Suchada Tansirimas/iStock via Getty Images

Arhaus (NASDAQ:ARHS) is an American high-end furniture retailer.

I wrote about the company in September 2022 and January 2023, both using a Hold rating and not recommending the stock purchase. I believe the company has good operations, is resilient, and has the potential to grow, but I wouldn’t say I liked the multiple on earnings at the time.

I believe that retailers require dense safety margins, given that small changes in sales or margins can generate large swings in profitability thanks to operational leverage.

In this review, I find that the company continues to show resilience, particularly compared to its peers. Also, some characteristics of its profitability and capital structure make it more resistant to an economic downturn.

However, I still consider the stock price too high to offer safety to the long-term shareholder. For that reason, I continue to believe that Arhaus is a Hold. Still, the company’s stock has been volatile for the past year, so opportunities might resurface. I would reconsider if the stock revisited the $7/9 range, like in June or November 2023.

Resilient ‘growth’

Despite the challenging environment for furniture retailers (higher lease and personnel costs, lower demand from new homeowners, lower discretionary spending, etc.), Arhaus has done well.

The company cites comparable revenue and demand (revenue plus change in deposits) improvements of 9% to 11% for the 9M23 period compared to FY22. Comparable means same-store for stores above 15 months open, according to the company.

However, when I aggregate the data on my own (revenues + change in deposits for the Q3’23 or 9M23 periods), I find the same range, only that looking at aggregate levels (that is, with new stores included). If Arhaus’ stores perform 10% better, while the company adds about 6% more square footage than last year, their aggregate sales levels should be higher.

Understanding the volume change is further complicated by the increase in stores (6 more stores in smaller formats leading to a 6% increase in square footage) and a falling furniture price index.

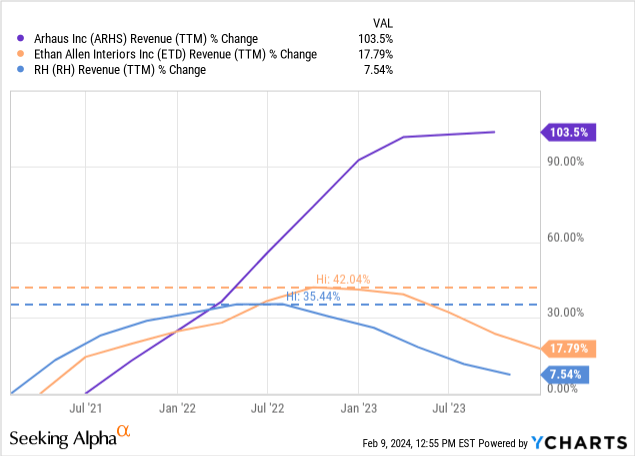

However, we can at least know that Arhaus is doing better than their competition. Ethan Allen’s and RH’s revenues peaked several quarters ago, whereas Arhaus’ are much more stable. These are the most comparable peers, given that they sell quality furniture.

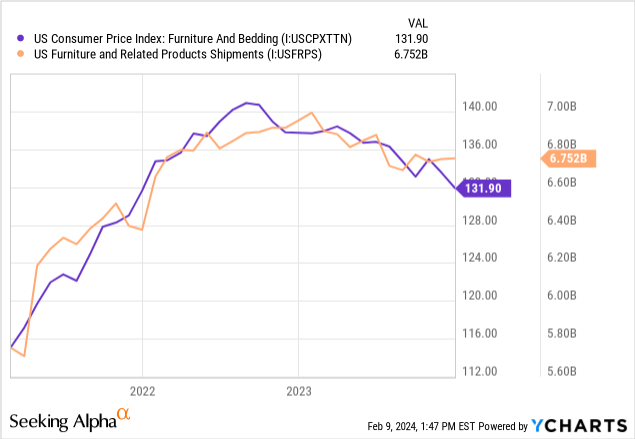

Further, the industry is deflating, as reported by the CPI for furniture and bedding. This has caused a decrease in the total sales figures for the industry as a whole.

The combined picture I get is that the industry is undergoing significant challenges, particularly on the price side, which leads to discounts while keeping volumes stagnant. In this context, Arhaus’ 10% growth, even if aided by the square footage increase, is still a good sign.

