travelif/iStock via Getty Images

June 18th was a rather painful day for shareholders of America’s Car-Mart, Inc. (NASDAQ:CRMT). Shares of the company collapsed, dropping at one point around 8%. This came in response to management reporting financial results for the final quarter of the 2024 fiscal year. Even though revenue exceeded forecasts, earnings per share fell significantly short of what analysts anticipated.

As a whole, revenue and cash flows for the company look disappointing, even though there has been some margin improvement from a gross profit perspective. Given these factors, as well as how shares are currently priced, I would make the case that the company deserves yet another downgrade.

This is unfortunate. I say this because, back in January 2023, I downgraded the stock from a “buy” to a “hold.” This was because, even though sales had been growing nicely at that point, bottom-line results were suffering.

Fast-forward to today, and that trend has definitely turned mixed. There has been some positive data. But a reduction in revenue, combined with cash flow issues, makes the company more difficult to get behind than it was previously. Because of this, I believe that downgrading the firm to a “sell” to reflect my view that shares will almost certainly continue to underperform the broader market is the right move.

A tough time

Author – SEC EDGAR Data

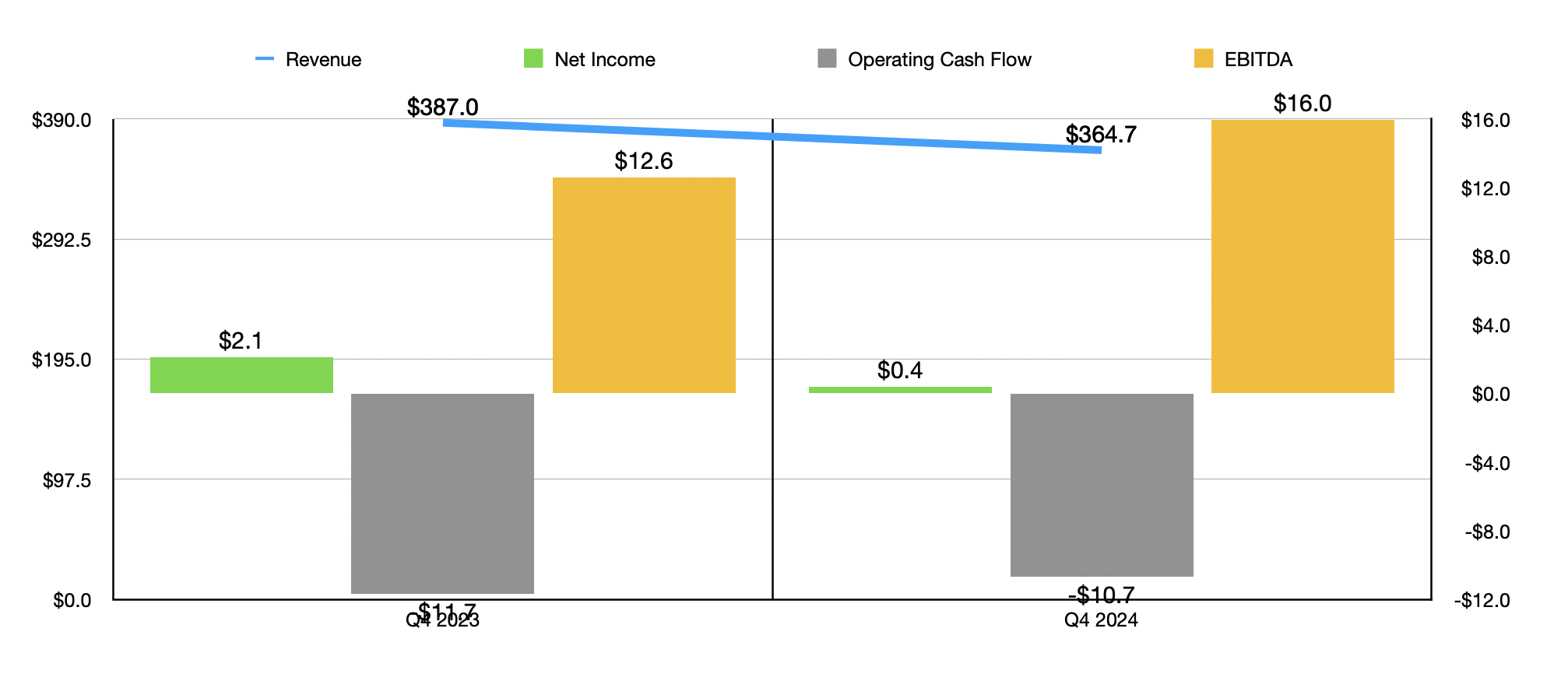

Before the market opened on June 18th, the management team at America’s Car-Mart announced financial results covering the final quarter of the company’s 2024 fiscal year. Revenue for that quarter came in at $364.7 million. While this is $3.3 million above what analysts anticipated, it actually represents a decline of 5.8% compared to the $387 million generated just one year earlier. This drop was really only attributable to a 13.6% decline in the number of vehicles the company sold.

