berlinguette/iStock via Getty Images

Recently, I’ve seen many articles pop up in my newsfeed touting B2Gold Corp.’s (NYSE:BTG) attractive dividend yield and why investors should buy the stock. Having been a professional resource investor for over a decade and knowing B2Gold quite well, I decided to take a serious look at B2Gold to see if is truly a ‘discount’ bargain.

In my opinion, BTG’s recent stock troubles has to do with fears that the company has bitten more than it can chew with the Back River project in Nunavut.

I personally believe B2Gold’s revised cost estimates are realistic and the recent gold forward sales suggest these cost overruns are fully financed. Therefore, I rate BTG a speculative buy.

Company Overview

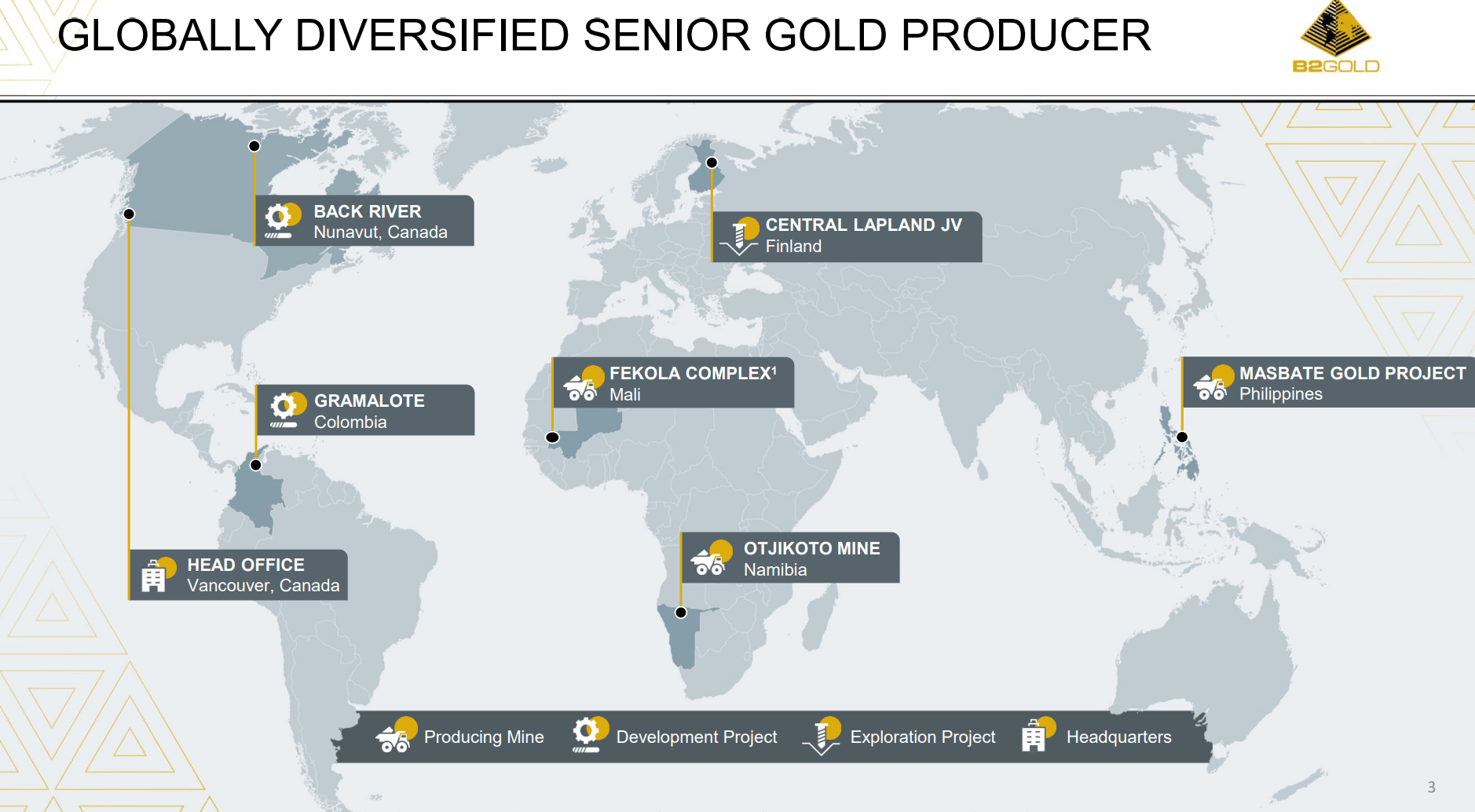

B2Gold Corp. is a senior gold producer with approximately 1 million oz. of gold production primarily from three producing mines (Fekola, Masbate, and Otjikoto) and its ownership interest in Calibre Gold (CXB:CA) (Figure 1).

Figure 1 – B2Gold asset overview (BTG investor presentation)

Brief History Of B2Gold

B2Gold is a rare success story in mining where a management team was able to build a senior gold producer from scratch via organic growth and acquisitions.

B2Gold was founded in 2007 by CEO Clive Johnson and other former executives of Bema Gold, which they sold to Kinross Gold (KGC) in 2007. Starting with Bema’s leftover package of exploration properties in Colombia and Russia, B2Gold went IPO on the Toronto Venture Exchange and raised C$100 million, a sizeable sum for a junior gold explorer/developer.

B2Gold graduated to producer status (and the TSX Exchange) through its 2009 acquisition of Central Sun Mining, a distressed producer with 2 mines (El Limon and La Libertad) in Nicaragua.

In 2012, B2Gold merged with ASX-listed CGA Mining, which gave the company the Masbate mine in the Philippines. With 3 operating mines producing a combined 350-400k oz of gold annually, B2Gold was now a mid-tier gold producer and began to take on more challenging capital projects to develop and build its own mines. The first B2Gold-developed mine was the Otjikoto mine in Namibia, acquired through a 2011 transaction with Auryx Gold.

In 2014, B2Gold also acquired ASX-listed Papillon Resources, which owned the Fekola project based in Mali. If my memory serves me correct, Fekola was a controversial project at the time, as some analysts on Bay Street had doubts as to whether B2Gold could successfully complete the development of the large-scale tier-1 Fekola mine with annual production of 350-400k oz per year.

However, B2Gold was able to complete the development of Fekola on-time and on-budget, catapulting the company’s production to ~1 million oz by 2018.

In 2019, B2Gold sold its Nicaraguan mines to Calibre Mining, with many investors and analysts speculating that the move was designed to recycle capital from the small Nicaraguan mines into potentially larger/newer development assets.

