The Bank of England has opted once again to hold the base rate at 5.25 per cent, a advance which will reinforce the view we’ve reached the peak for interest rates.

The decision marks its third pause in a row, after the Monetary Policy Committee voted to hold the base rate first in September, and then at the start of November.

Prior to that, there had been 14 consecutive base rate hikes since December 2021.

The MPC voted by a majority of 6–3 to hold base rate, with six voting to hold and three voting for a hike.

We explain why the Bank of England has paused interest rate rises and what it means for your mortgage, savings and the wider economy.

Third time in a row: The Bank of England has opted once again to hold the base rate at 5.25 per cent

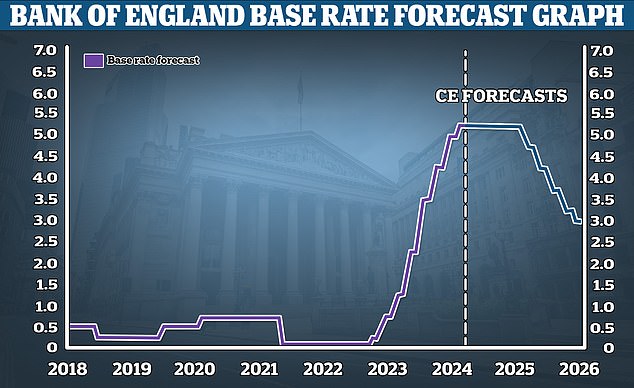

In recent months, forecasts for where the base rate will peak have fallen from a high of 6.5 per cent to the current 5.25 per cent level.

Today, a 5.25 per cent peak seems ever more likely. While the Bank of England is not ruling out advance rises, many will see this as a sign of its caution when it comes to pushing up rates any advance, unless inflation persists for longer than expected.

Swap rates, which banks and building societies use to price their fixed rate mortgages and savings products, have also been falling suggesting that financial markets are expecting interest rates to gradually fall from here on.

Why has the bank paused rate rises?

Today’s base rate decision was widely expected given the central bank’s decision to hold base rate in its two previous meetings and the fact that the rate of inflation has been falling.

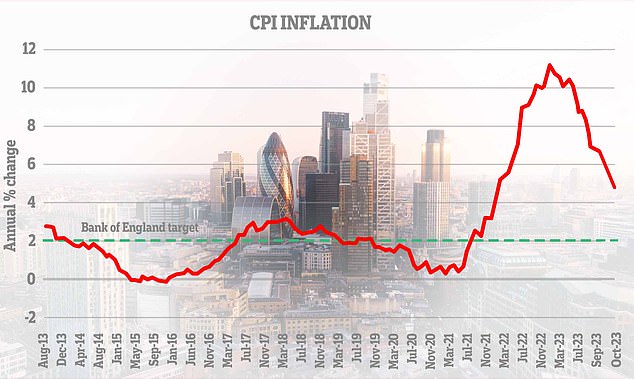

The official consumer prices index measure of inflation (CPI) fell to 4.6 per cent in October, a big drop on the 6.7 per cent recorded in September.

October’s CPI figure surpassed the expectations of many analysts, who had predicted inflation to fall to either 4.7 per cent or 4.8 per cent.

That said, inflation remains well above the Bank of England inflation target of 2 per cent.

Between December 2021 and August 2023, higher inflation led the bank to use the only real tool in its arsenal to try and bring it down – raising interest rates.

The official consumer prices index measure of inflation (CPI) fell to 4.6 per cent in October, a big drop on the 6.7 per cent recorded in September.

By raising the cost of borrowing for individuals and businesses it hoped to reduce demand, slowing the flow of new money into the economy.

In theory, more expensive mortgages and better savings rates should also encourage people to save more and spend less, advance pushing down inflation.

Now with the rate of inflation steadily easing back from its double-digit highs recorded earlier this year, the Bank of England appears to have enough confidence to halt for the time being, as it watches the impact of its earlier rate hikes filter through to the wider economy.

