wildpixel

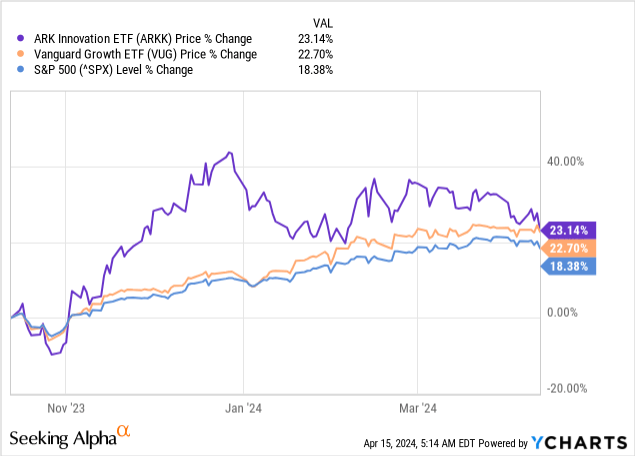

Following a disastrous performance over the past few years, ARK Innovation ETF (NYSEARCA:ARKK) seemed to be on track to recover in the months following November of last year. The momentum, however, has cooled-off rather quickly and the ETF is now very close to once again underperform the S&P 500 and other growth-oriented funds, such as The Vanguard Growth ETF (VUG).

But that’s not the main problem that ARKK shareholders are now faced with. More importantly, the ETF is extremely vulnerable to a potential market sell-off driven by the rising term premium.

The top largest holdings of ARKK could create a strong narrative around disruption & innovation, but in reality most of them are no longer benefiting from the loose monetary conditions that the market has been accustomed to in recent years. Thus, as the recent drop in the term premium is now reversing, ARKK is poised to continue to underperform.

On top of all that, is the issue with quality of ARKK’s holdings and the lack of diversification of the fund, especially during market downturns.

Turbulence Ahead

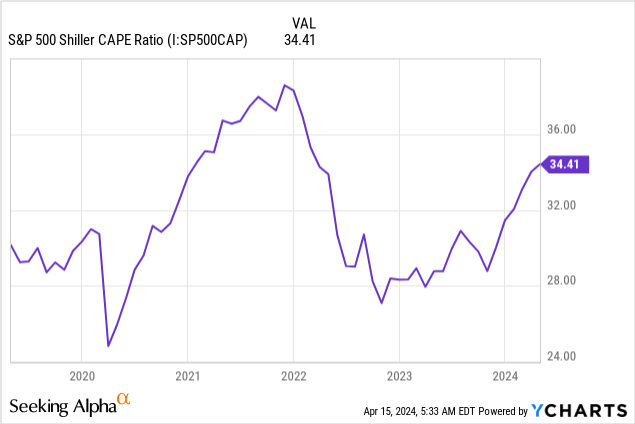

One recent market rally was almost entirely driven by multiple expansion with the S&P 500 Shiller P/E ratio skyrocketing since early November of last year. As a result, the current multiple is once again at near record levels and very far-off from the unsustainable levels of 2021 that led to the 2022 sell-off in equities.

I recently did a thought piece on another growth-oriented ETF where I explained the role of the U.S. Treasury in inducing this strong bull market in equities. I would highly recommend that you read it, if you are not familiar with the recent tailwinds for growth stocks that led to ARKK briefly outperforming the broader equity market.

