Joa_Souza/iStock Unreleased via Getty Images

In previous articles outlining my investment thesis on Banco Santander (Brasil) (NYSE:BSBR), I have primarily focused on the performance of the Brazilian bank’s shares, which have been affected by concerns over loan defaults and credit availability. These concerns have significantly impacted the broader Brazilian banking sector, negatively affecting the efficiency and profitability of Santander Brasil in recent quarters, where the bank has maintained a notably low Return on Equity (“ROE”) compared to its critical domestic peers.

During the preceding quarter, Q3, Banco Santander Brasil displayed promising improvement in critical areas, such as asset quality, credit origination, and a gradual profitability enhancement. This positive trajectory was reflected in the performance of Santander Brasil shares, which witnessed a notable increase of about 17% from Q3 to Q4.

However, complicating the analysis of the most recent Q4 results, while the outcomes were not entirely satisfactory, there are still positive aspects that could be pivotal for 2024.

The net income of R$2.2 billion underwent a notable 19% decline compared to the previous quarter. ROE measured the profitability at just 10.3%, maintaining low levels compared to the bank’s historical performance and some competitors. Notably, this figure is also below the 12.4% reported by Santander Group (SAN), its controlling entity, in the same quarter.

Consequently, the bank’s profitability, which had been on an upward trend, regrettably worsened this quarter. Despite these challenges, as I observe Santander Brasil trading at a premium multiple compared to its primary peers and exhibiting much more inconsistency in its fundamentals, I find little reason to adopt a more bullish stance on the bank at this time.

Santander Brasil’s Q4 Overview

In the fourth quarter of 2023, Santander Brasil reported a recurring net income of R$2.204 billion, falling below the market consensus, which had anticipated a profit of R$2.87 billion. Despite a year-over-year profit increase of 30.5%, there was a notable decrease of 19.2% compared to the second quarter of the same year.

Santander’s return on equity (“ROE”) remained at 10.3%, indicating a persistent low level compared to other industry peers such as Itaú Unibanco (ITUB) and Banco do Brasil (OTCPK:BDORY), both boasting ROEs exceeding 20%.

Key highlights from the quarter include an improvement in interest income (“NII”) and modest growth in the credit portfolio. While non-performing loans remained stable and decreased in the short term, provisions for bad debts raised concerns, albeit influenced by certain one-off factors.

As of the end of September, Santander Brasil reported total assets of R$1.153 trillion, with shareholders’ equity at R$86 billion. The following are key points from Santander Brasil’s fourth-quarter results segmented for clarity:

-

Interest Income (“NII”) Improvement: Notable positive performance in interest income.

-

Credit Portfolio Growth: Modest expansion observed in the credit portfolio.

-

Non-Performing Loans: Stability and a short-term decrease in non-performing loans.

-

Provisions for Bad Debts: Alarming provisions reported, influenced by certain one-off factors.

Modest Growth in Credit Portfolio

Banco Santander Brasil has reported a loan portfolio of R$516.6 billion, indicating a cautious quarterly growth of 2.8% and a yearly growth of 5.5%. This growth reflects a slightly more favorable macroeconomic environment with lower interest rates. Additionally, it is a consequence of a tentative improvement in credit quality, allowing the bank to venture into higher-risk lines. If we exclude the exchange rate effect, the quarterly growth would have been 3.1%, with a more substantial increase of 6.2% year-over-year.

Banco Santander Brasil’s IR

The standout performer in this quarter was the individual segment, experiencing growth of 3.1% within the quarter and 6% year-over-year. Consumer financing also contributed positively, showing an increase of 5.5% in the quarter and 2.6% year-over-year. Small and medium-sized companies exhibited growth of 5.2% within the quarter and a noteworthy 8.9% year-over-year. On the flip side, the large companies line (Corporate R$139 billion) saw a slight 0.1% decline year-over-year and a modest expansion of 4.5% year-over-year.

A noteworthy development is that the new crops originated in January 2022, characterized by a more appropriate risk level, now constitute 67% of the total portfolio.

Interest Income (“NII”): Margin Improvement

The bank’s interest income witnessed a quarterly increase of 4.8% compared to Q3 and an annual rise of 12.3% compared to Q4 of the previous year. NII Clients (margin with clients) slightly increased by 1.1% quarter on quarter. The Margin with the market (NII Mercado) showed a negative balance of R$263 million, a substantial improvement from the negative balance of R$827 million recorded in the same period last year, indicating a gradual improvement process.

