Xsandra/E+ via Getty Images

Applied Optoelectronics (NASDAQ:AAOI) has had an impressive run, and it would seem that the market forces are in its favor to continue its growth. However, substantial risks are present for the company, which is pretty expensive.

With the sensitivity in volatility impacting so much, this stock makes us consider further the meaning and implications of risk-adjusted return and the time horizon implications.

In the article, we will review

- Applied Optoelectronics in a nutshell

- Critical trends in the industry

- Valuation and risks

In a Nutshell

Applied Optoelectronics is a leading fiber-optic networking player specializing in designing, manufacturing, and selling various products that enable high-speed data transmission through optical communication technology. (Cable Television, Data Centers, Telecommunications, Fiber-to-the-home).

In the past, many communications were made by copper wire or coaxial cables. Fiber optics allow for better transmission by transmitting light instead of electrical pulses. That is why many of the company’s offerings deal with lasers.

Fiber optics has fewer information losses and higher energy density, which means higher information transmission and more security as it is harder to intercept and immune to electromagnetic interference. Their main products focus on the following:

- Optical modules: These compact devices convert electrical signals to light and vice versa, facilitating network data transmission.

- Lasers and laser components: The company manufactures the core building blocks of its modules, including different types of lasers needed to generate the light for data transmission.

- Subassemblies and turn-key equipment: A more specialized product, it offers pre-assembled components and complete solutions for specific applications, from individual subassemblies to entire network systems.

Its primary customers are:

- Internet data centers: AOI’s high-speed modules and equipment are crucial for the massive data flow within data centers.

- Cable television and telecom equipment manufacturers build their network infrastructure on components and systems.

- Internet service providers (ISPs): ISPs utilize AOI’s solutions to deliver high-speed internet access to end users.

Key Industry Trends

The data center market is experiencing booming growth, fueled by a multitude of factors that can be broadly categorized into three main forces:

1. Data Explosion:

- Digital Transformation: Every industry, from healthcare to finance to manufacturing, increasingly relies on digital technologies, generating and storing more data than ever.

- Internet of Things (IoT): Billions of connected devices, from smart sensors to autonomous vehicles, constantly produce data that needs to be processed and stored in data centers.

- Cloud Computing: The shift towards cloud-based services, with organizations migrating their data and applications to remote servers, further amplifies the need for data center capacity.

- Big Data and Analytics: Businesses leverage vast amounts of data for decision-making, driving demand for high-performance data center infrastructure to process and analyze it efficiently.

2. Technological Advancements:

- High-Speed Networking: Emerging technologies like 400G and 800G optical networking solutions enable faster data transmission within data centers, making them more efficient and scalable.

- Artificial Intelligence and Machine Learning: These technologies revolutionize data center operations, allowing for automation, resource optimization, and improved energy efficiency.

- Edge Computing: Processing data closer to its source reduces network latency and improves responsiveness, increasing demand for smaller, distributed data centers.

3. Evolving Market Dynamics:

- Government Initiatives: Many governments actively invest in digital infrastructure projects, including data center development, to boost connectivity and economic growth.

- Sustainability Concerns: The industry is pressured to adopt greener solutions with the rise of energy-efficient data centers powered by renewable energy sources.

- Geopolitical Landscape: Data security and sovereignty concerns drive demand for data centers in specific regions or countries.

These factors together create a perfect storm for continued data center market growth. With the insatiable demand for data showing no signs of slowing down, the future of this market appears bright.

Valuation & Risks

Revenue is the most straightforward part of the valuation. The revenue will likely continue to grow between guidance and industry trends shortly. That is the company’s vital part; the growth trends are clear, and likely, the real issues are cash, profitability, and risk.

Revenue Estimates (My Charts)

For these reasons, the low to high sides of the valuation are relatively stable and show steady growth. The adjustments in gross margin and SG&A costs truly move the valuation.