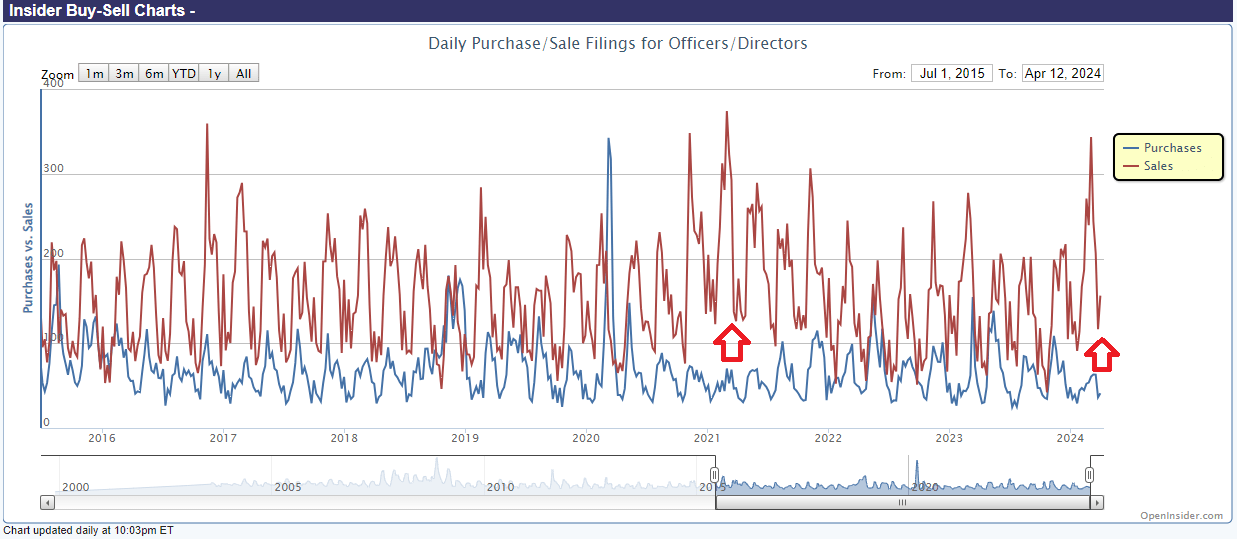

But as growth investors rejoice, the telling signs of a potential sell-off for equities are mounting. Another indication is the recent gap between insiders selling stocks (the red line in the graph below) and those who are buying (the blue line). The last time when this happened was once again in 2021.

Openinsider

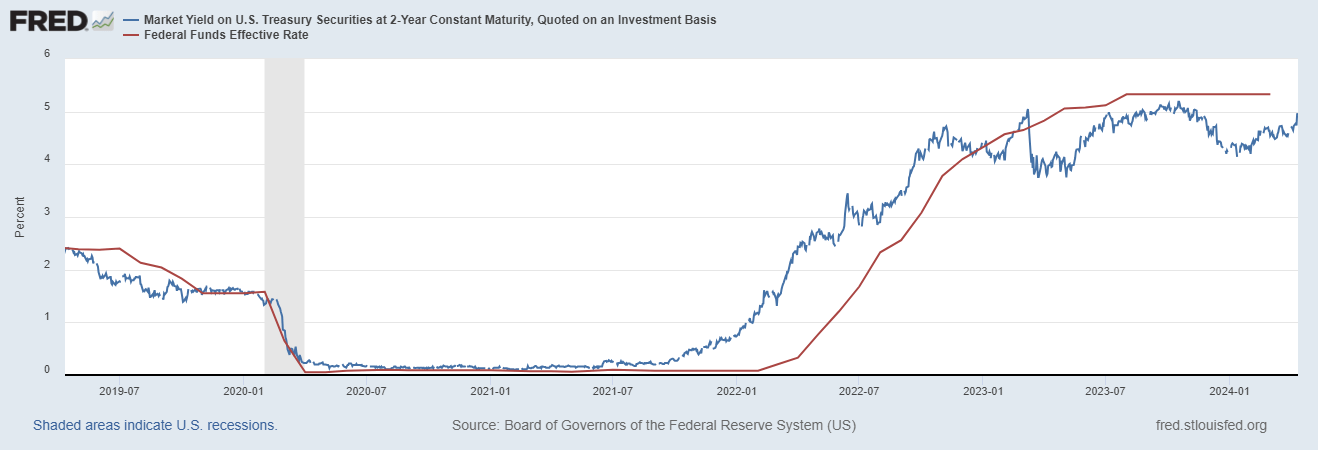

Since November of last year, market participants were also relying heavily on the assumption that the Federal Reserve’s policy would once again become accommodating for long-duration assets. That is why, the yield on the 2-year Treasuries (which is usually a telling sign of where the federal funds rate is going) has fallen sharply over the period from November of last year to early January.

