PaulMcKinnon

Amdocs Limited (NASDAQ:DOX) will always remain close to my heart, although I never worked there or invested in its stock. A close friend of mine was hired by Amdocs when they visited our college campus for a networking event in 2008/09. That may have been the worst time to graduate with a MBA degree and while everyone was busy attending events after events, this one guy was hired at a networking event casually because his profile was tailor-made for Amdocs: a communications guru who understood business strategy.

Amdocs, as a company, fits right into my area of expertise and interest as it operates in the Information Technology sector providing IT consulting, products, and other services. Headquartered in St. Louis, Missouri, Amdocs operates in many dozens of countries providing software and services for communications service providers. Amdocs boasts of more than 600 customers including the likes of AT&T (T) and T-Mobile US, Inc. (TMUS). The company went public in 1998 and reported $4.89 billion in FY 2023 revenue.

DOX Customers (Amdocs.com)

With that background out of the way, how does Amdocs look as an investment right now? I am presenting a few points that stand out in favor of DOX stock here. Let us get into the details.

Growing And Well-Covered Dividend

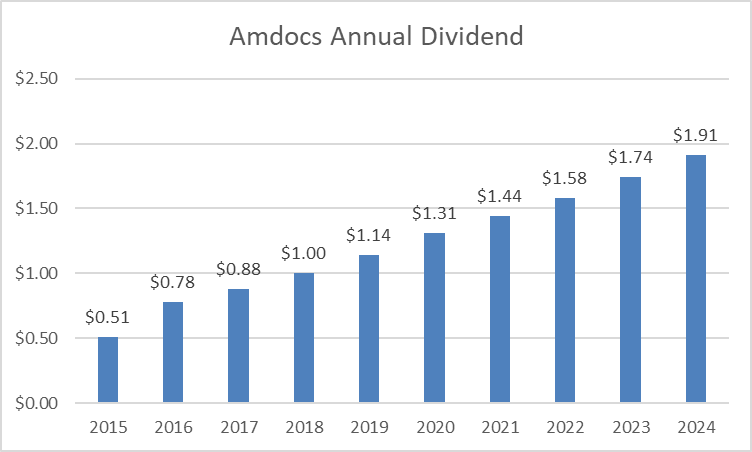

Amdocs has been paying dividends since 2012 with a budding dividend growth streak as the dividend has grown from 51 cents/share in 2015 to $1.74 in 2023. The company has also recently announced (page 49) that it plans to increase its quarterly dividend to $0.479 ($1.91 annualized) in 2024. That nudges the stock’s yield just past the 2% mark based on current market price of about $92.

DOX Dividend Growth (Author)

Based on forward earnings estimate of $6.51, Amdocs has an EPS based payout ratio of 29%. As I’ve stated in many of my articles, I prefer to use Free Cash Flow [FCF] instead of EPS as earnings tend to fluctuate, especially for technology stocks. As of the most recent quarter, Amdocs has 117 million shares outstanding, which means the company needs $56 million in quarterly FCF to cover its dividend commitment to shareholders. The company’s average quarterly FCF over the last 5 years stands at $150 million, which once again gives Amdocs a comfortable payout ratio of 37%. In short, I like the company’s budding dividend growth history and dividend coverage.

Pristine Balance Sheet

Amdocs has an enviable balance sheet with many stand out features.

- With total liabilities of $2.88 billion and total assets of $6.42 billion, Amdocs has an enviable debt-to-asset ratio of 0.44.

- Net Debt of just $64.8 million for a company with nearly $11 billion in market capitalization is not something we come across frequently in today’s over-leveraged world.

- Total common shares outstanding has gone down more than 8% since March 2021. Bear in mind we are talking about a company operating in the Information Technology sector, where dilution is one of the most frequently used methods to raise money.

Still Growing

Looking at the features above, a well-covered dividend, a disciplined balance sheet, and low-beta, one might falsely assume that Amdocs is a company that lacks growth, if not declining already. However, the company is expected to growth revenue by an average of about 5%/yr and EPS by an average of about 10%/yr. All these on the back of the company’s record revenue in 2023.

