eternalcreative

Alarum Technologies Inc (NASDAQ:ALAR) reported its latest quarterly results capping off a transformative year for the Israel-based software company. A decision to exit the cybersecurity business and other non-core segments in 2023 to focus on its “NetNut” web data collection platform has paid off evidenced by sharply higher sales and profitability. The introduction of new artificial intelligence-based tools has represented a new growth driver.

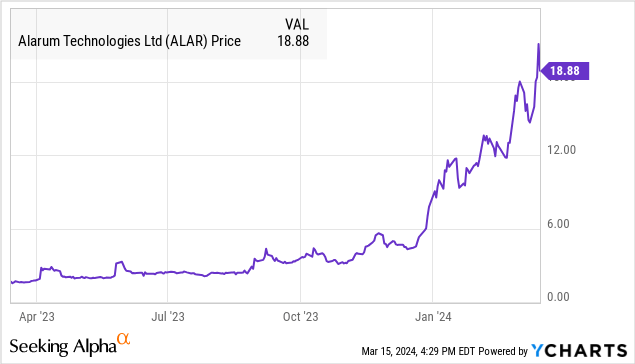

The company with a market cap of just $120 million is still tiny, but proving it has some real value supported by impressive operating trends and solid fundamentals. Shares of ALAR are up more than 1,100% over the past year and deserve a closer look.

ALAR Financials Recap

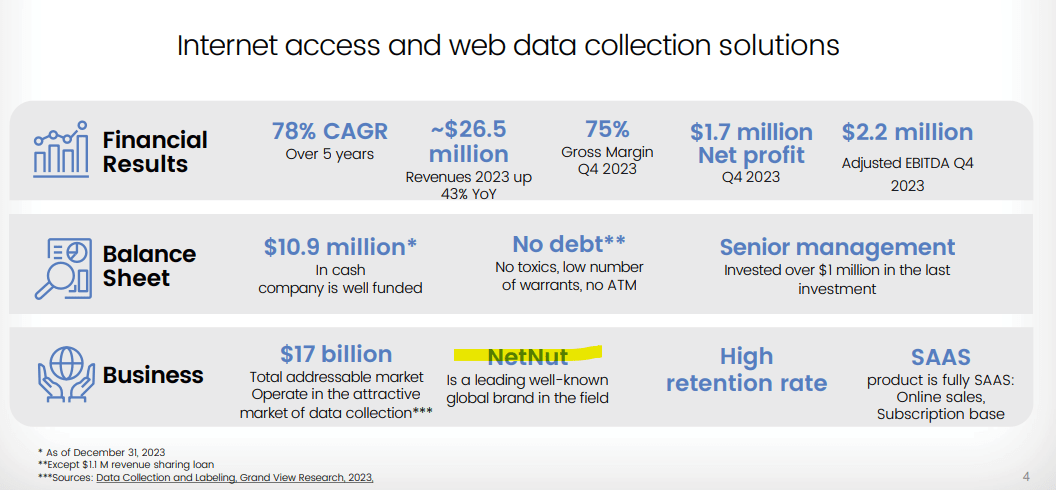

ALAR reported Q4 net profit of $1.7 million, reversing a loss of -$2.9 million in the period last year. Revenue of $7.1 million, climbed by 38% year-over-year, and also sequentially higher from $6.75 million in Q3. Full-year revenue of $26.5 million was up 43% y/y.