FRED

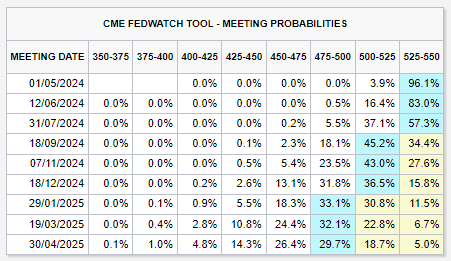

The recent Consumer Price Index release, however, has shown that investors were utterly wrong in making this assumption and the odds are now that the federal funds rate will be in the range of 5.0% to 5.25% at the end of 2024.

CME Group Website

This is in stark contrast to December of last year, when the market was pricing-in that 2024 will end in the range from 3.75% to 4.0%.

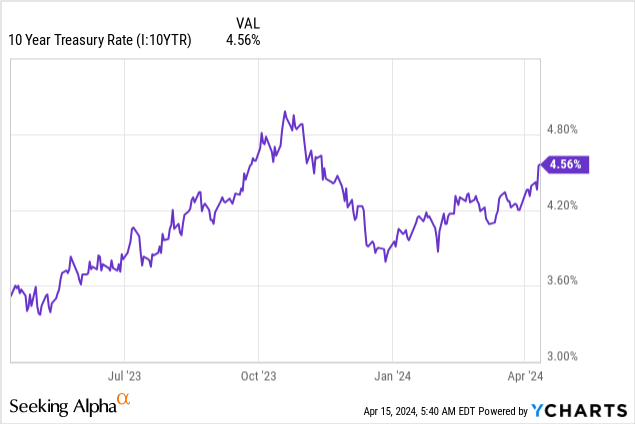

Although these are short-term rates, the term premium would also follow this course as the yield curve is finally headed to its normal state. We already see the 10-year yield headed to its prior high from October of last year, and I would not be surprised if we end 2024 above the 5% barrier.

All that would be a massive headwind for equities and long duration assets more broadly. In equities in particular, high growth and unprofitable businesses would likely be hit the worst, if the term premium increases. Unfortunately, in that regard ARKK ETF appears extremely vulnerable and prone to a major sell-off through the rest of 2024.

Low-Quality Businesses and High Correlation

The quality of a business is a subjective metric and depends on different criteria. One of the most widely-used ones, however, is profitability when also considering the relative size of a company and its future growth potential.

If a business is relatively small, then operating profitability could be only temporarily low as economies of scale are still relatively low and management prioritizes growth opportunities over profits.

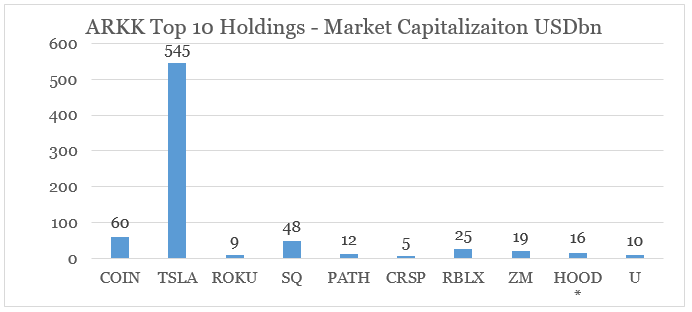

In the case of ARKK, however, all of its Top 10 holdings are multi-billion dollar businesses. The market cap numbers shown below might seem low when compared to that of Tesla (TSLA), but we should not forget that up until recently TSLA was among the top 10 largest public traded companies in the U.S. market.

