D3signAllTheThings

The lithium stocks are bouncing along the bottom and the recent merger between Livent Corporation and Allkem Limited to form Arcadium Lithium plc (NYSE:ALTM) could provide an opportunity to scoop up a forgotten stock in the shuffle. The stock quickly slumped following the merger close at the start of 2024 My investment thesis remains ultra Bullish on the lithium stocks having originally covered Livent.

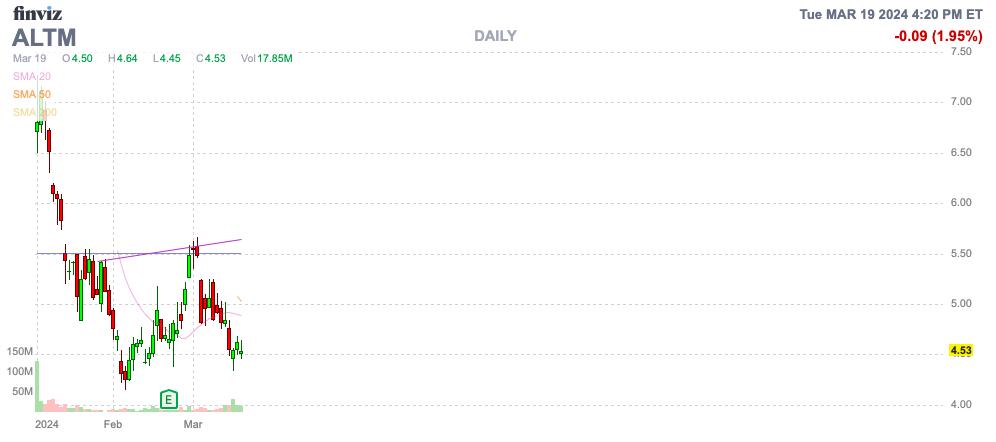

Source: Finviz

Merger Completion

Arcadium Lithium completed the merger January 4 with the reported results for 2023 only including the numbers for Livent. In a lot of similar cases, the market gets confused on the numbers listed in financials and wrongfully assigns valuations based on growth metrics from acquisitions and not organic growth.

The merger involved shareholders of both companies obtaining the following shares in Arcadium Lithium:

- Allkem shareholders received either: (a) one Arcadium Lithium ASX listed CDI; or (b) one Arcadium Lithium NYSE listed share depending where they resided and what election (if any) they had made for each Allkem ordinary share held, except for shareholders in certain ineligible jurisdictions, who will receive cash proceeds from the sale of the Arcadium Lithium CDIs in lieu of such CDIs after closing.

- Livent shareholders received 2.406 Arcadium Lithium NYSE listed ordinary shares for each Livent share held.

The combined company had pro-forma 2023 revenues of ~$1.9 billion, though the combined business only had Q4’23 sales of $324 million for an annual run rate of ~$1.3 billion.

The forecast is for the merger to realize cost saving synergies of $60 to $80 million this year on the path to $125 million in ultimate synergies. Arcadium will basically reduce overlap positions between the two legacy companies to achieve these cost reductions that appear necessary from the revenue hits alone due to lower lithium prices.

