A researcher works in a lab. LaylaBird

No matter whether the market is rallying or sliding, I contend as a long-term investor, there are always intelligent investments available to be made.

To say that the S&P 500 Index (SP500) has been on a tear as of late would be an understatement. Thanks to strong fundamentals, the index has already gained 6% so far this year according to Seeking Alpha. That’s making it a bit harder to find value, but it’s certainly not impossible.

REITs are one market sector that, I believe, has its share of bargains right now. Since peaking in April 2022 at $112 per Seeking Alpha, Vanguard Real Estate Index Fund ETF Shares (VNQ) have fallen 24%.

A specific REIT that I believe currently offers a great deal of value is the life sciences office REIT, Alexandria Real Estate Equities, Inc. (NYSE:ARE). For the first time since I initiated coverage in December, I will revisit the company’s fundamentals and valuation to underscore why I’m maintaining my buy rating.

Dividend Kings Zen Research Terminal

Even for a REIT, ARE’s 4.3% dividend yield catches my attention. Better yet, the fundamentals underpin my belief that plenty of dividend growth is still in the company’s future.

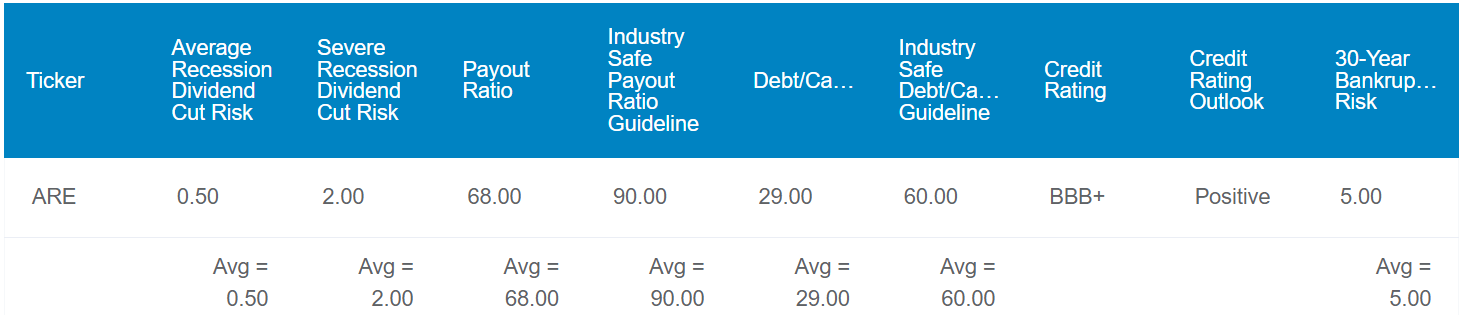

That’s because the 68% FFO payout ratio is below the 90% payout ratio that rating agencies desire from REITs. Also, ARE is well-capitalized. This is supported by a 29% debt-to-capital ratio, which is approximately half of the 60% debt-to-capital ratio that rating agencies prefer from REITs. Thanks to these vigorous fundamentals, ARE’s long-term debt is rated a BBB+ on a positive outlook from S&P. That suggests the 30-year probability of bankruptcy is somewhere between 2.5% (for an A- rating that ARE could eventually have) to 5% (for its current credit rating).

As a result of these factors, the risk of a dividend cut from ARE in the next average recession is 0.5%. In a severe recession, this rises to 2%. For context, these are the lowest allowed values in The Dividend Kings’ Zen Research Terminal.

Dividend Kings Zen Research Terminal

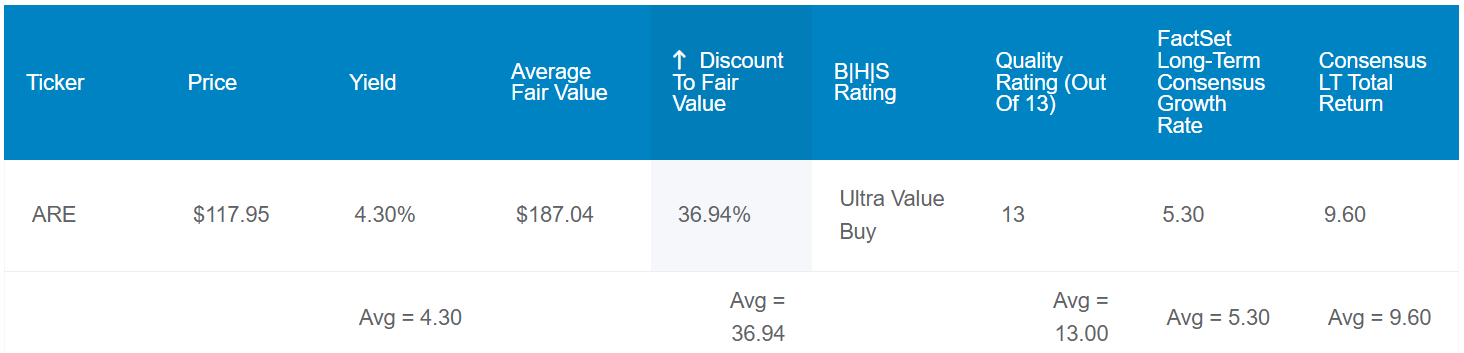

ARE’s appeal doesn’t end at its fundamentals, either. If the 10-year and 25-year P/FFO ratios and dividend yields are any guide, shares could be worth $187 apiece. Compared to the $119 share price (as of February 15, 2024), that would equate to a 36% discount to fair value.

