BeyondImages

Since the last time I wrote about the multi-commodity miner Anglo American (OTCQX:AAUKF) (OTCQX:NGLOY) in early July, its price has declined by 7.8%. Year-to-date [YTD] it has declined even more, by 31%. Considering that the commodity cycle is weak end right now, the softening in price is hardly surprising.

At the same time, Anglo American had overcorrected compared to both its past market multiples and those for the materials sector the last time I checked. This raises the question as to why the price continued to fall. Here, I explore the answer to exactly this question and also what’s next for it.

Price Chart (Source: Seeking Alpha)

Why’s the price still falling?

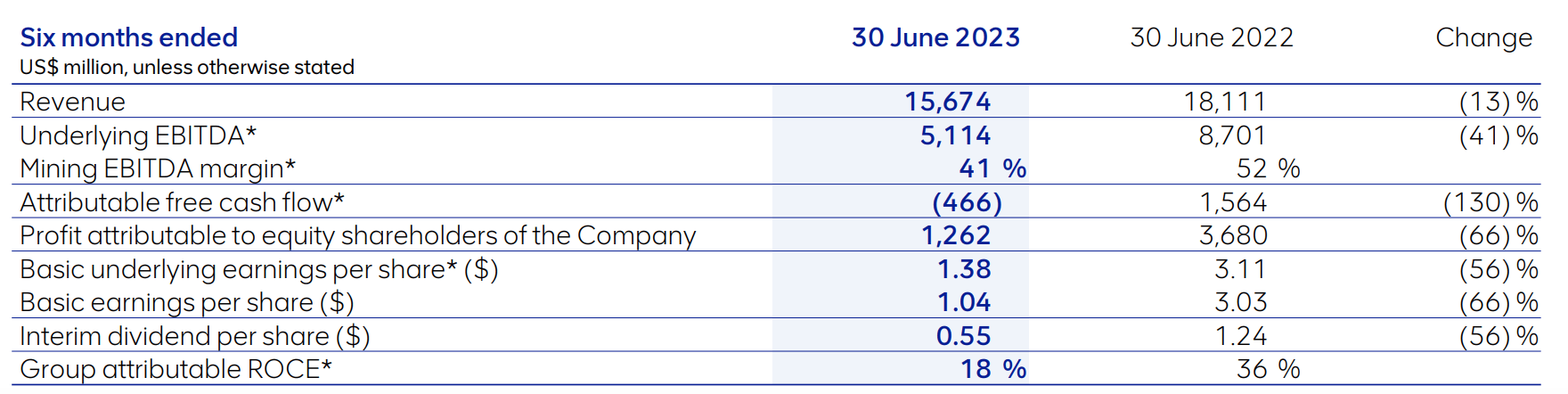

Since I last wrote, Anglo American released its financial update for the first half of 2023 (H1 2023), which was worse than expected and the company also cut dividends. The miner saw a 13% YoY decline in revenues and a huge 66% fall in attributable profit.

Key Financials (Source: Anglo American)

As a result, its trailing twelve months [TTM] diluted earnings per share [EPS] has more than halved to USD 1.71 from USD 3.68 for the full year 2022. This in turn has inflated the TTM GAAP price-to-earnings (P/E) ratio to 16x, which is almost the same as the average of 16.1x for the materials sector.

In contrast, when I last checked on Anglo American, the P/E was at 8.1x, significantly lower than the 13.75x for the materials sector. It’s now double the levels just a few months ago, and also higher than its own five-year average at the time of 10.3x.

Some recent improvements in metal prices

However, some recent developments in metal prices indicate that the softening in financial performance can be checked. In July, there was already a possibility of an uptick in metal prices on support from China’s government to buoy the economy. This has indeed played out. IMF’s metal price index saw a decline of 6.9% year-on-year (YoY) in Q1 2023 and 6.3% in Q2 2023. By comparison, in Q3 2023, it has actually risen by 6.7%.

