ASphotowed/iStock via Getty Images

Investment Thesis

I last covered AZZ Inc. (NYSE:AZZ) in early October when I preferred to remain on the sidelines due to mixed growth prospects and higher debt levels. The company’s outlook has improved since then as the upcoming interest rate cut should fuel recovery in some of its weaker markets. The company has also negotiated a slight reduction on its interest rate. This along with the upcoming reversal of the interest rate cycle should lower interest costs.

AZZ Inc. is poised to benefit from strength across its Infrastructure and commercial construction end markets supported by increased deployment of federal stimulus funds including the Infrastructure Investment and Jobs Act (IIJA), CHIPS and Science Act, and Inflation Reduction Act (IRA). Additionally, a higher probability of multiple rate cuts next year is expected to fuel the recovery in the residential and light commercial end markets. advance, improving demand in other end markets appreciate HVAC and appliances as well as easier Y/Y comparisons in the Precoat Metal business should benefit the company’s revenue in 2024.

On the margin front, I expect the company’s margin to remain flat sequentially but improve on a Y/Y basis benefitting from much easier comparisons in the coming quarters. The stock is trading at a discount to its 5-year historical average. Given good growth prospects and a discounted valuation, I am upgrading my rating on AZZ stock to a buy.

Revenue Analysis and Outlook

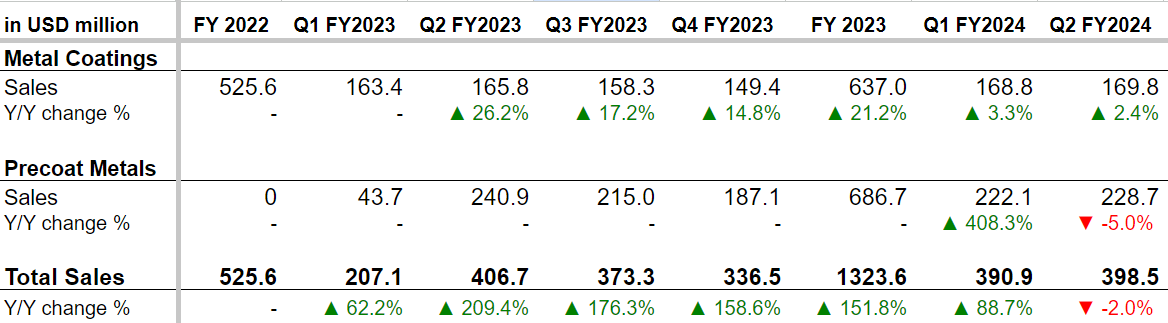

AZZ’s revenues have benefited from price increases as well as the acquisition of the precoat segment in FY23 as well as 1QFY24. However, as the end-markets slowed due to the tough macroeconomic environment, and the company anniversaried the first full quarter of precoat acquisition, the growth turned negative in Q2FY24. In the second quarter of 2024, AZZ Metal Coatings segment sales grew 2.4% Y/Y driven by a higher volume of steel processed and increased selling price. On the other hand, in the Precoat Metals segment, sales declined 5% Y/Y due to a lower volume of coil coated in HVAC, transportation, and certain construction end markets. The reject in precoat metals volume was partially offset by a 7% boost in average selling price attributed to value-pricing initiates and a shift in sales mix. On a consolidated basis, sales declined 2% Y/Y to $398.5 million in the third quarter.

AZZ’s Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, I am optimistic about the company’s growth outlook. While the slowdown in residential and commercial construction was a big worry at the time of my previous coverage, the recent development around the interest rate environment with increased expectations for multiple rate cuts next year bodes well for these markets. This increases the possibility that all three of the company’s construction end markets – infrastructure, commercial, and residential will turn positive as calendar year 2024 progresses. The construction-related revenues account for ~54% of the company’s total revenues. So, this is a big positive.

In the construction business, the Infrastructure construction which has been already seeing a good demand should continue to benefit from the increasing deployment of funds under the Infrastructure Investment and Jobs Act. In commercial construction, heavy manufacturing construction demand is already strong given the recent reshoring trend catalyzed by the CHIPS and Science Act and Inflation Reduction Act. In this market also, the increased deployment of federal stimulus funds should continue to help the end-market demand in 2024. advance, the light construction end-market, which has been seeing some weakness of late, should also pick up as the interest rate cycle starts reversing increasing the return potential of commercial projects and making many projects more viable. The residential construction market has a very favorable demand-supply situation with over a decade of underbuilding after the great housing recession of 2008. I believe this market should see a swift recovery once the interest rates start coming down increasing affordability for many new home buyers.

In addition to construction end markets, the company is also seeing the bottom in other end markets appreciate HVAC and appliance which were seeing some reject in the past few quarters. On the last earnings call, talking about these end markets, the company’s SVP of IR David Nark said,

I think as you look at it, as I mentioned in my commentary, the — some of the end markets are seeing the bottom, residential being 1 of them. And we think that HVAC and appliance are certainly tied to that. As you look forward, some of the customers that we’ve talked to in both the HVAC and appliance end markets are seeing the bottom and feeling optimistic about the balance of the year. So we’ll see how things go with them, and — but we think it certainly is going to be improved over the prior year.”