Banco Santander Brasil’s IR

The notable growth in NII, significantly when outpacing the loan portfolio, indicates an improvement in the net interest margin. The net interest margin represents the difference between the interest rate received on interest-earning assets (loans) and the interest rate paid on interest-bearing liabilities (such as deposits). A faster growth rate in NII compared to the loan portfolio suggests efficient management of funding costs, investment in higher-yielding assets, or favorable market conditions.

Delinquency: Stability Emerging After the Worst

Delinquencies over 90 days (management view) exhibited a modest increase of 0.1pp year-over-year and remained stable at 3.1%. This development is viewed optimistically as it reinforces a more favorable scenario for the banking sector in Brazil, signaling that “the worst is over,” especially considering the peak at 3.3% recorded in June of the previous year. The fourth quarter was characterized by stability in the individual segment but saw a marginal increase of 0.1pp quarter-over-quarter in large companies and small and medium-sized enterprises.

Banco Santander Brasil’s IR

A positive aspect in Q4 was the improvement in short-term delinquency (15-90 days), showing a quarterly decline of 0.2pp. This improvement was attributed to the better performance of new vintages, with individuals experiencing a significant contraction of 0.4pp within the quarter.

Asset Quality and Credit Provision Expenses

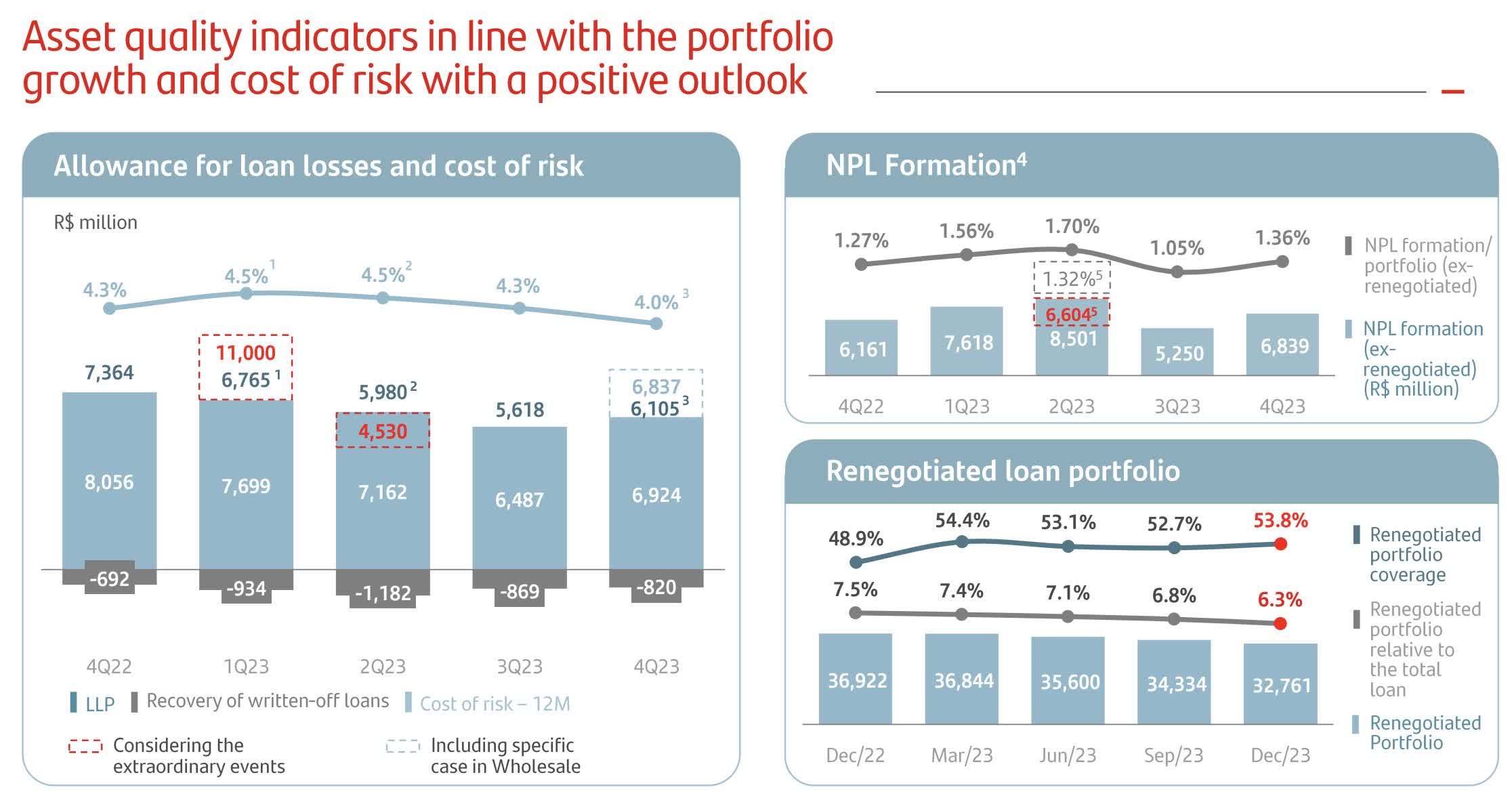

Upon initial examination, Santander Brasil’s asset quality results for Q4 may seem dire. Allowance for loan losses (“ALL”) reached R$6.8 billion, marking a quarter-over-quarter increase of 21.7%, despite a year-over-year decrease of 7.2%.

Banco Santander Brasil’s IR

