J. Michael Jones

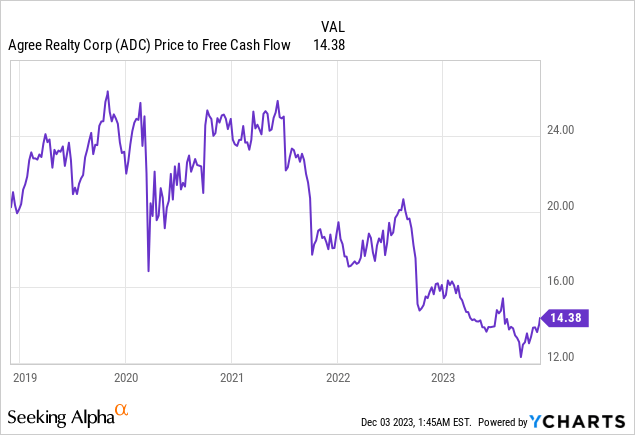

I’ve bought the common shares of Agree Realty (NYSE:ADC) on the back of its growing monthly dividend distributions, its BBB-rated investment grade balance sheet, and the upcoming positive outlook for Fed interest rate cuts. 2023 has not been great for common shareholders with ADC down 15% year-to-date in response to the Fed funds rate being hiked to a 22-year high at 5.25% to 5.50%. This has seen the REIT’s multiple to its free cash flow halved from 2021 highs. Despite recent comments from Powell, the Fed is more than likely done with encourage interest rate hikes with the CME’s 30-Day Fed Funds futures pricing data now placing a 25 basis points cut as the most likely outcome of the 20 March 2024 FOMC meeting. While this is likely too dovish and expectations for a cut in the first quarter of 2024 will likely be reduced, 2024 stands to see an inversion of a status quo in place since 2022 that has seen REITs suffer a sustained flight of investor capital to competing safer investments. CDs currently offer rates of up to 5.75%.

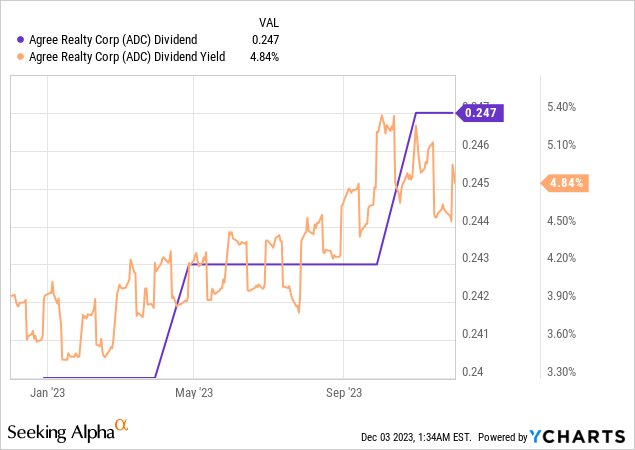

ADC last declared a monthly cash dividend of $0.247 per share, unchanged from its prior distribution for what’s currently a 4.9% annualized forward dividend yield. The current distribution is up 2.9% from a year ago. A recovery of this multiple looks likely as 2024’s base case. To be clear, ADC just bounced off 52-week lows from broader macro expectations that the Fed is done with rate hikes. This dynamic will continue to form the main driver for the direction of REITs until interest rates standardize from current highs. I last covered the ticker in September when sentiment towards the outlook for interest rate cuts was still somewhat negative on higher for longer mantra.

