RichLegg/E+ via Getty Images

Every tooth in a man’s head is more valuable than a diamond.” – Miguel de Cervantes.

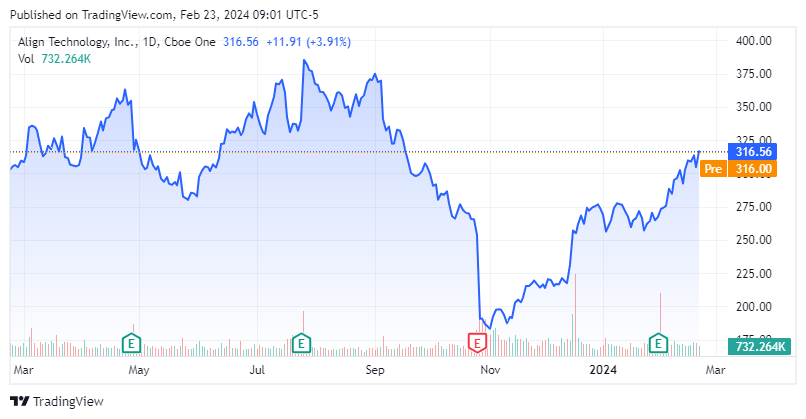

Today, we take a look at Align Technology, Inc. (NASDAQ:ALGN) for the first time since our initial article on this dentistry focused concern back in March of 2023. The shares traded around $335 and the recommendation was to avoid the shares due to valuation. The shares did slip to under $185 a share in last summer’s stock market selloff. However, recently they have rebounded to over $310 a share. Can the rise continue? An updated analysis follows below.

Seeking Alpha

Company Overview:

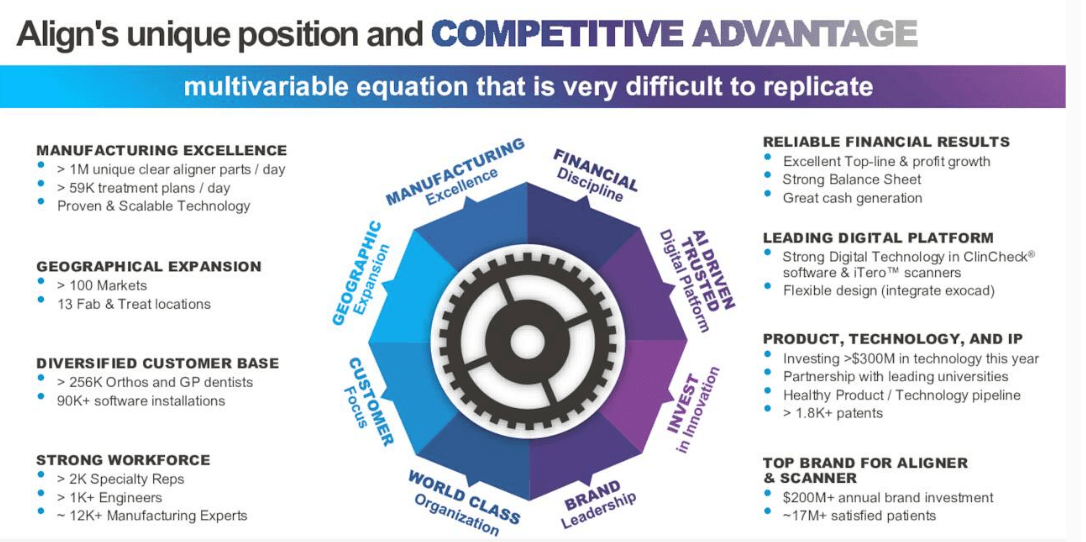

January Company Presentation

The medical device maker is headquartered in Tempe, AZ, and operates from two business segments: Clear Aligner; and Imaging Systems and CAD/CAM Services. The former is the heart of the business and provides dental products, including Invisalign comprehensive package that addresses the orthodontic needs of patients. Invisalign is an alternative to traditional metal braces. Align Technology operates both in the United States and globally. The stock currently trades just over $315.00 a share and sports an approximate market capitalization of $24 billion.