Worst case scenario

The problem with large store retailers is that they are operationally leveraged. Many of their costs are relatively fixed, their operating margins are not extremely high, and therefore, a tiny change in revenues can multiply at the profit level.

For that reason, I think that doing a worst-case scenario analysis of a retailer is interesting. The first question is how much revenues need to fall before the company generates operating losses.

For this exercise, we need to make some assumptions. One of them is that CoGS is mostly variable and that SG&A is mostly fixed. This is not entirely true.

First, about 10% of Arhaus’ CoGS is fixed store lease costs (about $70 million per year), which is not a variable component. Another portion is manufacturing facilities and warehouse costs, which are also not variable.

On the other hand, SG&A’s biggest component is personnel costs (given that even shipping to customers is considered in CoGS). Personnel is relatively fixed but can also move on the margin, for example, by reducing extra hours or seasonal workers.

Considering Arhaus’ current SG&A levels of $100 million per quarter, and gross margins of 42.5% on average for the past year, the company would require at least $950 million in revenues to cover its SG&A expenses.

That is a large reduction from the current $1.3 billion levels, 27% to be specific. However, as the figures from RH or ETD above show, a fall of 21% or 17% from the peak, respectively, is perfectly possible. Further, a fall in revenues generally goes hand in hand with more discounting to rotate inventories and, therefore, lower gross margins.

The second question is how much financial leverage and equity cushion the company has to sustain losses if they were to happen. Fortunately, Arhaus does not have financial debts, which is already an extremely important factor in resilience. Also, the company’s equity is $300 million, versus $450 million in total discounted lease liabilities. Therefore, the company could even sustain some store closures, which generate large equity losses from the reduction of ROU assets without a proportional reduction in lease liabilities, or from severances.

I’m happy in both cases that Arhaus could sustain a major setback without disappearing from Earth. Of course, if a recession happened and Arhaus’ sales collapsed, the stock would probably follow suit, but here I’m not concerned with that, but rather with the operational risk of the company running out of equity to sustain losses.

Valuation and conclusions

So far, the company is doing better than its peers, better than its industry, and is relatively well protected to weather a prolonged reduction in sales and capacity. Is it a buy, then? Well, not yet; we have to consider the price paid for the stock compared to its profitability in the future.

Unfortunately, we have to make do with not perfectly accurate models again.

The model is simple: CoGS is fully variable, and therefore gross margins are constant, and SG&A is $400 million. From the resulting operating profit, we charge 25% income taxes to arrive at net income.

Considering fixed SG&A expenses at $400 million is optimistic because the company’s current SG&A expenses are at $100 million quarterly but growing, and pessimistic because SG&A is not purely fixed.

The most sensitive parameter in the model is gross margins, again considering CoGS to be fully variable. For example, with current revenues of $1.3 billion, 40%, 42.5%, and 45%, gross margins generate $90, $114, and $145 million in net income, respectively, a sizable difference.

We could also vary revenue levels; for example, at 42.5% margins, revenues of $1.2, $1.3, or $1.4 billion generate $82, $114, or $150 million.

In reality, these figures should move proportionally so that lower revenues lead to lower margins. In that case, the range around the middle widens.

The company’s best performance TTM was generated during the third quarter of 2022, with a local maximum in gross margins (43% TTM). Operating profits came at $211 million TTM or $160 million in net income.

The company’s market cap is currently $1.6 billion, representing a 10x multiple of its best performance TTM period and a range between 10x and 20x depending on where margins and revenues go.

I would feel more comfortable with a reasonable multiple (say 10x) of the low-end earnings we calculated (say $90 million). In that case, the stock offers lower downside risk (probably some part of the recession is already playing out so that the future is brighter) and more upside potential.

I believe that the stock is pricing either significant growth ahead or a low probability of a bad macro scenario at current prices. I prefer to miss a stock that goes up than to invest in a stock that goes (permanently) down. Therefore, I will pass on Arhaus’ stock this time but will continue to monitor the name. The stock becomes more interesting at the valuations reached in June or November of 2023.

Q2 2024 Earnings Call Transcript")