Yield, Growth, And Stability

Agree Realty December 2023 Presentation

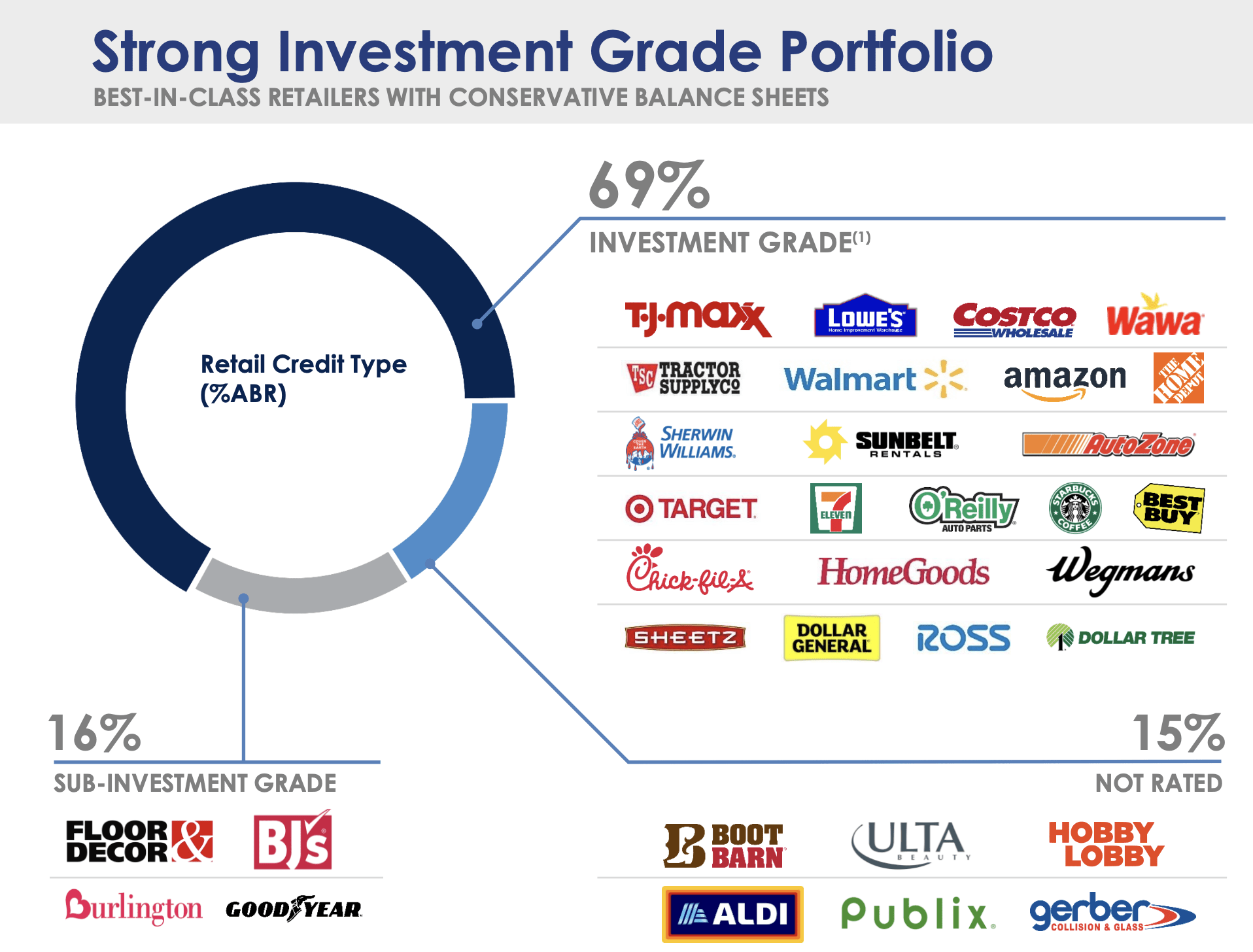

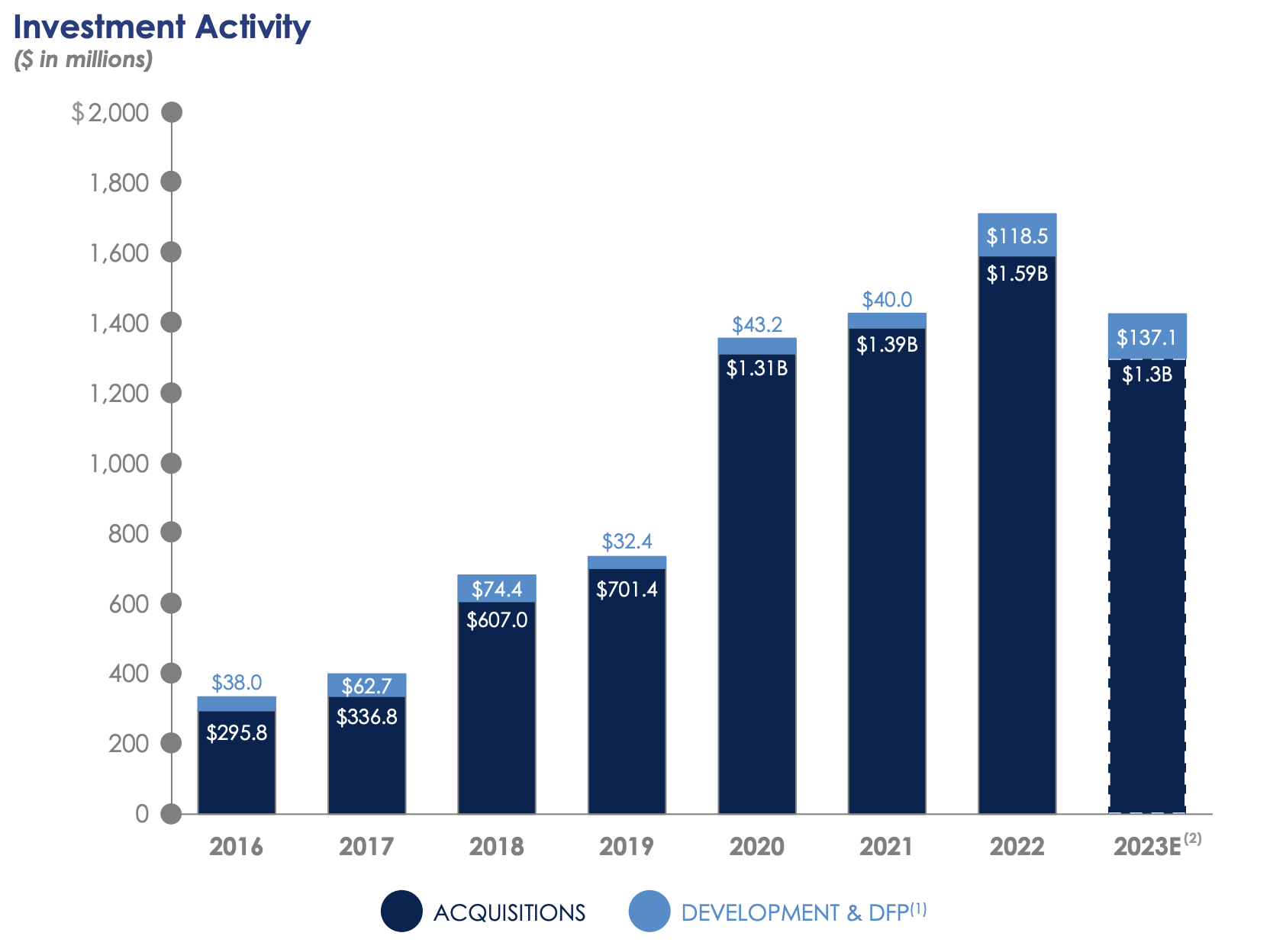

ADC had a terrific fiscal 2023 third quarter with revenue of $136.81 million up 24.3% over its year-ago comp and a beat by $1.84 million on consensus estimates. This was driven by strong investment activity with ADC set to push through $1.3 billion in investments this year. The REIT’s portfolio consisted of 2,084 properties across roughly 43.2 million square feet of gross leasable area at the end of the third quarter. This was 99.7% leased with a weighted average remaining lease term of roughly 8.6 years and with 69% of annualized base rents being derived from tenants rated investment grade.

