Hispanolistic

AutoNation, Inc. (NYSE:AN) recently delivered better than expected quarterly EPS, and noted beneficial words about 2024 cash flow and future vehicle supply and demand dynamics. In addition, I detected an increase in capital expenditures for growth initiatives for AN USA as well as IT and electrification efforts, which, in combination with cash acquisitions, made AutoNation a buy. Yes, there are risks with respect to changes in the credit markets, changes in the environmental regulations, and recent severance initiatives. With that being said, AN appears to be a buy at its current stock valuation.

AutoNation

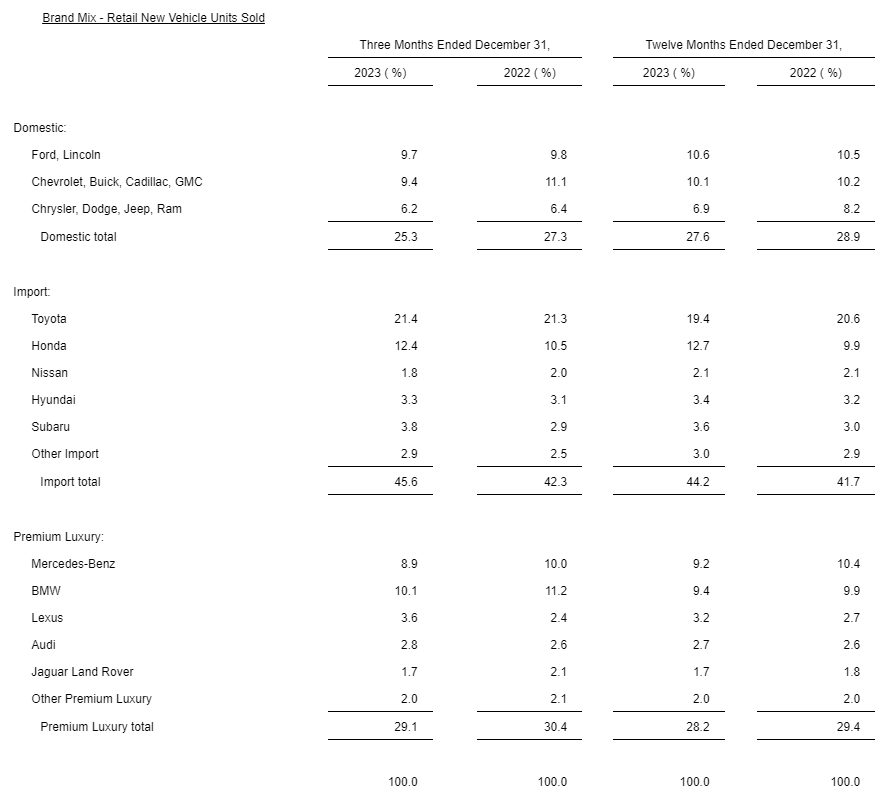

AutoNation, Inc., through its subsidiaries, is a large automotive retailer with vehicle franchises located in the United States. The company runs a network of dealerships with a wide variety of new and used vehicles, and offers customer financing, auto parts, and expert maintenance and repair services. AutoNation specializes in high-end brands like Honda, BMW, Ford, Mercedes-Benz, General Motors, Stellantis, Volkswagen, Audi, and Porsche. The following is a list of brands of retail new vehicles sold in 2023 and 2022.