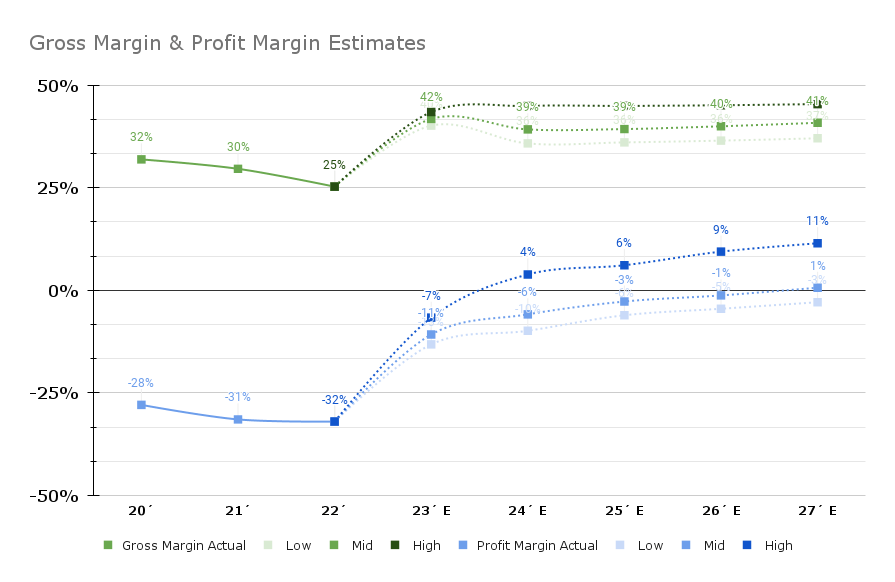

Gross and Profit Margin Estimates (Author Charts)

Gross margin is kept between 40-50% in perpetuity and improving gradually towards those goals between 2023-2027, growing fast at first and then stabilizing. While a 40% profit margin might sound like a substantial jump from the 2020 levels, most recent quarters are promising as the shift toward higher margin products like 800G, last quarter the company reached 40% gross margin, for example. The gross margin improvement is mostly driving the profit margin improvement.