In addition to improving end markets, the company should also benefit from easing comparisons in its precoat business. The company’s precoat sales saw a meaningful sequential reject in sales for Q3 FY23 ($215 mn) and Q4 FY23 ($187.1 mn) versus Q2 FY23($240.9 mn.) So, the comparisons are getting easier as we proceed into the second half of FY24 (ending February 2024) which should help precoat sales turn positive.

Overall, I’m optimistic about the company’s revenue growth prospects.

Margin Analysis and Outlook

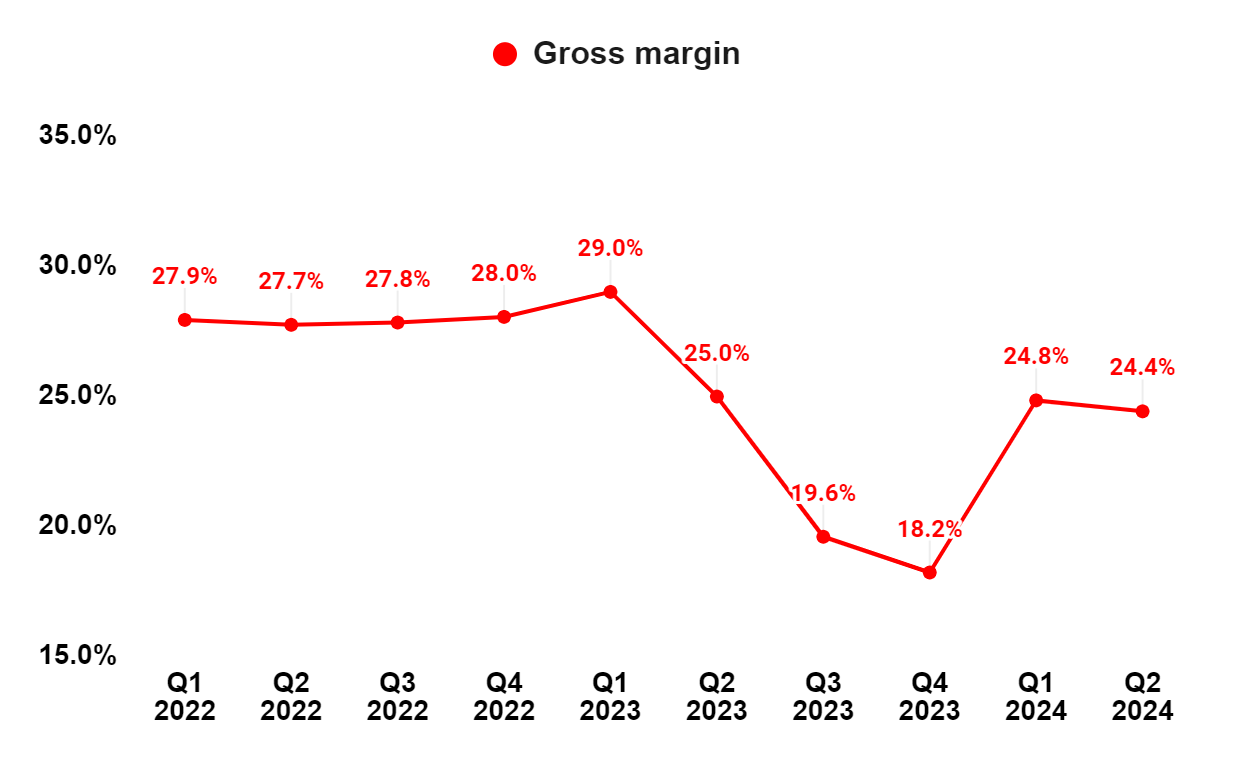

In Q2 2024, AZZ continued to encounter higher labor and zinc costs in the Metal Coatings segment, which negatively impacted its gross margin. This pressure was partially offset by the lower costs of sales and lower freight and storage costs in the Precoat Metals segment. As a result, the consolidated gross margin contracted by 60 bps Y/Y to 24.4%.