Author – SEC EDGAR Data

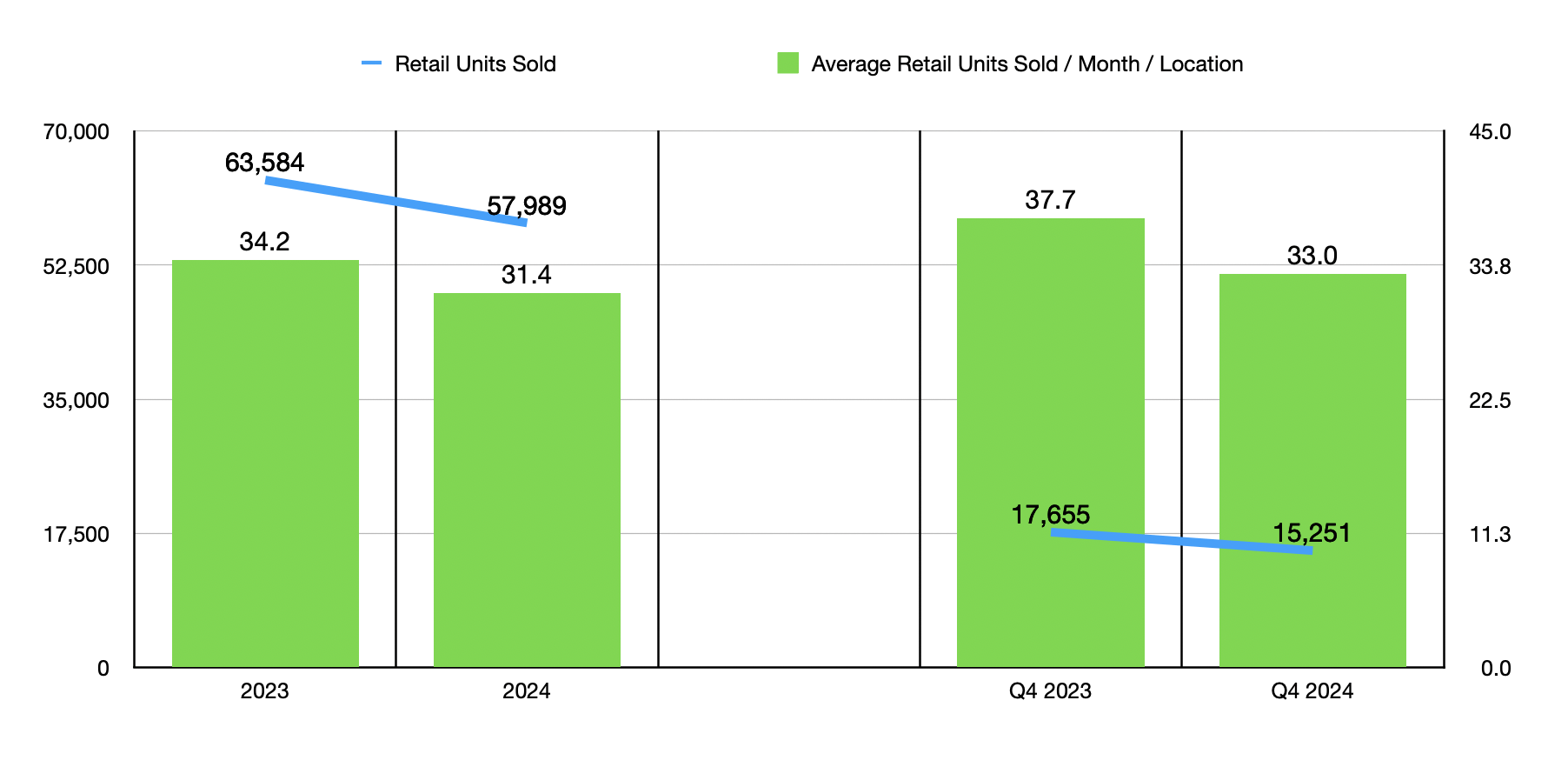

The firm, which has built its business around selling used vehicles to consumers with limited financial resources, reported the sale of only 15,251 vehicles in the final quarter of 2024. That’s a drop from the 17,655 reported one year earlier. Part of this drop can be attributed to a decrease in the number of stores from 156 to 154. But most of it is just because of reduced buying activity at its locations. In fact, the number of units sold per location per month fell 12.5% from 37.7 to 33.