Source: Quarterly Press Release

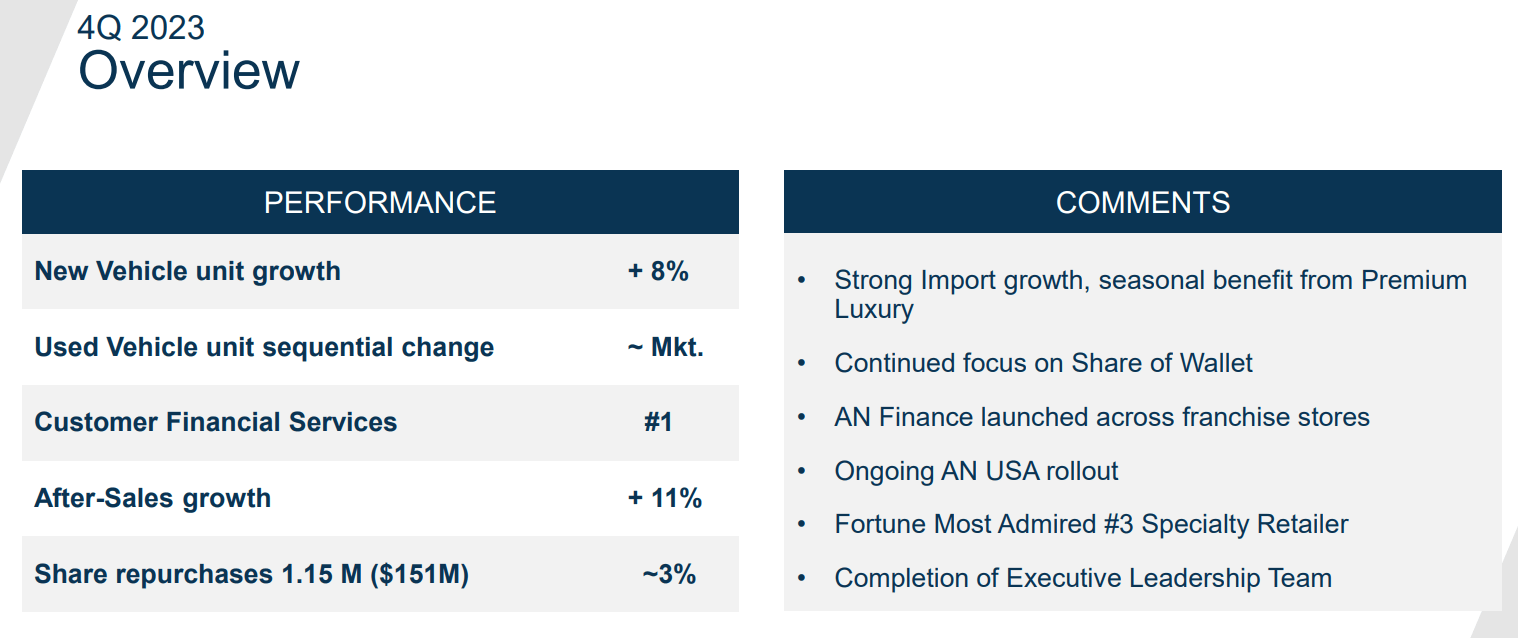

I believe that it is a great time to review AutoNation mainly because of the guidance given for 2024 and the words from management. In the last quarterly release, the company noted beneficial expectations with regard to vehicle supply and demand dynamics. In addition, AutoNation called its 2024 cash flow expectations very strong. With such type of words, I believe that many investors will most likely have a look at the company’s business model in the coming months.

While 2024 will reflect a continued normalization of vehicle supply and demand dynamics, we are excited to move forward, confident in our strong balance sheet, and laser-focused on executing our operating plan. We will continue to be a strong cash generator and allocate capital in a prudent manner to maximize shareholder returns. Source: Press Release

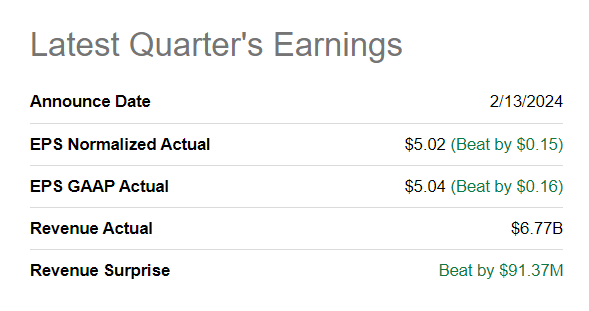

Some of the numbers reported in the last quarter were also quite beneficial. EPS GAAP Actual was close to $5 per share with larger quarter revenue than expected of $6.7 billion. In addition, AutoNation reported strong import growth, new vehicle unit growth of 8%, and double digit after-sales growth. Besides, we may see further increase in net sales because AN Finance was said to be launched across franchise stores.