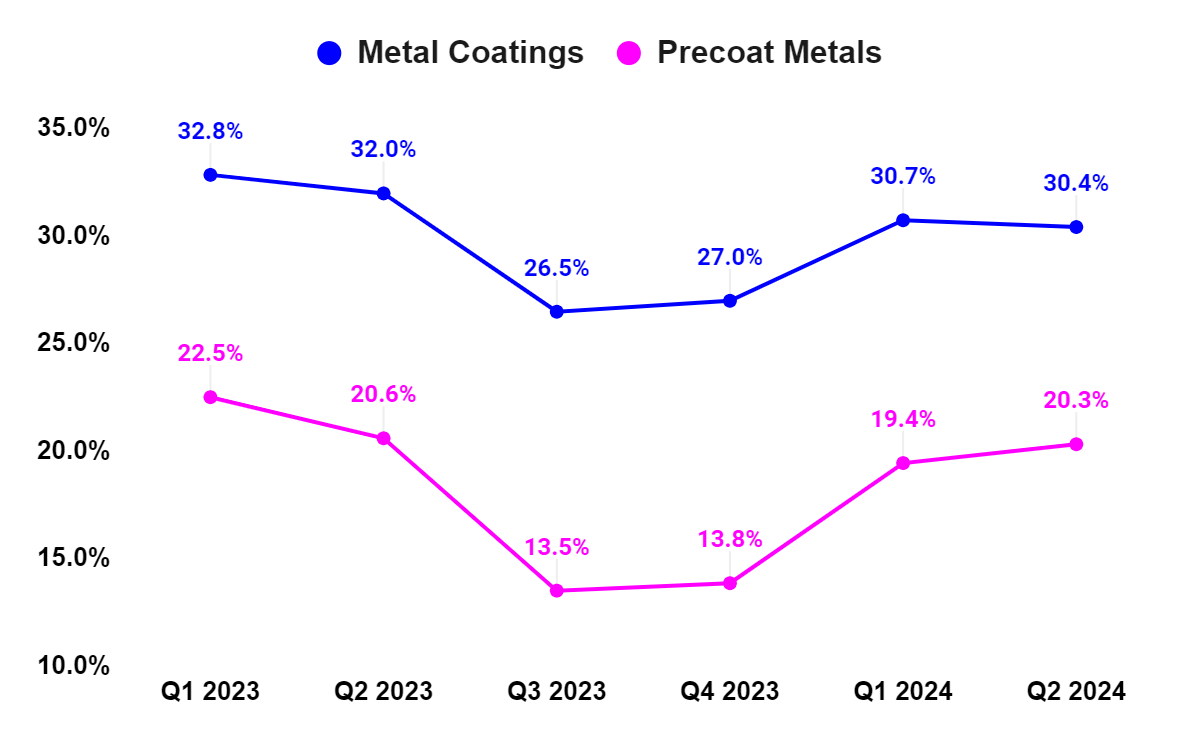

On a segment basis, the EBITDA margin in the Metal Coatings and Precoat Metals segments declined 160 bps Y/Y and 30 bps Y/Y, respectively.

AZZ’s Consolidated Gross Margin (Company data, GS Analytics Research)

AZZ’s Segment-Wise EBITDA Margin (Company data, GS Analytics Research)

Looking forward, the company’s margins are seeing a much easier Y/Y comparison which should result in Y/Y margin improvement. In the back half of 2023 and early FY24, the company faced a negative impact from precoat clients storing excess inventory at the company’s warehouse while dealing with supply chain disruptions. This created some inefficiencies and negatively impacted margins. The normalization in this situation has been helping the company post a sequential improvement in margins over the last few quarters.

I am not expecting any advance sequential improvement as things have already returned to normal. Similarly, the Metal Coatings business was impacted by high zinc prices but the situation has returned to normal there as well. So, sequentially I am expecting the company’s margins to remain around Q2 levels. However, there should be a good Y/Y improvement due to easing comparisons.

Net Leverage and Interest

One of the concerns I was having about the company was its high net leverage and over $1bn of variable interest rate debt (about half of which is hedged through interest rate swaps) where the interest rates were quite high. The company marginally reduced its debt by $40 mn in the last quarter and its net leverage (net debt to EBITDA [TTM]) at the end of Q2 FY24 was 3.4x versus 3.5x at the end of Q1 FY24. The company intends to advance reduce its debt as the year progresses which coupled with improvement in EBITDA should result in net leverage of less than 3x by the end of the year, as per management guidance.

In addition to reducing debt, the management was also able to reprice its $1.03 bn term loan B reducing its interest rates by 50 bps from SOFR plus 425 to SOFR plus 375. This should result in ~$5 mn of interest cost savings annually. advance, given half of this variable interest debt is still unhedged the upcoming reversal in the interest rate cycle should help the company’s interest effective interest outgo.

Valuation and Conclusion

AZZ is currently trading at 13.04x FY24 (ending Feb.) consensus EPS estimates and 11.88x FY25 consensus EPS estimates, which is at a discount compared to the company’s average forward P/E of 15.49x over the last 5 years.

I believe the company possesses good growth prospects thanks to the potential reversal in the interest rate cycle helping the recovery in residential and light construction end markets, increased deployment of federal stimulus funds benefitting construction and commercial end markets, favorable demand-supply dynamics in the residential end market, bottoming of end markets including HVAC and appliance, and easier comps in the precoat business. I expect the margins to be flat sequentially, but post Y/Y improvement benefitting from easier comps.

While I am still not thrilled about the current net leverage, I believe the upcoming reversal in the interest rate cycle, management’s focus on debt reduction, and improving end market outlook (which should help boost EBITDA thereby reducing the leverage ratio) indicates that the company can become an interesting deleveraging story moving forward. The valuation also looks attractive compared to its historical levels. Considering the company’s improving growth prospects and a reasonable valuation, I am upgrading my rating to a buy on AZZ stock.

Q2 2024 Earnings Call Transcript")