The quarter faced negative impacts from three specific cases: (1) a provision of 20% for the Lojas Americanas case (a Brazilian retailer involved in an accounting scandal), with 70% already provisioned; (2) the release of R$400 million to a Brazilian wholesaler in default; (3) a judicial recovery case in the beverages sector, resulting in R$90 million for the bank.

However, amidst the challenges, there were positive aspects. Notably, the provision was reduced with a reversal of R$392 million from the retail segment in Brazil. Additionally, a sale of $1.2 billion from a portfolio that had already been written off yielded a gain of R$49 million. Consequently, the coverage ratio ended at 222%, indicating a healthy safety margin concerning financial charges. However, it declined by seven percentage points in the quarter and eight percentage points in the year due to the mentioned charge increase.

Banco Santander Brasil’s IR

On the negative side, Santander Brasil reported an increase in total administrative expenses, reaching R$7.9 billion, up 8.4% in the quarter and 7.6% in the year. The quarter was particularly impacted by the September layoff last year, resulting in higher expenses for technical services, maintenance, and advertising.

Now, looking on the bright side, Santander Brasil has been proactive in expense reduction initiatives. They have been closing branches while maintaining stable employees, internalizing outsourced workers, and investing in financial advisory services. Additionally, the acquisition of brokerage firms, such as Toro, has been part of the bank’s strategic efforts to enhance its overall efficiency and service offerings.

Valuation and Dividends

Banco Santander Brasil, under the control of Spain’s Santander Group, has consistently prioritized returning a significant portion of its profits through dividends, making its shares an appealing income stock for many investors over the years.

