amount of floating-rate debt.

Systematic Income BDC Tool

This last feature should allow the company to moderate net income drops in a falling short-term rate environment. Only 18% of the company’s liabilities are fixed-rate versus close to 50% for the average BDC.

Overall, the company has lagged its upper middle-market peers admire ARCC, BXSL and OBDC over the past couple of years in terms of performance and this could be due to the company’s relatively conservative marking approach. The hope here is that so long as public credit spreads remain stable or tighten it will be able to write up the NAV drop we saw since 2022.

Systematic Income

The NAV is about 10% off the 2021 high while some other BDCs are seeing record NAV levels. 10% is a big number to write-up so there is some risk that a portion of the NAV loss is locked in.

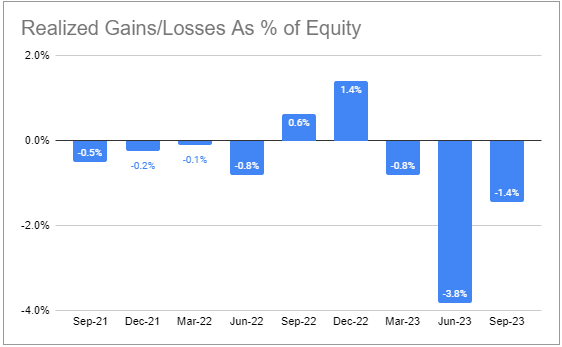

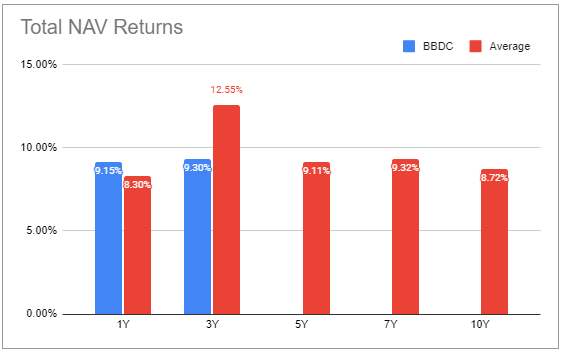

The Barings BDC (BBDC) didn’t have a great quarter. Total NAV return was 1.5% as the NAV fell by close to 1% due to a realized loss. This is a third quarterly realized loss in a row and is something that puts a spotlight on the firm’s subpar underwriting process.

Systematic Income BDC Tool

Over the last 3 years the company has underperformed the sector by around 2% per annum. Its valuation discount relative to the sector has tightened from about 30% to about 20%. Over the last year the company has more or less matched the sector performance so if this holds up and its underwriting improves it will start to look reasonable.

Systematic Income BDC Tool

Stance And Takeaways

BDCs continue to create attractive levels of net income owing to elevated short-term rates and modest levels of interest expense, having taken the opportunity to refinance fixed-rate debt at low levels over 2020 and 2021.

However, net income will start to get squeezed over the coming years from a likely drop in short-term rates as well as bonds coming to maturity. Separately, the macro picture remains cloudy as a possible recession remains on the table. Given this set of challenges it makes sense to foresee for better entry points to the sector and take advantage of continued relative value opportunities.

Q2 2024 Earnings Call Transcript")