WIN-Initiative/Neleman/Stone via Getty Images

Investment thesis

In June 2021, I wrote an article about Ascent Industries (NASDAQ:ACNT), which was then named Synalloy, as operations were improving significantly after all the disruptions suffered during 2020 when the coronavirus pandemic broke the strong growth trend experienced in 2017, 2018, and 2019, and the share price still traded at 57% below mid-term highs (reached in August 2018). Despite reporting a 17.72% revenue decline year over year in Q1 2021, these sales represented a 25% increase quarter over quarter, and profit margins were recovering at a rapid pace thanks to higher volumes, product price increases, and cost-control initiatives. For these reasons, I decided to give it a buy rating.

Finally, 2021 closed with a 30.75% revenue increase year over year, and profit margins continued to improve slightly, which was accompanied by strong investor optimism. However, when it seemed that everything was returning to normal, the company began to see how inflationary pressures began to take their toll on profit margins starting in the second half of 2022, and as their negative effects intensified, demand began to weaken, which caused a new price crash of ~60% from the highs reached in H1 2022 as the gross profit margin almost entered negative territory in Q4 2022 when it was as low as 0.48%.

Since then, the management has been making various efforts to get the company back afloat, which has led to a new share price increase of ~38% from these lows to date. Efforts to optimize operations and reduce expenses continued in force and the company finally decided to close its Munhall, Pennsylvania manufacturing facility on August 31, 2023, because it had a very low margin profile. In addition, this will allow Ascent to adapt to a macroeconomic panorama marked by lower demand as high customer inventories and weakened consumer purchasing power are causing reduced volumes again.

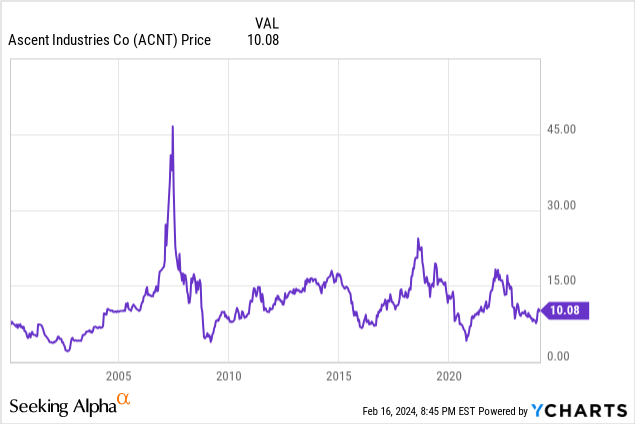

Now, the management’s objective is to buy back shares and take advantage of the low share price as it expects further operating improvements in the coming quarters, albeit at a slow pace, and the company appointed J. Bryan Kitchen as the new CEO in February 2024. Even so, the share price is still ~47.5% below the peak experienced in H1 2022, and ~59% below the peak reached in August 2018. In the previous article, I strongly recommended averaging down as the company is highly cyclical, and I still think it’s a good way to reduce risks as investors. As current headwinds appear to be temporary due to their direct link to the macroeconomic context, I consider now a good time to add shares for those investors whose average purchase price is above the current one, and also for those interested in starting a new position.

A brief overview of the company

Ascent Industries is a manufacturer of industrial welded pipe and tube products mostly made from stainless steel, duplex, and nickel alloys. It also manufactures specialty chemicals for third-party manufacturers, a rapidly expanding segment whose revenues doubled from $54 million in 2019 to $107.5 million in 2023. The company, which was founded in 1945, was formerly known as Synallow but changed its name to Ascent in August 2022, and its market cap currently stands at just ~$103 million.

Under the Tubular Products segment, which generated 74% of revenues in 2022, the company manufactures welded pipes and tubes, and under the Specialty Chemicals segment, which generated 26% of revenues in 2022, the company manufactures formulations and intermediates for manufacturers operating in a wide range of industries, including agrochemical paper, metal working, coatings, water treatment, paint, mining, oil and gas, and others.

As a consequence of the industries for which it operates, Ascent is a highly cyclical company as the share price of the last few years reflects. Furthermore, the cancellation of the dividend in 2019 discourages acquiring shares for any reason other than to eventually obtain capital appreciation. For this reason, and taking into account that it is a small-cap company, it is important to invest cautiously and take advantage of turbulent times to acquire shares at low prices.

