Stephen Brashear

Investment Thesis

I think that Alaska Air Group Inc. (NYSE:ALK) is a hold. The merger with Hawaiian Airlines (HA) brings opportunities for growth however there are also risks associated with their Boeing (BA) 737 MAX fleet. The merger will expand their market reach and services which can give them an edge and drive growth. However, relying on the Boeing 737 MAX comes with financial vulnerabilities since they have faced issues in the past. Even though a discounted cash flow (DCF) analysis suggests a solid return, I think it’s best to hold the stock currently. This outlook depends on avoiding economic downturns and any further disruptions caused by the 737 MAX. Therefore, when making investment decisions one should carefully consider the benefits of the merger while also taking into account the risks related to Alaska Air Group’s fleet composition.

Company Overview

Alaska Air Group is a well-known airline company headquartered in the Seattle area. They own two airlines: Alaska Airlines and Horizon Air. The company primarily earns its revenue by transporting passengers across the United States, Canada, Central America and the Caribbean, offering flights to 125 destinations. What sets Alaska Air Group apart is their customer approach, use of technology and commitment to sustainability. These qualities have earned them a robust customer base and numerous accolades within the industry.

The airline industry is highly competitive, with Alaska Air Group facing rivals such as Delta Air Lines (DAL), American Airlines (AAL) and United Airlines (UAL). These competitors often have vast flight networks and greater financial resources. However, despite this challenging landscape, Alaska Air Group has successfully maintained its presence in the aviation market throughout the Pacific Northwest and along the West Coast largely due to their efficiency. This success was further demonstrated by their announcement of acquiring Hawaiian Airlines, which strengthens their position within the industry.

The Hawaiian Airlines Merger Expands their Network And Enhances Customer Appeal

During Alaska Air Group’s earnings conference call, management provided updates on various key issues and opportunities that the company is currently facing. One of these updates involved the announced acquisition of Hawaiian Airlines. Under this deal Alaska Air Group will be purchasing Hawaiian Airlines at an agreed price of $18 per share. This acquisition will not only allow Alaska Air Group to expand its holdings but also significantly improve its product range and travel options. With service to 138 destinations, including 29 international destinations, customers will greatly benefit from this merger as emphasized by the management.

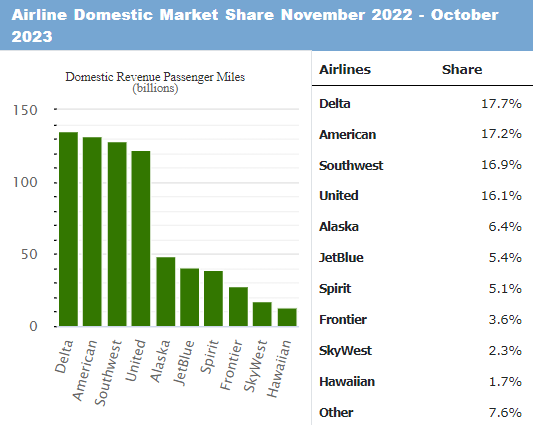

In my opinion the merger between Alaska Air Group and Hawaiian Airlines offers advantages for investors beyond simply expanding their network. Firstly, it aligns well with Alaska Airlines’ strategic goal of strengthening its presence on the West Coast and expanding its market reach. According to the report from the Bureau of Transportation Statistics Alaska Airlines holds a market share of 6.4% in the US domestic market – a slight increase from 2022 but still considerably lower than that of major US airlines. By adding Hawaiian Airlines to their portfolio, Alaska Air Group’s market share should surpass 8% closing in on the leading four airlines and narrowing the gap between them.

US Domestic Aviation Market Share (Bureau of Transportation Statistics)

I anticipate that this increase in market share will be reflected within the total revenue which should grow significantly following the acquisition. I also believe this merger will have a positive impact beyond just a proportional increase in market share and revenue as, in my opinion, it is likely that more customers will be inclined to fly with Alaska Airlines or Hawaiian Airlines as each of their product offerings, such as their loyalty programs will become more attractive as new route options open up that were previously unavailable. As such, my expectation is that Alaska Air Group will expand its market share at a faster rate following the merger.

However, despite the positives, the transaction will come at a considerable cost. The transaction is valued at approximately $1.9 billion or $19 per share which suggests a compelling premium for Hawaiian Airlines shareholders from the current price of $14.25, although most of the gains came the day of the announcement, given that the stock more than tripled. According to management, the merger is projected to generate high-single digit earnings accretion for Alaska Airlines within the first two years post-closure, with mid-teens return on invested capital by the third year. This suggests a strong potential for increased profitability and a healthy return on investment, which is a positive signal for investors. Moreover, the merger is designed with an eye towards maintaining a stable balance sheet, with a return to target leverage levels expected within 24 months, indicating a responsible approach to financial management that should be reassuring to investors. Whilst this is optimistic, I think it is important to consider that Hawaiian Airlines’ financials are not in a good position currently and it will take a lot of work to elevate the company to the level of Alaska Airlines which I believe will require patience from investors.