For a time, investors (myself included), thought a logical acquisition for B2Gold was the Namibia-based Twin Hills project owned by Osino Resources (OSI:CA), as it was being advanced by the same management team that sold Otjikoto to B2Gold and had very similar geologies and operations.

Another possibility was to expand its mine operations in Mali via the acquisition of nearby deposits to feed into the Fekola complex. B2Gold’s acquisition of ASX-listed Oklo Resources was an example of this strategy.

However, B2Gold surprised investors by acquiring Sabina Gold and its large-scale Back River project in Nunavut, Canada, in 2023.

B2Gold Taking On A New Challenge

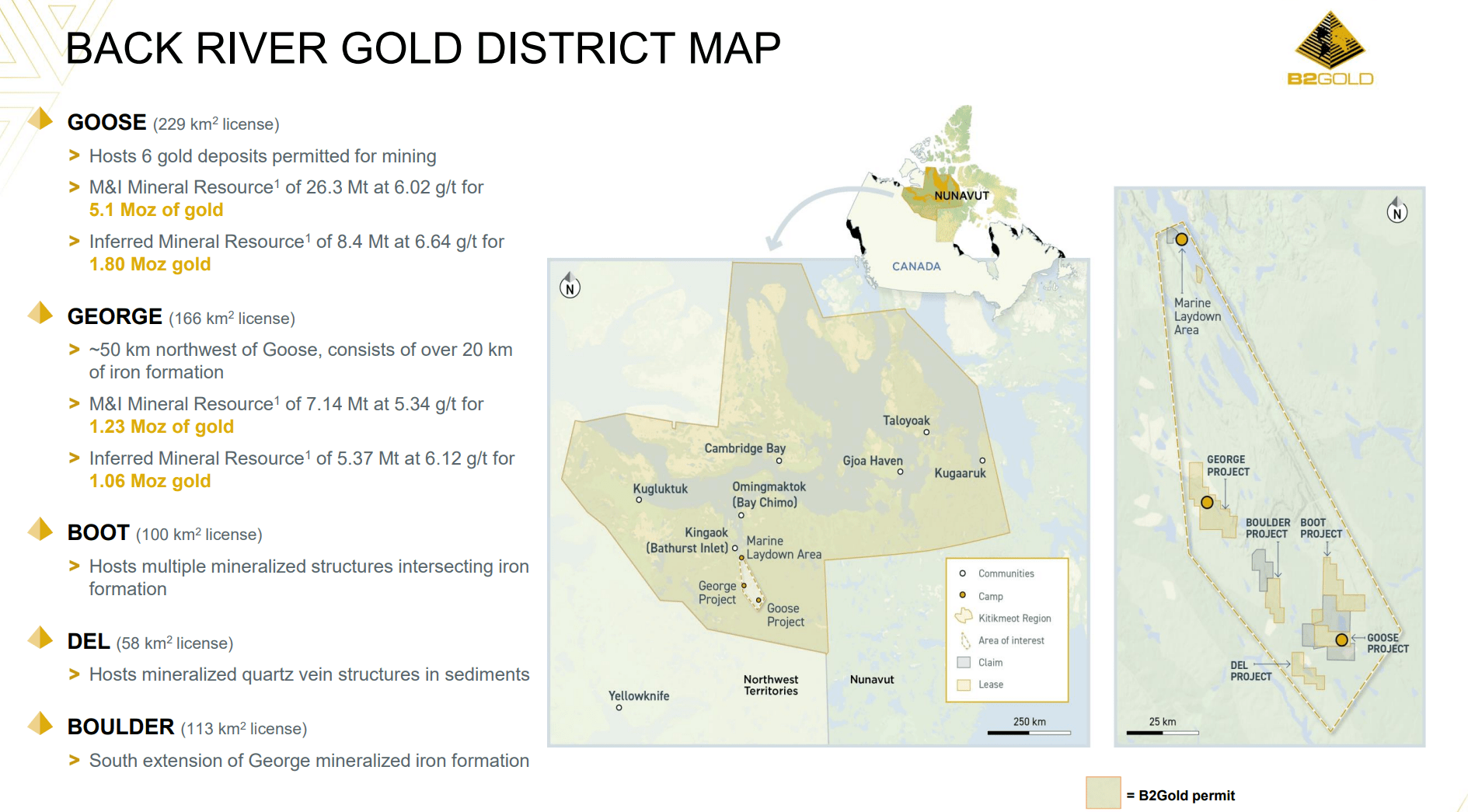