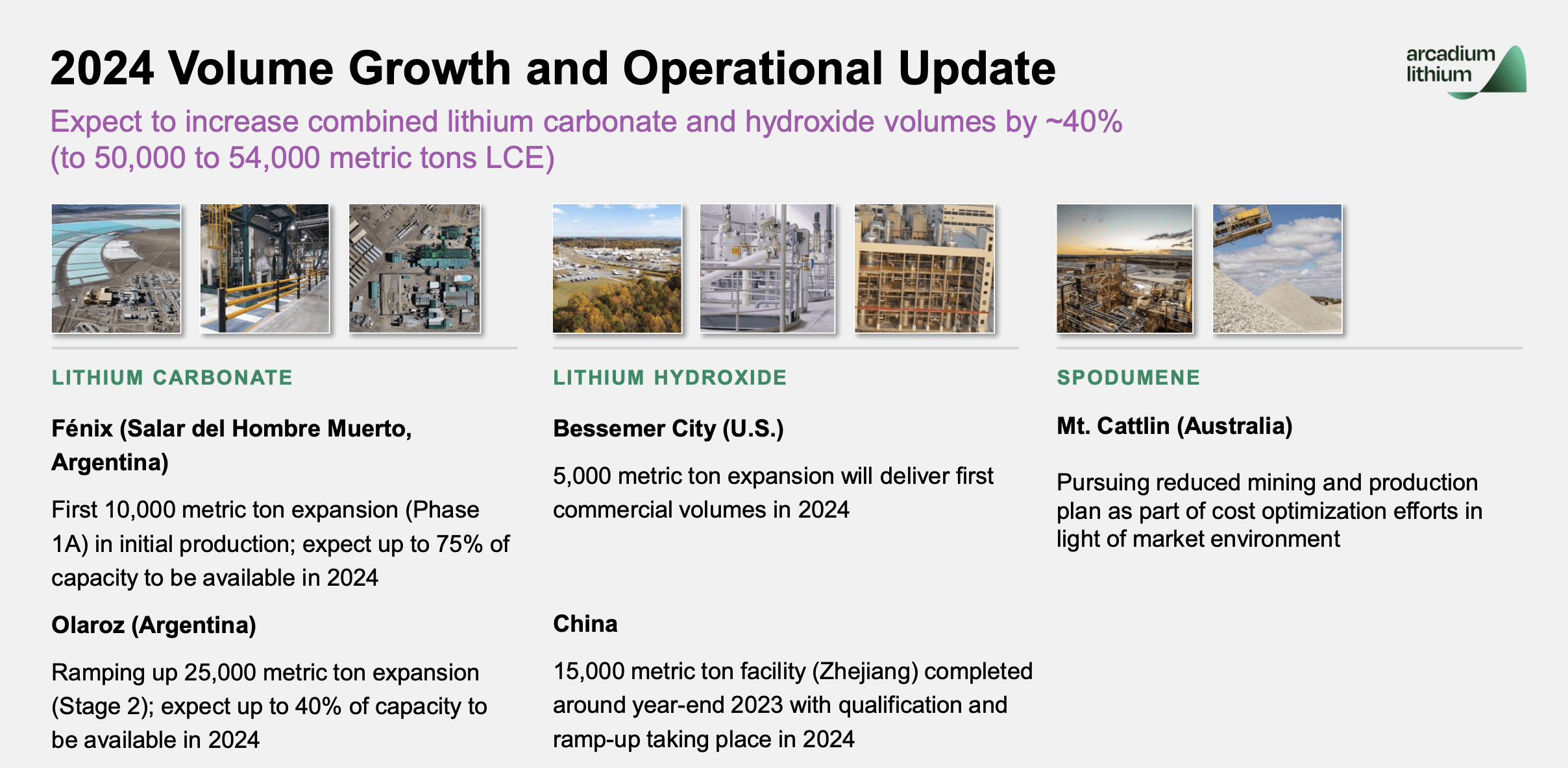

Arcadium is an interesting story due to the combined company immediately forecasted to boost lithium production by 40% annually in 2024. The forecast is for combined lithium production to reach 50,000 to 54,000 metric tons of LCE from growth at Fenix and Olaroz mines in Argentina.

Source: Arcadium Lithium Q4’23 presentation

As with the rest of the lithium market, Arcadium forecasts slowing capital spending in 2024 and beyond, as long as lithium prices remain low. In the Q4’23 earnings release, CEO Paul Graves highlighted how this market scenario is likely to boost future lithium prices similar to 2022:

“It is clear that very few lithium expansion projects make economic sense at current market prices, and the longer prices stay near these levels the greater the impact will be on future supply shortfalls. As we saw in 2022, this will increase the likelihood of a rapid increase in future lithium prices, although the complexity of the global battery supply chain makes both the timing and extent of such an increase difficult to predict.”

Arcadium will slow expansion capital spending down to $450 to $625 million in 2024 with another $100+ million for maintenance capital spending. In addition, the lithium company has run into problems with construction projects in Argentina, potentially slowing down 52K tons/year of LCE by 2027, though the company has suggested the existing projects with environmental permits already issued won’t be impacted.

Lithium ultimately will face a likely scenario where production doesn’t keep up with EV and green energy demand as prices now don’t support future mine development.

Big Upside Potential

Arcadium Lithium ended 2023 with $1.9 billion in combined sales while the stock valuation is at ~$5 billion. The new company has ~1.15 billion in outstanding shares with the stock trading at only $4.5.

Investors really shouldn’t bother focusing much on 2023 results with the real key what Arcadium Lithium is likely to produce in 2024 and beyond. The combination of the two companies and the forecasted 2024 production growth makes the investment decision focused on going forward targets, though pretty normal with any stock.