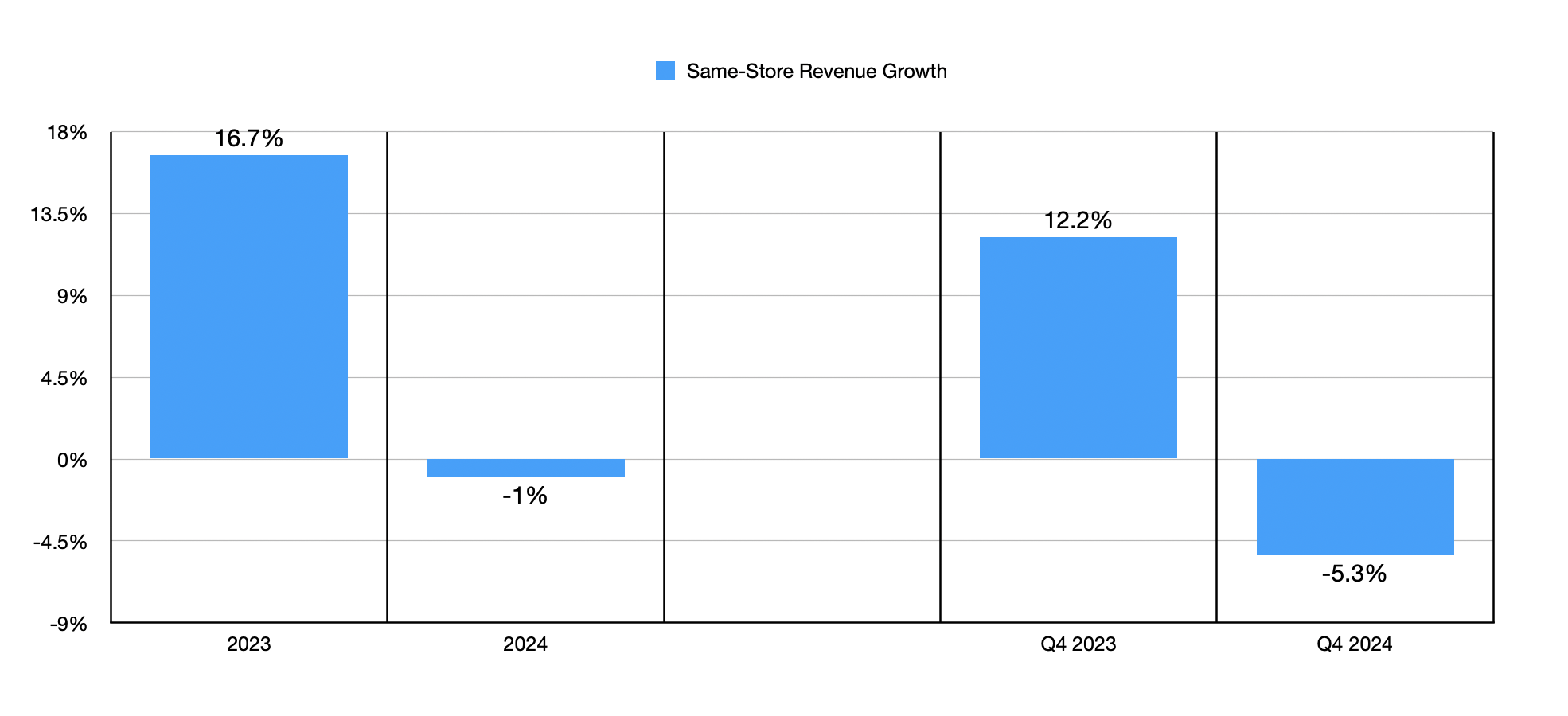

Same store revenue for the company actually took a hit of 5.3%. By comparison, in the final quarter of 2023, same store revenue for the business jumped 12.2% on a year-over-year basis. The picture would have been worse had it not been for the fact that management was able to sell its vehicles at a higher price this year than last year. The average retail price in the final quarter of this year was $19,256. That’s comfortably above the $18,133 reported last year.

Author – SEC EDGAR Data

From a margin perspective, the company did see some improvement. But that was extremely isolated. The average gross profit per unit sold rose from $6,354 in the final quarter of last year to $7,132 the same time this year. This translated to an increase in the gross profit margin per unit from 35.0% to 37.0%.