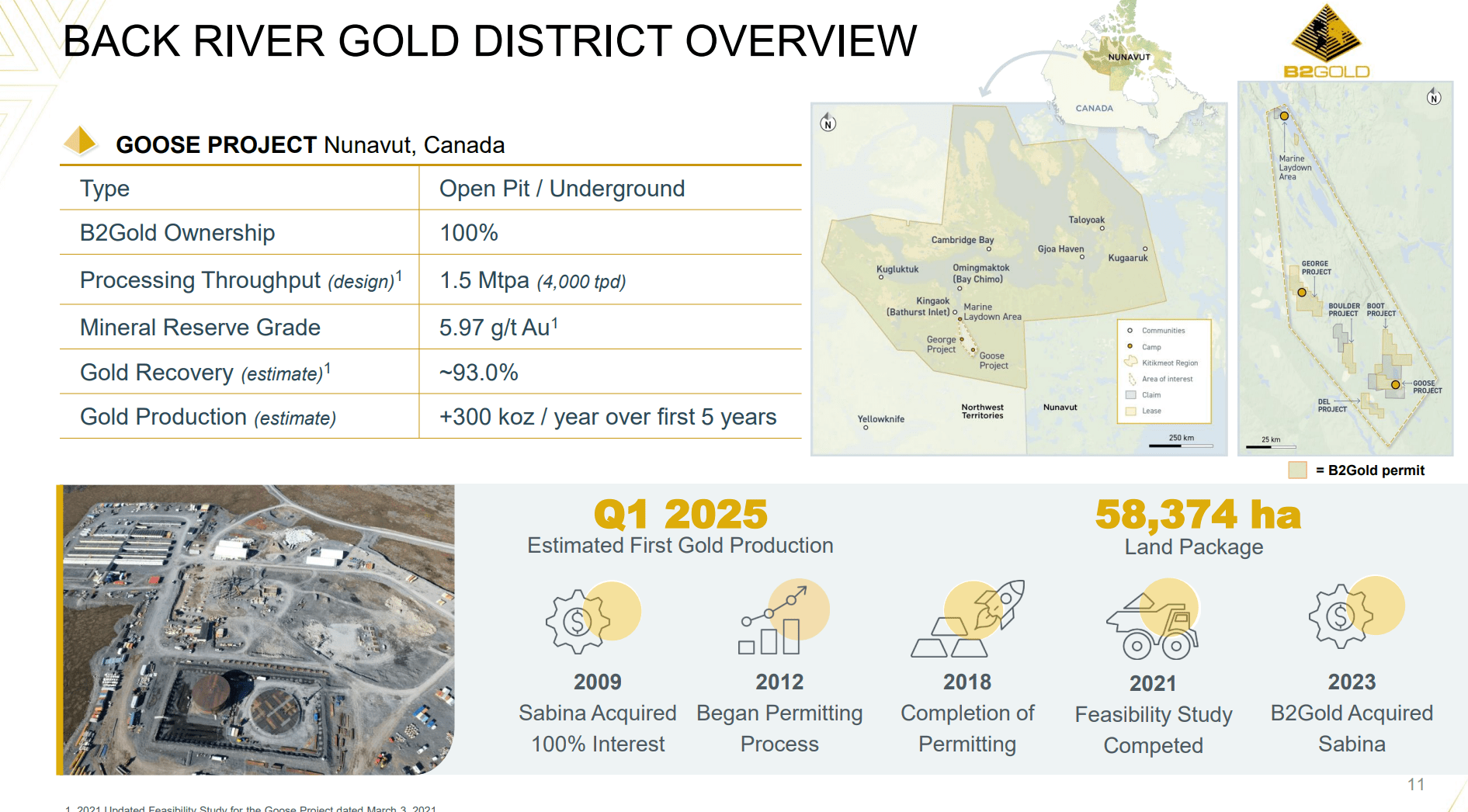

There is no doubt that Back River is a district-scale gold project with mineral resources of over 9 million oz of gold in 2 deposits (Goose and George) and almost unlimited exploration potential (Figure 2).

Figure 2 – Back River overview (BTG investor presentation)

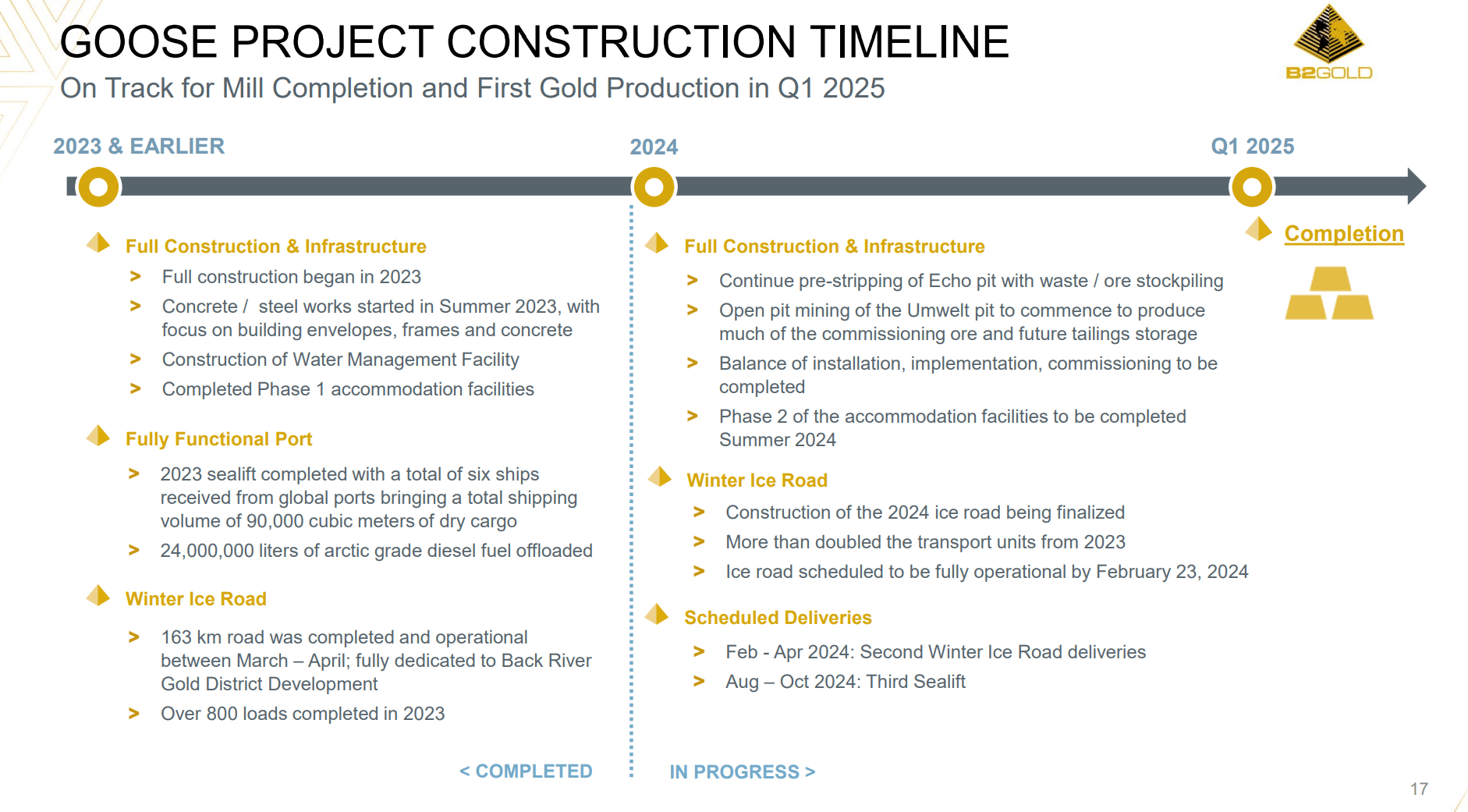

The challenge to Back River realizing its full potential has always been the remoteness of the project, as it is located in Nunavut, Canada’s far north. Geologyforinvestors gives a good overview of the challenges of working here, but as an example, B2Gold had to build its own seaport and winter ice road just to begin construction on the real project (Figure 3).