While many think interest rates have now peaked, it looks likely the MPC will continue to hold rates where they are until they are certain the inflation threat is under control.

In a recent speech, MPC member Jonathan Haskel said that ‘the still-high degree of labour market tightness continues to impart inflationary pressures’ meaning rates will need to be ‘higher for longer to get inflation sustainably to target.’

MPC member Megan Greene said in a recent speech that while ‘the data on output remains mixed, I continue to worry more about inflation persistence.’

Hold the line: It looks likely the MPC will continue to hold rates where they are until they are certain the inflation threat is under control

Ruth Gregory, deputy chief economist at Capital Economics, an economic research business says: ‘There was little doubt that the MPC would leave rates unchanged again.

‘However, there are three key reasons why we think it will retain its commitment to keeping interest rates higher for long.

‘First, the UK has had only one softer-than-expected inflation report while the US and the euro-zone have had a run of them.

‘Second, the MPC’s lingering concerns about the tightness of the labour market could also make it cautious about watering down or dropping its guidance.

‘Third, the MPC will be wary of causing the pound to fall and market interest rates expectations to shift decisively in favour of an even earlier cut.’

Future falls: Capital Economics is forecasting the the bank rate will be cut to 3% by the end of 2025

When will the Bank of England cut rates?

Looking ahead, markets are predicting the base rate will be cut next year.

Morgan Stanley has forecast that interest rates will be cut as soon as May and fall to 4.25 per cent by the end of next year.

The boldest UK interest rate forecast is from Goldman Sachs, which said a cut could come as early as February.

Meanwhile, Capital Economics is forecasting the base rate won’t be cut until late next year.

‘Our forecast is for rates to remain at their peak until late-2024, for four reasons,’ says Ruth Gregory of Capital Economics.

‘First, the effects of higher interest rates are filtering through the economy more slowly than in the past and are also being cushioned by the lingering effects of the pandemic.

‘That suggests interest rates need to be higher for longer to have the same dampening effects on activity, wage growth and inflation.

‘Second, rates have risen to a lower peak than most models suggest, which implies they need to stay higher for longer to compensate.

‘Third, the Bank knows that high inflation has dented its credibility so it will want to be absolutely sure that inflationary pressures are consistent with the 2 per cent inflation target before cutting rates. It’s likely to err on the side of policy being too tight than too loose.

‘Fourth, we expect the government to unveil a advance scaling back of the tightening in fiscal policy in 2024 ahead of the next election.

‘And in an environment where deficient supply rather than demand is the key factor holding back activity, a smaller drag from fiscal policy will add to price pressures and may mean interest rates need to stay higher for longer than might otherwise have been the case to compensate.’

Gregory adds: ‘Beyond 2024, we see a stagnant economy over the coming year will lay the groundwork for a more marked easing in price pressures in 2025 and more significant interest rate cuts.

‘Our forecast that rates will be cut to 3 per cent in 2025 is lower than the cuts to 4 per cent priced into the markets.’

What does this mean for mortgage borrowers?

The higher base rate has created a mortgage crisis for some – especially those who are due to remortgage in the near future.

Many borrowers are protected by the fact their interest rate is fixed for either two or five years.

However, there are some 1.6 million mortgage borrowers expected to roll off their fixed rate mortgages next year, many of whom will currently be enjoying a mortgage rate of less than 2 per cent.