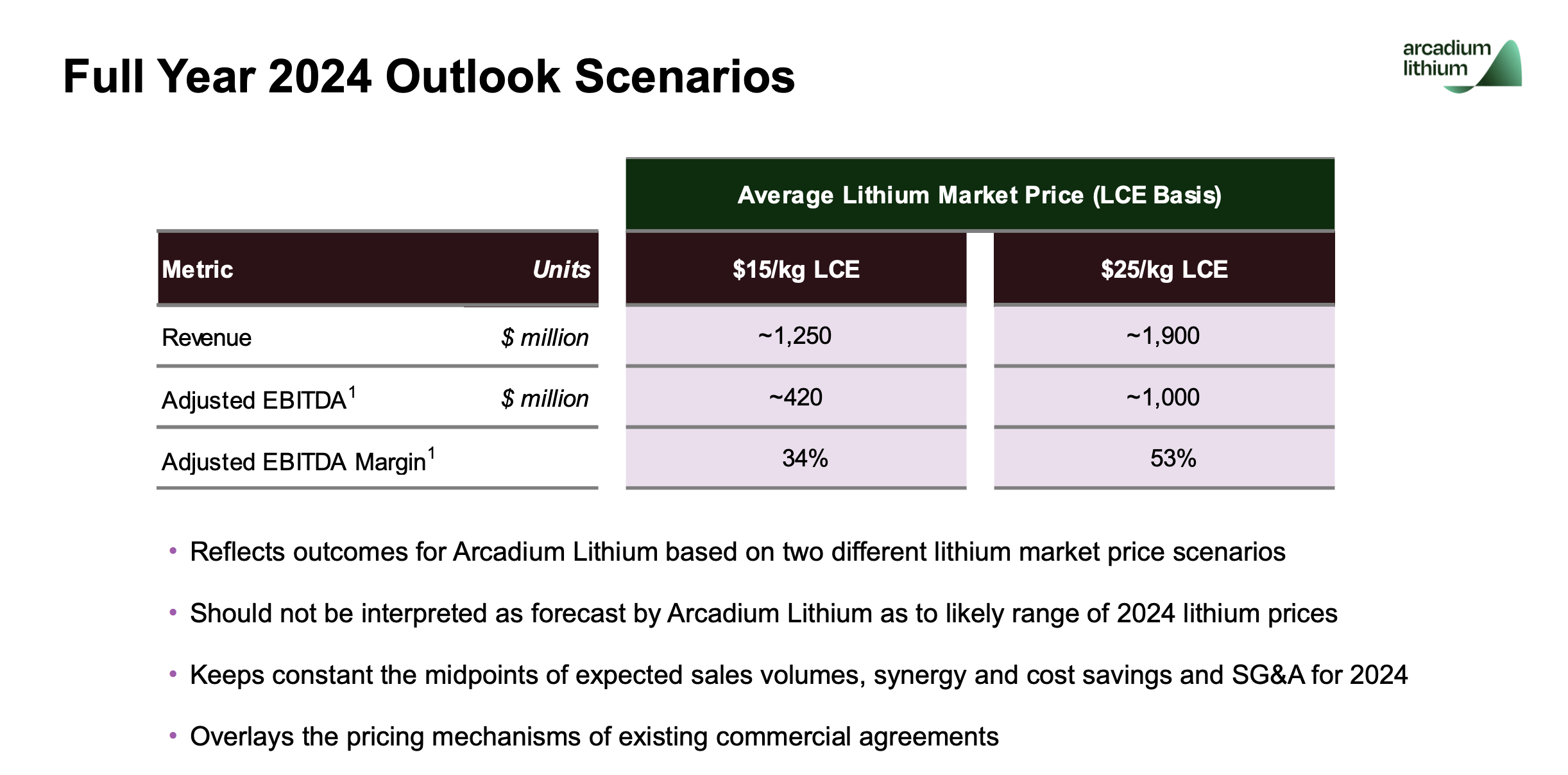

The company guided to revenues of ~$1.25 billion based on lithium prices of ~$15/kg of LCE. Remember, Arcadium Lithium would produce ~$2.8 billion worth of sales based on 2023 prices and the higher production levels in 2024.

Source: Arcadium Lithium Q4’23 presentation

Considering the ultimate massive EV demand from converting all vehicles to electrical in 2030 and beyond along with lithium mining problems, the $25/kg LCE price is a more likely scenario. Arcadium Lithium forecasts sales of ~$1.9 billion with adjusted EBITDA reaching $1.0 billion under that pricing scenario.

Remember, the company is forecasting spending $600+ million in total capex this year and adjusted EBITDA of only $420 million won’t provide the cash flows to continue spending at even the reduced 2024 levels. Arcadium Lithium would likely cut more capex in 2025 without a rebound in lithium prices.

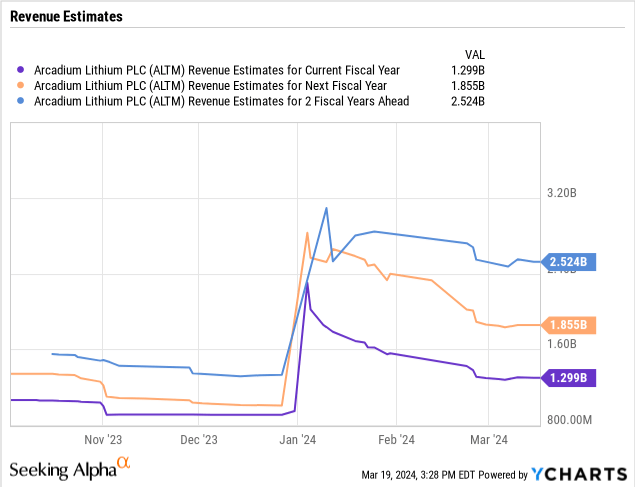

The consensus revenue estimates forecast revenue ultimately jumping up to $2.5 billion in 2026. The stock will be cheap under any scenario were revenues top just $2.0 billion and adjusted EBITDA exceeds $1.0 billion

Takeaway

The key investor takeaway is that considering the forecasted production growth and the likelihood that lithium prices spike again, an investor should assume Arcadium Lithium eventually makes a big run. Investors should use the current stock weakness to load up on Arcadium Lithium.

Q2 2024 Earnings Call Transcript")