Source: Presentation Source: Seeking Alpha

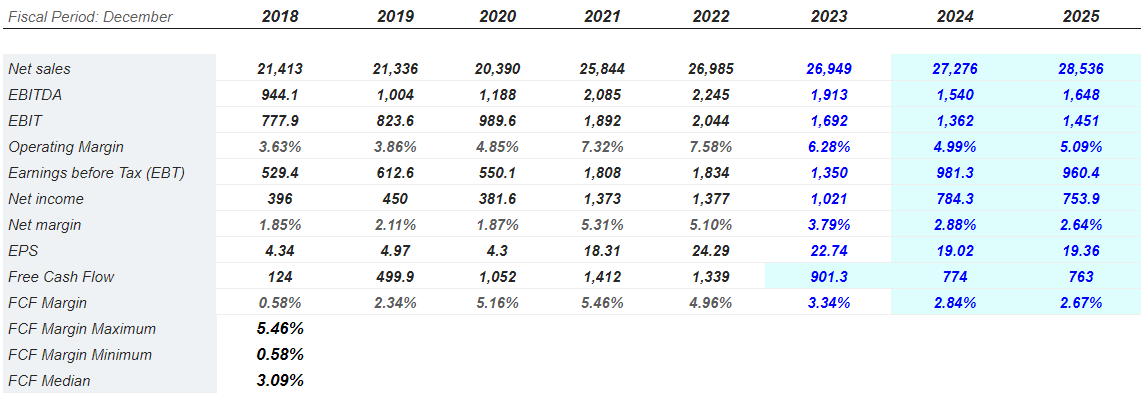

The numbers delivered by other investment analysts also seem beneficial. 2025 net sales are expected to be close to $28.536 billion, a bit better than that in 2024 and 2023. 2025 EBITDA is expected to be close to $1.648 billion, a figure that seems higher than the expected number for 2024. Free cash flow is not expected to grow in 2024 and 2025, however the FCF margin is expected to be around 2.8%-2.67%. The FCF margin in the past was only 3%-4% higher than what the company could report in 2025.

Source: Market Screener

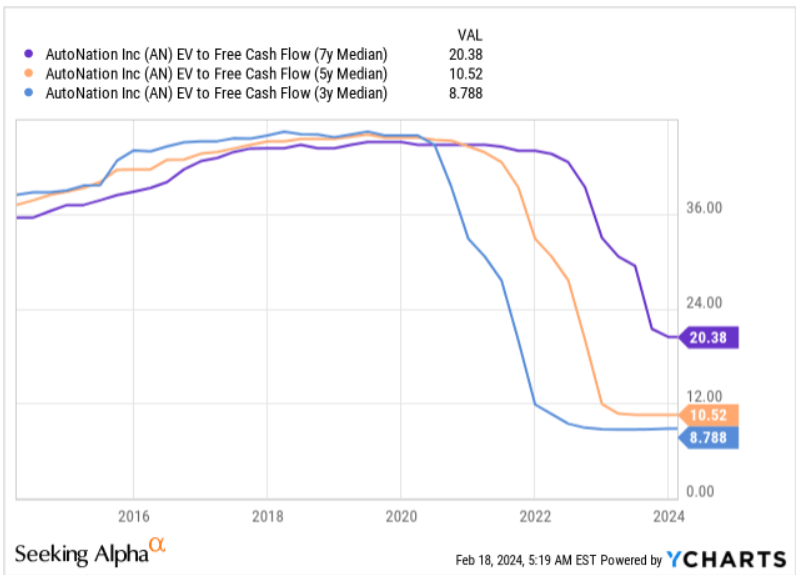

With the previous figures, I think that the current EV/EBITDA and EV/FCF do not seem a bit low. In the past, the company traded at double EV/FCF. The recent decline in the valuation was quite impressive.

Source: Market Screener Source: Ycharts

Equity Increased In 2023

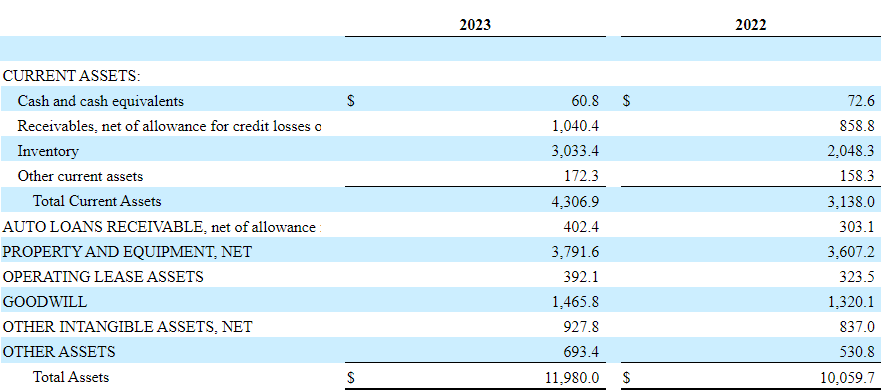

The balance sheet figures in the last quarter included a significant increase in inventory as compared to the figures noted in December 2022. AutoNation seemed to finance the increase in inventory with a combination of non-vehicle debt and notes payable. It is worth noting that the total amount of equity increased in 2023, which the market did not seem to recognize. The stock went from trading at around $180 per share in August 2023 to less than $144 per share in 2024.

