Andrew Burton

Despite reporting decent earnings numbers last month, Alibaba’s (NYSE:BABA) stock failed to gain momentum and has been underperforming against the broader market in recent quarters. As international capital continues to leave China in droves while the geopolitical risks are on the rise, it’s safe to assume that Alibaba’s stock is likely to remain ‘dead money’ in the foreseeable future due to the lack of major catalysts that could improve the situation. Therefore, I believe that it’s much better to look for opportunities back home rather than trying your luck investing in Alibaba, which still hasn’t recovered from the Beijing-led crackdown that began more than three years ago.

More Challenges Ahead

Since the publication of my latest article on Alibaba in November, the company’s shares have depreciated by over 5% and greatly underperformed against the broader market. Even though the company revealed a decent earnings report for Q3 last month, which showed that the revenues during the period increased by 5% Y/Y to $36.67 billion, it was not enough for Alibaba’s shares to appreciate and create additional shareholder value along the way.

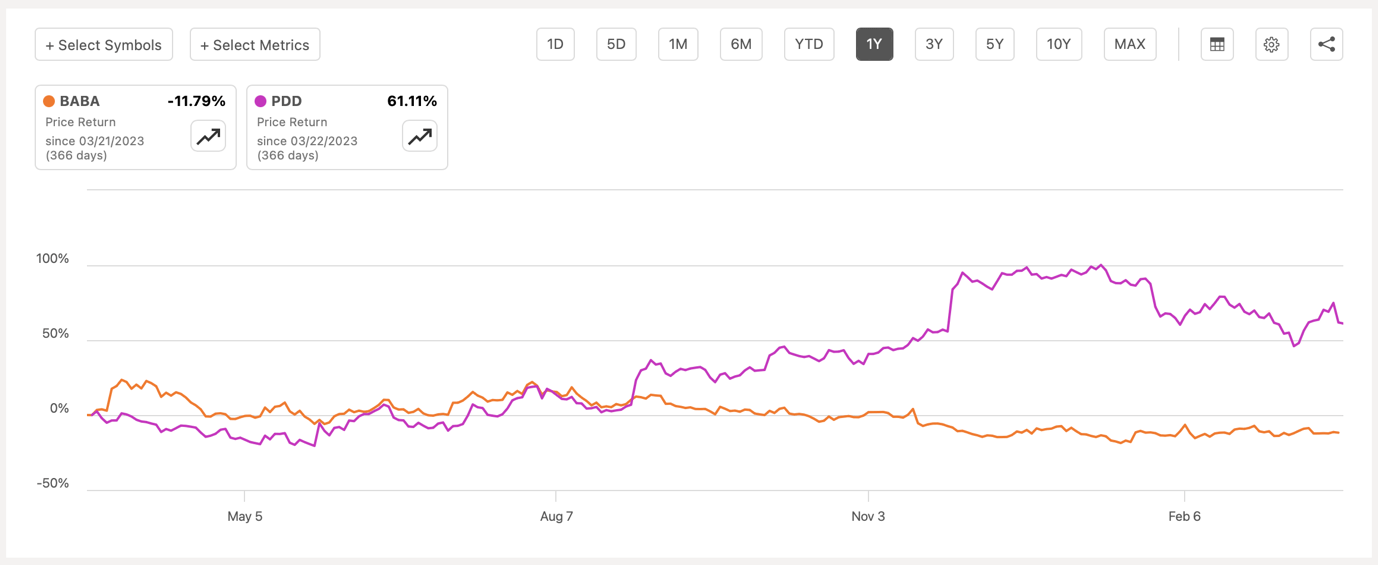

In part, this is due to the fact that Alibaba’s core eCommerce business is unable to pick up momentum amidst China’s economic troubles. In Q3, Alibaba’s Taobao and Tmall Group business generated $18.18 billion in revenues, an increase of only 2% Y/Y. For comparison, Alibaba’s competitor PDD Holdings (PDD) recently announced that it generated $12.52 billion in revenues for the December quarter, an increase of 123% Y/Y. Such an impressive growth rate has been achieved in part thanks to the aggressive marketing strategy that the company’s Temu business executes to drive sales and quickly attract new customers. In the last year, PDD Holding’s shares have already outperformed Alibaba and if the business continues to grow at a similar aggressive rate, then it’s only a matter of time until it starts to generate more revenues than Alibaba’s core business itself.