Currently, shares are trading at $10.08, which represents a 47.5% decline from recent highs of $19.20 reached in March 2022 and a 59.35% decline from mid-term highs of $24.80 reached in August 2018. Despite the share price surge experienced in the last two months, this reflects a strong pessimism among investors as headwinds continue to negatively impact operations, and although inflationary pressures have relaxed significantly, the company was not prepared to operate in a low-volume environment as decreasing volumes caused significant margin contraction in recent quarters.

Acquisitions and divestitures

As I mentioned in the previous article, the company is in a deleveraging phase after an acquisition spree that began in 2012, and since that article, it has made another acquisition and one divestment, both focused on improving overall margins.

In this regard, the company acquired DanChem, a specialty chemicals contract manufacturing company, for $32.95 million in October 2021 to keep on with efforts to improve profitability. This caused some share dilution as the company received $10.1 million from share issuance for the acquisition. At the time of the acquisition, DanChem was generating ~$30 million of annual revenues with EBITDA margins of over 15%, which means that the acquired company is highly profitable. On the other hand, the company sold Specialty Pipe & Tube for ~$55 million in December 2023 to pay down debt and improve its margin profile, which suggests that the new CEO is giving more priority to profitability than to sales, just what the company needs at this time.

Revenues are declining again as demand is currently weak

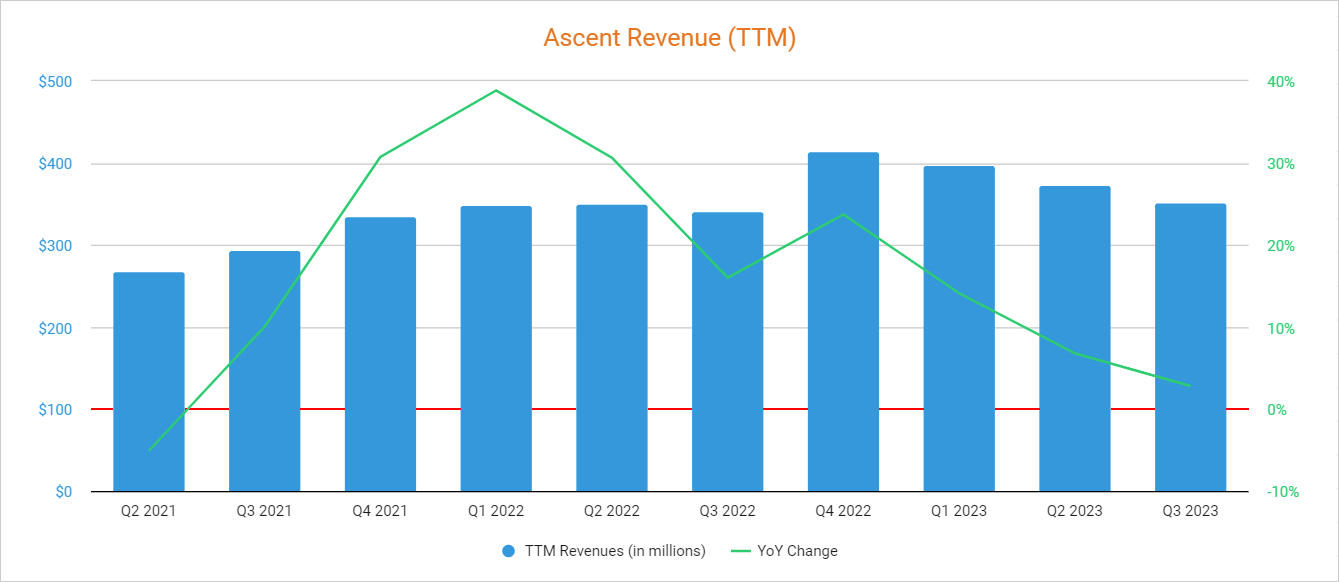

Despite the strong improvement in sales experienced in 2021 and 2022, which led the company to report record sales of $414.1 million in 2022 (36% above 2019), the company’s two operating segments have been negatively affected by current headwinds. A considerable reduction in consumers’ discretionary spending and high customer inventories have caused a significant decrease in demand at a time marked by strong competition from imported products as customers are importing cheaper products to reduce costs.