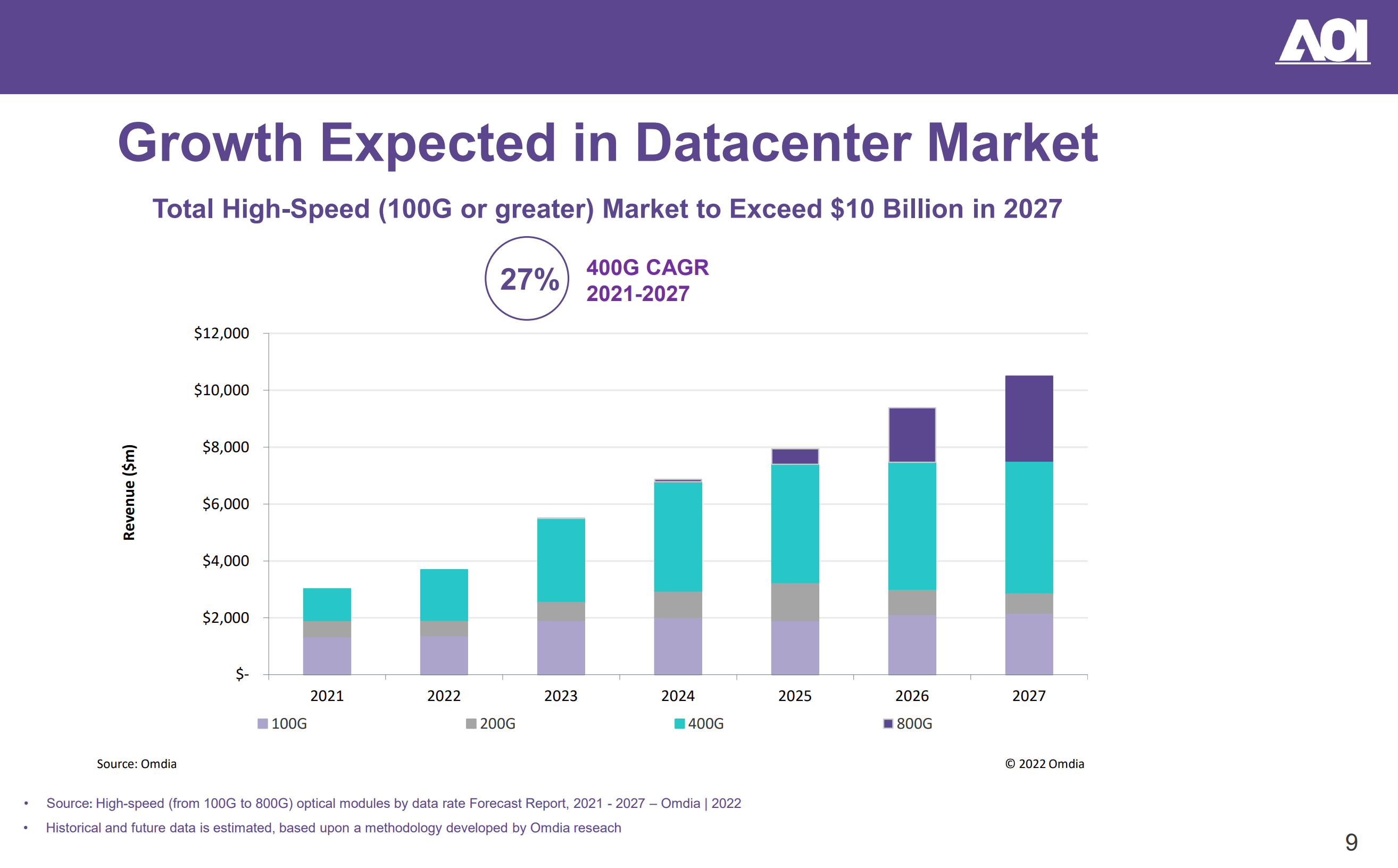

Data Center Growth Expectations (Investor Relations)

The future gross margin could be higher with a better product mix and demand. The image above shows that the company expects high revenue growth levels in its data center business. Still, more importantly, the growth comes substantially from the 800G, which has a higher margin.

However, a 40-50% gross margin is still considered in the perpetuity as it is more realistic; given the current margins and expansion expectations, it is hard to gain a larger market share and grow margin simultaneously.

EPS Estimate (Seeking Alpha)

With these margin assumptions, the company is forecasted to reach profitability in 2024 in the high range, 2027 in the mid-range, and 2030 in the low range. These projections are generally more pessimistic than Seeking Alpha estimates for 2024.

EPS Estimates (My Charts)

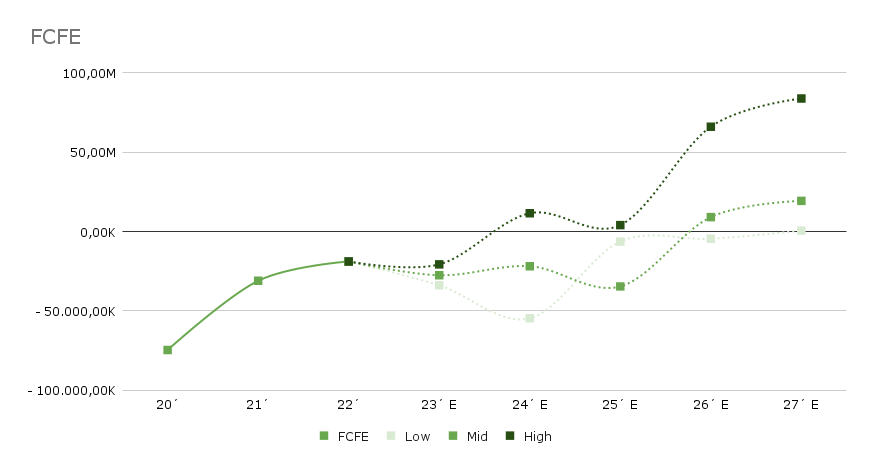

While profitability is essential, the valuation uses FCFE as a reference, which is reflected differently because of the working capital and capex required for continuous revenue expansion.

FCFE Estimate (My Charts)

For the valuation, the cost of equity depends on the Beta (the risk compared to the market), which changes this valuation substantially. While this is true in all valuations, there are substantial reasons to question the correct Beta.

The Beta used is typically based on the stock’s recent history. However, past volatility is consistent with a younger, smaller company than our current one and the one that might perform in the future. It is now closer to reaching profitability and cash-positive status, and the long-term trends pushing the fiber optics markets are closer and more robust than before, making it theoretically a less volatile situation going forward.

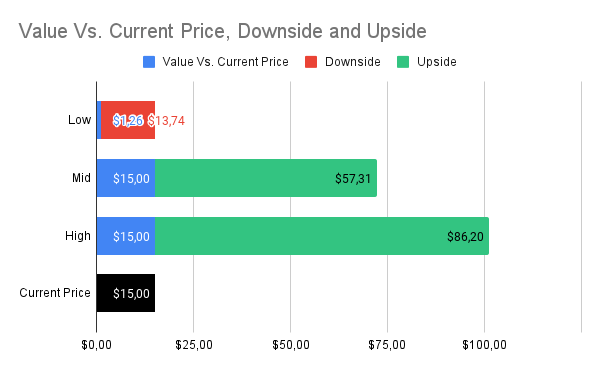

Using a five-year-monthly approach for the Beta, the company has a 2.04, while a more forward-looking approach would have a beta of 1.28. With the 2.04, the valuation range is as follows.

Fair value estimate range (2.04 Beta) (My Charts)

With this estimate, the valuation becomes extreme, with a high upside in the high scenario but steep downsides in the mid and low scenarios. While a 300% upside might sound attractive in the Gaussian distribution, the mid scenario is the most likely outcome, representing an 80%+ drawdown.