Alaska’s Concentrated Fleet Structure Could Be A Double Edge Sword

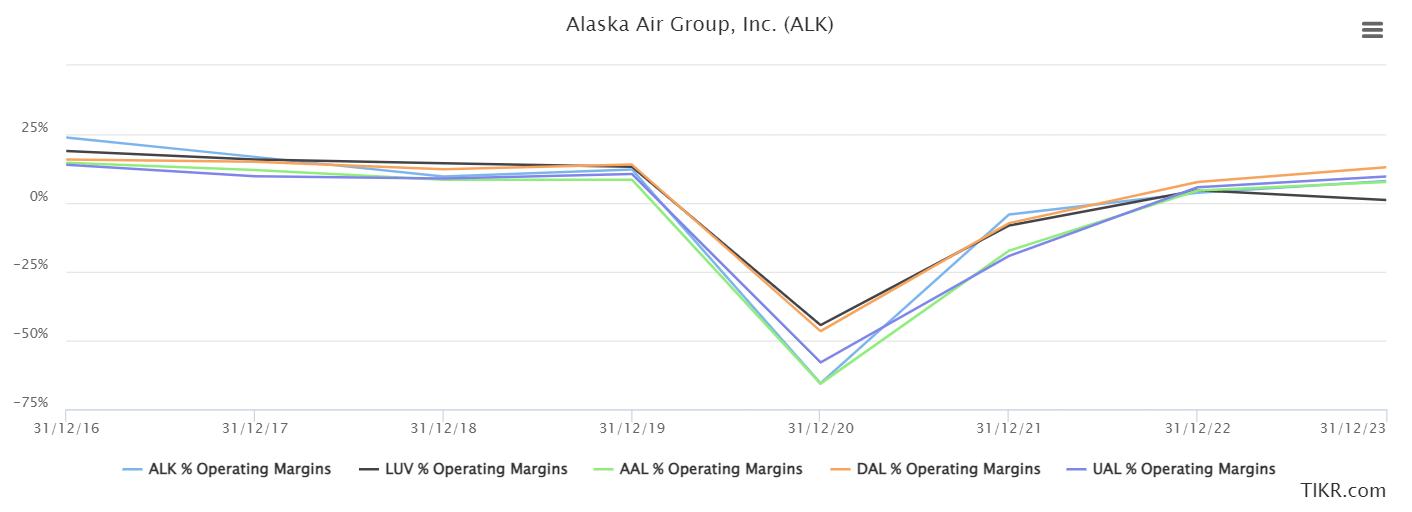

One of the reasons that Alaska has been put in a position to acquire a competitor such as Hawaiian Airlines is its strong operational efficiency and cost management which is better than many of its competitors and is reflected in their operating margins which regularly exceeds that of major airlines such as American Airlines and Delta, although it’s worth noting that their margins have yet to recover to pre-pandemic levels.

Comparison of Operating Margins for Major US Airlines (TIKR)

I believe that one of the driving forces behind the company’s strong operational efficiency is the fleet structure, which is heavily concentrated on one aircraft, the Boeing 737. As of 31 December 2023, Alaska Air Group maintains an operational fleet of 231 Boeing 737 aircraft and 83 Embraer 175 aircraft with the 737s being operated by Alaska Airlines whilst the Embraer 175 aircrafts being operated by Horizon Air. Operating a fleet with a single aircraft model offers several operational and cost advantages. This approach simplifies maintenance and ground operations significantly. With a uniform fleet, ground crews can master their tasks more efficiently leading to improved operational productivity. This uniformity extends to maintenance as well, where the need for various parts and specialized training for different aircraft types is eliminated. As a result, this not only reduces the time spent on maintenance but also lowers operational costs due to the reduced complexity in managing inventory and training requirements. This, however, also exposes the company to heightened risk if issues arise with one of the aircraft types, something we have seen recently.

As we have seen, Alaska Air Group has recently faced a notable decline in its stock price, primarily due to issues with its Boeing 737 MAX aircraft. For context, in early 2024, an incident involving a Boeing 737 Max 9 aircraft operated by Alaska Airlines led to an emergency landing following a mid-air scare. This incident, which involved a rapid loss of cabin pressure and resulted in the temporary grounding of the entire Boeing Max 9 fleet, which was followed by a directive by the Federal Aviation Administration (FAA) to do so for all US-based operators of the fleet. This caused significant operational disruptions for the airline. This included numerous flight cancellations, which inevitably affected the company’s stock price. The grounding of these planes, which are a significant part of Alaska Air Group’s fleet, has raised concerns about potential impacts on their first-quarter results for 2024 due to reduced traffic and operational challenges.