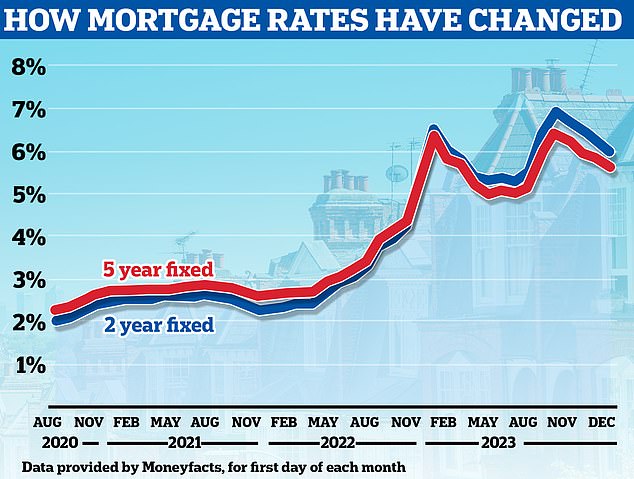

The average two-year fixed mortgage rate is now 5.99 per cent, according to Moneyfacts, and the average five-year fix is 5.59 per cent – meaning these borrowers are set to see a big jump in their monthly payments.

> Check the best mortgage rates based on your home’s value and loan size

Heading down: The average two-year fixed mortgage rate is now 5.99 per cent, according to Moneyfacts, and the average five-year fix is 5.59 per cent

The average borrower coming off a two-year fix would see their rate boost from 2.34 per cent to 5.99 per cent, if they fixed for two years again today.

On a £200,000 mortgage over a term of 25 years, this would mean monthly mortgage payments rising from £881 to £1,287 – an boost of £406 a month or £4,872 a year.

Of course, it’s important to also recollect these are the average rates across the entire market. The cheapest deals available paint a slightly more positive picture, particularly for those with big deposits or lots of equity built up within their home.

It’s possible to get a rate as low as 4.65 per cent on a two-year fix, and as low as 4.29 per cent when fixing for five years. It is worth speaking to a mortgage broker to find the cheapest deal that you may be eligible for.

However, those that can bag a below-average rate are still likely to face a serious hit to their finances.

Mark Harris, chief executive of mortgage broker SPF Private Clients, says: ‘Those with fixed-rate mortgages who need to refinance next year will still face a payment shock as we must all get used to a higher interest rate environment but it might not be as bad as it could have been.

David Hollingworth, associate director at broker, L&C Mortgages, broadly agrees.

He adds: ‘Although far better than earlier this year, fixed rates will still often be double those available a few years ago so there will be payment shock to contend with.

‘The drop in rates could well continue to the end of the year and into next. That means that borrowers can now safeguard a rate and then keep tabs on any advance rate moves to see if they can advance to a better deal before they complete.’

> How to remortgage your home: A guide to finding the best deal

Mortgage shake up: Britain’s biggest building society sent ripples across the mortgage market last week after it announced its eleventh consecutive round of rate cuts

Mortgage borrowers on tracker and variable rates may either be breathing another sigh of relief today or perhaps frustration at the fact base rate isn’t already being cut.

Variable rate mortgages include tracker rates, ‘discount’ rates and also standard variable rates. Monthly payments on all these types of loan can go up or down.

Trackers follow the Bank of England’s base rate plus or minus a set percentage, for example base rate plus 0.75 per cent.

Standard variable rates are lenders’ default rates that people tend to advance on to if their fixed or other deal period ends and they do not remortgage on to a new deal.

These can be changed by lenders at any time and will usually rise when the base rate does, but they can go up by more or less than the Bank of England’s advance.

What next for fixed rate mortgages?

Mortgage borrowers on fixed term deals should focus less on the base rate decision today, and more about where markets are forecasting the base rate to go in the future.

This is because banks tend to pre-empt the base rate hike. They change their fixed mortgage rates on the back of predictions about where the base rate will ultimately be in the future.

Mortgage rates have been heading lower and lower despite the Bank of England opting to hold base rate at 5.25 per cent.

The cheapest mortgage rates are now almost 1 percentage point below base rate and many analysts are not forecasting base rate to fall until later next year.

Lender’s are instead pricing their mortgages based on future market expectations for interest rates whilst also trying to hit their own funding and lending targets.

Market interest rate expectations are reflected in swap rates. These swap rates are influenced by long-term market projections for the Bank of England base rate, as well as the wider economy, internal bank targets and competitor pricing.

Sonia swaps are used by lenders to price mortgages. Last week, five-year Sonia swap rates dropped below 4 per cent for the first time in months.