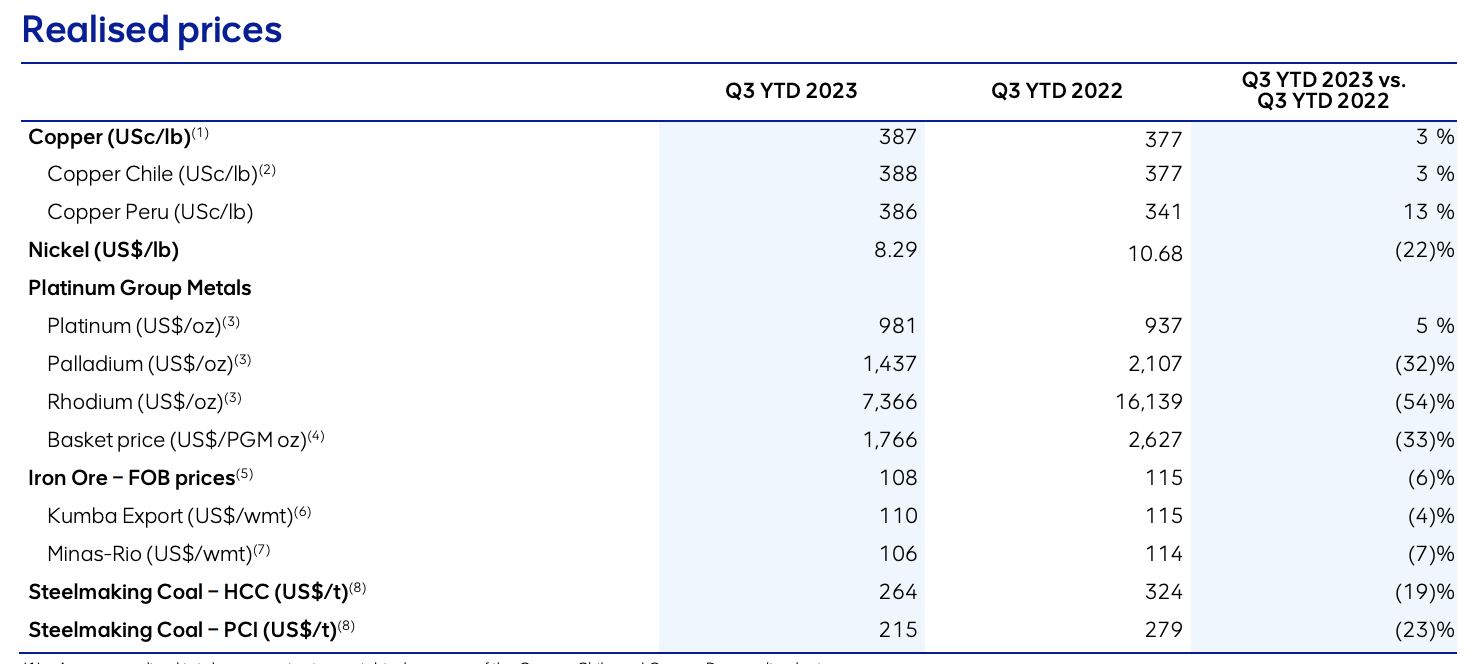

In line with this, Anglo American, too, has seen some improvement in realised prices’ trends in Q3 2023. This is most visible for copper, which is significant, considering that it’s the second biggest contributor to both revenues and earnings, with a share of 22% share in revenue and 39.9% in underlying earnings. Copper price is up by 3% YoY in Q3 2023 (see table below), compared to a 2% decline in H1 2023.

Source: Anglo American

Iron ore trends have improved too, but not quite as much. Prices have still declined by 6% but by a much smaller percentage compared to the 22% fall in H1 2023. Iron ore is the biggest revenue generator for Anglo American with a 23.4% share in H1 2023 and a 57.1% share in earnings.

However, there’s less to say for the company’s other two big earning generators, platinum group metals [PGMs] and coal. While PGMs too have seen a slowing down in price decline, it’s not a significant decline. And coal price decline has accelerated. With iron ore and copper accounting for a bulk of the earnings, it’s possible though that the extent of decline can be checked, even though there are factors weighing profits down.