Comparison Chart (Seeking Alpha)

At the same time, Alibaba’s cloud business also continues to struggle due to the increased competition and geopolitical challenges. For the December quarter, Alibaba’s cloud business generated $3.95 billion in revenues, up only 3% Y/Y. For comparison, the cloud businesses of Microsoft (MSFT), Amazon (AMZN), and Google (GOOG)(GOOGL) generated $25.9 billion, $24.2 billion, and $9.19 billion in revenues which implies a growth of 20% Y/Y, 13% Y/Y, and 25.5% Y/Y, respectively.

At the current growth rate, Alibaba is unlikely to pose a threat to Western dominance in the cloud industry anytime soon and the rising domestic competition will only make it harder for the company to greatly improve its cloud business. That’s why it’s also likely that Western tech companies will continue to outperform Alibaba and be a more attractive investment in the foreseeable future.

Comparison Chart (Seeking Alpha)

The only major upside for Alibaba at this stage is the fact that the company is likely to decently improve its top-line and bottom-line growth rates in the following years after a disappointing performance last year. However, that might not be enough to help the stock greatly appreciate anytime soon.

Chinese Communist Party Is Here To Stay

Back in 2021, I started covering Alibaba here on Seeking Alpha, and my first article on the company was titled Alibaba: Like It Or Not, Chinese Communist Party Is Here To Stay. In that article, I said that while it appeared that the Beijing-led crackdown against the private sector is coming to an end, there’s no guarantee that Alibaba won’t feel any more pressure from the central government. Since that time, Beijing has greatly strengthened its grip over Chinese society, Alibaba’s share price has halved in half, and the Chinese government now officially has a stake in some of the company’s businesses. While all of that is the result of the structural changes that happened in China under the leadership of Xi Jinping, those changes are likely to continue to have a direct negative impact on the performance of Alibaba’s business and its shares in the long run.

Currently, China is the only major economy in the world that is dealing with deflation and there’s an indication that things there are unlikely to improve anytime soon due to the unwillingness of Beijing to approve new stimulus measures. This is likely to have a direct impact on Alibaba’s struggling eCommerce business.

What’s more, is that the international capital is now leaving China and last year the country suffered its first net outflow of funds in years. Without an influx of international capital, it’s hard to see how the shares of Alibaba are supposed to appreciate anytime soon, especially at a time when China itself continues to face new systemic risks.

On top of all of that, Beijing is likely to continue to put additional pressure on the private sector and centralize the power in the country in light of the rising geopolitical tensions that threaten to undermine the current rules-based international order. As such, it’s hard to justify a long position in Alibaba even at the current price since it appears that risks continue to outweigh the growth opportunities.

The Valuation Argument

In most of my previous articles on Alibaba, I’ve been saying that the company is fundamentally undervalued but the valuation argument doesn’t significantly matter at this stage. This is due to the fact that the current market sentiment has continued to be heavily biased against Chinese companies since late 2020 when the Beijing-led crackdown against the private sector began. While Alibaba has been fundamentally undervalued for a while, it didn’t stop its shares from continuing to depreciate further and trading in distressed territory.