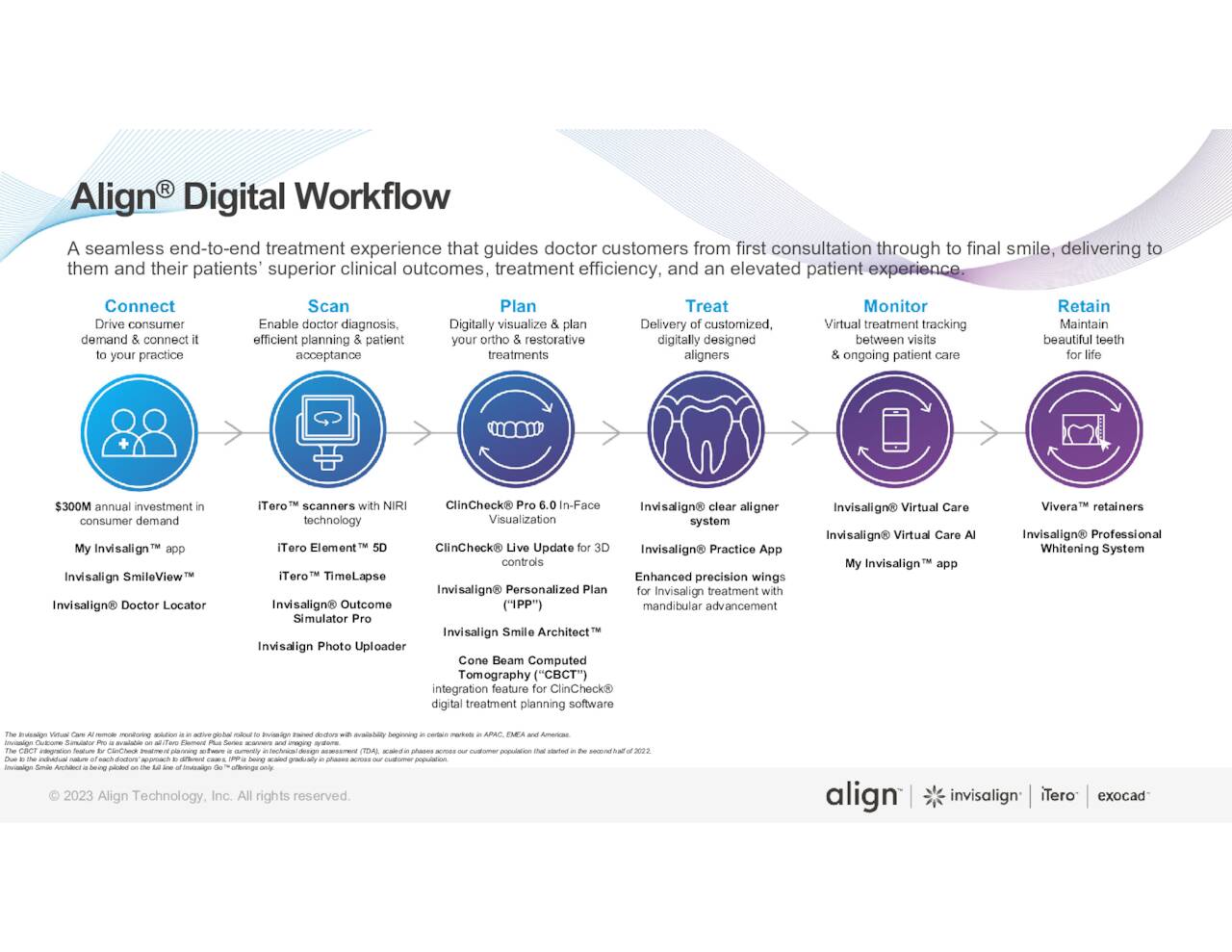

Company Presentation

Fourth Quarter Results:

Align Technology posted its Q4 numbers on January 31st. It was a solid quarter to close out the year. The company delivered non-GAAP earnings per share of $2.42, nearly a quarter a share above consensus. On a GAAP basis, the company earned $1.61 as share in the quarter. Non-GAAP operating margin was 21.4% for the quarter and 16.7% on a GAAP basis. Margins were affected to the 70bps due to foreign exchange impacts.