More in particular, the company noted cash and cash equivalents worth $60 million, with receivables worth $1040 million, inventory of about $3033 million, and total current assets worth $4306 million. Besides, with property and equipment of about $3.791 billion and goodwill of close to $1.465 billion, total assets stood at $11.980 billion.

Source: 10-k Source: Seeking Alpha

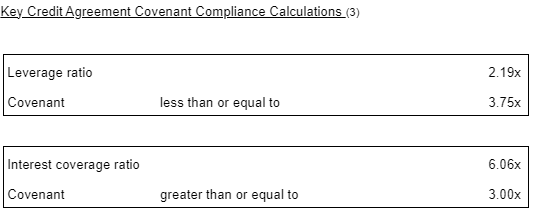

I am not concerned about the total amount of debt because the Company’s covenant leverage ratio was 2.19x, which is below the limit imposed by debt holders. Besides, AutoNation appears to have $1.46 billion of availability under a revolving credit facility.

Source: Quarterly Report

As of December 31, 2023, AutoNation had $1.5 billion of liquidity, including $61 million in cash and $1.46 billion of availability under its revolving credit facility, net of commercial paper borrowings. The Company’s covenant leverage ratio was 2.19x at quarter-end and the Company had $4.0 billion of non-vehicle debt outstanding. Source: 10-k

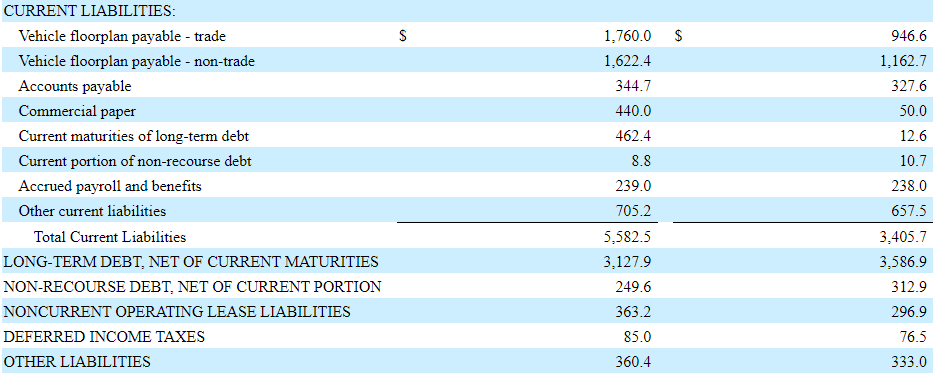

The list of liabilities included Vehicle floorplan payable worth $1622 million, with accounts payable of close to $344 million and total current liabilities of close to $5582 million. The current ratio is lower than 1x, however given the total inventory accumulated, I believe that banks would offer more financing to AutoNation if necessary.

Long-term debt stands at close to $3.127 billion, with non-recourse debt of $249 million, noncurrent operating lease liabilities of about $363 million, and other liabilities of close to $360 million.

Source: 10-k

Assumption # 1: Capital Expenditures Will Most Likely Lead To Capacity Growth, IT, And Electrification

AutoNation appears to be making significant capital expenditures to increase capacity in the United States as well as to enhance IT and electrification efforts. I believe that these investments will most likely serve as net sales catalysts.

Source: Presentation

In 2023, capital expenditures stood at close to $410 million, 24% more than that in 2022. In my view, further CAPEX acceleration will most likely lead to capacity increases and perhaps more stock demand from investors.

Source: Quarterly Report

Assumption # 2: Acceleration Of Cash Acquisitions Will Most Likely Lead To FCF Margin Growth

AutoNation reported an increase in the cash used for acquisitions in 2023 as compared to that in 2022. The company acquired a mobile solution for automotive repair and maintenance, and also purchased seven stores. In my view, further acceleration of the number of acquisitions could lead to economies of scale, net sales growth, and FCF margin growth.

Source: Quarterly Report

I do appreciate that management did not issue new shares. Given the price paid in the market for the shares and the state of the balance sheet, cash appears to be the right option. Moreover, it is worth noting that severance expenses increased to close to $6.6 million in 2023. In 2022, the company did not seem to report any severance expenses. In my opinion, efforts made by AutoNation may have a beneficial impact on future cash flow statements.