If ARE reverted to fair value and met the growth consensus, here are the total returns that could lie ahead over the next 10 years:

- 4.3% yield + 5.3% FactSet Research annual growth consensus + a 4.6% annual valuation multiple expansion = 14.2% annual total return potential or a 277% 10-year cumulative total return versus the 10% annual total return potential of the S&P or a 159% 10-year cumulative total return

Closing 2023 With Decent Growth

ARE Q4 2023 Earnings Press Release

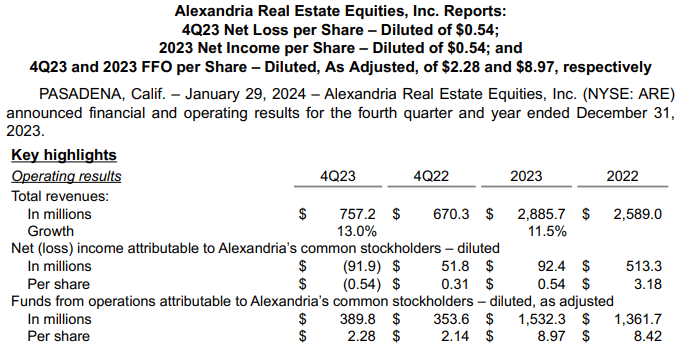

ARE’s operating results for the fourth quarter ended Dec. 31 were respectable. The company reported $757.2 million in total revenue during the quarter, which was up 13% over the year-ago period.

Even accounting for a share count that was up 3.4% year-over-year, that’s a satisfying growth rate.

What’s more, this revenue figure was $5.8 million greater than the analyst revenue consensus.

The driving factor behind this topline growth was the 2.5 million rentable square footage of properties that were placed into service in 2023. For context, these activities lifted ARE’s total rentable square footage by over 6% over the year-ago period to 42 million to conclude 2023.

Another equally important ingredient that fueled the company’s rent growth in 2023 was its rent escalators. That’s because according to ARE, 96% of its leases contain contractual annual rent escalations of approximately 3%. Additionally, the REIT’s occupancy remained high at 94.6% to end 2023.

The company’s FFO per share grew by 6.5% year-over-year to $2.28 in the fourth quarter. That missed the analyst consensus by just $0.01. ARE’s much higher revenue was only partially offset by a 130 basis point decline in its FFO margin to 51.5% for the quarter. Coupled with the higher share count, this explains how the company’s FFO per share rose at a slower rate than revenue during the quarter.

ARE’s FFO per share growth in Q4 was also the same as its overall FFO per share growth in the full year 2023. Looking ahead to 2024, the company issued midpoint FFO per share guidance of $9.47 – – a 5.6% growth rate over the $8.97 in FFO per share generated in 2023. Analysts agree with this growth forecast, also predicting $9.47 in FFO per share for 2024. The path to this level of growth is straightforward, which is why I think the company and analysts will be proven correct.

After acquiring $259 million of properties in 2023, ARE believes that it will acquire anywhere from $250 million to $750 million in 2024. At the midpoint, this would be a significant uptick from 2023.

As interest rates have somewhat stabilized, it makes sense that the company would be more aggressive with acquisitions. That’s especially the case considering that ARE just priced $1 billion of notes – – $400 million due in 2036 at 5.25% and another $600 million due in 2054 at 5.625%. Given the high interest rate environment, this is attractively priced capital from my perspective.

Alongside some of the company’s ongoing projects that are expected to be placed into service in 2024, this is why I am optimistic that ARE can deliver on its guidance (unless otherwise hyperlinked or noted, all details were sourced from ARE’s Q4 2023 Earnings Press Release).

Solid Dividend Growth Ahead

ARE’s quarterly dividend per share has cumulatively compounded by 30.9% in the past five years to the current rate of $1.27. That’s equivalent to a 5.5% compound annual growth rate.

Moving forward, I wouldn’t be surprised if the company delivered similar dividend growth. Assuming the quarterly dividend per share is raised to $1.30 in June, ARE would be on track to pay $5.14 in dividends per share in 2024. Against the $9.47 FFO per share midpoint, that would be an FFO payout ratio of just 54.3%. Such a low payout ratio would allow dividend growth in line with FFO per share growth to persist for the foreseeable future.