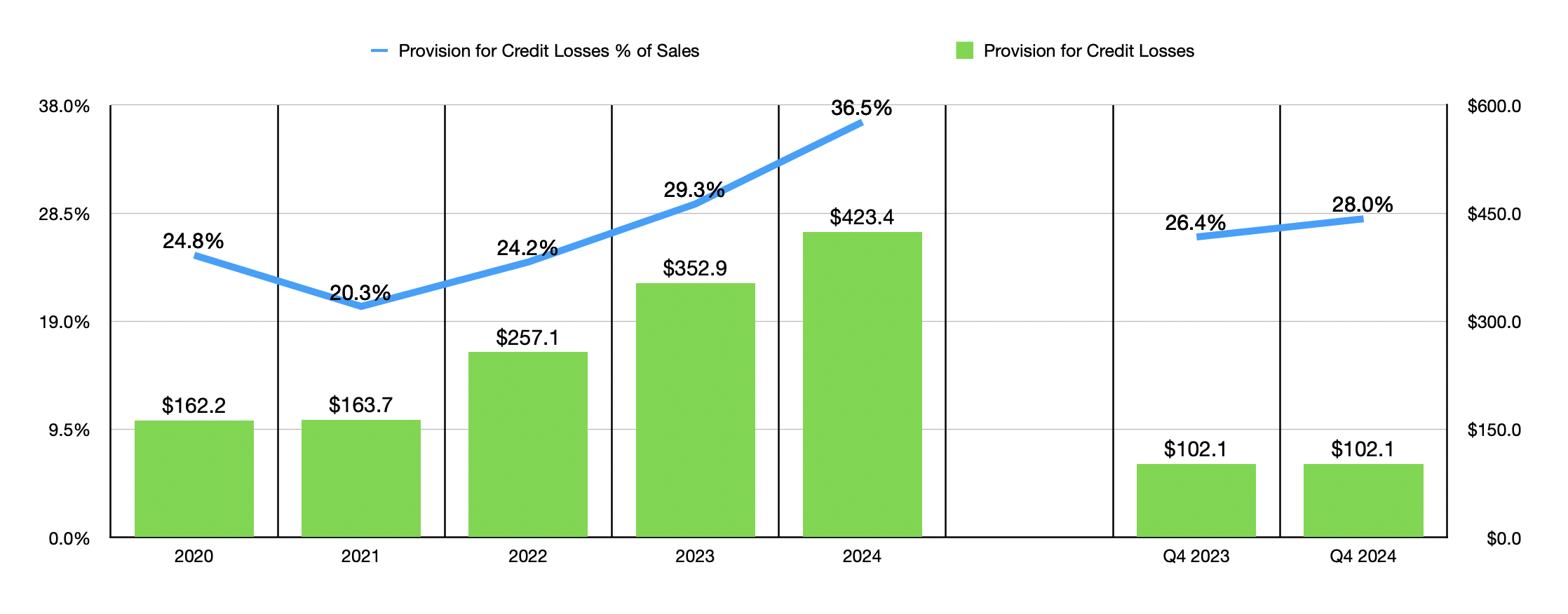

As great as this was to see, the company’s bottom line actually took a hit, with net income falling from $2.1 million to only $0.4 million. There were a couple of drivers behind this bottom-line pain. For starters, the provision for credit losses for the company increased from 26.4% of sales to 28%. Using the revenue generated in the final quarter of last year, that’s an extra $5.8 million in pre-tax costs that investors would have seen this year compared to last year. In addition to this, interest expense managed to grow from $12.9 million to $17.8 million. Given the environment we are in, this is not shocking in the least bit.

On a per-share basis, earnings came in at only $0.06. In addition to being substantially lower than the $0.32 per share generated at the same time one year earlier, the earnings figure reported by management was $0.14 per share lower than what analysts were hoping for. Other profitability metrics for the company came in better than this. Operating cash flow went from negative $11.7 million to negative $10.7 million. Meanwhile, EBITDA for the business expanded from $12.6 million to $16 million.