Source: Quarterly Report

Assumption # 3: Stock Repurchase Acceleration May Push The Stock Price Up

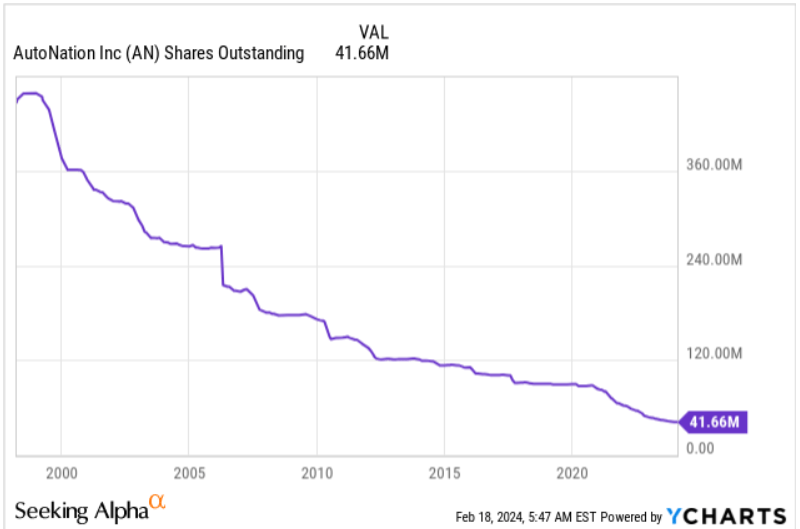

In the last quarter, I observed acceleration in the total amount of shares acquired under the stock repurchase plan. AutoNation repurchased 1.15 million shares. The decrease in the share count seen since the year 2000 is remarkable. I believe that at some point the demand for the stock may lead to price increases. In the year 2000, the total amount of shares was more than 360 million. Right now, the share count is close to 41 million.

During the quarter, AutoNation repurchased 1.15 million shares of common stock (3% of shares outstanding at start of quarter) for an aggregate purchase price of $151 million. As of February 9, 2024, AutoNation had approximately $320 million remaining under its current Board authorization for share repurchases. For the full year 2023, AutoNation repurchased 6.4 million shares for $864 million, reducing shares outstanding by 13% during the year and more than 50% since the end of 2020. Source: Quarterly Press Release

