Nora Carol Photography/Moment via Getty Images

2024 is off to the races, with the S&P 500 (SPY) making a new all-time high. After a brief dip to open the year, the index has gained ~ 1.5% year to date (YTD). Amazon (NASDAQ:AMZN) stock followed a similar pattern and has gained a little over 2%. The company will report Q4 and full-year earnings on February 1st after the market closes. You’ll be able to listen to the conference call here.

Here are some things to watch this year.

Will AWS growth accelerate?

Here are three reasons for optimism.

Artificial intelligence (AI) could be a massive growth driver for Amazon Web Services (AWS), and I’ll cover it below. Still, there is another reason I am optimistic that growth will accelerate in 2024: New budgets.

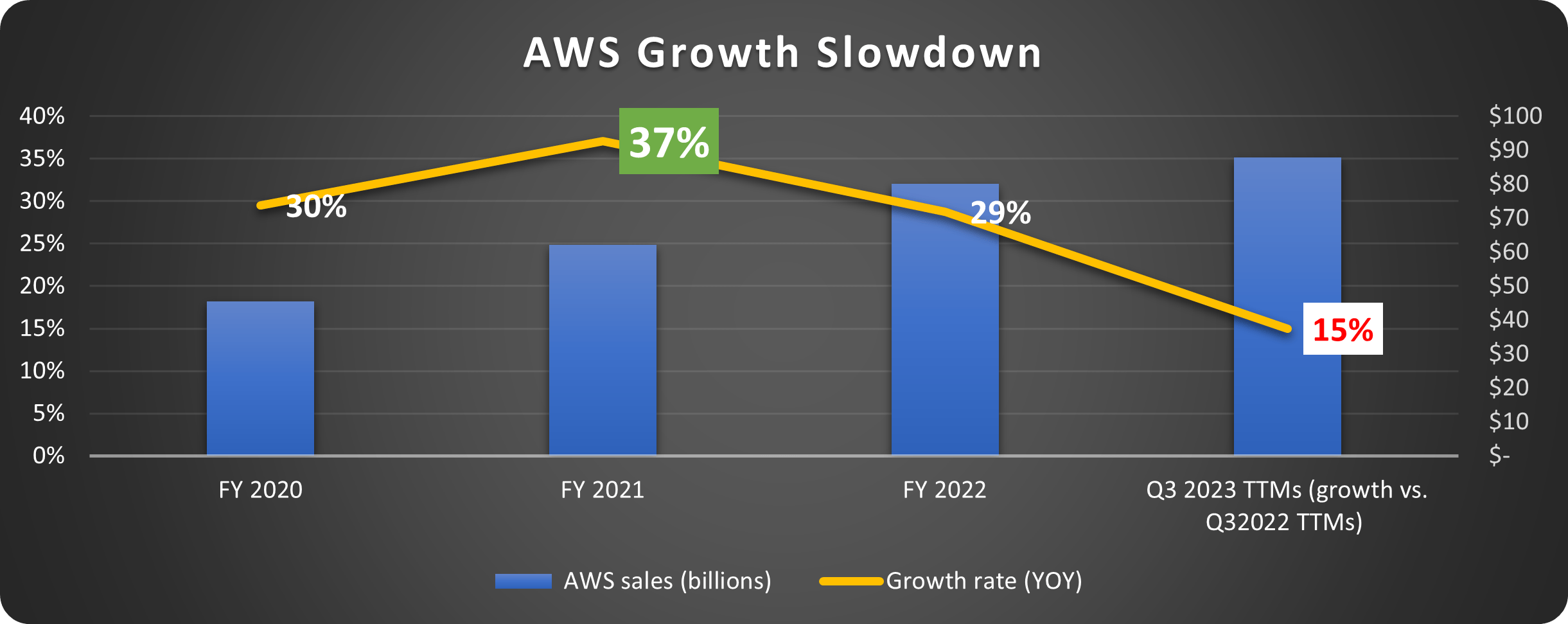

Many (probably a vast majority) of us expected a recession in 2023 that never materialized. This includes businesses that use cloud data. Much of AWS’s revenue functions like a utility – users pay for the data they use. It’s a terrific secular model since data use is almost guaranteed to increase exponentially over time. But it hurt in 2023, as depicted below.

