peepo

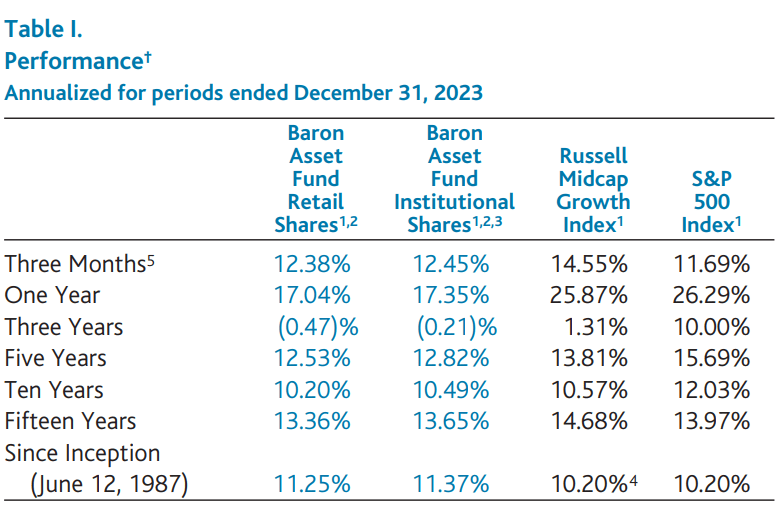

Performance

Moderating inflation and softening labor market conditions contributed to both falling interest rates and investors’ growing belief that a hard landing economic recession will be avoided. This optimistic scenario propelled a risk on investor mindset and a strong equity market rally during the quarter. Most sectors closed higher, led by Information Technology (IT), which benefited from widespread gains in fast-growing software and semiconductor companies. Other leading sectors included Real Estate and Financials, which generally benefited from declining rates, as well as Industrials and Consumer Discretionary, which were bolstered by moderating recessionary fears. Defensive sectors, including Consumer Staples, Health Care, and Utilities, underperformed amid this market environment. The Energy sector declined, as oil prices fell throughout the period.

Against this backdrop, Baron Asset Fund® (the Fund) gained 12.45% (Institutional Shares) in the fourth quarter, trailing the Russell Midcap Growth Index (the Index), which gained 14.55%. The Fund’s relative underperformance was driven partly by headwinds from its style biases, notably its underexposure to stocks with elevated beta and residual volatility, as well as the impact of stock selection.

Performance listed in the above table is net of annual operating expenses. Annual expense ratio for the Retail Shares and Institutional Shares as of September 30, 2023, was 1.30% and 1.05%, respectively. The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate; an investor’s shares, when redeemed, may be worth more or less than their original cost. The Fund’s transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month end, visit Baron Funds – Asset Management for Growth Equity Investments or call 1-800-99-BARON.

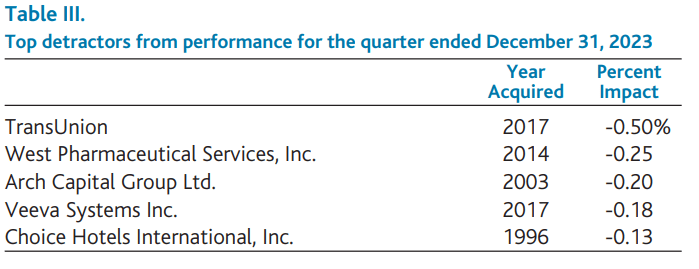

Several holdings in Consumer Discretionary, Industrials, and Financials were generally responsible for the relative shortfall during the quarter. Weakness in Consumer Discretionary was driven by declines from global ski resort company Vail Resorts, Inc. (MTN) and hotel franchisor Choice Hotels International, Inc. (CHH) Vail’s stock underperformed on concerns that limited snowfall would impact its results for the ski season, but we are optimistic that Vail’s strong sales of season ski passes will offset this effect. Choice’s shares were pressured by its proposed hostile takeover of Wyndham Hotels. If this acquisition is completed, we expect various benefits from the combined companies’ greater scale. If the deal falls through, we believe the stock would rebound to higher levels.