Ascent Revenue (Seeking Alpha)

In this regard, revenues decreased by 19.46% year over year in Q1 2023, by 28.29% year over year in Q2 2023, and by 28.26% year over year in Q3 2023 (and by 7.50% quarter over quarter) caused by significant volume declines in both segments. Volumes are expected to remain weak for a long time, and acquisitions are currently not a priority as stated in the Q3 2023 earnings call conference. For this reason, the recovery is expected to be rather slow, but I would expect some growth once customers manage to partially empty their inventories, which will, in my opinion, most likely start as soon as in H2 2024 as that year is expected to close with some growth (~6%) compared to 2023, excluding the impacts from the divestment of Specialty Pipe & Tube.

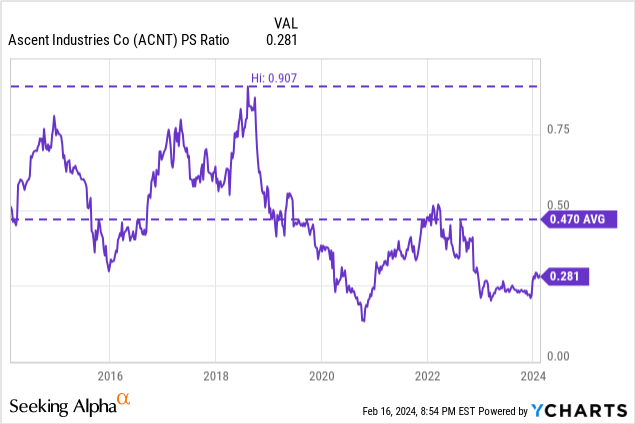

These low expectations are one of the main reasons that caused the share price decline experienced at the end of 2022 and throughout 2023, which has sent the P/S ratio to very low levels at 0.281, much lower compared to the sector median of 1.18. This means the company generates annual sales of $3.56 for each dollar held in shares by investors.

This ratio is 40.21% lower than the average of the last 10 years and represents a 69.02% decline from 10-year highs of 0.907 reached in 2018, which means that investors are giving less value to the company’s sales due to two main factors. The first, as I have already mentioned, is that growth expectations for the coming quarters are quite pessimistic, and the second is because profit margins, despite the recent improvements and ongoing efforts suggesting that they will continue increasing, are still too weak compared to what investors were used to.

In the past, investors have placed more or less value on sales based on profit margins, revenue projections, and the balance sheet’s health, exceeding the average in times of optimism and moving away from it in times of pessimism, so I think that with sales expected to start picking up in 2024, it’s a good idea to wait for recent efforts to improve profit margins, which should once again sow optimism among investors, especially once sales start to improve.

Profit margins will likely keep improving in the coming quarters

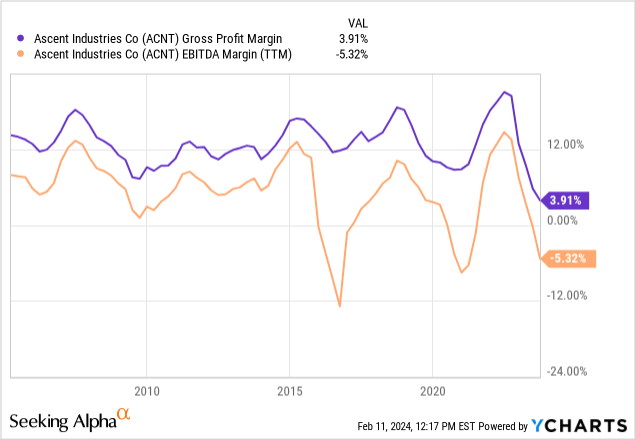

Historically, the company has suffered profitability issues during difficult times, and recent headwinds have once again caused a significant margin contraction. After a strong 2021 and H1 2022, lower volumes (as well as delays in orders for higher-margin products) and inflationary pressures have sent the gross profit and EBITDA margins to very depressed levels as the trailing twelve months’ gross profit margin currently stands at 3.91% whereas the EBITDA margin is at -5.32%.

