turbo83/iStock Editorial via Getty Images

Investment thesis

Alaska Air Group (NYSE:ALK) is demonstrating a strong recovery with stable consumer demand and strategic fleet management, despite facing increased competition and higher-than-expected hiring costs. The company’s proactive adjustments to its fleet delivery schedule and effective cost management highlight its resilience. Additionally, the potential acquisition of Hawaiian Airlines could enhance ALK’s market presence in a key region, supporting long-term growth.

Q1 earnings review

We’ve previously published several articles on Alaska Air Group. The last one available was published in February 2024

Q1 results missed our expectations due to higher hiring pace:

- Revenue for Q4 totaled $2 232 mln (+1.6% y/y), in line with our forecast of $2 265 mln and consensus of $2 180 mln.

- EBITDA totaled ($6) mln, down from our forecast of $51 mln. The difference was driven by a hiring pace that surpassed our expectations (23 thousand people versus the estimate of 22 thousand people).

Otherwise, operating and financial data met our expectations. Alaska showed some signs of recovery, despite some of the key flight destinations to Hawaii are still distressed, while the competition on domestic market increased due to higher fleet capacity:

- ASM (capacity) totaled 15 378 (-2.1% y/y)

- Load factor was 81.44%, which was slightly higher than average pre-COVID Q4 level

- Passenger Yield was ₵16.01 (+1.3% y/y). Also management has noticed rising further tariffs and showed confidence during the conference call.

Yields have a support, despite rising competition in the industry

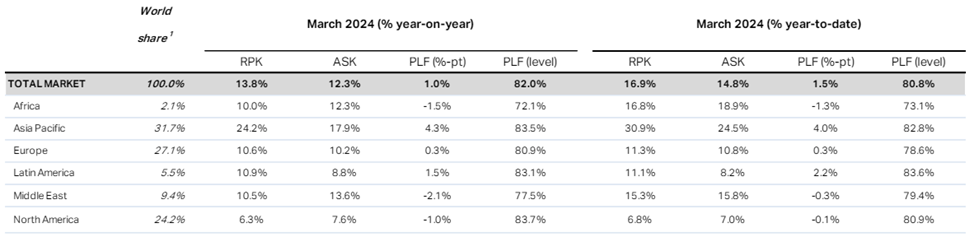

The situation continued to improve for air carriers in 1Q 2024, despite rising competition in the industry. The management of Alaska Air Group, as well as managers of other airlines (UAL, AAL, etc.) note consumer stability and see good demand, which allows them to maintain airfare increases. Bookings of tickets for late dates remain stable, which confirms the thesis of consumer confidence.

We earlier expected competition to be more intense this year as the capacity of US airlines started to exceed existing traffic.