Within Industrials, strong performance from private rocket and spacecraft manufacturer Space Exploration Technologies Corp. was overshadowed by the underperformance of consumer credit bureau TransUnion (TRU) and data and analytics vendor Verisk Analytics, Inc. (VRSK) TransUnion fell after the company reduced its full-year guidance and reported third quarter financial results that missed Street expectations. Despite reporting strong quarterly earnings, Verisk’s stock lagged due to investor concerns that revenue growth will normalize in 2024 following outsized growth in 2023. In the Financials sector, specialty insurer Arch Capital Group Ltd. (ACGL) gave back a portion of its strong performance from earlier in the year, given a market rotation away from defensive securities to more speculative stocks following a decline in interest rates.

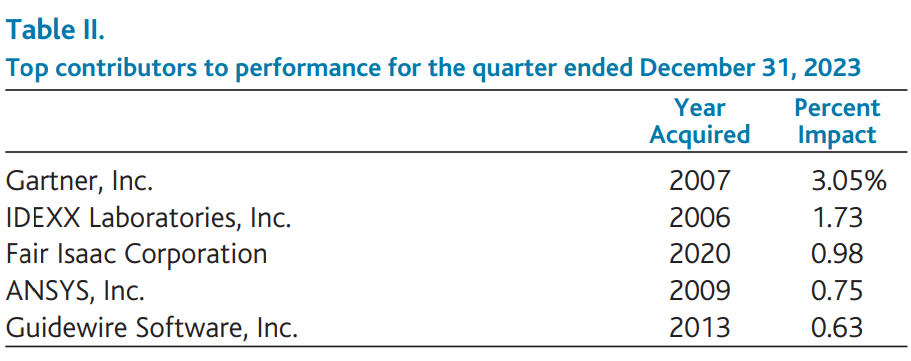

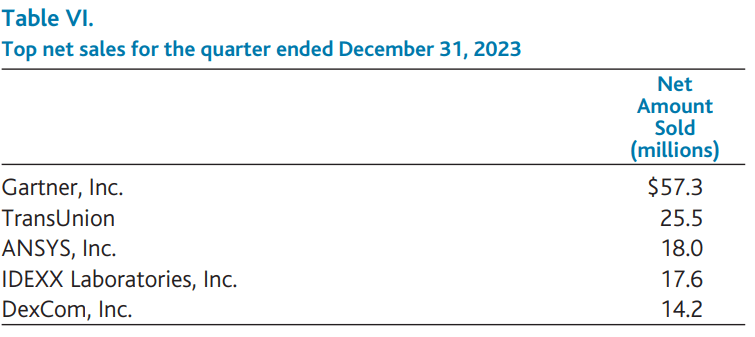

Partially offsetting the above was the strength in IT coupled with a lack of exposure to the lagging Energy and Consumer Staples sectors. Stock selection accounted for a portion of the relative gains in IT. Shares of syndicated research provider Gartner, Inc. (IT) soared after reporting excellent quarterly earnings results, with impressive growth in its core subscription research businesses.

Shares of Gartner, Inc., a provider of syndicated research, soared after reporting excellent quarterly earnings results. Gartner’s core subscription research businesses continued to compound at attractive rates, and we believe that its growth will accelerate over the next several quarters. We believe Gartner will emerge as a critical decision support resource for any company contemplating the opportunities and risks of artificial intelligence for its business. We expect this development to provide a tailwind to Gartner’s volume growth and pricing realization over time. We expect that Gartner’s sustained revenue growth and focus on cost control should drive continued margin expansion and enhanced free-cash-flow generation. The company’s balance sheet remains in excellent shape, and we expect ongoing aggressive share repurchases.