Figure 3 – Back River construction timeline (BTG investor presentation)

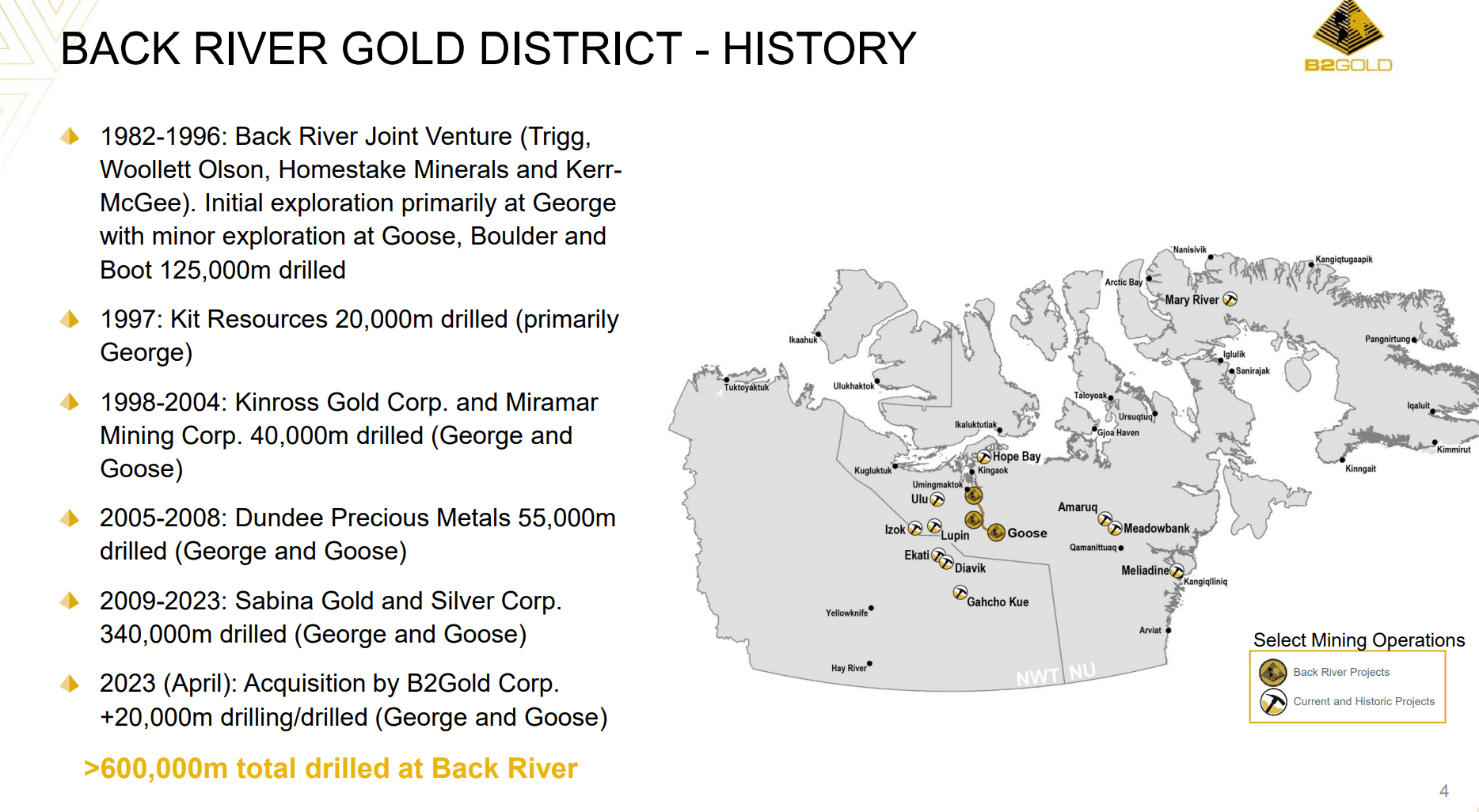

That is why despite being discovered in 1982, the Back River Gold District has never been fully developed until B2Gold acquired Sabina and greenlit the project (Figure 4).

Figure 4 – Back River history (BTG investor presentation)

Once complete in Q1/2025, Back River is expected to produce over 300k oz of gold p.a. in its first 5 years (Figure 5).

Figure 5 – Back River production estimates (BTG investor presentation)

Cost Overrun Was My Biggest Worry

While many fellow analysts and investors have been gushing about B2Gold’s dividend and ‘rebound potential’ for months, I have been more cautious due to the risks involved with developing the Back River project. As a long-time resource investor, I understand just how challenging building a mine can be, even in the best circumstances. However, in B2Gold’s case, it must also deal with extreme weather in the Canadian far north and inflationary pressures.