IATA

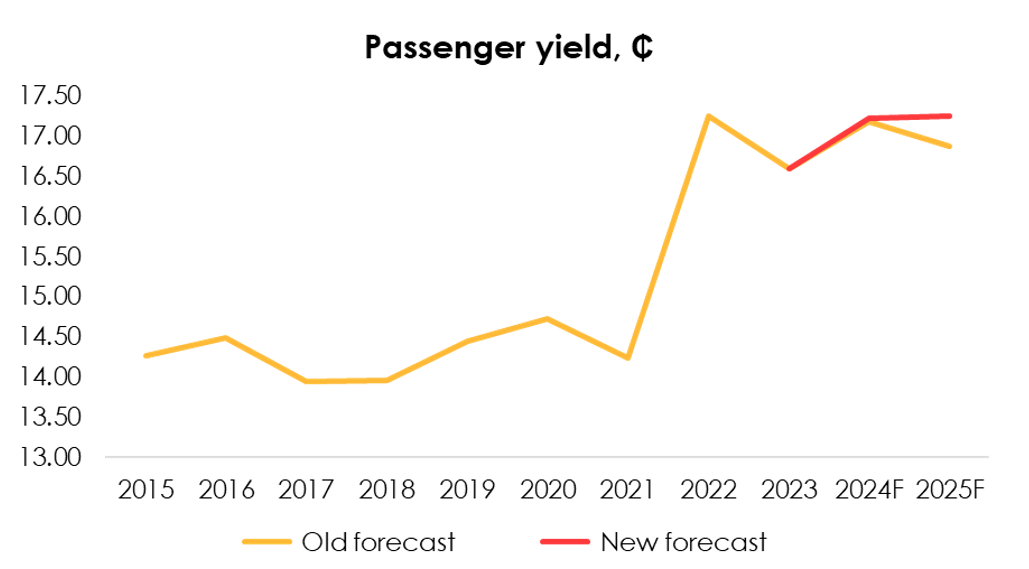

However, we see it doesn’t put significant pressure on booking prices of future flights, which led us to raise the forecast for ALK’s yield per revenue passenger mile from ¢17.19 (+3.5% y/y) to ¢17.23 (+3.7% y/y) for 2024, and from ¢16.87 (-1.8% y/y) to ¢17.26 (+0.2% y/y) for 2025.

Invest Heroes

Boeing’s technical issues didn’t make a significant impact either on the company’s reputation or its finances as the losses from the emergency landing of the 737-9MAX were fully compensated by the supplier, and all the models with identical specifications have already returned to operation following additional inspections.

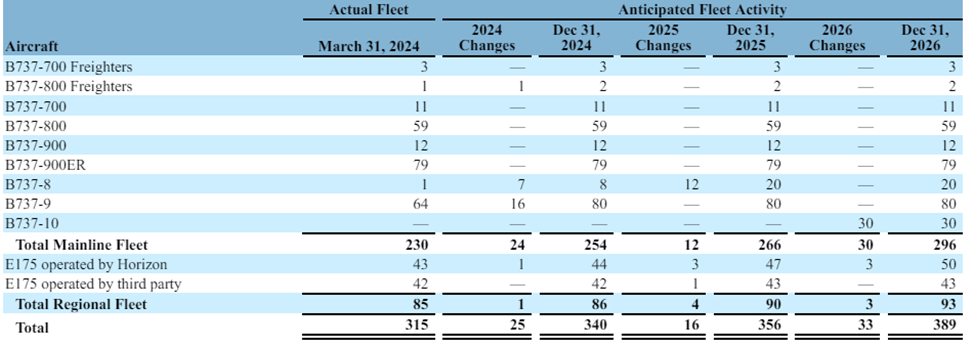

However, Alaska Air Group canceled the delivery of one Boeing 737-9 MAX airplane in 2024 and moved back the delivery of 11 737-10 MAX planes from 2024 to 2025.

Alaska Air Group

Amid accelerated hiring, we saw heightened utilization of active fleet, with the metric reaching 29.9% of the theoretic level, up from the forecast of 28.9%. Amid accelerated hiring and the postponement of deliveries of some airplanes, we have slightly raised the forecast for the utilization of the existing fleet (on average by 1.5% from the theoretic maximum level for 2024 and by 1% for 2025).