Source: Ycharts

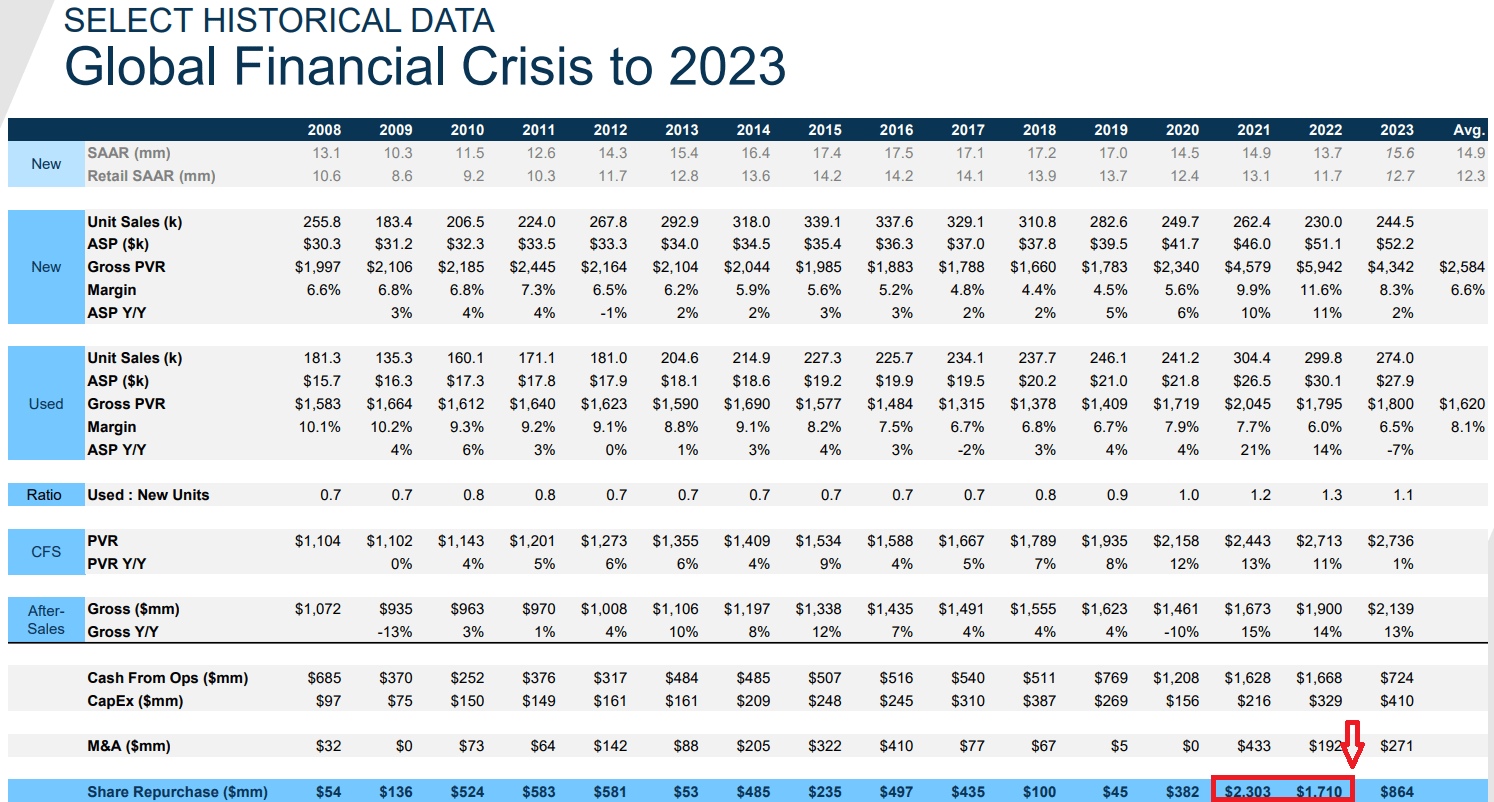

I also believe that it is worth studying the recent acquisition of shares. In 2021, 2022, and 2023, shares acquired were significantly higher than that in the past. In my view, AutoNation is buying more of its shares right now because they are trading at multiyear low valuations.

Source: Presentation

FCF Expectations Under My Best-Case Scenario

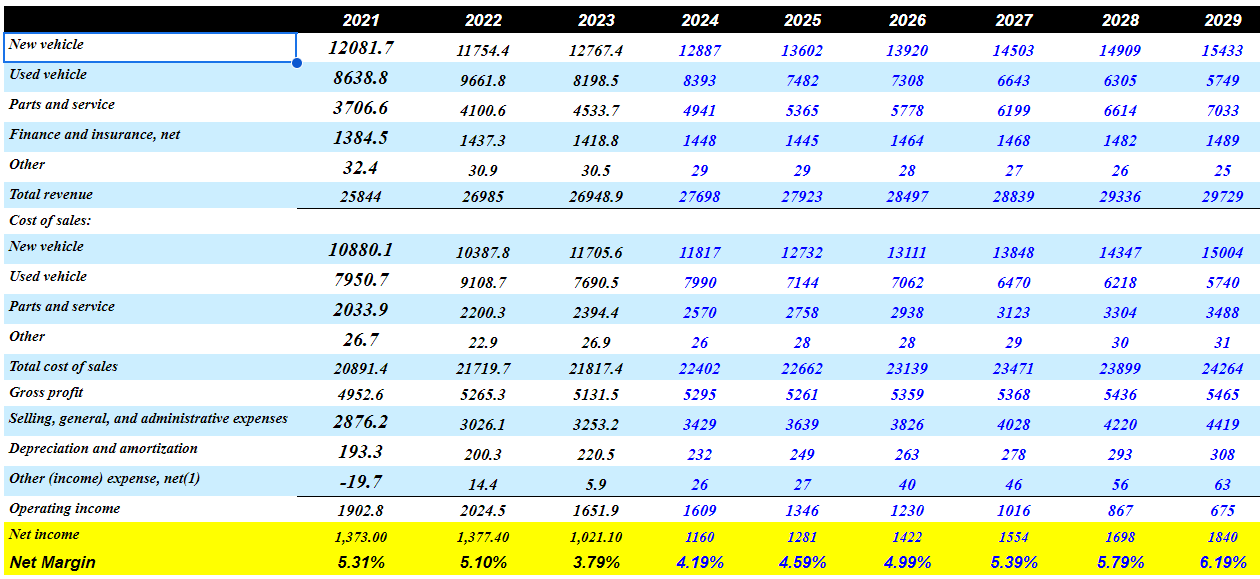

Under my base-case scenario, I assumed 2029 new vehicle sales of $15.433 billion, used vehicle sales of $5748 million, and parts and service worth $7032 million. Total revenue would be close to $29.729 billion.