Shares of veterinary diagnostics leader IDEXX Laboratories, Inc. (IDXX) contributed to the quarter’s performance. While foot traffic to veterinary clinics in the U.S. has been subdued for the past year, IDEXX’s excellent execution has enabled the company to continue delivering robust financial results. Traffic to clinics now appears to be rebounding, and we expect this to lead to accelerated revenue growth. We believe IDEXX’s competitive trends are outstanding, and we expect new proprietary innovations to contribute to growth in 2024 and beyond. We see increasing evidence that long-term secular trends around pet ownership and pet care spending have been structurally accelerated, which should help support IDEXX’s long-term growth rate.

Shares of Fair Isaac Corporation (FICO), a data and analytics company focused on predicting consumer behavior, contributed to performance. The company reported good earnings results and gave preliminary guidance that appears conservative, especially since pricing initiatives in the company’s highly profitable Scores business remain on track. CEO Will Lansing expressed confidence that the business can perform relatively well across different economic backdrops and expressed optimism about the accelerating revenue momentum in its software business. We believe Fair Isaac will be a steady earnings compounder, which should drive solid returns for the stock over a multi-year period.

TransUnion is a consumer credit bureau that helps businesses make lending and marketing decisions. Shares fell after the company reported quarterly financial results that were below consensus expectations and reduced full- year guidance. Lending and marketing activity softened during the quarter, particularly among smaller, subprime lenders. Management believes that its new financial guidance is achievable and is increasingly focused on cost efficiency to improve margins. We reduced our position and are closely monitoring developments. We expect its earnings growth to improve as cyclical headwinds abate, and the company integrates recent acquisitions.

West Pharmaceutical Services, Inc. manufactures components and systems for the packaging and delivery of injectable drugs. The stock declined after the company reported sales that missed analyst forecasts and cut its forward earnings guidance due to inventory management by certain customers, which delayed orders into 2024. We believe this shortfall is a timing issue and does not detract from the positive long-term outlook for the business. We believe West has a competitively advantaged business that should grow at attractive rates on a normalized basis, driven by mix shift, volume, and price.

Portfolio Structure

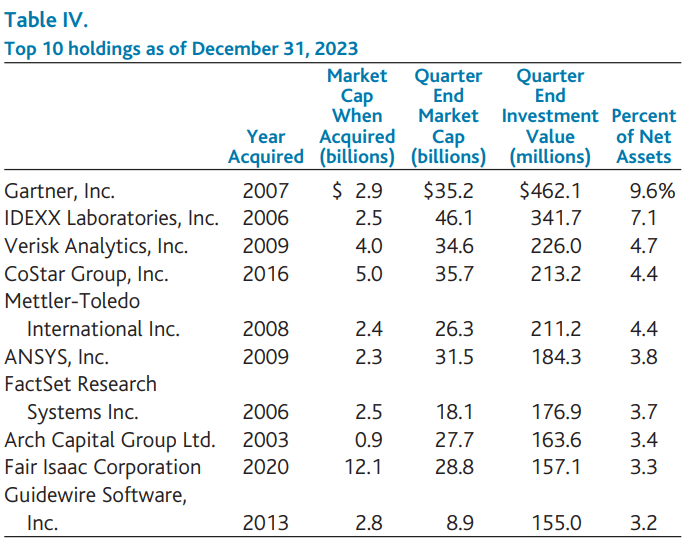

At December 31, 2023, Baron Asset Fund held 51 positions. The Fund’s 10 largest holdings represented 47.5% of net assets, and the 20 largest represented 70.9% of net assets. The Fund’s largest weighting was in the IT sector at 29.5% of net assets. This sector includes software companies, IT consulting firms, and internet services companies. The Fund held 22.8% of its net assets in the Health Care sector, which includes investments in life sciences companies, and health care equipment, supplies, and technology companies. The Fund held 16.7% of its net assets in the Industrials sector, which includes investments in research and consulting companies and aerospace and defense companies. The Fund also had significant weightings in Financials at 13.3% of net assets and Real Estate at 7.0% of net assets.