Five-year swaps are currently at 3.78 per cent. Two-year swaps are now at 4.38 per cent.

Only as recently as July, five-year swaps were above 5 per cent. Similarly, the two-year swaps were coming in around 6 per cent.

Mortgage expert: David Hollingworth says that fixed rates will still often be double those available a few years ago so there will be payment shock to contend with for many

Most mortgage brokers are of the view that interest rates are likely to continue falling.

‘Some of the bigger lenders continue to reduce their mortgage rates for both new purchases and those remortgaging, increasing the choice for borrowers at more palatable rates,’ adds Harris.

‘Lenders remain keen to lend and will want to do more business next year as this one has been so challenging, which is likely to mean advance rate reductions.

‘Borrowers should scheme ahead if they need a new mortgage next year and speak to a whole-of-market broker about the best deals available to them.

‘Rates can be booked up to six months before you need them so if you reserve one now for peace of mind you can always switch onto a cheaper rate when you come to remortgage should a better deal become available.’

The big decision for borrowers is often whether to fix for two years or five years or even take their chances with a two-year tracker mortgage without early repayment charges.

To fix or not to fix: While some borrowers will be trying their luck with a tracker mortgage in the hope that rates will fall, fixed rates are the cheaper option at present

David Hollingworth says: ‘We have seen a shift toward shorter term fixed rates as borrowers hold out hope that rates will fall in time and they will be able to switch to a new, lower rate.

‘However five year rates are cheaper right now and as they continue to drop we may see more feel that five years may still be a good call to give security at a lower rate, when no one expects interest rates to return to the historic lows of a couple of years ago.

‘Trackers can still have a place where the borrower requires more flexibility and can often be found with no early repayment charges – but of course there is always the chance that the direction of rates does change and so there has to be some flex to deal with higher rates as well.’

Harris adds: ‘With two and five-year fixes available from less than 4.5 per cent, many of our clients are still opting for a shorter fix in the hope that rates will come down by the time they come to remortgage, when they can lock in for longer.

‘Others who don’t need the certainty of a fix and are prepared to take a risk are opting for two-year trackers with no early repayment charges, as they scheme to advance onto a fixed rate once pricing comes down advance.’

What does the base rate pause mean for savers?

The Bank of England’s successive interest rate rises since December 2021 have been good news for savers.

The best savings accounts now offer some of the highest interest rates seen since 2008.

Now, with the base rate hike cycle appearing to peak at 5.25 per cent, as the Bank of England pauses it for the third successive month, savers will be wondering whether it is the end of the savings rate heyday for their nest eggs.

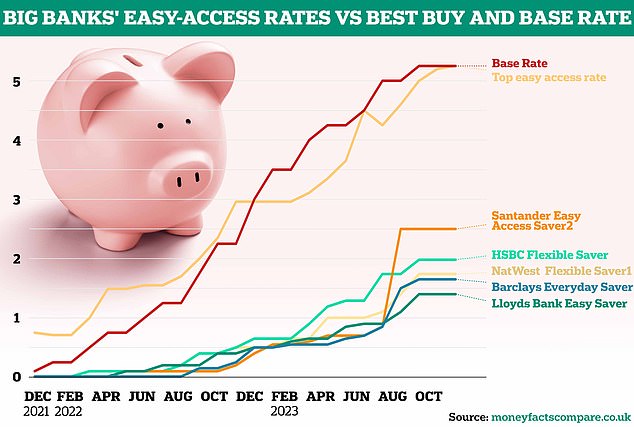

Savings experts have been calling the top of the market for some time now. Previous headline-grabbing deals including Santander’s 5.2 per cent special edition easy-access rate and NS&I one-year bond paying 6.2 per cent have all but vanished.

However, there are still decent rates available, including five one-year fixes paying 5.5 per cent or more as well as 13 easy-access deals paying 5 per cent or more.

Though this has plummeted from three one-year fixed paying 6 per cent or more and 20 easy-access deals paying 5 per cent or more at the time of the last Bank of England base rate meeting in November.