I also included 2029 new vehicle cost of sales worth $15003 million, used vehicle costs of $5740 million, parts and service of about $3488 million, and total cost of sales of about $24263 million.

Finally, gross profit costs would be close to $5.465 billion, with selling, general, and administrative expenses of about $4419 million, depreciation and amortization close to $308 million, and 2029 net income of about $1.839 billion.

Source: My Expectations

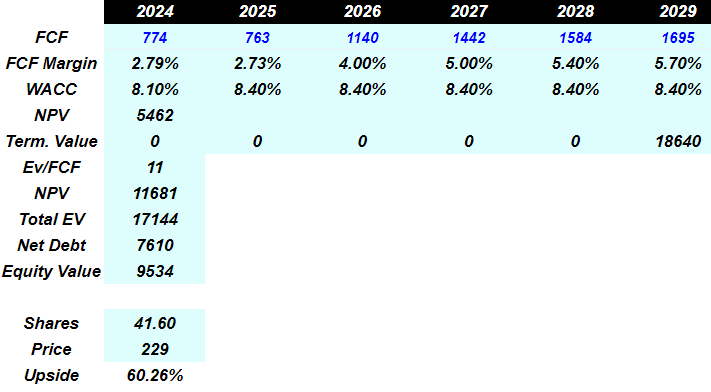

Now, with a FCF margin ranging from 2.7% to 5.7%, a WACC of 8.4%, and an exit multiple of 11x, the implied enterprise value would be close to $9.53 billion, and the implied valuation would be close to $230 per share. We would be talking about an upside potential of close to 60%.

Source: My Expectations

Risks Associated To My Worst-Case Scenario

AutoNation depends on several vehicle manufacturers. In my view, if the company fails to negotiate an adequate product mix and affordable prices, both the demand for the company’s cars and the FCF margin will most likely decline. In addition, if the company fails to receive direct financial assistance or advertising assistance from vehicle manufacturers, or competitors receive more help, AutoNation’s cash flow statement may also suffer. In this regard, management gave the following explanation.

The success of our stores is dependent on vehicle manufacturers in several key respects. First, we rely exclusively on the various vehicle manufacturers for our new vehicle inventory. Our ability to sell new vehicles is dependent on a vehicle manufacturer’s ability to design, manufacture, and allocate to our stores an attractive, high-quality, and desirable product mix at the right time and at the right price in order to satisfy customer demand. Second, manufacturers generally support their franchisees by providing direct financial assistance in various areas, including, among others, floorplan assistance and advertising assistance. Third, manufacturers provide product warranties and, in some cases, service contracts to customers. Source: 10-k

I also believe that changes in the credit conditions could affect the company’s net income results. In particular, if clients do not successfully receive lending to acquire cars, net sales may lower.

We are subject to various risks associated with originating and servicing auto finance loans through indirect lending to customers, any of which could have an adverse effect on our business. Source: 10-k

I would also be a bit concerned in case the interest rates increase. As a result, AutoNation may have to renegotiate its debt agreements. The covenant ratio limit may lower, which may lead to detrimental consequences. Management may not be able to acquire other companies, or certain expenses may be limited.

AutoNation’s future cash flow statements may also suffer from new changes in the environmental regulations. New taxes or governmental initiatives could limit the company’s EBITDA margin. In addition, changes in the behavior of consumers with regard to this matter may also lower future net sales growth.

Concerns over the long-term impacts of climate change have led and will continue to lead to governmental initiatives aimed to mitigate those impacts. Consumers may also change their behavior as a result of these concerns. We will need to respond to new laws and regulations as well as consumer preferences resulting from climate change concerns which may affect vehicle manufacturers’ ability to produce cost effective vehicles. Source: 10-k