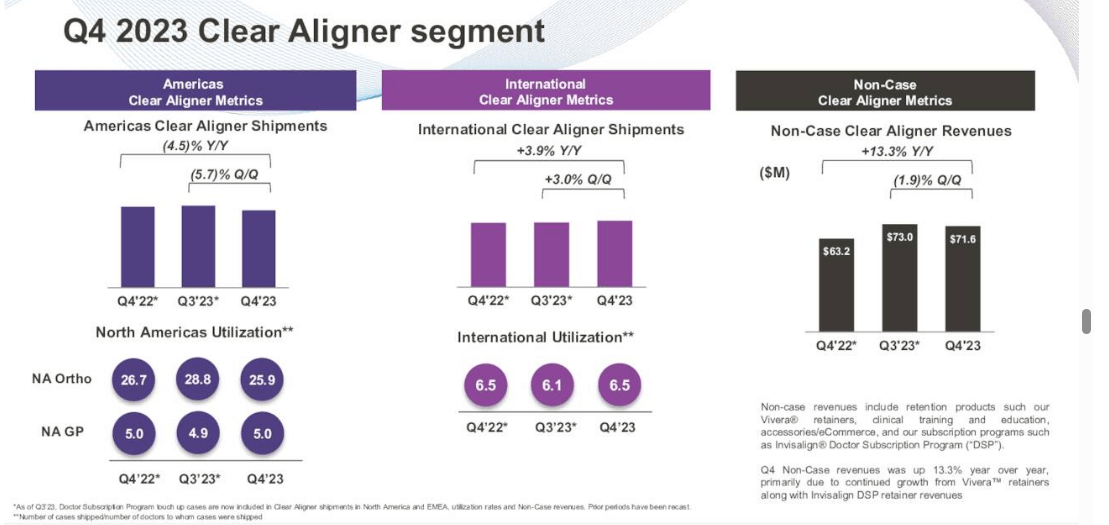

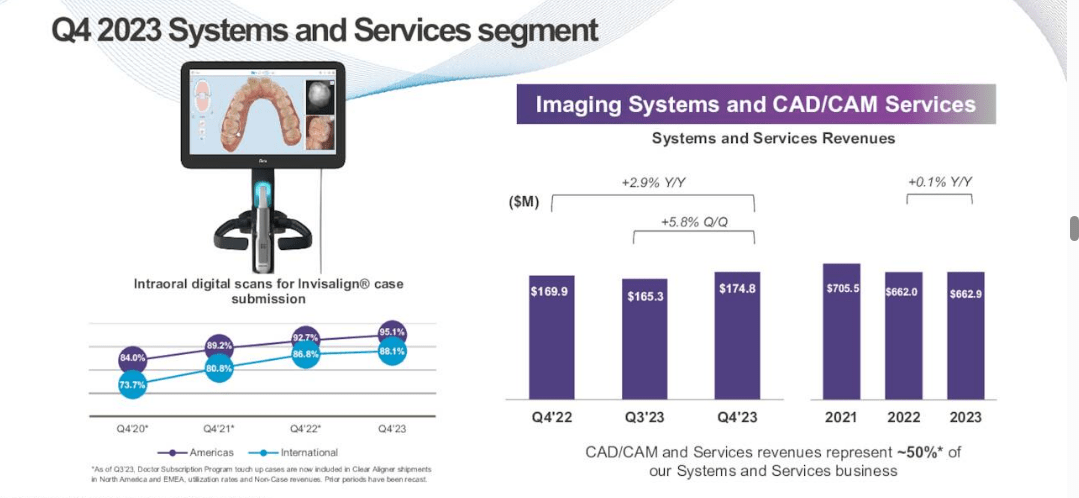

Revenues climbed a bit over six percent on a year-over-year basis to $956.7 million, more than $20 million north of expectations. $3.2 billion of overall sales came from the Clear Aligner business.