As the chart below shows, the Fund’s largest investments all have been owned for significant periods – 8 of the 10 largest holdings have been owned for longer than a decade. This is consistent with our approach of investing for the long term in companies benefiting from secular growth trends with significant competitive advantages and best-in-class management teams.

Recent Activity

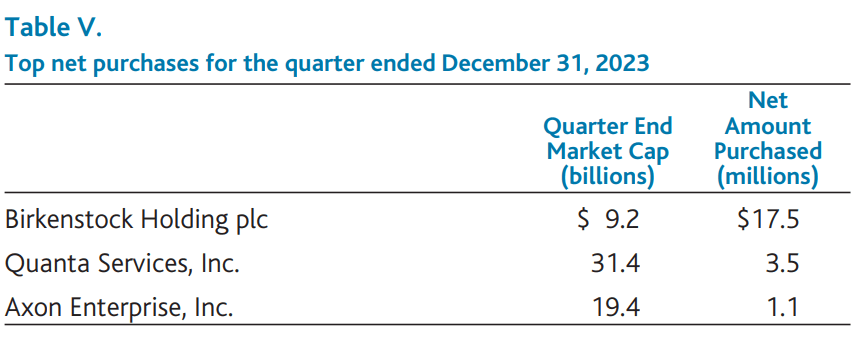

We participated in the initial public offering of Birkenstock Holding plc. (BIRK) Birkenstock is a global footwear company with roots dating back to 1774. Embedded in American culture since the 1960s, the brand is best known for its iconic Arizona and Boston sandals. Although the Birkenstock brand has existed for more than two centuries, the Birkenstock family brought in its first outside management team, led by Oliver Reichert, in 2009. Under new leadership and vision, the business has been transformed from a family-owned, production-oriented company into a professionally managed enterprise committed to growing the Birkenstock brand globally.

Following the arrival of new management, Birkenstock revenues have grown at a 20% CAGR from fiscal 2014 to fiscal 2022, when the company generated revenues of €1.2 billion with profitability margins in the mid-30% range. We believe this combination of an iconic brand with high growth and industry-leading profitability makes the Birkenstock brand an attractive asset.

Unlike nearly all other footwear brands, Birkenstock manufactures products in-house with over 95% in its German factories. We believe this provides the company with better quality control and less risk in its supply chain. Birkenstock products are sold both direct and through wholesale partners. Wholesale represents roughly 60% of sales through 6,000 selected wholesale partners in approximately 75 countries. The remaining 40% of sales are generated direct-to-consumer, with the vast majority sold through e-commerce. The company has just 45 stores, though they expect to increase that number meaningfully. The American and European markets are most developed, and Asia represents a large, untapped opportunity.

Over the medium term, we believe Birkenstock will be able to increase revenue by 15% per year or more, driven by ongoing growth in its core styles, expanded year-round product mix, new stores, and geographic expansion. We also expect Birkenstock to maintain its industry-leading profitability

We took some profits and managed the position size of long-term holdings Gartner, Inc. and IDEXX Laboratories, Inc. We took some profits in ANSYS, Inc. after the stock jumped on rumors that it would be acquired by Synopsys, a software company focused on electronic design automation. We reduced our position in TransUnion after the company reported quarterly financial results that were below consensus expectations and reduced full-year guidance. We reduced our position in DexCom, Inc. (DXCM), which sells a continuous glucose monitoring system for diabetics, because of uncertainty about the impact that GLP-1 weight loss medications may have on the company’s business.

Outlook

Although macroeconomic forecasts do not explicitly influence our stock selection process or portfolio management, we are optimistic that the U.S. Federal Reserve has successfully orchestrated a soft landing. Inflation has moderated, and long-term interest rates have declined meaningfully from their fourth quarter peak. Many of our companies’ management teams have observed improved business conditions, and they are not anticipating a recession. Current economic conditions appear more favorable than virtually all forecasters had expected at the beginning of 2023, and this was a key driver of higher stock prices throughout the past year. As 2024 unfolds, we expect an environment of declining interest rates and growing corporate earnings to be beneficial for stocks.