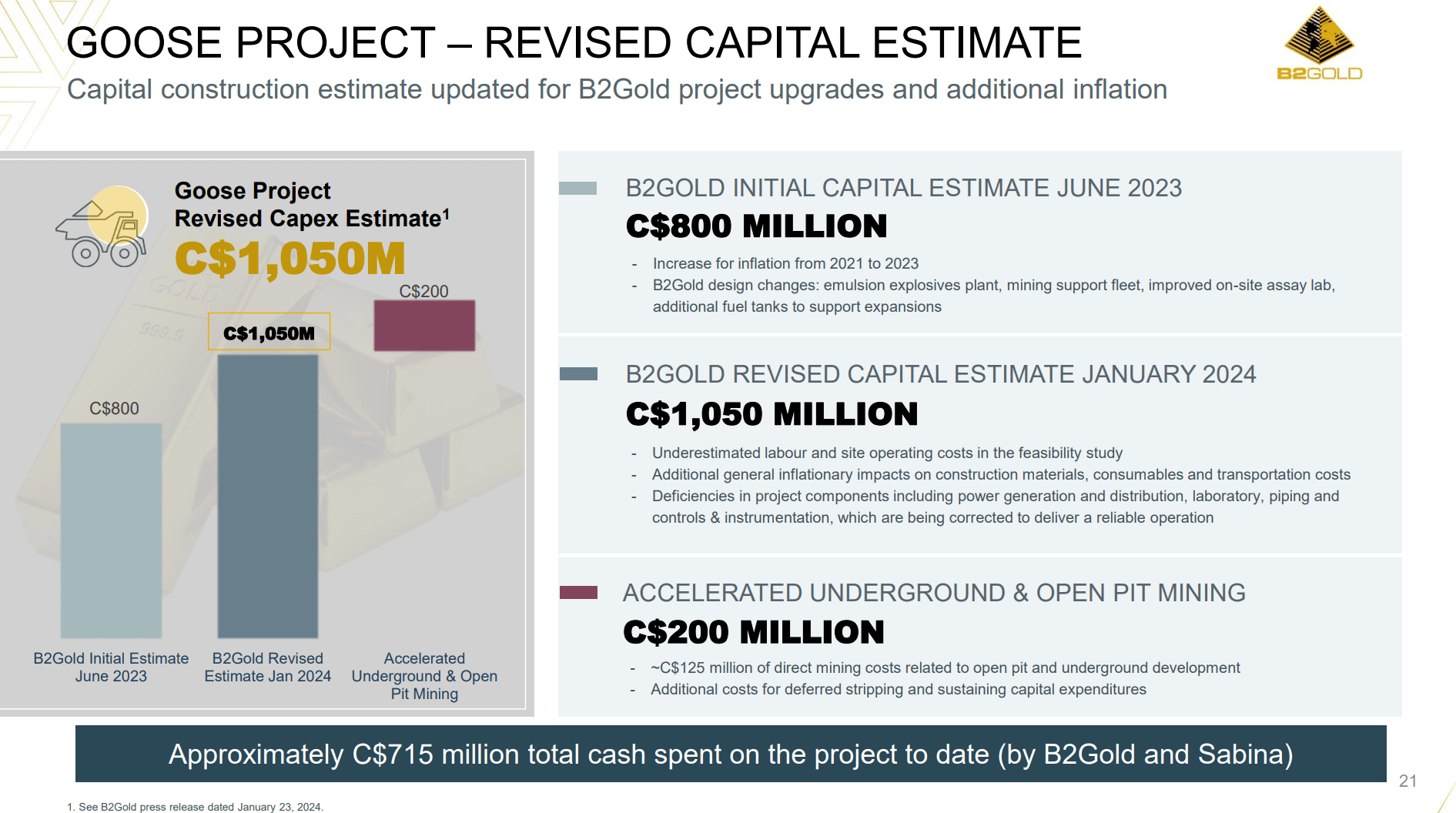

My fears were realized when B2Gold recently increased its project cost estimates by $450 million (+56%) vs. the company’s initial $800 million estimate from last June (Figure 6).

Figure 6 – Back River revised capital estimate (BTG investor presentation)

While I am hopeful that final costs will be within B2Gold’s revised $1.25 billion estimate, investors also need to be prepared for the risk that this figure can climb significantly as construction develops over the coming quarters.

To get a sense of how bad construction inflation can get, investors can study TC Energy’s (TRP) Coastal GasLink project in British Columbia’s relatively mild climate. When the project was initially sanctioned a few years ago, Coastal GasLink was estimated to cost C$6.6 billion. However, to date, Coastal GasLink’s costs have ballooned to C$14.5 billion (February 2023 estimate), and the final tally is likely even higher as construction has dragged into 2024.

Expect Outperformance Once Back River Costs Are Finalized

While history doesn’t repeat, it often rhymes. Investors currently considering B2Gold can get a sense of what has been driving its recent under-performance by studying the stock’s history.

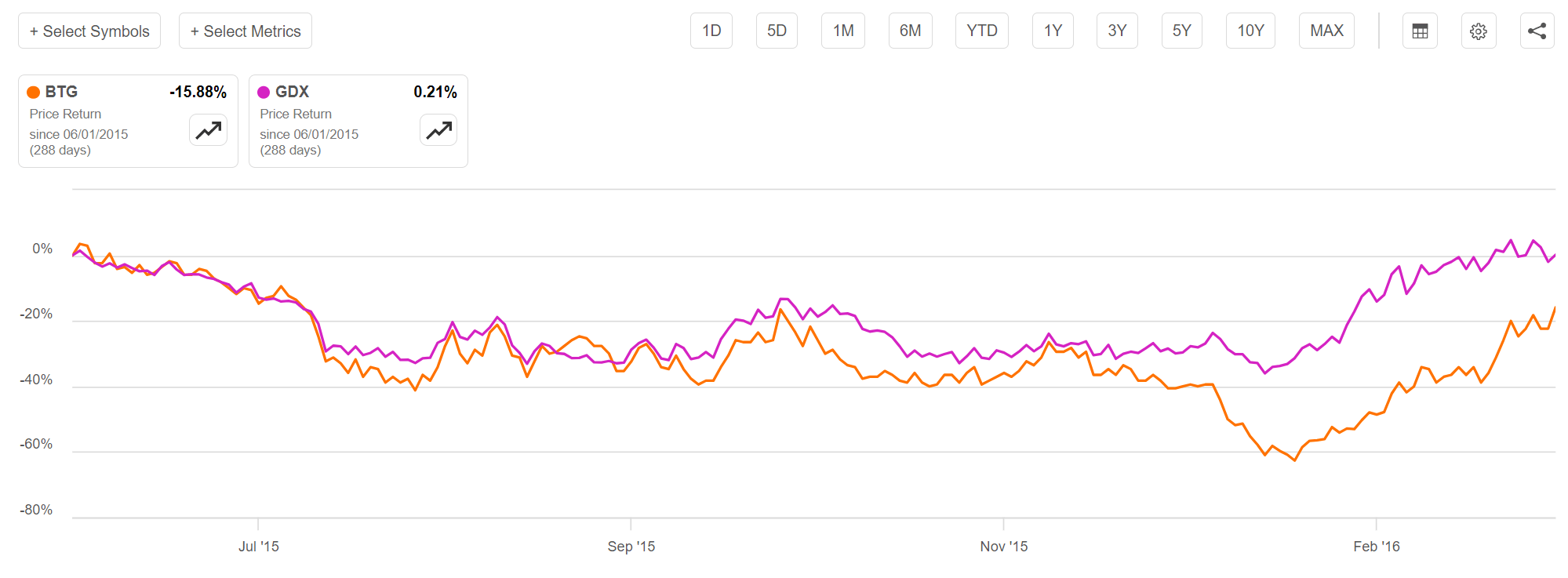

B2Gold underperformed the VanEck Gold Miners ETF (GDX) from when the Fekola mine was sanctioned in June 2015 to when the company arranged financing to fully fund Fekola’s construction in March 2016 (Figure 7).