Data source: Amazon. Chart by the author.

Companies across industries cut data-usage budgets last year. This is what happens when an economic slowdown happens or when it is widely forecast.

The second thing that happened is that many companies still operating on-premise paused moving to the cloud in 2023. Companies aren’t going to plan costly switches in advance of a recession. You may think, “Okay, but many are predicting a recession this year, too.” While that’s true, I don’t believe companies will hunker down two years in a row on a “maybe.”

Lastly, the massive data needs of generative AI could have a galvanizing effect. This third piece is also budget-related. We will see businesses investing in and experimenting with new technologies for years.

Much of the consternation over Amazon’s performance was the significant slowdown in the growth of AWS. The stock could take off if AWS sales accelerate. Q1 2024 results will be a great indicator.

Can advertising sustain the momentum?

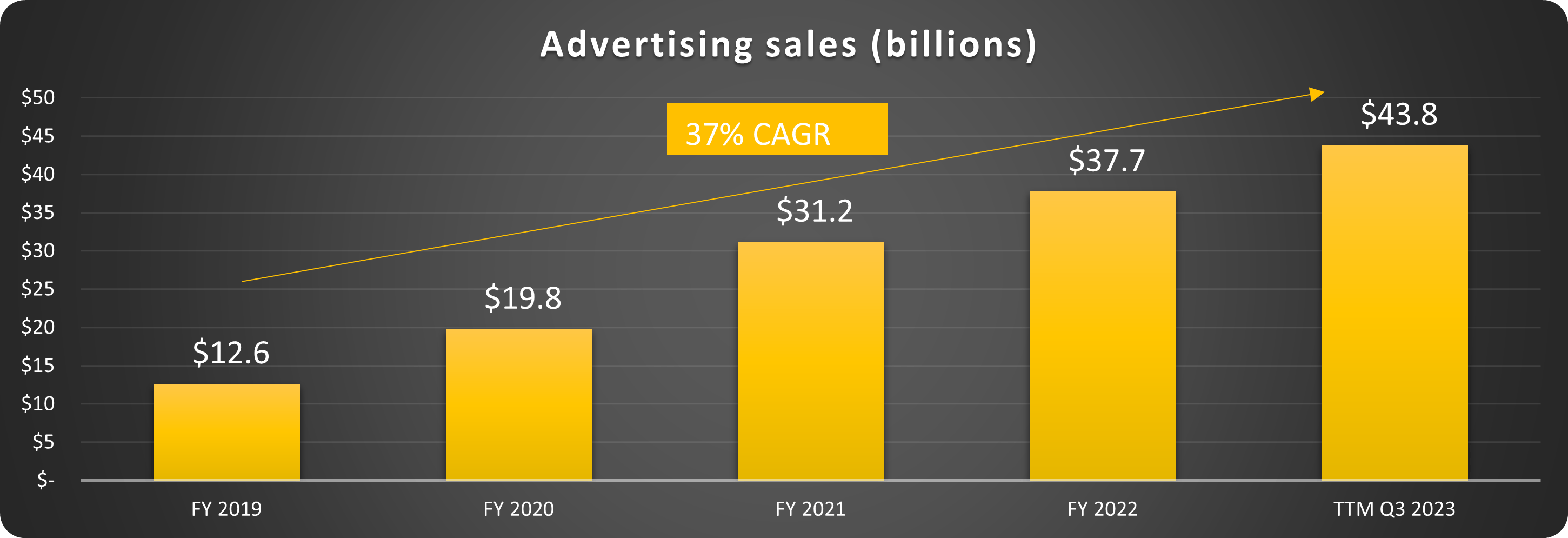

Digital advertising was a revelation last year. The overall ad market was flat, but Amazon’s pay-per-click, product placement, and other ads grew more than 20% YOY each quarter, including a 2023 high of 25% in Q3. Holiday advertising in Q4 could take this even higher.