The company reported a quarterly gross profit margin of 10.72% in Q3 2023, which despite representing a significant improvement compared to the 5.32% reported in Q2 2023, is still well below the 18.02% reported in the same quarter of 2022. Still, this improvement has been steady for three consecutive quarters from the 0.48% reported in Q4 2022.

As for the quarterly EBITDA margin, it continued to decrease to -19.08% as the company reported $2.6 million of pre-tax cash charges and $10.1 million of noncash charges related to the permanent closure of its Munhall, Pennsylvania facility so far (adjusted EBITDA was positive at $0.9 million vs. $8.2 million reported in the same quarter of 2022). The management decided to close this facility on August 31, 2023, to reduce production capacity and thus adapt to the current low-demand environment. Furthermore, this has allowed the company to cease the manufacture of galvanized products, which were expensive to manufacture and delivered low margins.

I expect EBITDA margins to keep improving in the coming quarters as the impact of weak volumes will be greatly reduced thanks to lower manufacturing capacity, and cash and noncash charges from the divestment of Munhall are one-time events. Furthermore, the recent sale of Specialty Tube & Pipe will likely help Ascent deliver higher margins, and product prices in the Specialty Chemicals segment are expected to increase throughout Q1 2024.

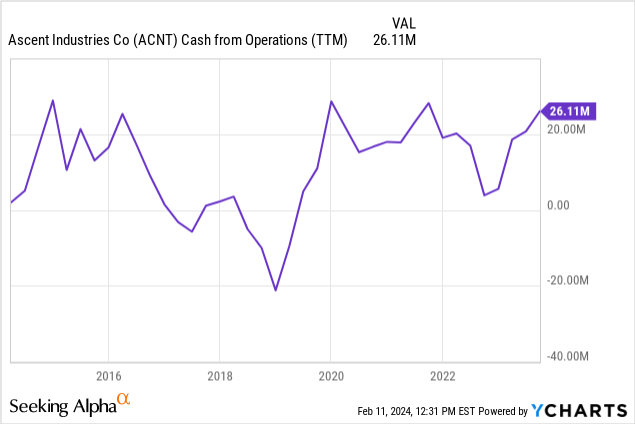

Despite this, it is important to remember that the current situation is very delicate as net income was -$17.9 million in Q3 2023 compared to a positive $0.6 million reported in Q3 2022. For now, this has not prevented the company from continuing to reduce its debt exposure as inventory destocking and the use of accounts receivable have allowed it to generate cash from operations of $26.11 million in the last 12 months.

Regarding Q3 2023, cash from operations was $3.5 million while inventories increased by $8.7 million. During the same period, accounts receivable decreased by $2.2 million while accounts payable increased by $3.6 million. While this reflects the recent strong improvement in profit margins, the company also had to cover $1.2 million of capital expenditures and $1.1 million of interest expenses.

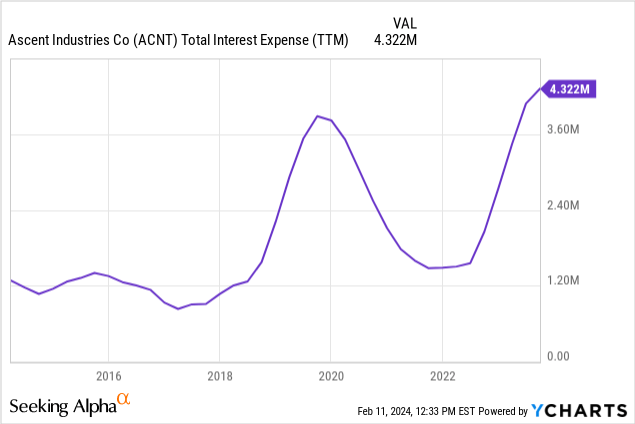

Fortunately, the recent sale of Specialty Pipe & Tube, which has not yet been reflected in the results, will provide the company with significant cash, so it should be able to significantly reduce debt in the coming quarters and, therefore, part of the interest expenses that need to be covered at the end of each period.