January Company Presentation January Company Presentation

Management gave initial FY2024 guidance, projecting mid-single digit growth in revenues in the new fiscal year. Leadership expects margins to be slightly above that of FY2023. It also projected capital expenditures to be right at $100 million as the company continues to build out manufacturing capacity.

Analyst Commentary & Balance Sheet:

Since fourth quarter results posted, five analyst firms including Evercore ISI and Piper Sandler have reiterated Buy/Outperform ratings on the stock. Surprisingly, three of these contained slight downward price target revisions. Price targets proffered range from $325 to $340 a share. Both Goldman Sachs ($225 price target) and Bank of America ($215 price target) maintained Sell ratings on the equity.

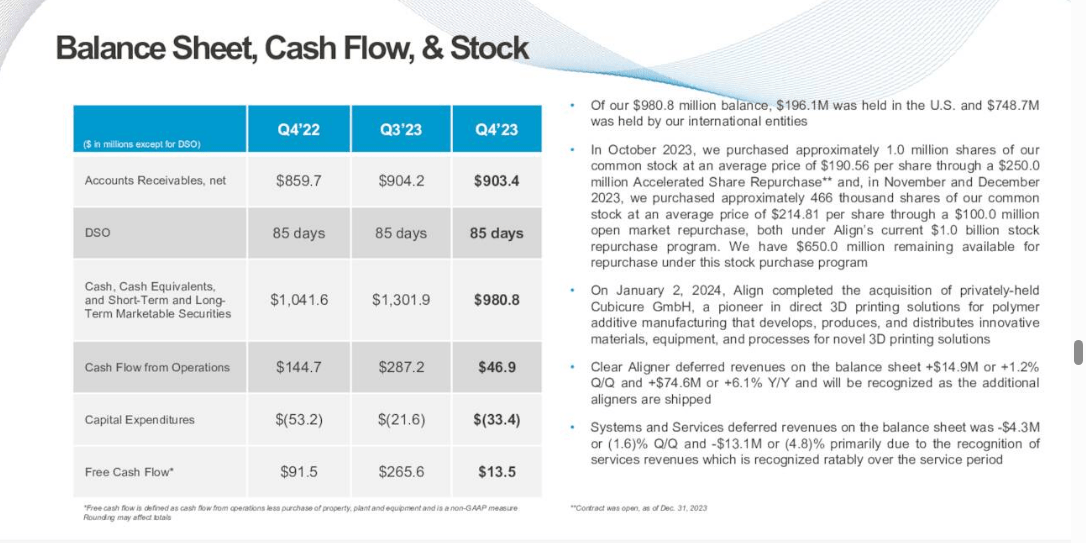

Just over two percent of the outstanding float in this stock is currently held short. The CEO bought nearly $2 million worth of shares in late October and early November of last year at under $200 a share during the stock market pullback. Another insider has sold just over $700,000 worth of equity. Align Technology exited its fiscal 2023 year with just over $1.04 billion in cash and marketable securities on its balance sheet. Align lists no long-term debt. The company also repurchased $600 million worth of stock in 2023.

January Company Presentation

Verdict:

Align Technology, Inc. made $8.61 a share in FY2023 on $3.86 billion in sales. The current analyst firm consensus is for profits to rise to $9.28 a share in FY2024 as revenues clock in at $4.04 billion. The project earnings moving to $10.50 a share in FY2025 on nearly 10% sales growth.

The company appears to be executing well. The challenge for an investor is all around ALGN valuation. The stock sells for nearly 35 times forward earnings and six times forward sales. This seems quite steep for a firm that should deliver eight percent earnings growth on a five percent rise in sales in FY2024 and pays no dividend. With Align Technology, Inc. shares approaching bullish analyst price targets, the recommendation is to stay on the sidelines with this name and hope another dip buying opportunity comes around again in 2024 like in October of last year.

Blessed are they who hold lively conversations with the helplessly mute, for they shall be called dentists.”― Ann Landers.

Q2 2024 Earnings Call Transcript")