If you haven’t reviewed your savings recently, now is a good time to check your rate and advance to a table-topping rate while you still can.

> Check the best savings rates using This is Money’s independent best buy tables

Switch: If you haven’t reviewed your savings, now is a good time to check your rate and advance to a table-topping rate while you still can. Some of the biggest banks offer the worst rates

Sarah Coles, of Hargreaves Lansdown, says: ‘Savings rates peaked a while ago, and have been falling gradually for weeks, as the market digests the fact that we’re unlikely to see any more Bank of England rate rises in this cycle.

‘2024 is likely to bring more of the same, as it starts to ponder an expectation that interest rates will fall. We’re unlikely to see a huge watershed moment when savings rates are cut. Instead, we expect to see them slowly drift south throughout the year.

‘It means shopping around will be more important than ever as rates fall. If your cash has been sitting with a high street giant, it’s well worth considering a switch to a smaller or newer bank, or a cash savings platform, where your savings can work harder.’

Is it downhill from here for savings rates?

This year has seen rates climb, with banks scrabbling to take the top spot for savings rates and attract new customers.

With many now seeing 5.25 per cent as the peak for base rate, experts agree that rates are likely to advance downwards.

Andrew Hagger, personal finance expert and founder of MoneyComms says he expects savings rates will slowly start to slip back

However, rather than savings rates crashing back down, most commentators are expecting a gradual refuse over the coming years.

Andrew Hagger, personal finance expert and founder of MoneyComms says: ‘I can’t envisage any dramatic changes over the next few years’.

‘I think we will see a very gradual refuse in base rate from a high of 5.25 per cent this year to somewhere around the 4 per cent mark in the next three years.

‘As for 2024, perhaps a couple of 0.25 per cent cuts towards the end of the year would be my prediction.

‘I therefore expect easy access savings rates to hover around the 5 per cent mark for the coming 12 months.

‘Meanwhile, I think one-year fixed rate savings deals could fall back to around 5.3 or 5.4 per cent over the coming year.’

Which banks offer the best savings rates?

When it comes to choosing an account, it’s always worth keeping some money in an easy-access account to fall back on as and when required.

Most personal finance experts believe that this should cover between three to six months’ worth of basic living expenses.

The best easy-access deals, without any restrictions, pay north of 5 per cent. If you’re getting a lot less than this at the moment, then consider switching to a provider that pays more.

In terms of the best of the best, Ulster Bank (which is part of the NatWest Group) is now offering a market-leading easy-access deal paying 5.2 per cent.

Someone putting £10,000 in Ulster Bank’s account could expect to earn £520 in interest over the course of a year.

> Find the best easy-access savings rates here

Those with extra cash which they won’t immediately need over the next year or two should consider fixed-rate savings.

Fixed rates offer the best returns at present. The best one-year deal is offered by Al Rayan Bank and Union Bank of India (UK), paying 5.7 per cent.

But the gap between one year-fixed rate deals and easy-access accounts has narrowed to just 0.5 per cent.

There are no longer any one-year fixed-rate accounts paying 6 per cent or more.

Bridging the gap: The chasm between the top easy-access rate and one-year fixed-rate savings account has narrowed to 0.6%

Someone putting £10,000 in Al Ryan or Union Bank of India’s deal will earn a guaranteed £570 interest over one year. It comes with full protection under the Financial Services Compensation Scheme (FSCS) up to £85,000 per person.

Metro Bank is paying 5.66 per cent, Smartsave Bank is paying 5.52 per cent and Gate House Bank is paying 5.5 per cent. All offer FSCS protection.

> Check out the best fixed rate savings deals here

Savers should also consider using a cash Isa to protect the interest they earn from being taxed.

The top one-year fixed-term cash Isa is paying 5.4 per cent interest, while the top two-year fix is paying 5.15 per cent.

Those wishing to keep their money in an easy-access cash Isa can also get 5.08 per cent with Zopa Bank.

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to encourage products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")