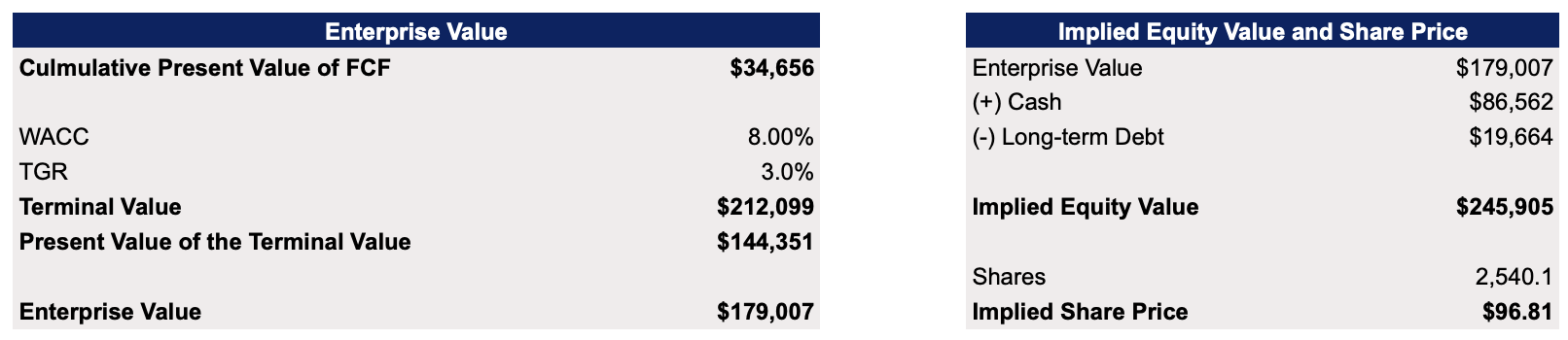

My DCF model below clearly shows that Alibaba’s shares are worth holding from a purely fundamental point of view. The assumptions in the model are mostly either in-line with the street estimates or are close to the historical levels. The terminal growth rate in the model is 3%, while the WACC is 8%.

Alibaba’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

The model shows that Alibaba’s enterprise value is $179 billion, while its fair value is $96.81 per share, which represents an upside of ~34% from the current market price.

Alibaba’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

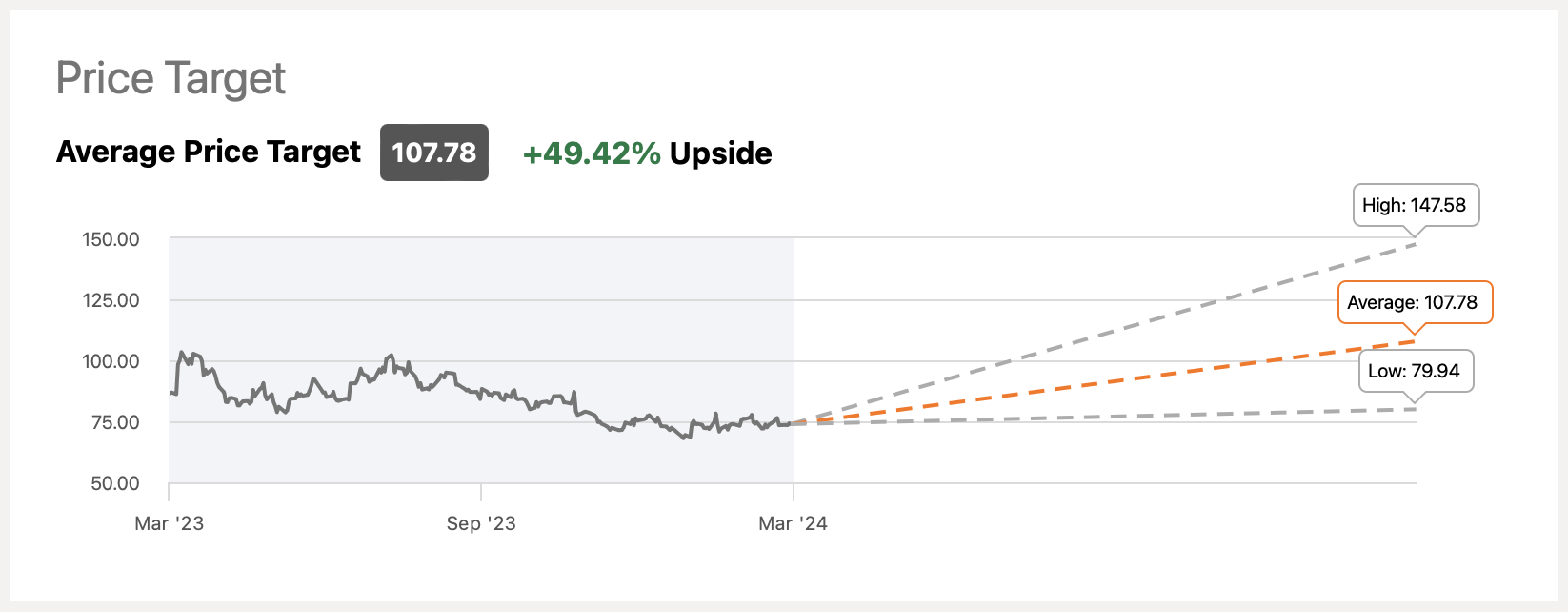

Such a price target is also slightly below the consensus on the street, but also significantly above the lowest target.