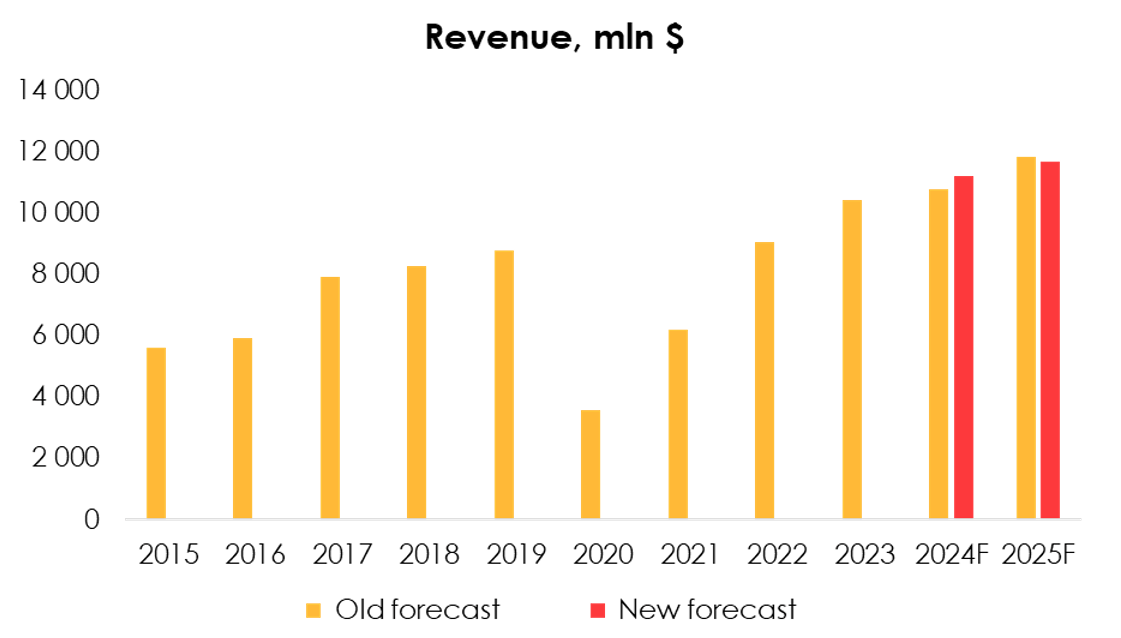

Given the changed schedule for airplane deliveries, the increased forecast for airfares, and the higher forecast for fleet utilization, we are raising the revenue forecast from $10 763 mln (+3% y/y) to $11 207 mln (+7% y/y) for 2024, but are lowering it from $11 825 mln (+10% y/y) to $11 671 mln (+4% y/y) for 2025.

Invest Heroes

Cost structure remains mixed, still allowing to deliver positive margins

From the perspective of costs, we see both positive and moderately negative factors:

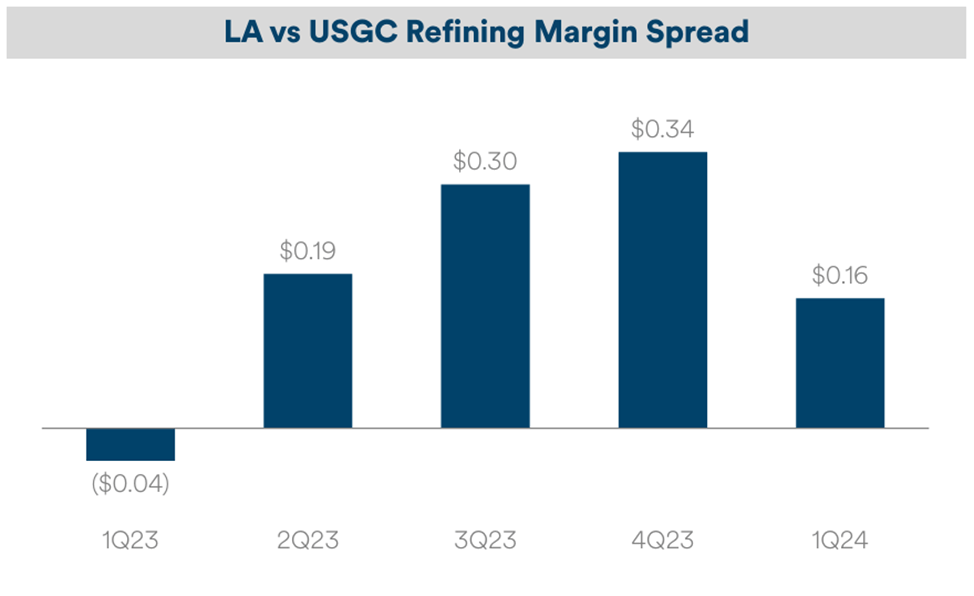

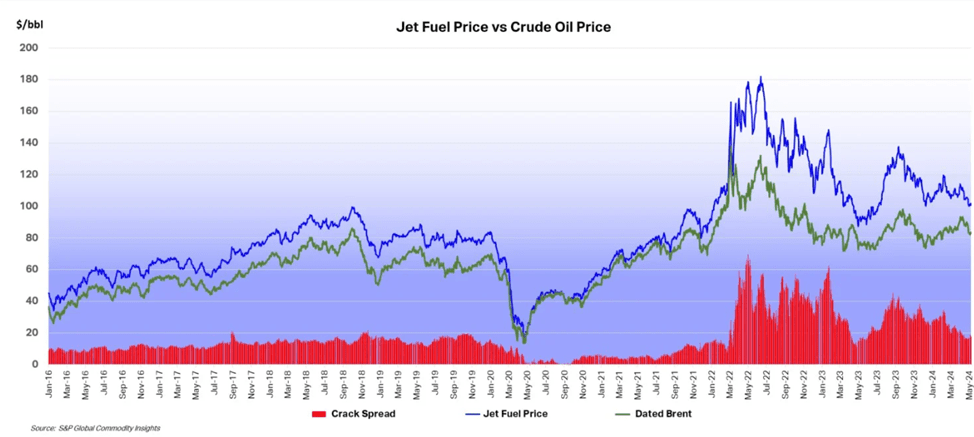

Crack spreads continued to decline, as expected. Of particular importance was the fact that the difference between crack spreads on the US West and East coasts fell by more than 50% q/q. We assume that most of refinery maintenance work in the region was completed and crack spreads will normalize by the end of this year.