DOX EPS Growth (Seekingalpha.com) DOX Revenue Growth (Seekingalpha.com)

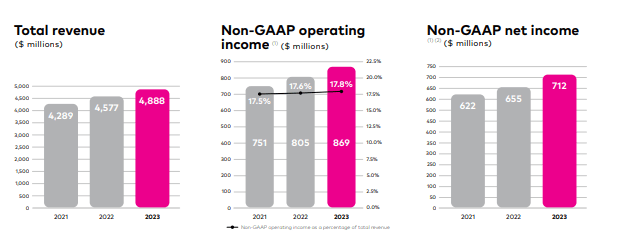

Amdocs reported increasing revenue, operating income and net income in 2022 as well as 2023, backed up its impressive portfolio of products and services. Operating at the cutting edge of digital experience, Amdocs is perfectly positioned to take advantage of advancements in telecommunications. As an example, as more consumers and telecom companies adopt 5G, Amdocs’ 5G experience lab not only incubates new solutions but also their monetization. Looking forward to 2024 and beyond, the company’s Chief Marketing Officer remarks that “2024 will be the beginning of a transformative era for global communications service providers.“

DOX Stats (amdocs.com)

Upcoming Earnings, Risks And Conclusion

Amdocs is expected to report earnings after-market on Tuesday, February 6th. All EPS and revenue revisions (although just 3 in total) have been to the downside, earning DOX an earnings revisions grade of just “D+” on Seeking Alpha. Should Amdocs meet its EPS and revenue estimate of $1.56 and $1.24 billion, it’d represent a YoY increase of 7.50% and 4.20% respectively. Given the company’s history of beating EPS and revenue revisions more often than not, I am willing to bet Amdocs delivers a double-beat.

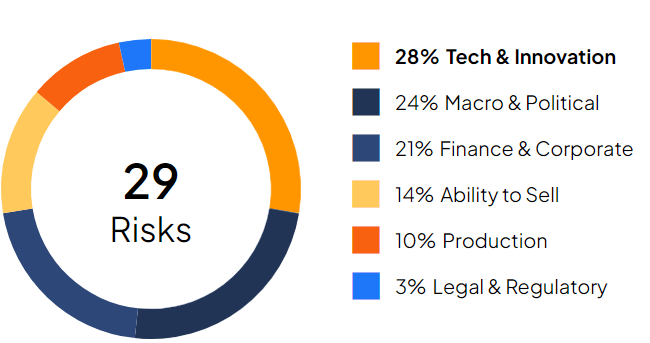

As positive as the sections above may depict Amdocs as an investment, no stock is devoid of risks. At a time when the market seems to be making new highs every day, Amdocs, with its low beta, is likely to underperform as and when investors embrace riskier positions. At the same time, Amdocs is not a high-yield investment either that some sections of the market will turn to when seeking safety. And therein lies the reward for those who look for hidden gems, which may not make headlines frequently but maybe quite effective in providing capital appreciation and income potential. While most of the risks outlined below may seem generic, Amdocs’ exposure to Israel needs to be called out as a significant risk.

DOX Risk (tipranks.com)

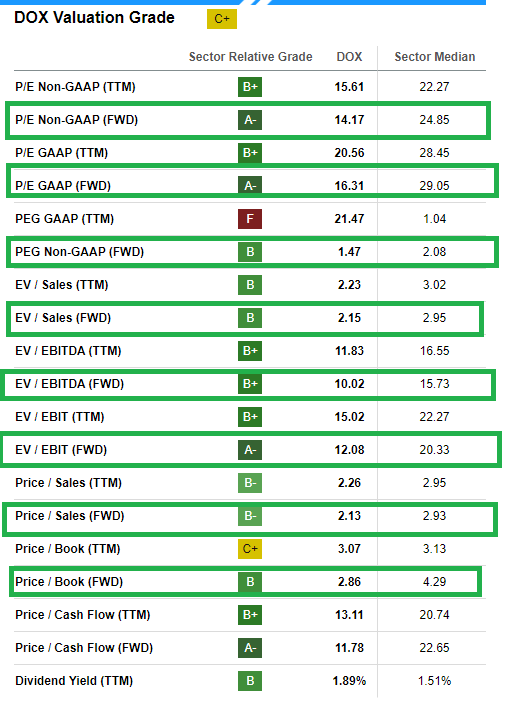

Overall, I rate the stock a “Buy” backed by its reliable dividend, competitive position, impressive forward valuation metrics (as shown below), and balance sheet health. Even if Amdocs is given just 75% of the sector median non-GAAP forward PE of 24.85, DOX stock will still be fairly valued at ~$120. That the stock is nearly 15% away from its median analyst price target of $105 helps as well. I look forward to revisiting my thesis in a quarter or two. Meanwhile, what do you think about Amdocs? Please leave your comments below.

DOX Valuation (Seekingalpha.com)

Q2 2024 Earnings Call Transcript")