georgeclerk

Aston Martin (OTCPK:AMGDF) is a storied carmaker but has been a disaster for many stock investors since its 2018 listing (bondholders have done well). Its cars are lovely, but for now its finances attract me less.

I last covered Aston Martin with my June 2023 “hold” piece Aston Martin: A Lot Still To Prove.

The Company has Been Raising More Finance

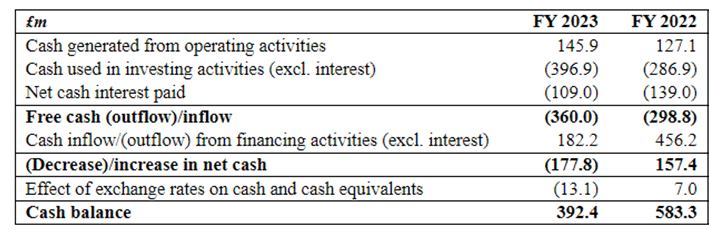

Net debt at the end of last year was £814m, an increase of 6% compared to the prior year position.

The balance sheet has been a significant and substantial concern at the company. The operating loss last year narrowed but was still a sizeable £111m. Net financing costs fell but were still £129m.

So last year saw free cash outflows move up, to almost a million pounds a day. Over a year, that is around a quarter of the company’s current market capitalisation.

Company prelim results

This month, the company announced a £1.15 billion refinancing. This consisted of debt maturing in 2029 with coupons of 10% and 10.375%. Those are costly loans.

The company also agreed new super senior revolving credit facility agreement with existing lenders, increasing their binding commitments by around £70m although for now the facility remains undrawn.

The mixture of pound and dollar denominations adds exchange rate risks. I think the high coupons speak for themselves, although the successful completion of the sizeable fundraise shows that Aston Martin continues to find buyers in the debt market.

It was only last year that the company issued new equity to help “further deleverage its balance sheet”. That approach, then, didn’t ultimately work out given that a large new raft of leverage is now being piled onto the balance sheet, bringing sizable interest obligations. Net cash interest payments fell last year but were still a painful £109m. That’s just interest, remember, not capital repayment. A back of the envelope calculation for the latest refinancing suggests it will bring additional annual interest costs of around £116m, higher than last year’s entire costs.

At the time of its prelim results at the end of last month, the company had forecast 2024 net cash interest expense of c. £110m, assuming static exchange rates, but that was before the latest fundraising announcement.

Long-Term Plan is Ambitious

The gambit here is that the company can boost sales and improve product mix such that it moves into profitability while having the necessary liquidity.

If that ever happens, it could involve yet more shareholder dilution along the way.

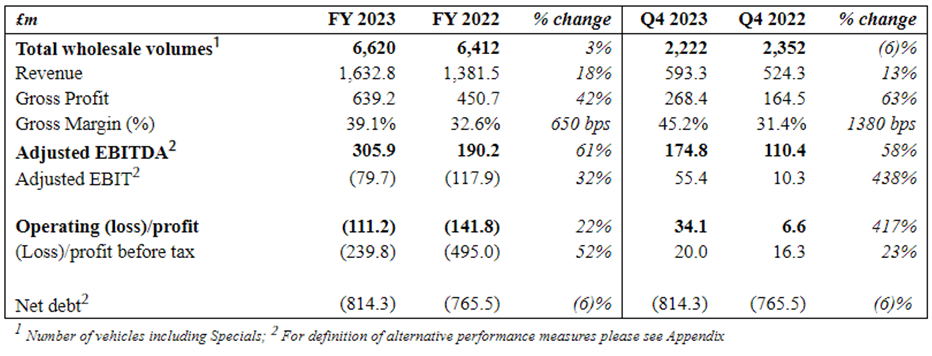

When it comes to profitability, the company is certainly moving in the right direction, although volume growth is sluggish.

Company prelim results announcement

The margin improvement and gross profit growth rate far outstripping revenue growth is significant. The company has been moving even higher end, opening a flagship store on Park Avenue last year as well as unveiling its most powerful production model ever (DBS 770 Ultimate), which sold out before production started. A new Vantage was unveiled last month. Skewing the product mix more towards very expensive vehicles is an important part of trying to achieve the sort of revenue and especially EBITDA growth the business is targeting.

The company currently maintains the following medium-term outlook for 2027-28:

|

2027-28 target |

Variance vs. 2023 |

|

|

Revenue |

c. £2.5 billion |

+53% |

|

Gross margin |

mid-40s% |

+c. 600 basis points |

|

Adjusted EBITDA |

c. £800 million |

+c. 162% |

|

Adjusted EBITDA margin |

c. 30% |

+c1,140 basis points |

|

Free cash flow: |

sustainably positive |

+£360m |

Table calculated and compiled by author using data from company prelim results announcement

Margins have been going up but I doubt product mix alone will hit that revenue growth target – likely volumes will also need to grow more strongly.

Meanwhile interest is a very real cost. From a shareholder perspective, EBITDA does not seem like a helpful metric for valuing Aston Martin. Even if it hits its medium-term EBITDA target, so what? In 2027-28, if nothing changes, it will still have both large interest costs and sizeable net debt.

Another New Chief Executive is on the Way

Last week, Aston Martin announced another new chief executive, the former chairman and chief executive of Bentley Motors.

The current chief exec has been in situ for less than two years, and the new appointment marks the fourth man at the steering wheel in as many years.

The executive chairman seems not to have found a way to work with a chief exec over the long term. That is not especially encouraging from the perspective of a private investor with no boardroom clout.

Valuation Looks Increasingly Challenging

The turnaround here is working in as far as there is sales growth and the product mix is moving in the desired direction.

But the company continues to bleed cash and its balance sheet is unattractive. It has massively diluted shareholders in the past five years and I see a risk of more dilution in future while negative free cash flows combine with high net debt.

I moved to a “hold” rating in 2022 after a string of negative pieces. I do not like the risks for equity holders implied by the latest, sizeable high-coupon fundraise and remain to be convinced that the company is on track to deliver on positive free cash flows in 2027 or 2028. Accordingly I am downgrading my rating back to “sell”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")