Risks To Consider

As the leader in the life sciences REIT space, ARE is a high-quality business. Nevertheless, the REIT has risks that are worth at least a brief discussion.

One key risk to ARE is the potential for construction projects to experience cost overruns and time delays. The company’s contractors and material suppliers could experience issues or go out of business. If that happened, there would be no guarantee the company could find new contractors and suppliers to take their place who would meet material or labor needs.

Another risk is the potential for its properties to develop mold and other air quality issues. If this happened, ARE could be held liable for such events and be forced to sink substantial resources into remedying such an issue.

Summary: A High-Quality, Reversion To The Mean Pick

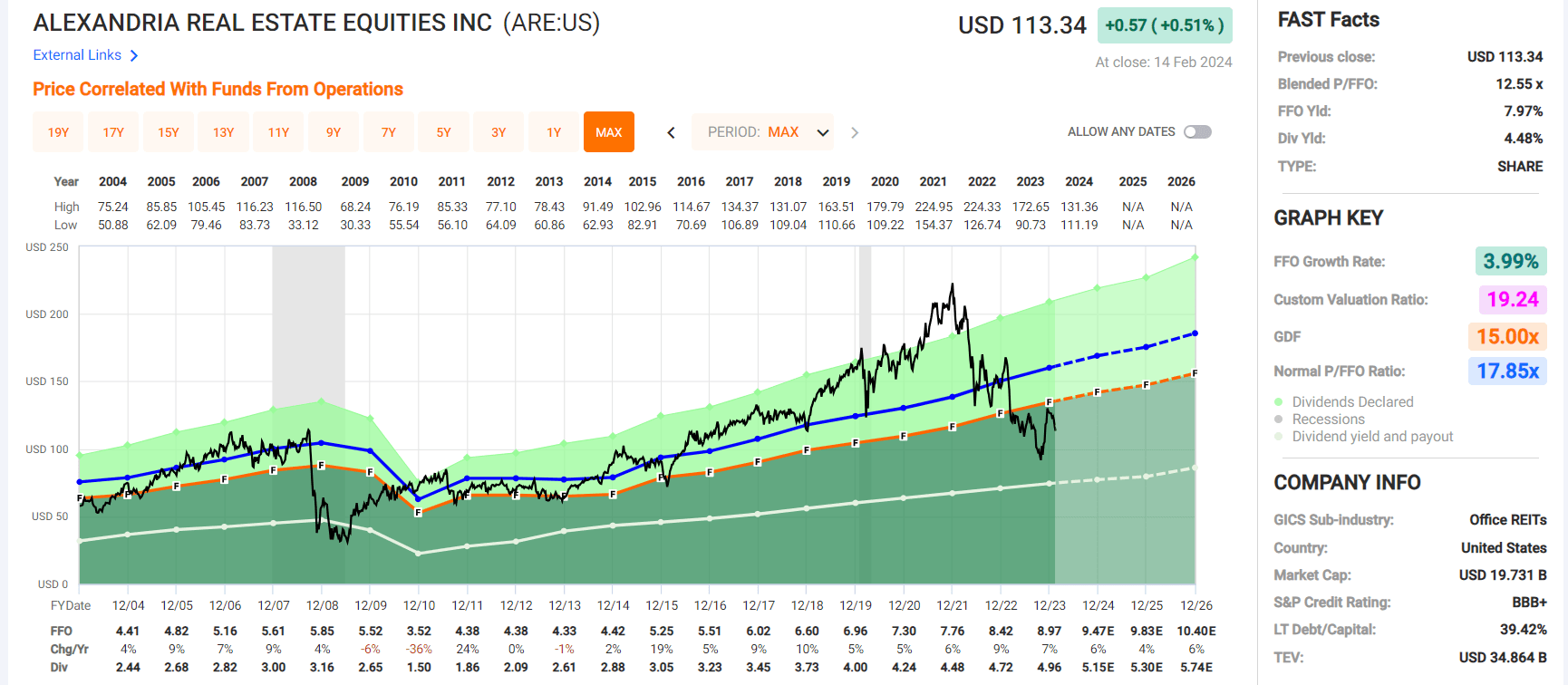

FAST Graphs, FactSet

ARE is an intriguing value pick in my opinion. The company’s blended P/FFO ratio of 12.6 is well below the normal P/FFO ratio of 17.9. ARE’s fundamentals appear to be about as strong as they have been in the past. As the company keeps delivering mid-single-digit annual FFO per share growth, I believe the market will have no choice but to rerate the stock at a valuation multiple closer to its historical norm. That’s why I am confident in reiterating my buy rating now.

Q2 2024 Earnings Call Transcript")