Author – SEC EDGAR Data

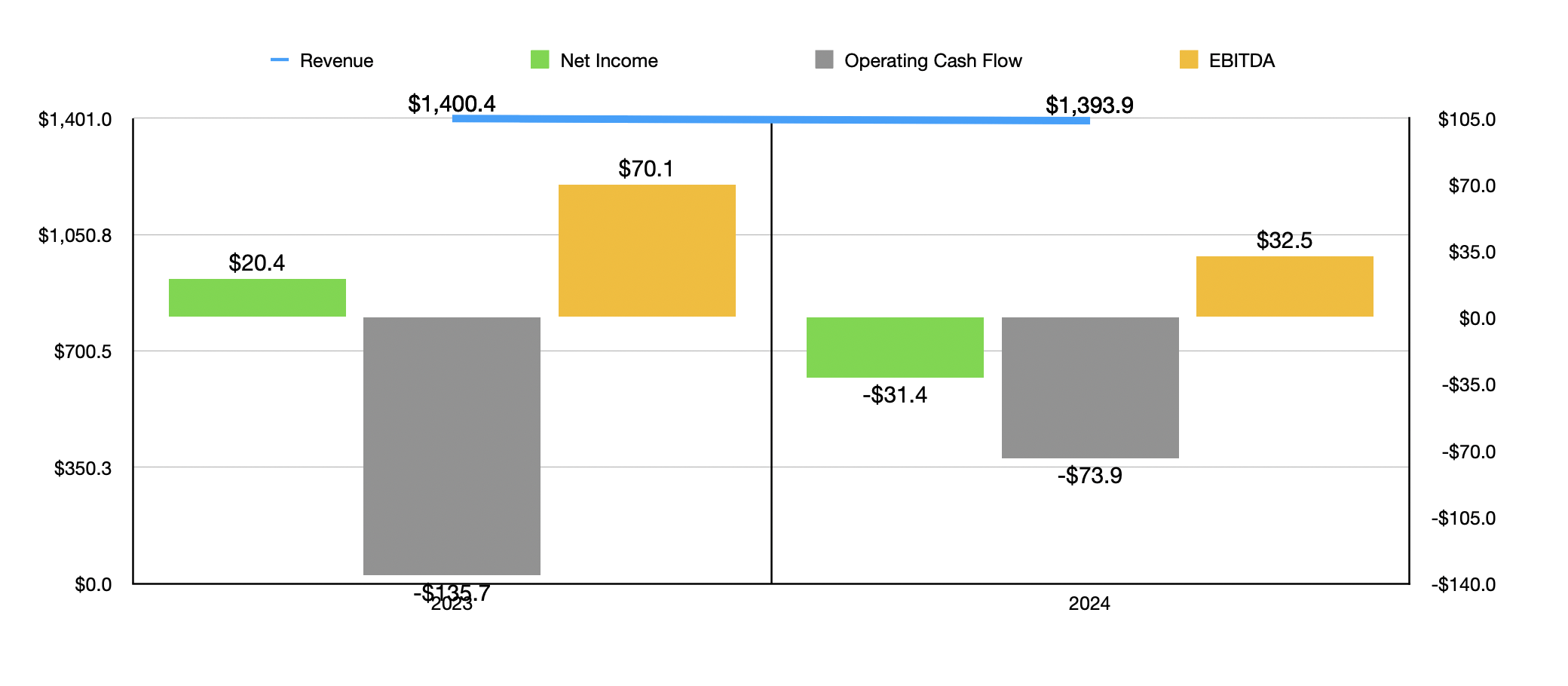

The final quarter of 2024 was not the only quarter in which the company has faced problems. In the chart above, you can see financial results for all of 2023 and all of 2024. Revenue dipped slightly from $1.40 billion to $1.39 billion. This came about as the number of retail vehicles sold dropped from 63,584 to 57,989. Total same store revenue declined by 1% during this window, with the number of retail units sold per location per month dropping from 34.2 to 31.4. The only thing that stopped sales from falling further was the fact that the average price per unit sold expanded from $18,080 to $19,113.

We don’t really know what to expect moving forward. We do know that even management said that sales for the company fell short of its own expectations. Management also lauded some acquisition activities that the company engaged in, including its most recent acquisition of Texas Auto Center that closed in early June. The firm did say that it is working to better control costs. However, some of these are likely outside of management’s ability to control it.