source: company IR

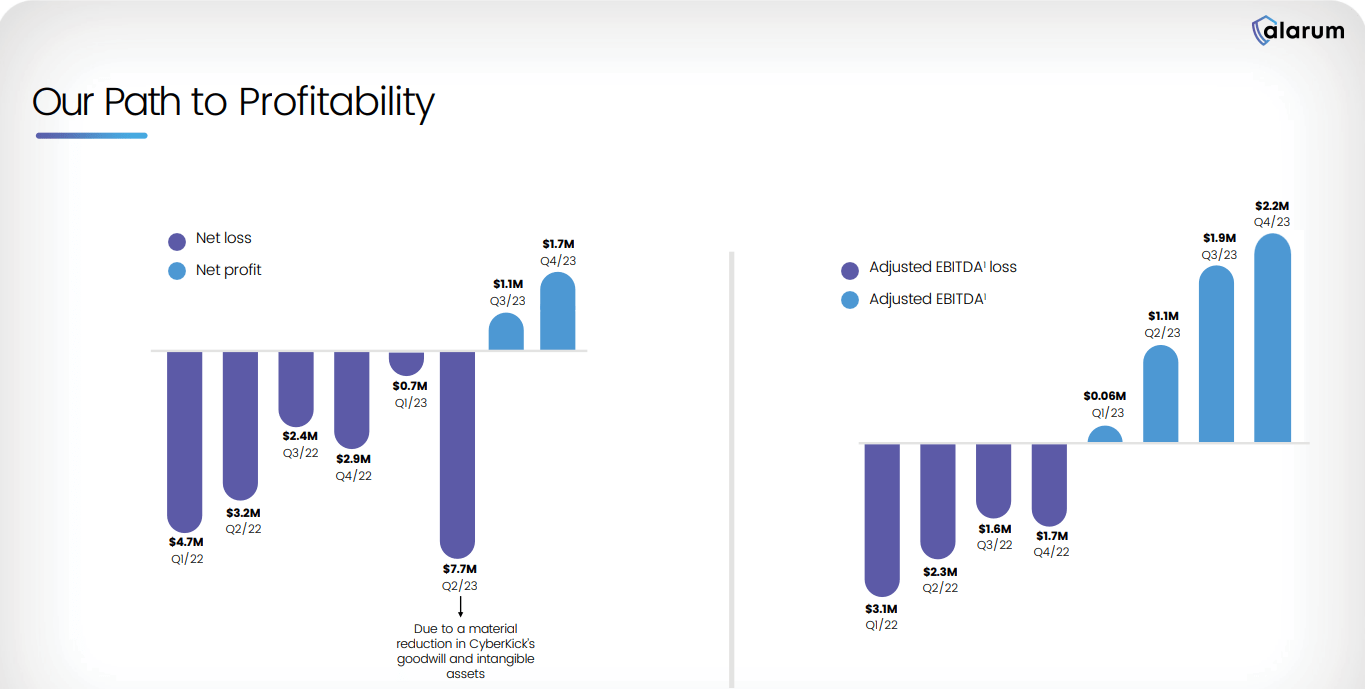

This was the second consecutive quarter of profitability with net income of $1.7 million climbing from $1.3 million in Q3. For the full year, there was a large write-off related to the “CyberKicks” divestiture and accounting charge on goodwill in Q2 dragging lower the results. Nevertheless, 2023 adjusted EBITDA at $5.2 million has climbed sequentially for the past four quarters, including $3.2 million in Q4 highlighting the underlying earnings momentum.