Interest expenses have skyrocketed, but long-term debt will likely decrease in the near term

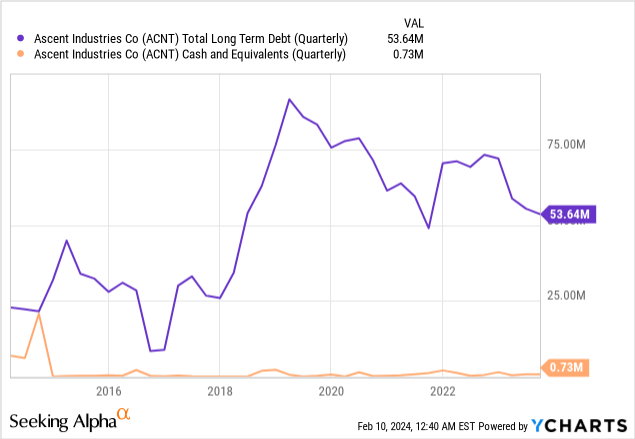

Since 2012, Ascent has gone from being debt-free to reaching $87.48 million in long-term debt in 2019 (which allowed the company to double its sales from 2010 to 2019 thanks to acquisitions). From that moment, the company canceled the dividend and acquisition-fuelled growth efforts ceased as operations were very weak in 2019 and paying down this debt load was a top priority, and long-term debt has been successfully reduced to $53.64 million.

To this, we must add that the company spent $32.6 million on the DanChem acquisition in 2021 and has not yet received the proceeds from the sale of Specialty Pipe & Tube. Once received, long-term debt should continue decreasing (if the management does not find a new acquisition opportunity), and a portion of that cash will be very useful to face current headwinds as recent margin improvements will most likely not translate into higher cash from operations in the foreseeable future as the company has already converted significant resources from the balance sheet into cash.

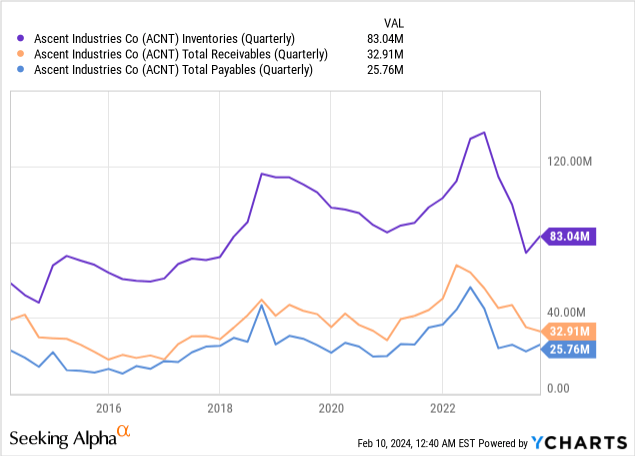

In this regard, inventories significantly decreased by $54.8 million in the last four quarters while accounts receivables decreased by $22.7 million and accounts payable increased by $3.6 million, which shows how unprofitable the company has been in 2023 as it only reported cash from operations of $26.11 million in the same period.

Luckily, the worst of the current headwinds’ impact occurred in H1 2023, so the company should not need to make such intensive use of its remaining balance sheet resources, and this is why I believe that the debt will continue to decrease in the coming quarters. This will be decisive in improving the company’s prospects as trailing twelve months’ total interest expenses have skyrocketed from $1.48 million in Q3 2022 to $4.32 million in the last 12 months.

It is for these two reasons (improving margins and the proceeds expected from the divestment) that I consider that the risk for investors has been significantly reduced in the past three quarters as the company can continue to pay down debt. Furthermore, this will also help management to continue carrying out share buybacks at low prices.

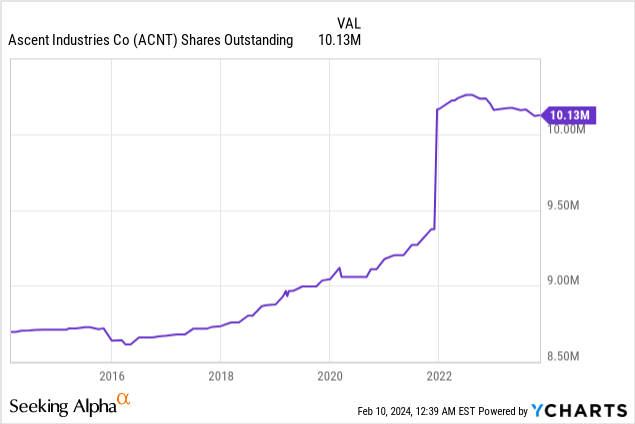

Share buybacks will likely continue

The total number of outstanding shares has been slightly reduced since H2 2022 as the management is trying to undo some of the share dilution suffered at the end of 2021 to finance part of the DanChem acquisition. Despite this, the recent decrease of 1.31% is very low compared to the entire share dilution suffered for the acquisition as the total number of shares outstanding is still 10.04% higher than before the acquisition.