During 2023, as the market recovered from the prior year’s dramatic sell-off, the types of stocks that performed best included higher beta, cyclical, and lower quality companies. The Health Care sector, which is the Fund’s second largest weighting, was a particular laggard in this environment. As the economy stabilizes and the stock market continues its recovery, we expect the types of companies that the Fund favors to outperform – leading companies that benefit from secular growth drivers, secure competitive positions, and talented management teams.

It is also worth noting that the Index has dramatically underperformed the Russell Midcap Value Index during the past three years by 706 basis points annually. It has also underperformed the Russell 1000 Growth Index, a key benchmark for large-cap growth stocks, by 755 basis points annually over this same period. This has reduced the relative premium that the market generally accords faster growing mid-cap stocks, and we believe it presents an attractive opportunity to invest in this area.

Footnotes

† The Fund’s 3-year historical performance was impacted by gains from IPOs and there is no guarantee that these results can be repeated or that the Fund’s level of participation in IPOs will be the same in the future.

1 – The Russell Midcap® Growth Index measures the performance of medium-sized U.S. companies that are classified as growth. The S&P 500 Index measures the performance of 500 widely held large-cap U.S. companies. All rights in the FTSE Russell Index (the “Index”) vest in the relevant LSE Group company which owns the Index. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. The Fund includes reinvestment of dividends, net of withholding taxes, while the Russell Midcap® Growth Index and S&P 500 Index include reinvestment of dividends before taxes. Reinvestment of dividends positively impacts the performance results. The indexes are unmanaged. Index performance is not Fund performance. Investors cannot invest directly in an index.

2 – The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

3 – Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns for the Institutional Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher.

4 – For the period December 31, 1987 to December 31, 2023.

5 – Not annualized.

Investors should consider the investment objectives, risks, and charges and expenses of the investment carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds. You may obtain them from the Funds’ distributor, Baron Capital, Inc., by calling 1-800-99-BARON or visiting Baron Funds – Asset Management for Growth Equity Investments. Please read them carefully before investing.

Risks: Securities issued by medium sized companies may be thinly traded and may be more difficult to sell during market downturns. Even though the Fund is diversified, it may establish significant positions where the Adviser has the greatest conviction. This could increase volatility of the Fund’s returns.

The Fund may not achieve its objectives. Portfolio holdings are subject to change. Current and future portfolio holdings are subject to risk.

The discussions of the companies herein are not intended as advice to any person regarding the advisability of investing in any particular security. The views expressed in this report reflect those of the respective portfolio managers only through the end of the period stated in this report. The portfolio manager’s views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time based on market and other conditions and Baron has no obligation to update them.

This report does not constitute an offer to sell or a solicitation of any offer to buy securities of Baron Asset Fund by anyone in any jurisdiction where it would be unlawful under the laws of that jurisdiction to make such offer or solicitation.

Beta explains common variation in stock returns due to different stock sensitivities to market or systematic risk that cannot be explained by the US Country factor. Positive exposure indicates high beta stock. Negative exposure indicates low beta stock. Residual volatility captures relative volatility in stock returns that is not explained by differences in stock sensitivities to market returns. A positive exposure indicates a high residual volatility. A negative exposure indicates a low residual volatility. The portfolio manager defines “Best-in-class” as well-managed, competitively advantaged, faster growing companies with higher margins and returns on invested capital and lower leverage that are leaders in their respective markets. Note that this statement represents the manager’s opinion and is not based on a third-party ranking. Free cash flow (FCF) represents the cash that a company generates after accounting for cash outflows to support operations and maintain its capital assets.

BAMCO, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission (SEC). Baron Capital, Inc. is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (FINRA).

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Q2 2024 Earnings Call Transcript")