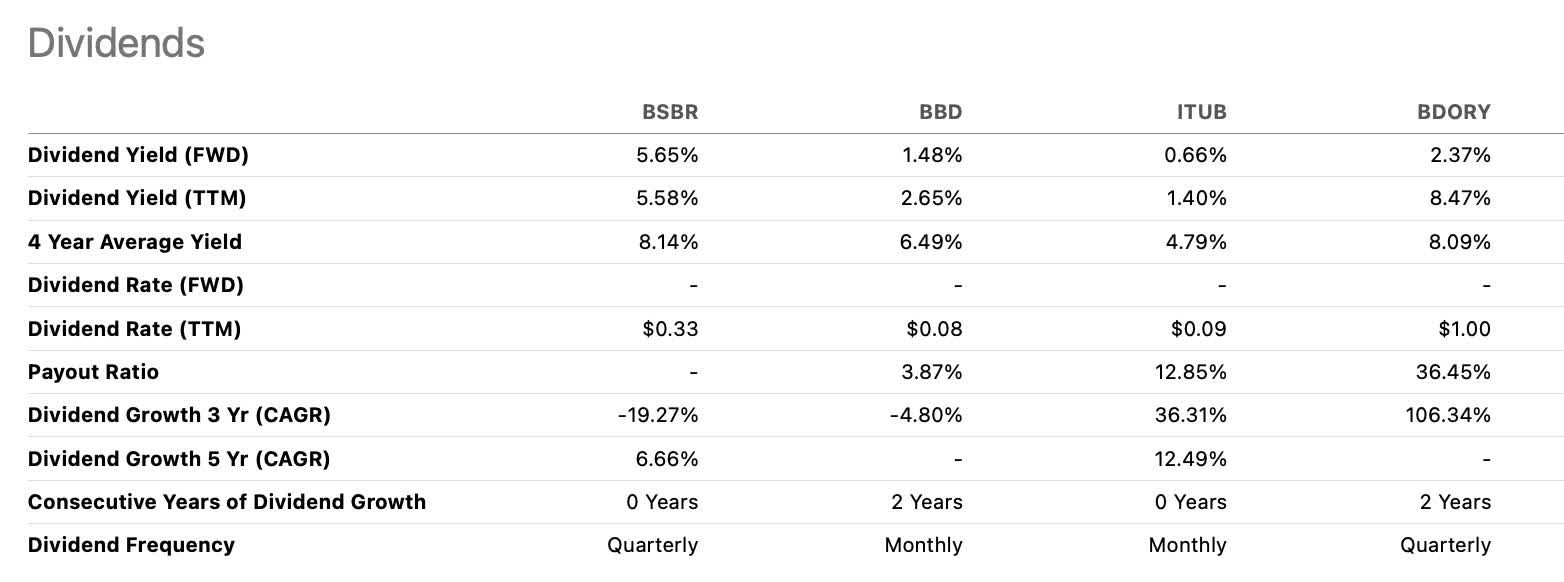

Examining the dividend payment history among major Brazilian banks, Santander Brasil stands out favorably. It boasts a forward dividend yield of 5.5%, second only to Banco do Brasil, a state-owned bank. Additionally, Santander Brasil has maintained an average yield of 8.1% over the last four years, surpassing all its industry peers.

Seeking Alpha

However, a significant part of this appeal for dividends is evident in the premium valuation the bank consistently maintains compared to its peers. Banco Santander Brasil trades at a forward P/E ratio of 10.9x, surpassing all other peers. Although its price-to-book ratio is 1.04, it is second only to Bradesco (BBD).

Seeking Alpha

In my perspective, Banco Santander’s current valuation seems challenging to justify solely based on the attractiveness of its peers. Notably, Banco do Brasil, despite being state-owned, reports a Return on Equity (“ROE”) almost double that of Banco Santander Brasil. Furthermore, Itau Unibanco, presently the bank with the most robust credit and profitability indicators in the sector, trades at a more discounted valuation in certain aspects compared to Banco Santander Brasil. It’s worth noting that Banco Santander Brasil still exhibits some weaknesses.

The table below displays the indicators of the main Brazilian banks up to Q3, except for Santander Brasil, which incorporates Q4 results.

|

Loan Portfolio (R$ bi) |

Delinquency Rate |

Expanded ALL (R$ bi) |

Coverage Ratio |

ROE |

CET1 |

Basel |

|

|

Santander Brasil |

516.6 |

3% |

-6.8 |

222% |

10.3% |

11.5% |

14.5% |

|

Banco do Brasil |

1070 |

2.8% |

-7.5 |

199% |

21.3% |

12.4% |

16.2% |

|

Itaú Unibanco |

1163 |

3% |

-9.3 |

209% |

21.1% |

14.6% |

16.3% |

|

Bradesco |

877.5 |

5.6% |

-9.1 |

182.5% |

11.4% |

13.4% |

12.9% |

The Bottom Line

Despite Santander Brasil’s fourth-quarter results falling short of expectations, marked by a significant decline in net profit compared to the previous quarter, persistently low ROE, and a halt in the upward trajectory of profitability, coupled with a PDD result strongly impacted by toxic credits from Lojas Americanas (now 70% provisioned), there are still positive aspects to consider for 2024.

The bank made strides in fortifying its balance sheet during this quarter through credit provisions, potentially alleviating the need for future provisions. Additionally, revenue lines are anticipated to rebound, driven by growth in segments with higher spreads and increased service revenues. While the Q4 result may not be overwhelmingly positive, it might not be as bleak as it appears, especially given the stability and short-term decrease in defaults.

I have maintained a neutral stance on Banco Santander Brasil for a considerable period and find it challenging to shift towards a bullish outlook in light of results that continue to lag behind the bank’s potential. The current valuation does not necessarily provide a compelling advantage over peers trading at more discounted multiples and exhibiting more robust results.

Given these factors, I am again on the fence, awaiting more excellent stabilization, particularly in provisions, throughout the year. An improvement in ROE would instill more confidence in Banco Santander Brasil’s investment thesis before considering a more positive outlook.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")