Figure 7 – BTG underperformed GDX from June 2015 to March 2016 (Seeking Alpha)

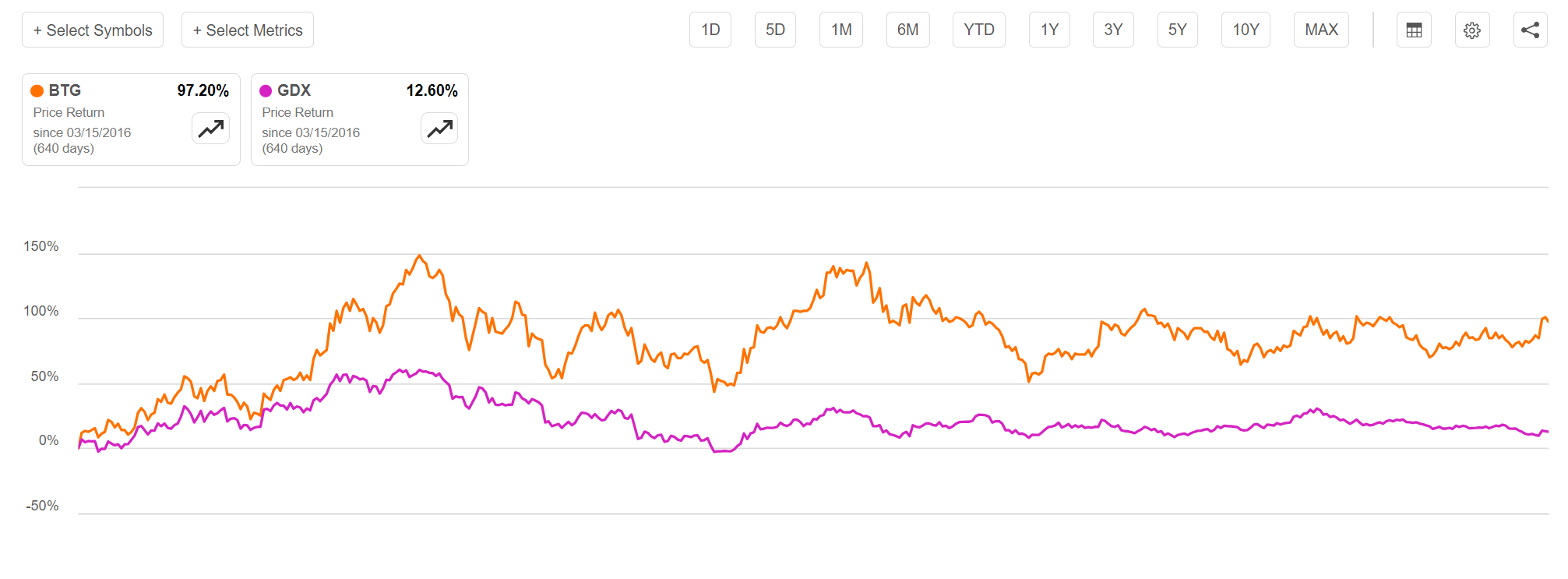

Incidentally, B2Gold also used forward gold sales to finance Fekola. Once financing was assured, then we saw B2Gold massively outperform its peers on a go-forward basis (Figure 8).

Figure 8 – BTG outperformed once financing was secured for Fekola (Seeking Alpha)

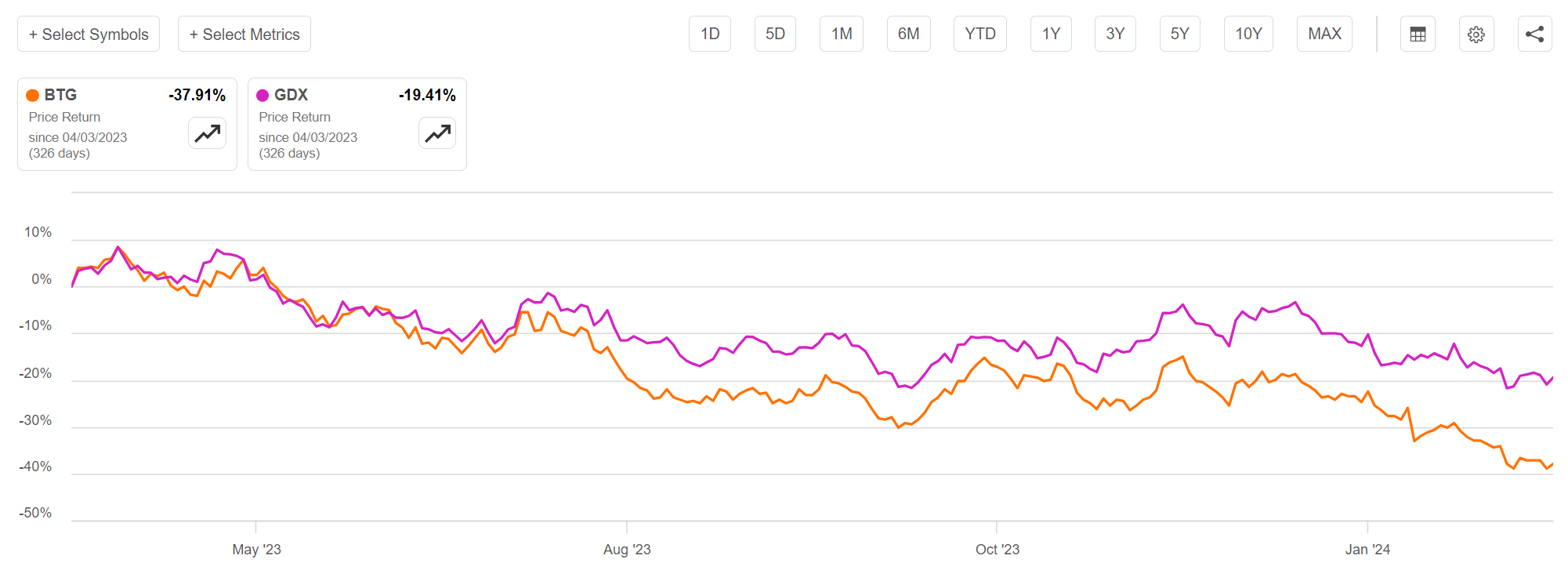

For B2Gold currently, it has underperformed GDX since the Sabina acquisition in April 2023, as the market did not believe the company’s initial cost estimates (Figure 9). Unfortunately, the market was proven correct when B2Gold recently released dramatically higher cost estimates.

Figure 9 – BTG has underperformed GDX since April 2023 (Seeking Alpha)

If the recent increase in costs is final, then we may see a bottom in B2Gold’s shares. If not, B2Gold may continue to underperform.