Even so, efforts to reduce share dilution remain in force as the company repurchased 100,000 shares in the first three quarters of 2023, which has cost $0.7 million. In this sense, investors can expect more share repurchases in the foreseeable future as the management stated that it is a priority during the Q3 2023 earnings call conference.

Risks worth mentioning

In my opinion, Ascent Industries is a high-risk/high-reward investment because although investor pessimism is keeping the share price depressed, it is a highly cyclical company amid a restructuring process at a time marked by significant headwinds. Therefore, I would like to highlight below those risks that I believe investors should take especially into account.

- A potential recession could be triggered by recent interest rate hikes, which could have a significant impact on Ascent’s operations as a consequence of the high cyclical component of the industries for which it operates.

- The Specialty Chemicals segment is very concentrated on few customers as 67% of its revenues came from the top 15 customers, and 21% from the largest one.

- The company could suffer another contraction in profit margins if inflationary pressures intensify again.

- If operations do not continue to improve in the coming quarters, the management could decide to cease share buybacks.

- The election of a new CEO in February 2024 could change the direction that the past management was taking, which, in my opinion, is destined to offer good results in the short, medium, and long term.

- We are currently in times of high volatility, both operationally and in terms of share prices. For this reason, I strongly recommend having an averaging down approach as there is a high risk of further share price declines in the foreseeable future.

Conclusion

In my opinion, Ascent Industries is not an investment for everyone, and only investors with enough risk appetite should purchase its shares. Likewise, I consider that it should represent a small position compared to the total size of any portfolio, and it should be invested in tranches as the share price could continue to decline due to current volatility.

Although significant sales growth is not expected in the short term, everything indicates that the management is doing the right things to improve the company’s profitability. The acquisition of DanChem and the sale of Specialty Pipe & Tube should help maintain more robust margins in the long term, and the product price increases that will occur during Q1 2024 should help absorb a significant part of the recent impacts derived from inflationary tensions. Furthermore, part of the divestment proceeds will presumably go into reducing long-term debt even further, which would reduce interest expenses.

The divestment of Specialty Pipe & Tube and the closure of the Munhall facility makes me think that the priorities of the management are exactly what the company needs: focusing on profitability and not so much on revenue growth. Still, it remains to be seen if the new CEO continues on the same path, although luckily the most important changes (the recent acquisition and divestment and the closure of the Munhall facility) have already been made, so this is not something that should cause too much concern. The company has been operating for many years and the balance sheet is, in my opinion, strong enough to allow it to navigate current headwinds for a long time. Furthermore, current headwinds are, in my opinion, temporary due to all the disruptions the company has suffered due to external factors, and the recent share price decline should not be a cause for panic as, after all, Ascent is a highly cyclical company.

Considering that the P/S ratio is still 40.21% below the average of the past 10 years and that sales are expected to start increasing in 2024, I believe that investors looking for capital appreciation can achieve significant returns by waiting for the ratio to reach that average as 2024 should mark the beginning of a new growth era thanks to the company’s ability to deleverage the balance sheet in the short term. I consider this a metric that should serve as a reference as investors have historically tended to put more value than the 10-year average in times of optimism, as well as less value in times marked by headwinds such as the current ones. In this regard, I strongly believe the share price can approach the $18 mark as recent efforts materialize into improved results, the moment from which each investor must assess whether it is a good idea to sell. In my opinion, and considering the strong cyclical nature of the company, I would not wait for further price increases and I would sell once the average P/S ratio is reached, I believe that Ascent in its current form, despite having demonstrated its ability to grow sales over the years, will always be strongly influenced by the macroeconomic landscape as it operates by supplying highly cyclical manufacturers.

Q2 2024 Earnings Call Transcript")