Thankfully for ALK, as of January 31 the FAA has approved an enhanced inspection for Boeing 737 Max 9 so the planes can return to service, however this does not fill me with confidence given the myriad of issues the aircraft type has had. This situation highlights the risks associated with a fleet that has a heavy reliance on a single aircraft type, especially when that type has regularly faced operational issues. The incident with the Boeing 737 Max 9 and the subsequent grounding reflect the vulnerability of airline operations to unforeseen technical problems, which can lead to immediate financial repercussions and affect investor confidence and for me, this is a factor that cannot be overlooked given the impacts to operations a long-term grounding of the type could cause and I urge investors to consider this risk particularly when weighing up an investment into ALK. Furthermore, this scenario underscores the inherent challenges in the airline industry, where safety concerns and fleet reliability can have a direct and immediate impact on business operations and financial performance.

Financial Analysis

As of Q4 2023, ALK has shown solid financial performance for the aviation industry. In my opinion, the rise in revenue from $4.9 billion in 2015 to 10.43 billion in the last 12 months (LTM) is solid. This corresponds to a CAGR of approximately 7.6%. The company’s Book Value Per Share (BVPS) has also seen a steady increase, moving from $19.26 in 2015 to $32.62. Despite the big decline due to Covid, BVPS has managed to CAGR at 6.0%. This suggests to me that the company has been effective in building its intrinsic value.

ALK’s Revenue Per Year (Author)

The Earnings Per Share (EPS) has been somewhat variable, peaking at $7.75 in 2017 and later falling to $1.83 LTM, although it is worth noting that EPS was -$10.72 in 2020 and has been slowly trending up since then. The management team has shown solid financial responsibility in my opinion, especially in their approach to managing debt, with the company’s total debt standing at $3.82 billion currently. I believe debt maturities over the next several years are manageable, with $286 million in principal due in 2024 and $343 million due in 2025.

When it comes to liquidity, the most recent quarterly data shows cash and short term investments of $1.79 billion which indicates to me that the company is in a good position to meet its short-term obligations.

For the near future, specifically the upcoming quarter, my expectation is that ALK will report earnings below their original forecast as a result of the disruptions caused by the 737 MAX issue. I expect that management’s guidance regarding the 7-point impact to first quarter capacity will be relatively accurate given that their assumption of the 737 MAX being grounded until the first week of February has more or less played out.

Looking beyond the next quarter, the management team expects that the EPS will be between $3 to $5 for 2024, this outlook assumes a $150 million negative impact from the fleet grounding. The EPS guide implies a flat to slightly improved result in 2024 versus 2023. For me I anticipate that Alaska Air Group will likely deliver at the lower end of the guidance given the turbulent start to the year in addition to the fact that I expect the 737 MAX will continue to cause issues for the business going forward, most notably in relation to the delivery of the 23 new 737 MAX aircrafts.

Overall, I’m mixed about ALK’s growth prospects, on the one hand you have the acquisition of Hawaiian Airlines which I anticipate will significantly boost revenue and expand the company’s market share whilst on the other hand you have the large exposure to the 737 MAX which could see another issue arise at any moment.

Valuation

In my opinion, valuation should be a comparison between the market capitalization and the underlying business fundamentals, including future earnings. One method I find useful for this is a DCF analysis. As of Q4, 2023, Alaska Air Group’s current LTM earnings per share is $1.83. For 2024 I have assumed an EPS of $3.25 which is towards the lower end of the company’s guidance. Using a growth rate of 7.6%, which is in line with historical performance for the remaining years, an EPS of $4.36 is projected by 2028.

Using an exit multiple of 16, which is based on what is reasonable for the airline in a stable, pre-covid economic environment over the past decade, the estimated price target for the stock in five years would be $59.86. Therefore, if you invest in ALK at its current share price, the expected CAGR would be about 10.5% over the next five years, based on these calculations. It should be noted that this 10.5% stock price CAGR assumes that we face no major economic headwinds that would affect travel demand for the next 5 years as well as no further disruptions from the 737 MAX or any other aircraft type the company operates. Obviously, the return will be worse if something unforeseen happens to the economy. Based on the DCF analysis, I believe that Alaska Air Group is a hold at current prices.

ALK DCF Analysis (Author)

Conclusion

The potential merger between Alaska Air Group and Hawaiian Airlines shows promise for expanding the market, improving services and driving growth. However, there are concerns about the risks associated with the Boeing 737 MAX fleet. These risks have already impacted Alaska Air Group’s stock price as well as factors such operational efficiency and passenger capacity. Despite these challenges a DCF analysis suggests that ALK may offer a return of 10.5% indicating that it might be wise to hold onto the stock for now. This analysis assumes growth without a major economic downturn or further issues related to the 737 MAX. I think situation at Alaska Air Group currently highlights the importance of the balance between promising opportunities, from merging with Hawaiian Airlines and the inherent risks of operating in the aviation industry.

Q2 2024 Earnings Call Transcript")