Despite Challenges, B2Gold Should Pull Through

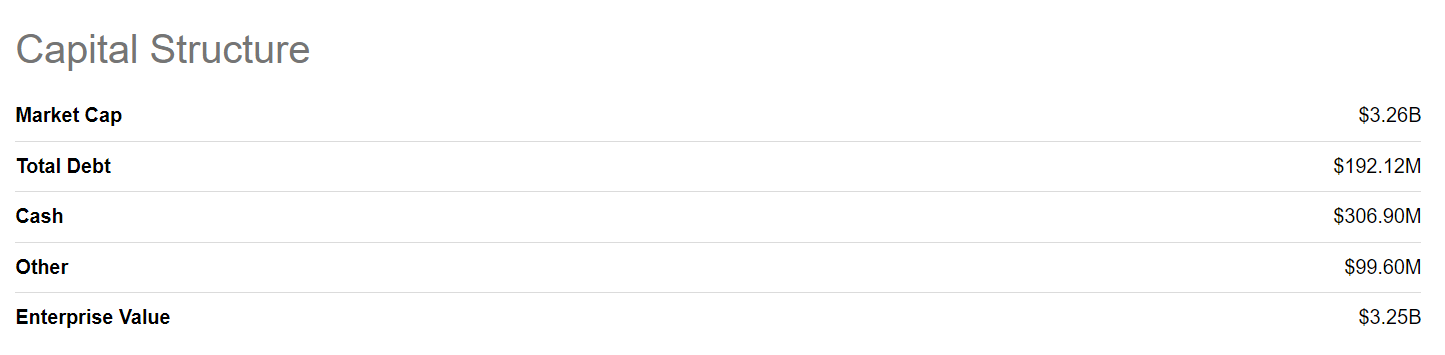

However, despite capital cost challenges, I do expect B2Gold will eventually pull through and complete the Back River project. B2Gold currently has a pristine balance sheet with only $190 million in debt versus LTM cash flows from operations (“CFO”) of $715 million (Figure 10).

Figure 10 – BTG enterprise value (Seeking Alpha)

Even if Back River capital costs overrun by a few hundred million dollars, B2Gold should be able to borrow this amount and complete the project without stressing its balance sheet.

An example of B2Gold’s ability to find financing is shown by the company’s recent announcement that subsequent to 2023 year-end, the company entered into a series of prepaid gold sales, receiving upfront payment of $500 million in exchange for 264,775 oz of gold from July 2025 to June 2026 at a gold forward price of approximately $2,191/oz. This represents approximately 10% of the company’s expected annual gold production in each of 2025 and 2026 and should fully fund the Back River capital overruns noted above without diluting shareholders.

Outlook Is Indeed Bright For B2Gold

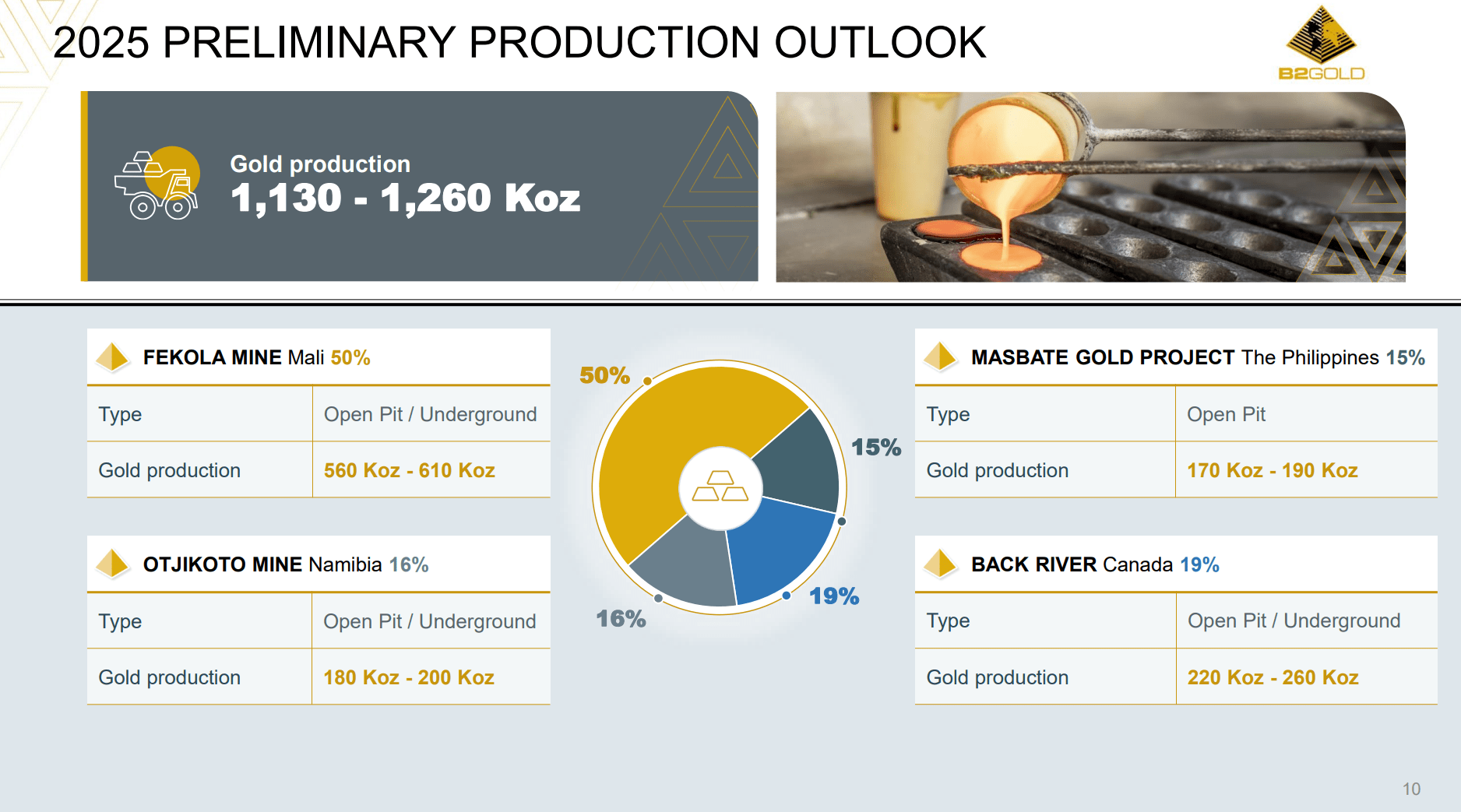

Once Back River is constructed, B2Gold should have annual production of ~1.2 million oz (Figure 11).