prepared by the author, using data from Seeking Alpha

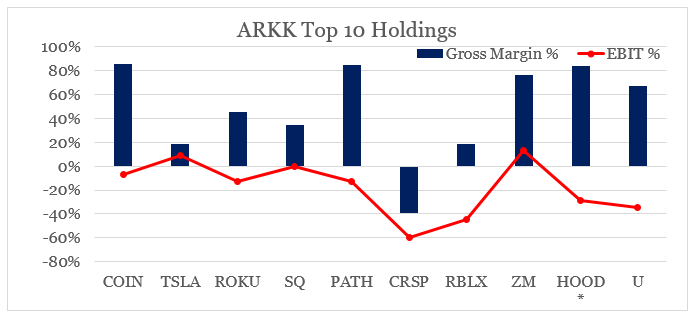

This is an issue when considering that the average gross margin of the 10 companies shown above is only 48%, while 8 out of the 10 are loss making entities on an operating margin basis.

prepared by the author, using data from Seeking Alpha

This significantly increases the duration of these stocks when compared to the mostly profitable stocks within the S&P 500 and with that they benefit heavily when the term premium is falling.

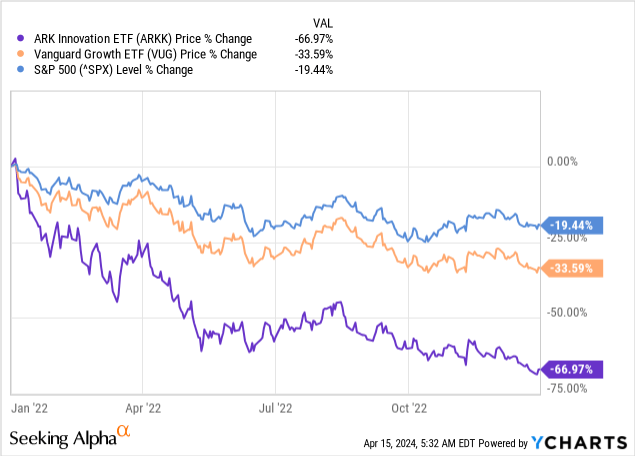

When the opposite occurs, however, they are prone to sharp sell-offs which is the reason why ARKK lost almost 70% of its value during the 2022 broader market downturn. At the same the S&P 500 fell less than 20% and even growth-oriented VUG ETF lost only 34%.

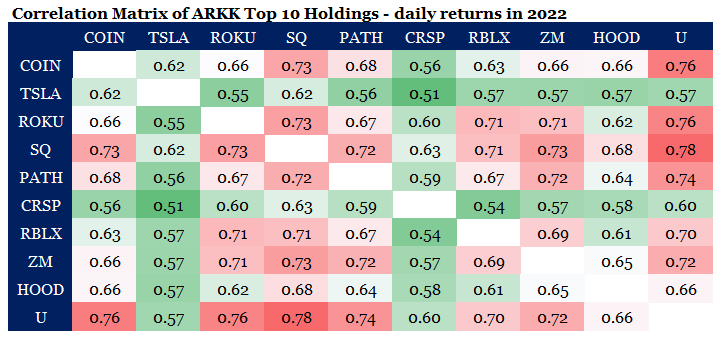

In addition to ARKK’s holdings sensitivity to the term premium and their low quality from a margin point of view, the top 10 holdings also exhibit very high correlation with each other during market downturns. The correlation matrix below shows the correlation of each holding with the rest within the ETF in 2022.

prepared by the author, using data from Seeking Alpha

The lowest correlation coefficient was 0.51, between returns of CRISPR Therapeutics AG (CRSP) and Tesla. Although it is marked in green on the table above, this is still very high and illustrates the poor diversification properties of the ETF.

Conclusion

In spite of the recent optimism and high monthly returns, ARK Innovation ETF is at significant risk of continuing to underperform not only other growth-oriented ETFs but the broader equity market as well. Higher risk and longer duration assets are now very vulnerable to a potential sell-off and with that ARKK investors are taking enormous risk. The fund’s poor performance in recent years could also explain why it is now doubling down on loss-making business on the assumption that these will benefit from a potential drop in yields. Unfortunately, this now appears a very unlikely scenario for the rest of 2024.

Q2 2024 Earnings Call Transcript")