Alaska Air Group IATA

However, we updated the outlook for Brent oil price, which caused a slight increase in the forecast for fuel prices in 2024 from $2.99/gallon (-7% y/y) to $3.07/gallon (-4% y/y).

Also, amid accelerated hiring, we have raised the forecast for payroll expenses from $3 201 mln (+5.3% y/y) to $3 494 mln (+14.9% y/y) for 2024 and from $3 678 mln (+14.9% y/y) to $3 698 mln (+5.9% y/y) for 2025.

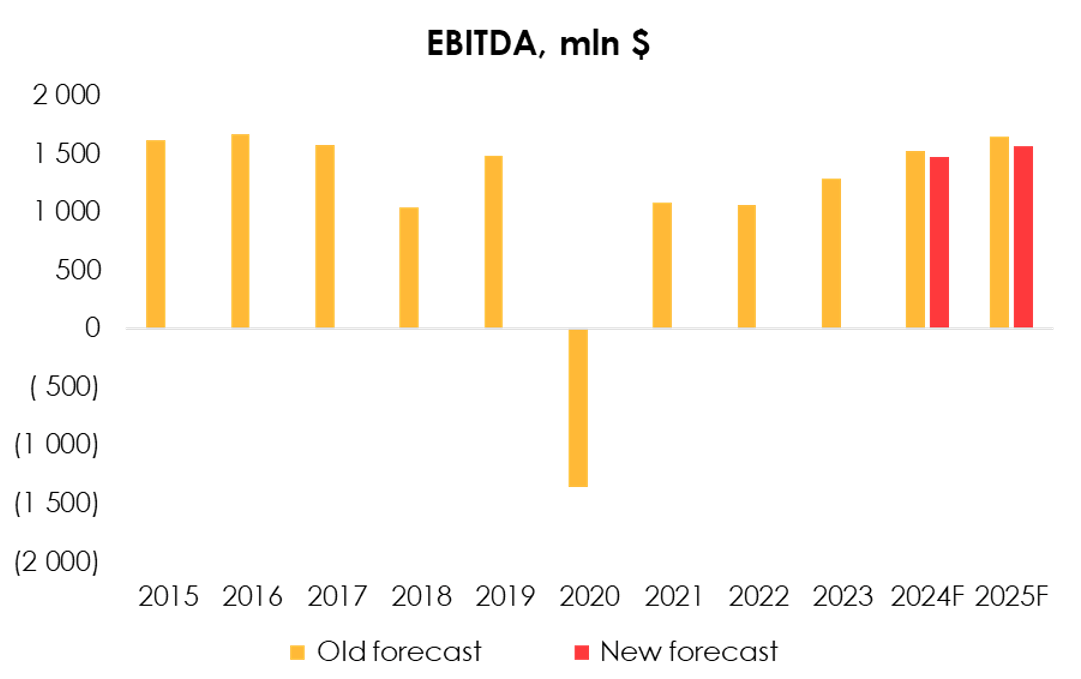

Given the revised revenue outlook, and the increased forecast for operating costs, we are lowering the EBITDA forecast from $1 526 mln (+19% y/y) to $1 474 mln (+15% y/y) for 2024, and from $1 645 mln (+8% y/y) to $1 568 mln (+6.4% y/y) for 2025.

Invest Heroes

The outlook for financial results does not include a potential acquisition of Hawaiian Airlines. The deal is still under review by the US Department of Justice, with a deadline for a decision set for August 5.

We believe that the probability of regulatory approval in this case is higher than in the JetBlue-Spirit deal, as the combination would achieve market domination only in one US region: Hawaii (about 51% of the combined company’s capacity). At the same time, Hawaii has still not recovered from last year’s Maui fires, even though the destination was opened for tourists, with tourism generating about 70% of the region’s gross revenue. Given the stress that befell Hawaii, it would make sense for the regulator to support the industry by approving the deal.