Figure 11 – BTG 2025 estimated production (BTG investor presentation)

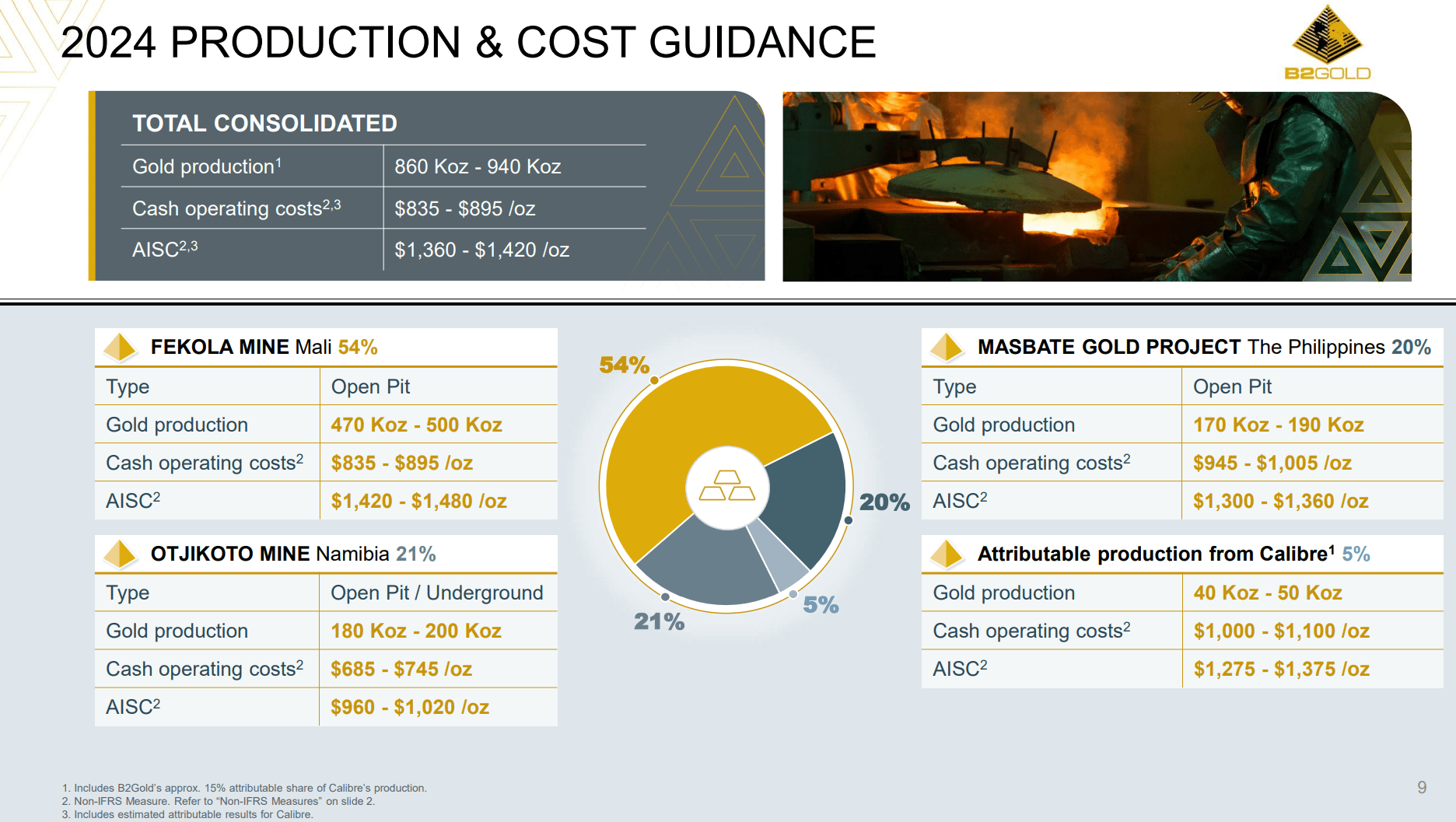

At current corporate all-in sustaining cost (“AISC”) estimate of ~$1,400/oz for 2024, this 1.2 million oz production could translate into ~$700 million in ‘free cash flows’ (“FCF”), assuming realized gold prices of $2,000 (Figure 12).

Figure 12 – BTG production cost guidance (BTG investor presentation)

Note, this FCF figure may be conservative, as Back River’s 2021 Feasibility Study showed cash costs of $679/oz and AISC of $775/oz. Although costs have risen considerably since 2021, Back River’s costs should still be lower than B2Gold’s current corporate average.

Hugely Successful Company But Investors Have Earned Subpar Returns

Taking a step back, B2Gold may be a perfect example of just how tough the gold mining business can be. By many measures, B2Gold is a huge success, as the company was able to go from 0 to ~1 million oz of production within 2 decades via shrewd M&A transactions and top notch mine-building.

However, investors who bought the IPO at C$2.50 would have only realized total returns of 66%, or 3.2% CAGR (Figure 13).

Figure 13 – B2Gold has only delivered 3.2% CAGR returns since IPO (Seeking Alpha)

That is why, for most investors without the time to understand the nuances of specific projects and companies, I recommend they stick to royalty companies like Wheaton Precious Metals (WPM) or the commodities themselves via bullion trusts like the SPDR Gold Shares ETF (GLD).

Simply ‘buying gold stocks for its 6% yield’ is unlikely to work if you do not understand what is driving the stock lower.

Risks To B2Gold

The biggest near-term risk to B2Gold remains cost overruns at Back River. As detailed above, until costs are finalized, B2Gold is unlikely to find investor support, no matter how ‘cheap’ it looks on paper.

Another risk with B2Gold has to do with its current production. As the company noted in its recent earnings release, 2024 production is expected to be 860-940k oz, a miss versus previous guidance and estimates due to “lower production at the Fekola Complex as a result of the delay in receiving an exploitation license for Fekola Regional from the Government of Mali, delaying the 80,000 to 100,000 ounces that were scheduled in the life of mine plan to be trucked to the Fekola mill and processed in 2024”.

Geopolitical risks, like the Mali license delay, is something that is hard to estimate and plan for. Throw in continued guerilla attacks and Fekola production may be further curtailed with little notice.

On the upside, as a gold producer, B2Gold will obviously benefit if gold prices increase. If gold prices rally significantly, then B2Gold’s shares should perform well on an absolute basis.

Conclusion

To be very clear, if one is buying B2Gold here, I believe one is making the bet that the costs for Back River are now realistic and will not rise any further. If that is indeed the case, then B2Gold should outperform its peers going forward.

I personally believe one can start to make that bet, given B2Gold’s track record of developing and building mines, so I rate B2Gold a speculative buy. Readers may make their own judgment.

Q2 2024 Earnings Call Transcript")