This segment went from an afterthought to a powerhouse by nearly quadrupling sales in four years, as depicted below.

Data source: Amazon. Chart by author.

There are several reasons for this success. First, advertising is in a transition period. There are so many platforms now with streaming television, video, and social media platforms. Programmatic is taking hold, and advertisers are thinking beyond television.

Amazon is an attractive place to move those budgets because these ads reach consumers actively looking to purchase certain products. The company is also using AI to enhance performance for advertisers. Here is an example:

In advertising, we just launched a generative AI image generation tool, where all brands need to do is upload a product photo and description to quickly create unique lifestyle images that will help customers discover products they love. – CEO Andy Jassy on Q3 2023 earnings call.

This type of value-adding initiative will keep Amazon’s ad business growing faster than the industry as a whole.

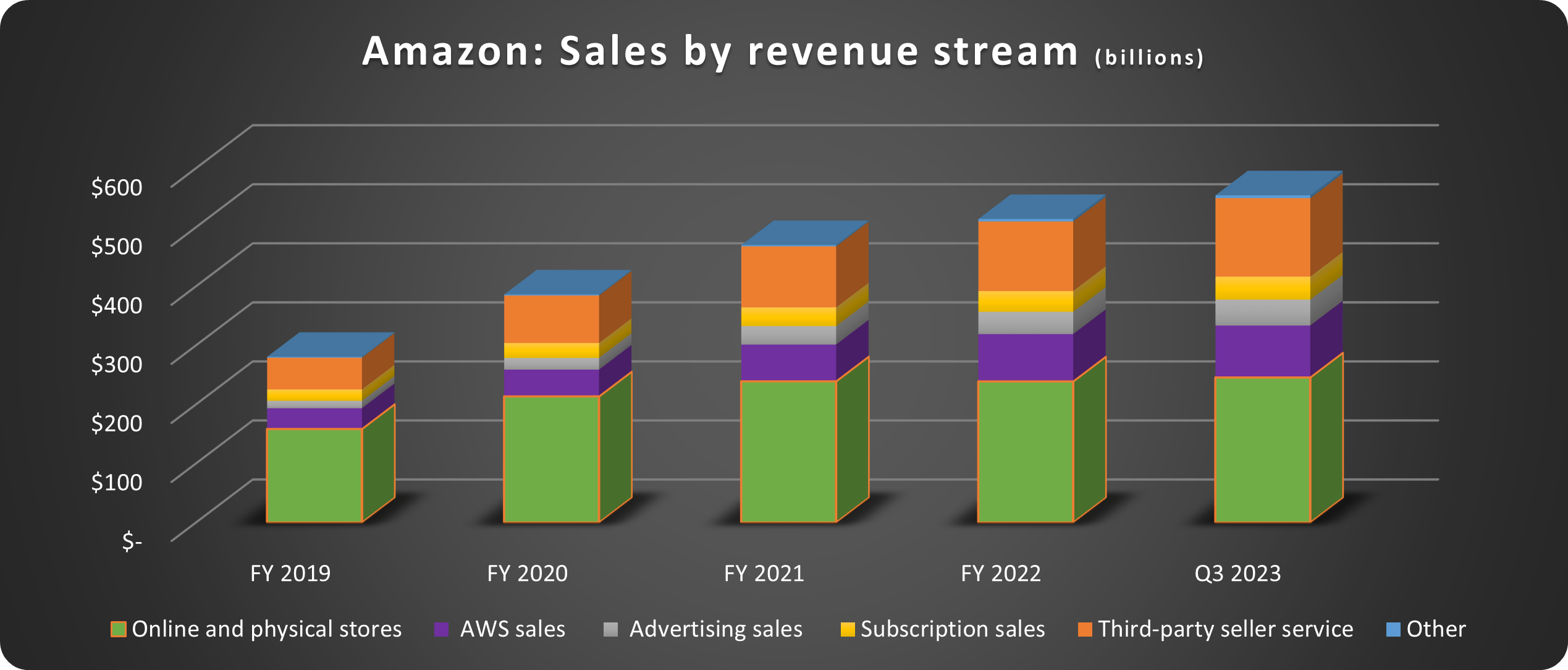

The advancement of this segment creates another solid service revenue stream, further diversifying into segments with high-margin potential, as shown below.