Consensus Price Target (Seeking Alpha)

Despite this, it’s hard to give Alibaba a BUY rating at this stage due to the lack of momentum and the fact that the current market sentiment continues to be mostly biased against Chinese companies.

That’s why when it comes to value or growth investing, I continue to believe that there are much better opportunities back at home where undervalued companies are more likely to create shareholder value in comparison to their Chinese-based peers. The comparison chart below clearly supports this view since the typical ETF (SPY) that holds shares of companies from the S&P 500 Index which trade at greater multiples has been outperforming Alibaba in recent years.

Comparison Chart (Seeking Alpha)

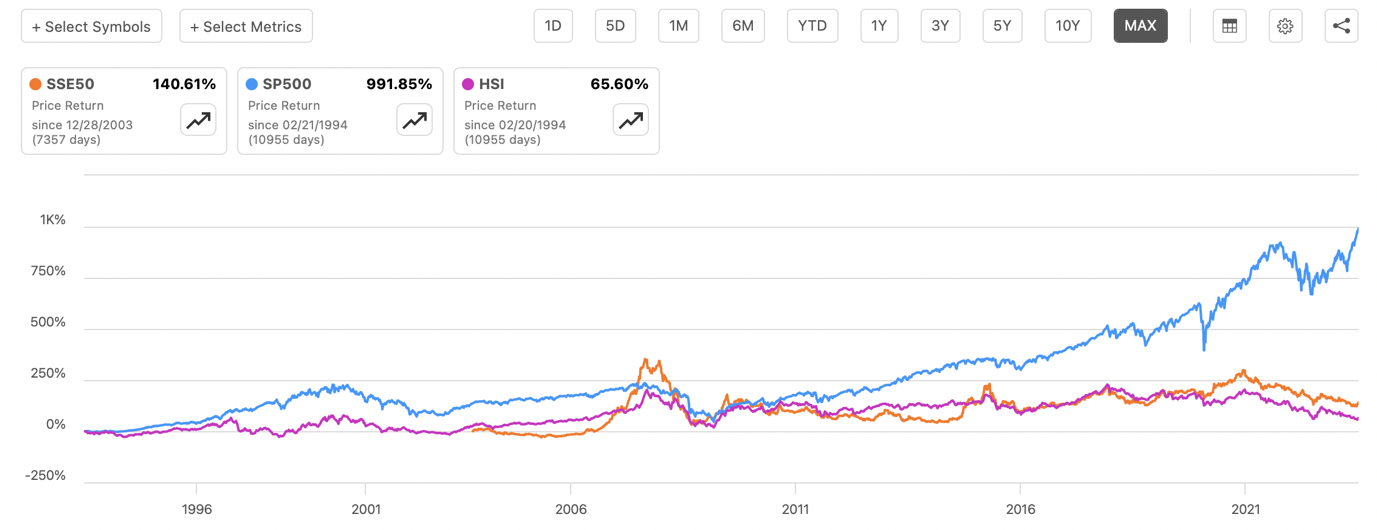

What’s more, is that Chinese-based investments have been a bad bet for investors in recent decades. Although the Chinese GDP has been growing at an impressive pace since the country’s inclusion into the WTO in 2001, the S&P 500 has nevertheless greatly outperformed the main Chinese (SSE50) and Hong Kong (HIS) indexes since the start of the 21st century. Given the rise of geopolitical tensions, it’s safe to assume that this will continue to be the case in the foreseeable future.

Comparison Chart (Seeking Alpha)

The Bottom Line

Given Alibaba’s history of constant underperformance despite reporting decent earnings numbers and trading at a discount from a fundamental point of view, it makes sense to assume that its stock will remain ‘dead money’ in the foreseeable future. That’s why I’m sticking with my HOLD rating since the stock will likely continue to trade around the current price with a limited upside and downside at the same time, as was the case in recent years.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")