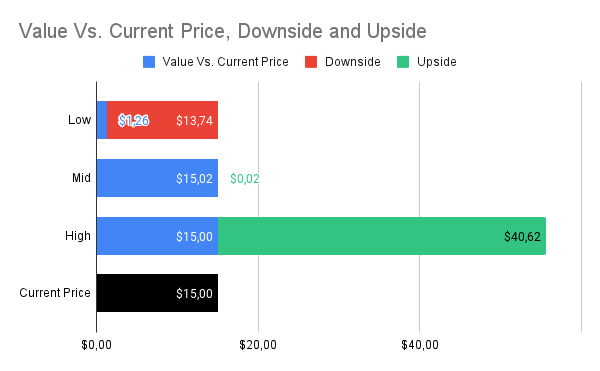

On the other hand, a 1.28 beta shows a much different perspective.

Fair Value Estimate Range (1.28 Beta) (My Charts)

With the optimistic side of the Beta, the stock becomes filled with upside and relatively low risks, which would only represent a 90% drawdown in the low scenario. The “right” Beta is likely somewhere between there, but the where is hard to point and impossible to confirm. So, instead, let us evaluate where the current market price implied Beta is.

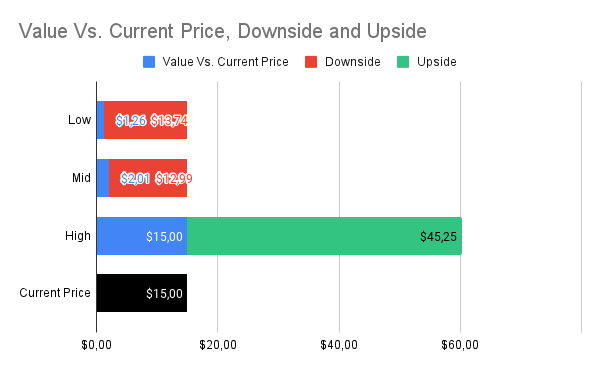

Fair Value estimates at 1,43 Beta (My Charts)

With this approach, we adjust beta so that the Mid scenario is at fair value. With this, we have a combination of market expectations and model projections. With this, we can answer two questions. What is the implied beta of the stock? What is the true risk profile that the stock offers with the model?

First, the implied beta of 1,43 seems a bit low considering its volatile margin expectations and current unprofitability, suggesting that the stock might be overvalued.

On the second front, we have a clearer picture of the risk profile, on the one hand, a 270% upside, and, on the other hand, a 90% drawdown, which is a good statistical bet, which is a fabulous profile if the model is accurate.

Conclusions

The company is an extreme play, high risk, high reward. It is small and filled with potential but is pricy and has volatile expenses and risks.

Timing is tricky for the company. The stock has been trending down for a while after a spectacular run-up. Another critical factor is that several company insiders have been dumping shares recently.

While I usually do not pay much attention to one insider selling, as it may be completely unrelated to the stock, this case might be different and substantial. The CFO sold over 10% of its stock holdings, the CEO and founder sold about half a million, and three VPs also sold shares (North America, Asia, and Legal)

Rationally, anyone should take a coin flip bet that offers to triple your money if you win, but take it all if you lose. This is because infinite repetitions of this bet would yield substantial results; however, psychologically, humans tend to value losses more than potential gains. Besides this loss aversion bias, some portfolio risks do not allow for the possibility of a steep drawdown.

The Tortoise and the Cat.

I have been making two dummy portfolios to showcase the importance of risk profile and portfolio construction in the selection of stocks. I am building Dummy portfolios of a Tortoise and a Cat to do so.

The Cat portfolio: The stock would be an excellent fit for this portfolio, as it relies on the immediacy of catalysts despite the added risk those may present. The upside is attractive enough to justify the potential drawdown. While the current insider movements are concerning, a step-by-step process of building the position and analytical tracking of the stock could be a good way to get into it.

The fear of missing out and the trends are good fits for this risk-seeking portfolio.

The Tortoise portfolio: The Tortoise portfolio would not make an allocation. While the trends are interesting and the potential is substantial, the drawdown and the volatility are too high for this point. If and when the stock stabilizes, it might be worth reconsidering. But this risk-averse portfolio would be clear of including the stock.

As for my portfolio, I will hold off on adding a position. My portfolio is already exposed to many of the critical trends that AAOI offers. The drawdown makes waiting a good option. Avoid the FOMO and eventually add a position slowly; the prospects seem solid, but the timing is not ideal, and while I have a long-term view and momentum does not play a major part, in this case, it is worth considering.

Q2 2024 Earnings Call Transcript")