Worst-Case Scenario

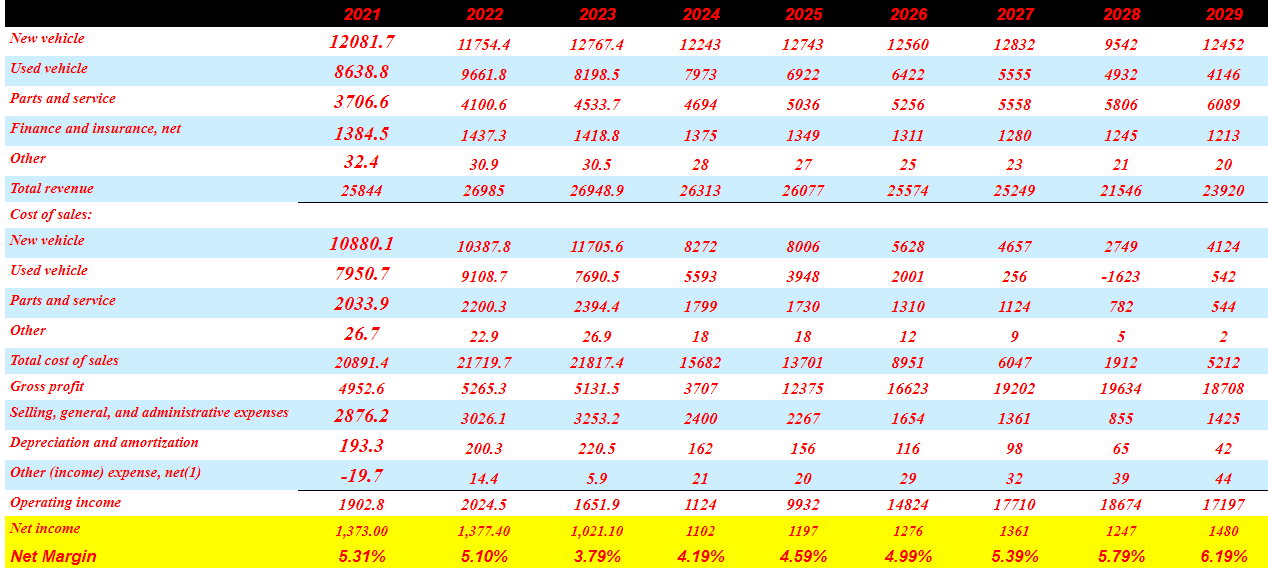

Under this case scenario, I included the following assumptions. 2029 new vehicle sales would stand at close to $12.452 billion, with used vehicles of about $4.146 billion, parts and service worth $6089 million, finance and insurance close to $1.212 billion, and total revenue of close to $23.920 billion.

With costs for used vehicles being close to $542 million, parts and service costs of $544 million, and total cost of sales worth $5211 million, 2029 gross profit would be close to $18.708 billion. If we also assume 2029 selling, general, and administrative expenses of about $1.425 billion and depreciation and amortization close to $42 million, net income would stand at $1.480 billion.

Source: My Expectations

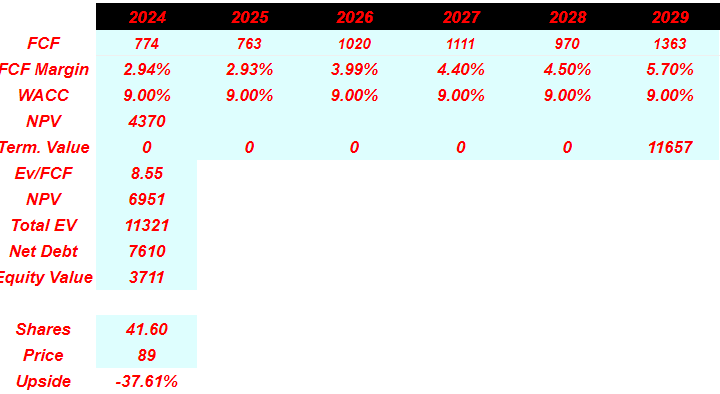

Under the previous assumptions, a WACC of 9%, and EV/FCF terminal multiple of 8.55x, the implied equity valuation would be close to $89 per share, and the market capitalization would not be far from $3.71 billion.

Source: My Expectations

Conclusion

AutoNation reported better than expected EPS, and delivered beneficial words with respect to future cash flow in 2024 as well as vehicle supply and demand dynamics. I also think that further increases in capital expenditures to build further demand, growth initiatives in AN USA, and IT and electrification could bring net sales growth expectations. The recent increase in acquisitions financed with cash and recent increases in severance costs are also worth noting. Even taking into account risks from new environmental regulations or changes in the credit markets, I believe that AutoNation appears quite cheap right now. It looks like a buy.

Q2 2024 Earnings Call Transcript")