Outlook for financials in 2023 and 2024

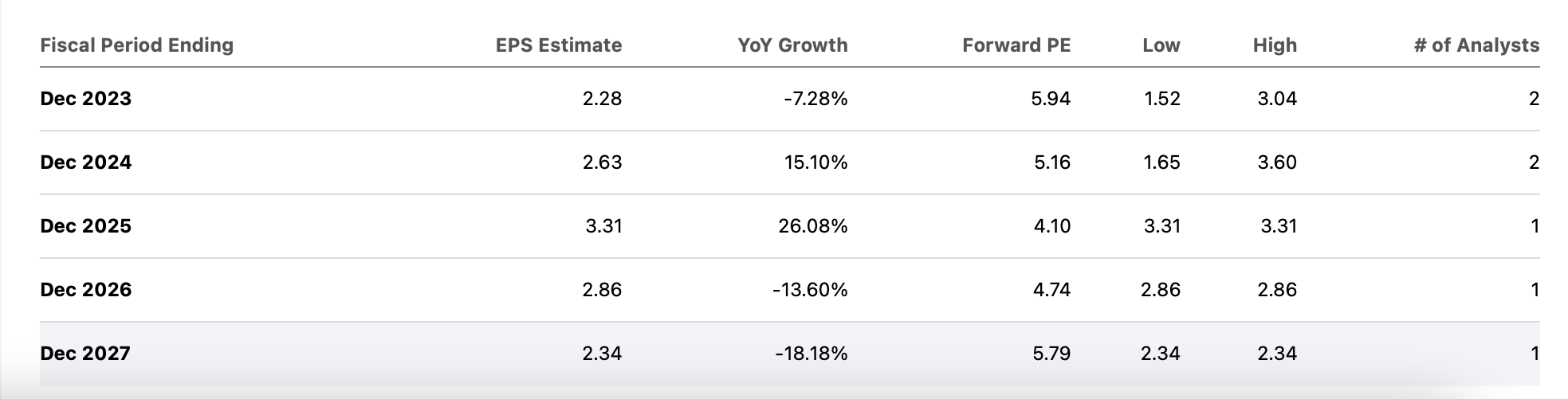

Analysts too, are more optimistic about the full-year numbers. Even though estimates for the expected decline in 2023 revenues are now at 8.8% from the 1.3% when I last checked, they do reflect that the extent of softening would likely be lesser in H2 2023. Further, the EPS decline is seen at 7.3% compared to a 56% fall so far in the year. Moreover, next year, an uptick is expected in EPS in 2024 (see table below).

EPS Estimates (Source: Seeking Alpha)