Author – SEC EDGAR Data

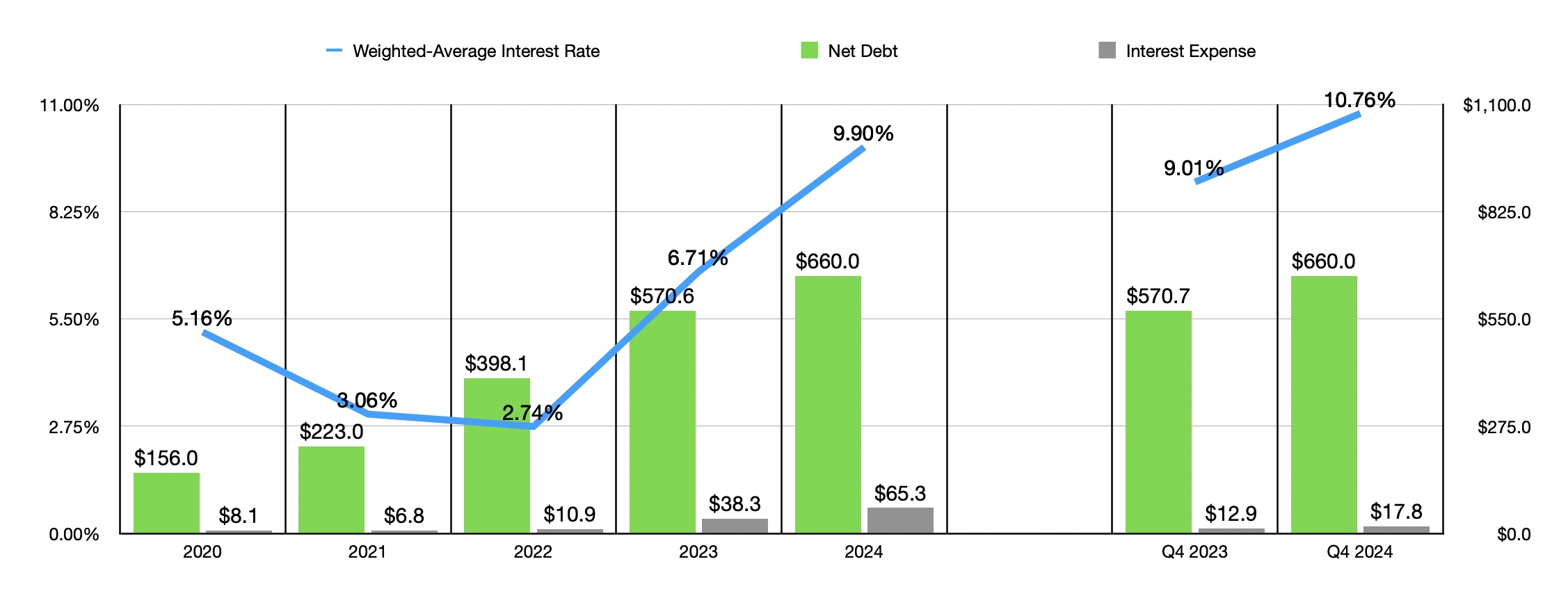

For starters, the overall financial situation of America’s Car-Mart has worsened over the past few years. The value of net debt on the company’s books, for instance, rose from $156 million back in 2020 to $660 million at the end of 2024. This rise in debt, combined with higher interest rates, caused interest expense for the company to balloon from $8.1 million to $65.3 million. In fact, the effective interest rate of the business has nearly doubled, from 5.16% to 9.90% over this window of time.

If we get selective, we get an even larger rise. In 2022, for instance, the weighted average interest rate for the business was only 2.74%. It is worth noting that, even though interest rates have been stable, they were even higher in the most recent quarter of this year, hitting 10.76% compared to the 9.01% reported for the final quarter of 2023.

Author – SEC EDGAR Data

It’s very likely that the increase in interest rates for the company is what has been responsible for the surge in the provision for credit losses that management has reported. After dropping from 24.8% of sales in 2020 to 20.3% of sales in 2021, the company’s provision for credit losses has nearly doubled, hitting 36.5% in 2024. In the most recent quarter, that reading was 28%. But that was still above the 26.4% increase seen the same time last year. This, combined with the rise in interest rates, is having a rather painful impact on investors.

It would be different if shares of the company were trading on the cheap. But that’s not exactly the case. Since earnings and cash flows were both negative in 2024, we can’t value the company based on those. And the EV to EBITDA multiple of the company surged from 14.6 using data from 2023 to 31.5 using data from 2024. In the table below, you can see how these numbers stack up against five similar enterprises. Given the results seen in 2024, America’s Car-Mart is actually the most expensive of the five companies that I decided to compare it to.

| Company | EV / EBITDA |

| America’s Car-Mart | 31.5 (14.6 Using 2023 Data) |

| CarMax (KMX) | 17.7 |

| AutoNation (AN) | 7.9 |

| Penske Automotive Group (PAG) | 9.0 |

| Group 1 Automotive (GPI) | 7.9 |

| Asbury Automotive Group (ABG) | 9.4 |

Takeaway

At this point, I believe that America’s Car-Mart is not a very pleasant company to own shares in. Some investors might view this drop as an opportunity to buy discounted. But I would argue that continued deterioration caused by broader market conditions and rising net debt should give America’s Car-Mart, Inc. investors pause. Because of this, I think that downgrading the firm to a ‘sell’ make sense.

Q2 2024 Earnings Call Transcript")