ArtistGNDphotography

Summary

I’m following up on my coverage on Ashtead Group (OTCPK:ASHTY), which I reiterated my buy rating as ASHTY continued to show that it finds deals in mega projects. That was a very bullish indicator of a long-term trend, in my opinion, given the nature of the projects. This post is to provide an update on my thoughts on the business and stock. I reiterate my previous buy rating for ASHTY, as I continue to be positive about ASTHY’s long-term growth potential and the magnitude of it. Recent disclosures about ASHTY winning 30% of the mega project deal flow are very positive, and while this means that margins are going to see headwind in the near term, I see this as a transitional headwind that will ease over time.

Investment thesis

2Q24 performance continues to point to positive growth traction, as ASHTY reported revenue growth of 13%, in line with consensus estimates. Underlying the 13% growth was rental revenue growth of 11% y/y in constant currency. As the US represents the majority of AHT’s business (95% of EBITDA in FY23), I will focus on the US segment. In the US, rental-only revenue was up 13%, general tool business was up 13% y/y, and specialty business was up 14% y/y, implying topline growth was driven by strength across all business units. Profitability in terms of EBITDA also performed well, with margins coming in at 47.1%, in line with guidance.

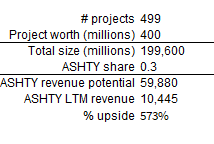

From a long-term perspective, I think the growth outlook remains very favorable for ASHTY as the deal flow for mega projects remains healthy. Management highlighted their bullishness on the construction outlook, noting a robust construction pipeline driven by onshoring and reshoring. Growth drivers for more technology-related construction, such as aviation and renewable energy, also paint a positive trend for the industry. For better context, it was mentioned that there are 499 mega projects (projects that are worth more than $400 million) that have started or are due to start by April 2024, and ASHTY has already won 30% of these deals so far. In case readers do not grasp how big this disclosure is, consider that the total deal size is worth $200 billion, and ASHTY has captured ~$60 billion worth of revenue potential. This ~$60 billion is nearly 6x the current revenue size of ASHTY. Of course, the growth will be spread out over the next couple of years or decades, but this just means that there is a long runway of growth. If ASHTY were to capture a larger portion of deals, the growth magnitude would be much higher. I would also note that my calculation assumes all projects to be worth $400 million, which is clearly not the case from a mathematical standpoint as mega projects are worth at least $400 million.

Own calculation

As we’ve indicated previously, we’ve signaled our confidence in doubling our overall market share on these projects and presently exceeding this with an estimated 30% share of the total combined projects currently underway.

As a reminder, our internal definition of a mega project is one that has a cost of $400 million and above. We’ve included all projects meeting this definition where construction is either underway or planned to start by April ’24. 2Q24 earnings results call

As for margins, I expect it to see some near-term headwinds followed by periods of continuous margin expansion. In the near term, margins should continue to see headwinds from lower utilization due to the early delivery of equipment and the early stages of mega projects. It takes time to ramp up utilization as the project progresses, so this headwind is pretty much a mix and timing issue. In terms of cadence, this utilization headwind will probably last for another year or so as management sees a 4 to 5-quarter ramp-up on mega projects. The combination of utilization recovery and improvements in supply chains should collectively drive margin expansion in 2H25. Specifically for the supply chain, recent data has proven that recovery is on track, as OEMs are now delivering equipment on time more than 95% of the time, compared to 60% two years ago.

And if we go back two years ago, let’s just say OEMs were landing, you know, less than 60% on time and quantity. Last year, they were landing more 75%, 80% on average across the full year, improving towards the end. And this year, they’ve been more 95% plus. 2Q24 earnings results call

To fund these mega projects, ASHTY would need a strong balance sheet, which it does have as of 2Q24. The company exited the quarter with ~$7 billion in net debt, which is around 1.6x net debt to EBITDA. I think the ASHTY is in a pretty comfortable position, considering that this net debt to EBITDA profile is after ASHTY CAPEX surged from $2 billion a couple of years ago to $4.5 billion over the last 12 months. Given that the megaprojects are in ramp-up mode (more construction equipment deployment), CAPEX is naturally higher. But as ASHTY progresses through these projects, CAPEX should gradually taper, which means more cash flow for ASHTY to bring down the debt level.

Valuation

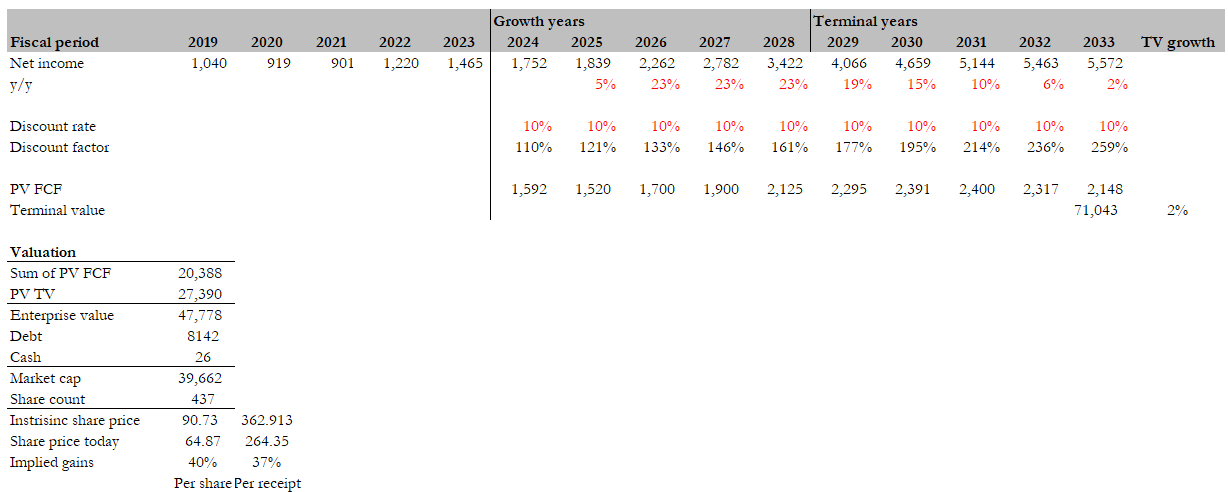

Own calculation

My target price for ASHTY based on my DCF model is $90.73. Changes to my DCF model include a downward revision of FY24 and FY25 net income as I expect margins to face headwinds from the ramp-up in mega projects (by management comments, this headwind will start to ease 4 to 5 quarters from now, which is in 2H25). That said, regarding the positive comment regarding the ASHTY share of these mega projects and revenue potential, I have increased my earnings growth expectations in the growth years to low-20% growth instead of 20%. I draw readers’ attention to the ASHTY growth years between FY12 and FY19, where net income has increased by 8x over the period, implying a CAGR of 34%. Hence, my 23% assumption is not implausible. My terminal years assumption remains the same: earnings growth will taper down to the inflation level eventually.

Risk

The ramp-up of megaprojects could take significantly longer than expected, which could continue to depress margins in the near term. Short-term investors who are not patient are likely to sell the stock and only reinvest when margins inflect upward. This means that the near-term valuation and share price could be rangebound, making it an opportunity cost for investors.

Conclusion

I reiterate my previous buy rating for ASHTY as it continues to win share in mega project deals. ASHTY’s recent disclosure of capturing 30% of projects valued at $400 million or more, totaling around $60 billion in revenue potential, indicate strong growth potential over the long-term. Despite short-term margin headwinds stemming from early project delivery and utilization issues, I see these challenges as transitional and expect them to gradually ease over time.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")