Valuation

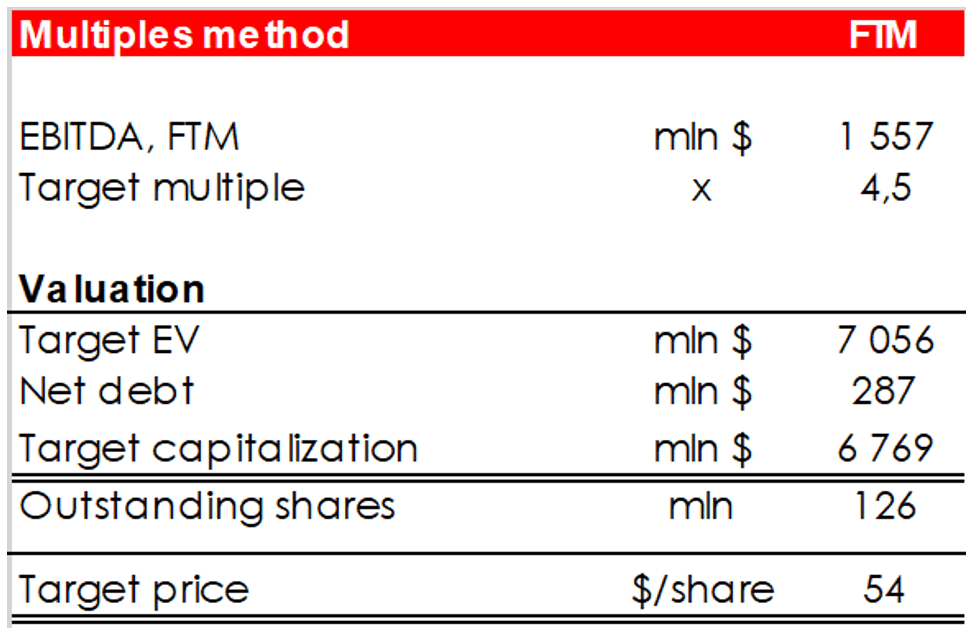

We’re evaluating ALK fair stock price based on FTM EV/EBITDA multiples method.

We are raising the target price of the shares from $49 to $54 due to:

- the reduced EBITDA forecasts for 2024 and 2025 (-$3 from the valuation);

- net debt falling from $744 mln to $287 mln (+$4 to the valuation);

- the shift of the FTM valuation period (we earlier included the period from 1Q 2024 through 4Q 2024 into the forward 12 months EBITDA forecast, while now the forecast period runs from 2Q 2024 to 1Q 2025). (+$4 to the valuation).

The target price is $54. Based on the new assumptions and the limited upside, we are lowering the rating for the shares to HOLD.

Invest Heroes

Risks

We believe that Alaska Air Group is positioned well due to fully domestic exposition, but yet is a subject to several systematic & unsystematic risks, just as any other airline company:

- Jet fuel price remains the biggest expense account for the company. Though we’re seeing positive momentum and expect crack spreads to decrease in the middle-term, unexpected oil price increases, refineries lay-ups or maintenances may significantly influence ALK’s business.

- Airplane breakdowns are another unpredictable major risk factor. Though ALK’s fleet has recently gone through several inspections, there’s always a small probability something could go wrong once again.

- Airfares, being a major revenue source, are one of the most significant aspects for an airline business. Its dynamics creates both upside and downside risks for Alaska Air Group. One the one hand, fleet capacity in the US is already exceeding pre-COVID levels and creates a procompetitive environment. On the other hand, executives of different air transportation companies note a positive momentum in bookings and further passenger yields. Given moderate business profitability, passenger yield dynamics may significantly affect financials and implied target share price.

Conclusion

Alaska Air Group is our favorite in the airline sector due to low debt burden and clear business growth plan. Despite in the near term business may trail behind other airlines due to full exposure on domestic market and crack-spreads volatility, we believe overall company is well-positioned in the long term.

To manage the position, we suggest keeping an eye on ALK and its peers financials & industry research (e.g., IATA and FAA).

Q2 2024 Earnings Call Transcript")