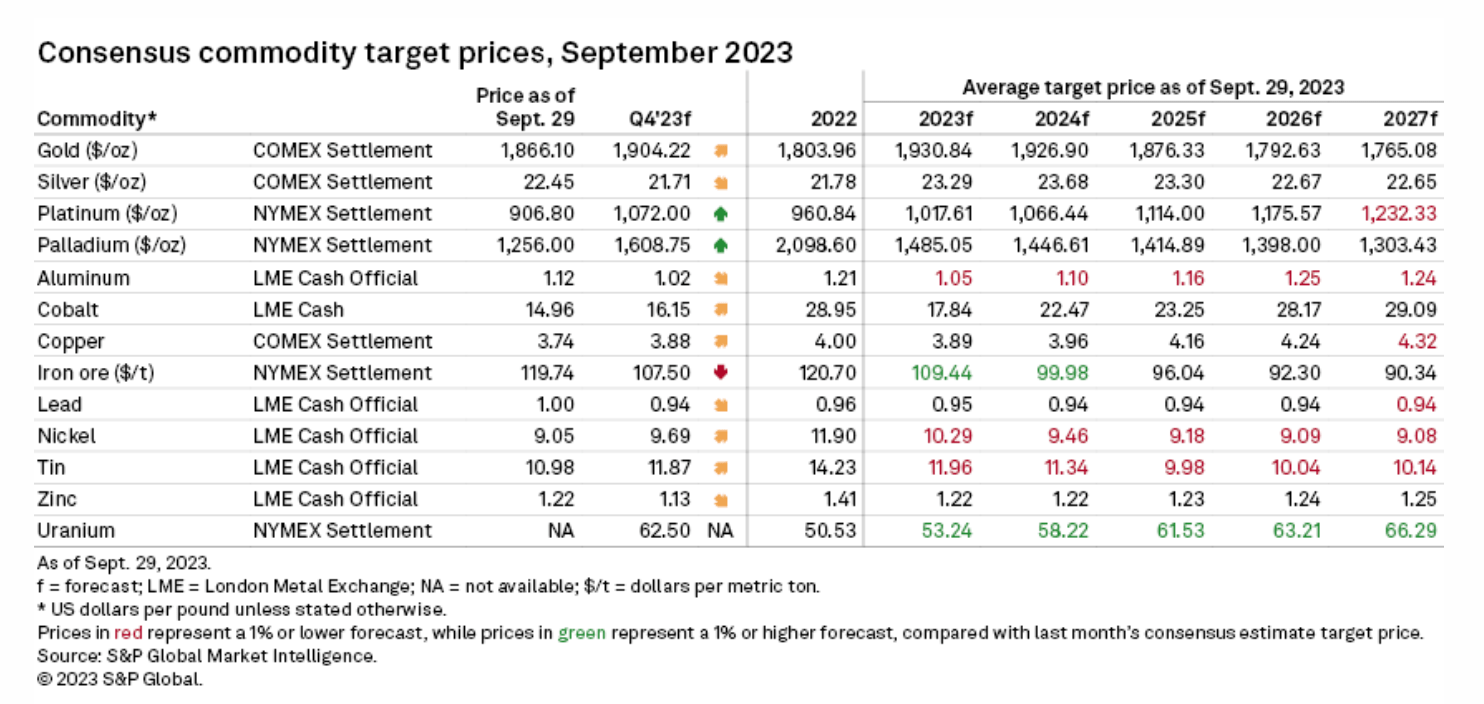

The outlook for metal prices is mixed so far for 2024 (see table below). While metals like copper and platinum are expected to see some increase, iron ore is still seen softening further. So it’s not as if there aren’t risks to the outlook, but going by the low base of 2023, there’s also room for improvement.

Source: S&P Global

The forward dividend yield

Anglo American’s current dividend yield at 4.8% is already significantly higher than the average level of 2.3% for the materials sector, and only a shade lower than its own five-year average of 4.9%. It has declined from the 6.7% the last time I checked, but it still looks alright.

Further, my estimates of the forward dividend yields look even better. With a 40% payout policy, an expected decline in earnings also indicates another dividend cut for next year, to be sure. At the same time, with analysts’ EPS estimate of USD 2.28 for 2023, the forward yield is at 6.7% for 2024.

Attractive forward multiples

Also, the forward GAAP P/E has now fallen to 6.2x from the 7.1x it was at the last time I checked. This is also far more attractive than the 15.7x levels for the materials sector. With the TTM P/E reflecting that the stock is fairly valued, the forward P/E actually shows an upside now.

What next?

The outlook for Anglo American is far more mixed since I last wrote about it. Its most recent numbers, for H1 2023, have been expectedly weak on softening commodity prices. Smaller earnings have inflated the TTM P/E ratio to levels that indicate it’s fairly valued compared to the sector now, compared to its far more attractive valuations until even a few months ago.

However, there has been some improvement in metal prices recently on China’s stimulus measures. This is, in particular, positive for Anglo American’s copper segment, where realised prices have inched up a bit in Q3 2023. Iron ore prices are also declining far more slowly than earlier.

While both revenue and earnings are expected to soften in 2023, going by analysts’ outlook, it appears that H2 2023 could still be much better for the company. In 2024, it’s expected to see an earnings uptick again. Even with weaker earnings for now though, both its forward dividend yield and forward P/E ratio are competitive compared to the sector.

On balance though, I do think that the risks can’t be ignored right now, in light of the fact that Anglo American has missed earnings estimates recently and the outlook for metal prices is still grey. I do think that it’s still a good long-term buy as an established multi-commodity miner, but for now, it’s better to wait until its TTM P/E looks more compelling or its next results show signs of improvement. I’m downgrading it to a Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")