source: company IR

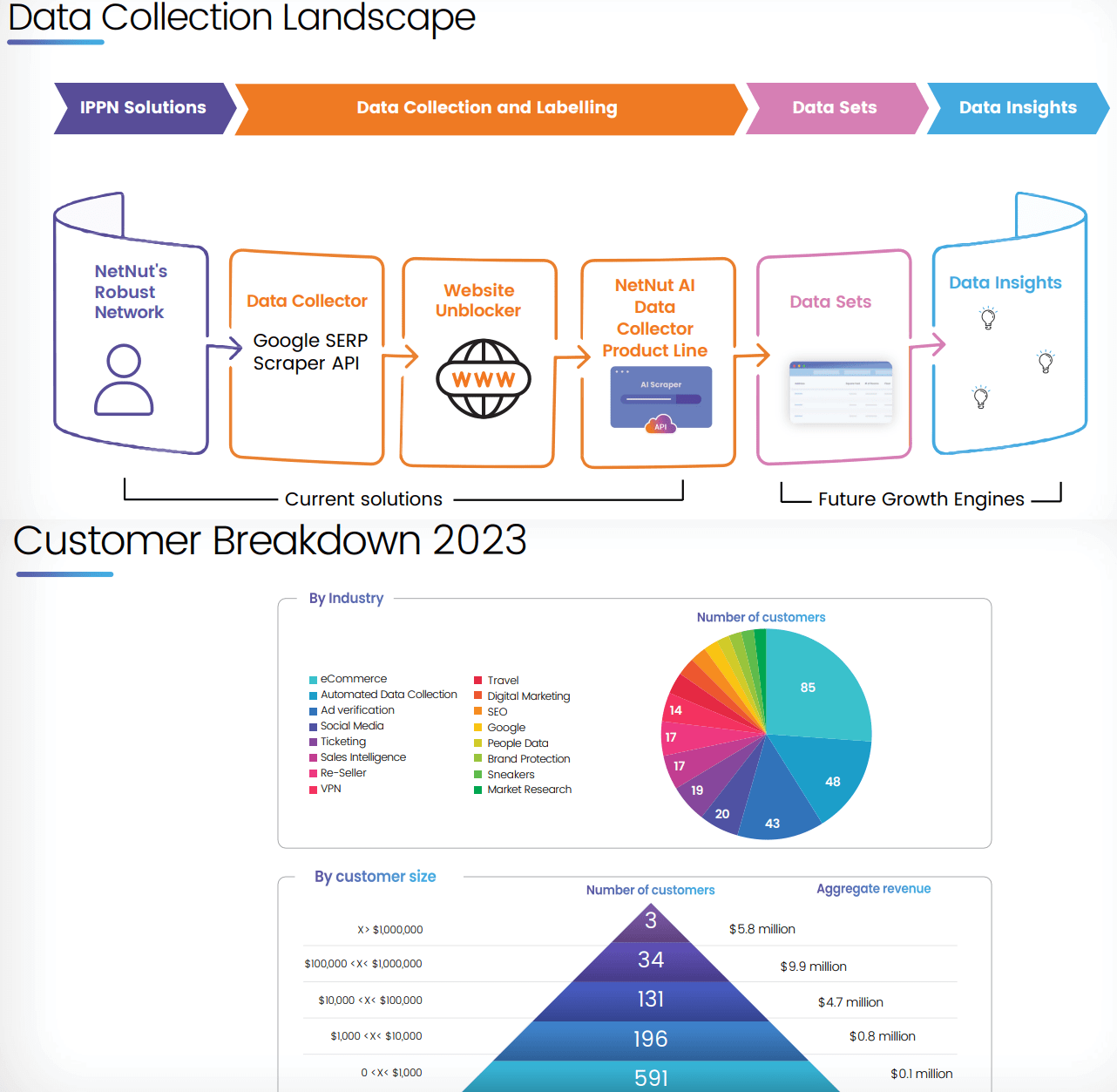

We mentioned the strong growth story. NetNut full-year revenue of $21.3 million representing 80% of the overall business climbed by 150% y/y. By this measure, the underlying trends are even stronger than the headline measures suggest considering NetNut is now the primary focus.

Part of that NetNut surge reflects the launch of new products including a SERP Scraper API while gaining new customers in the fintech market. Management notes that AI features have received a positive response.

The metric that stands out is the net retention ratio which reached 153% this quarter, up from 144% in Q3. The interpretation here is that existing customers are spending more on various tools offered, well beyond the impact of regular churn.

For context, the target market for Alarum are web-based businesses that need to collect analytics on traffic trends or customer insight. In terms of use cases, the types of tools offered include advertising verification, brand protection, search engine optimization (SEO) monitoring, and web data extraction.

source: company IR

One example that explains the value proposition considers how websites often need to present a different landing page and even pricing options depending on where users are geographically located. NetNuts’s Internet Protocol Peering Networks (IPPN) tool can navigate the web as a simulated user which is an important aspect of competitor analysis.