Data source: Amazon. Chart by author.

The difference between 2019 and now is astronomical and a testament to terrific management.

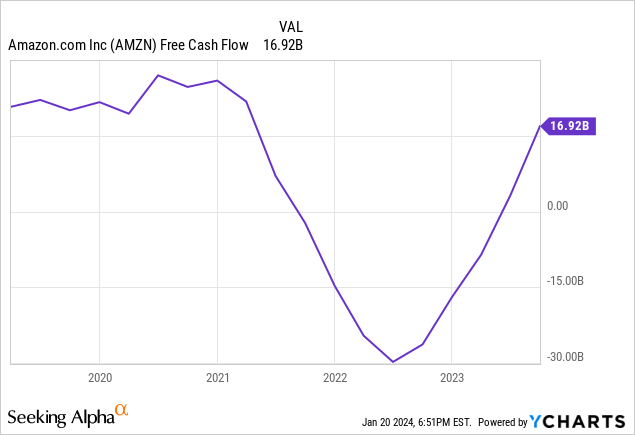

Will free cash flow stay strong?

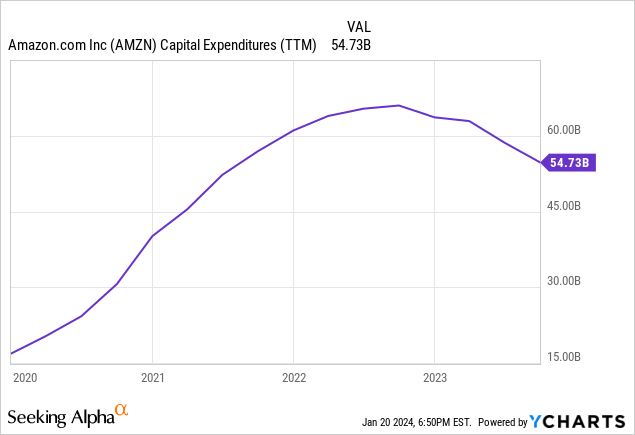

Cash is back! After bottoming in 2022 due to a plethora of COVID boomerang effects and significant capital investment (CapEx). Now, CapEx has stabilized, as depicted below.

Other issues like labor and logistics were also ironed out last year, and free cash flow came back in a big way:

The tailwinds in Amazon’s service revenues could push this higher in 2024.

Is Amazon stock a buy?

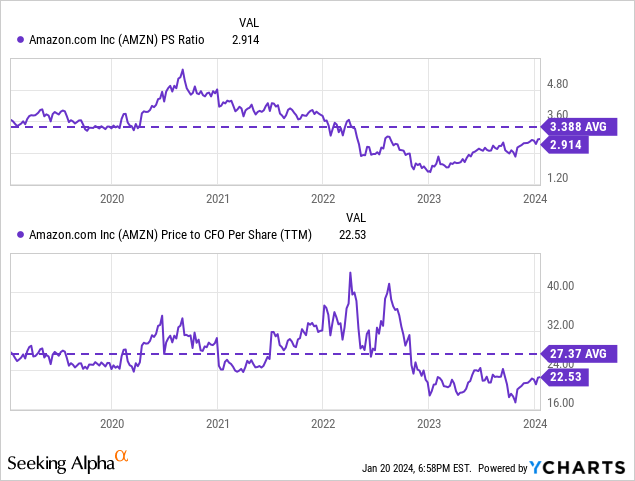

Despite the tremendous performance and kudos given to the Magnificent 7, Amazon is undervalued historically, 17% below its all-time high, and the price doesn’t reflect the company’s potential. There are numerous ways to value Amazon stock; I prefer looking at it in terms of sales and operating cash flow.

These metrics put the stock 16% to 21% below 5-year averages. Amazon is a terrific long-term investment and will have an excellent 2024 if AWS, advertising, and cash flow thrive.

Q2 2024 Earnings Call Transcript")