We find that Alarum has relatively good diversification by industry covering eCommerce customers, social media sites, and ticketing platforms among others. While the majority of accounts contribute less than $1,000 a year in revenue, 37 customers are noted as driving more than $100,000 in annual sales, including 3 clearing more than $1 million.

Finally, we note ALAR ended the year with $11 million in cash against zero debt. We view the balance sheet as a strong point of the company’s investment profile. While not offering official financial guidance for 2024, comments during the earnings conference call projected confidence that the trends can continue with optimism for the year ahead.

What’s Next For ALAR?

With a current market cap of around $110 million, Alarum Technologies is in the micro-cap category but an outlier to any negative connotation that classification carries based on the latest trends. The attraction here is that when we put the numbers together, it’s clear to us that ALAR is more than just a speculative “penny stock” or climbing simply due to AI hype.

Annualizing the Q4 earnings to $6.8 million or adjusted EBITDA to a run-rate of $8.8 billion, ALAR is trading at an implied forward P/E around 17x or 12x as an EV to forward EBITDA multiple. In our view, these multiples are very attractive for a company that just delivered 43% revenue growth over the past year. A baseline here is that the company can at least grow sales by 20% in 2024.

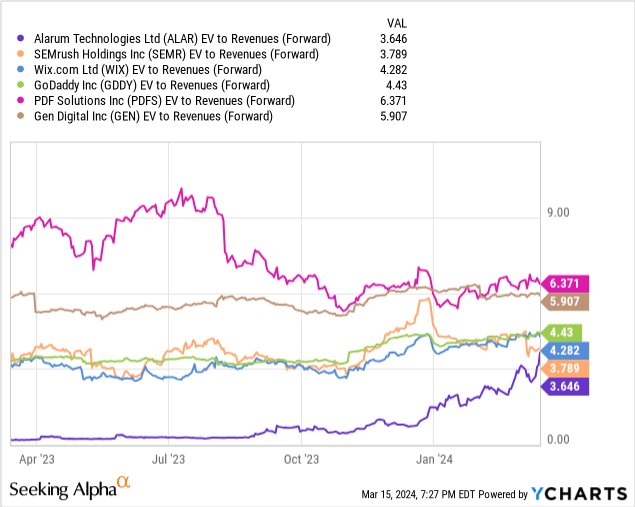

Notably, ALAR’s EV-to-revenue multiple of 3.6x remains below the average closer to 5x for a group of what we would consider to be comparable internet access, web data services providers including SEMrush Holdings Inc (SEMR), Wix.com Ltd (WIX), GoDaddy Inc (GDDY), PDF Solutions Inc (PDFS), and Gen Digital Inc (GEN).

Naturally, Alarum with its significantly smaller scale warrants some level of small-company discount but we simply don’t see anything to suggest the stock is materially overvalued or a “bubble” even after rallying 140% YTD.

On the other hand, the caution we have is that this segment of online tools aimed at internet website developers can be fragile in terms of facing the competitive environment.

Management comments during the earnings conference call noted its patents in the field as well as established relationships as representing barriers to entry. There is also an aspect of high switching costs for customers attempting to transition to a different product.

Still, it’s an aspect of a company this size that needs to be considered within the risk backdrop. With a critical eye, we would also cite the limited number of large customers driving more than $1 million in annual revenue as a weak point, in a scenario where Alarum loses a contract for any number of reasons that would have an outsized impact on quarterly results.

Final Thoughts

We rate ALAR as a buy, with a sense that the stock remains under the radar, and has room to capture an expansion of valuation multiples going forward as the next several quarterly earnings confirm the financial momentum. Monitoring points through 2024 include trends in the gross margin, posted customer net retention ratio, cash flow, and adjusted EBITDA.

We already covered some of the risks to consider, but we’ll add to that with an expectation for shares to remain volatile and sensitive to shifting growth expectations. A broader market-wide selloff or weakness in the tech sector has the potential to push shares lower.

Q2 2024 Earnings Call Transcript")