Agree Realty December 2023 Presentation

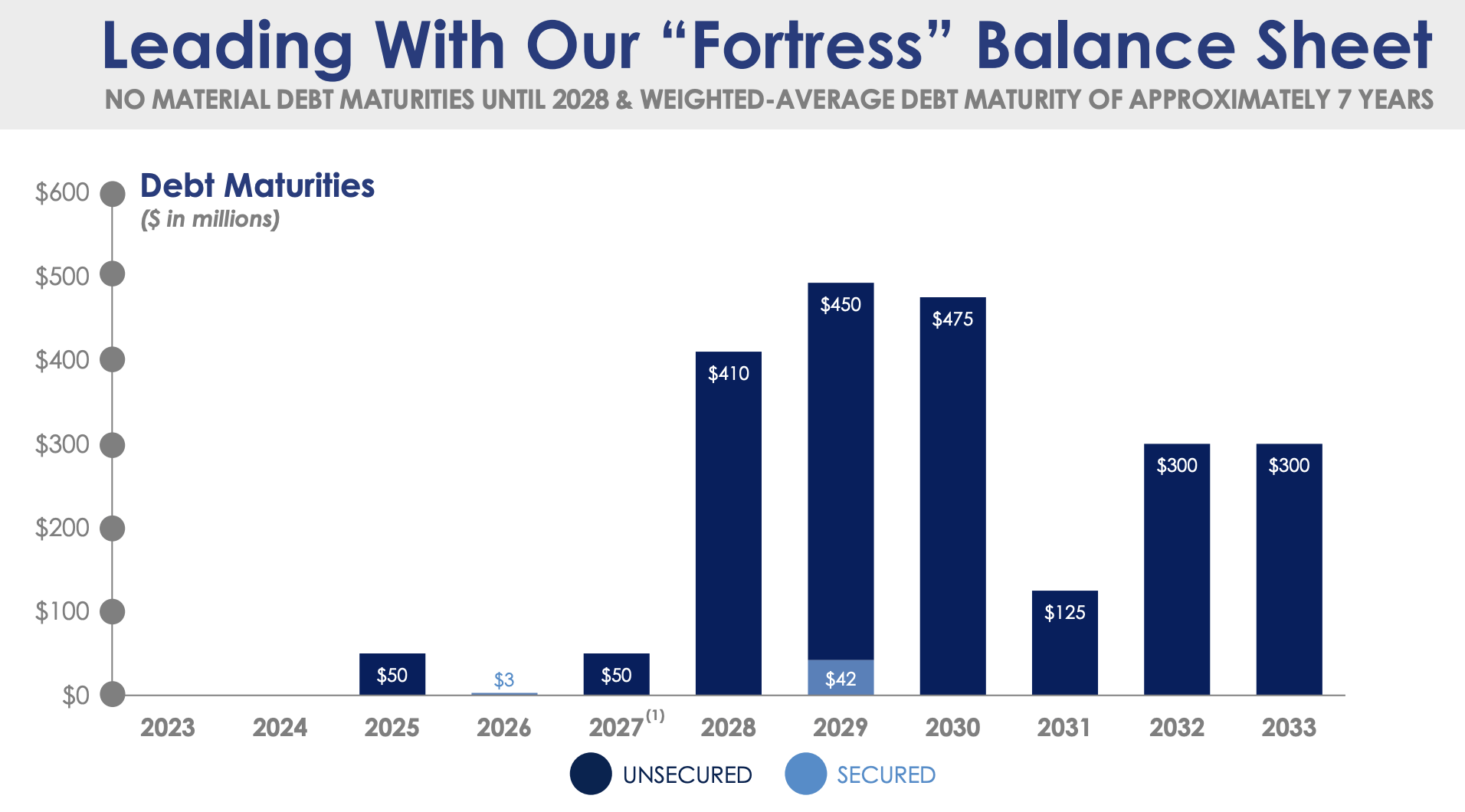

ADC’s core FFO per share at $1 meant the 3-month aggregate of the dividend is being 135% covered, a roughly 74% payout ratio. encourage, FFO per share grew by 4 cents from its year-ago comp with this set for encourage gains on the back of what’s been quite intense acquisition activity. Third-quarter property acquisitions at $398 million came with a weighted average cap rate of 6.9%. ADC’s balance sheet and near-term maturities are also extremely strong with no debt maturities coming due next year and only $53 million coming due from 2025 to 2026.

Agree Realty December 2023 Presentation

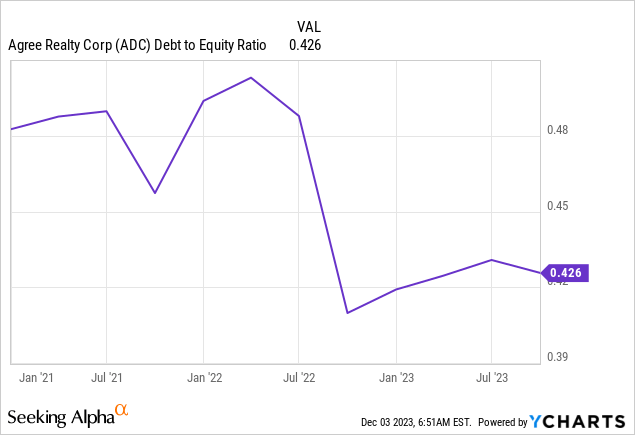

Critically, ADC’s extremely long-dated maturity profile and its low leverage mean stability against the specter of a recession and have meant the REIT being able to follow acquisitions even through a period where interest rates have been hiked to near-term highs. ADC’s debt-to-equity ratio at 0.43x is prudent especially when coupled with its investment grade rating and low payout ratio. The dividend is likely set for another near-term hike with total returns set to get a boost from the upcoming dovish pivot.

The Monthly Paying Series A Preferreds

QuantumOnline

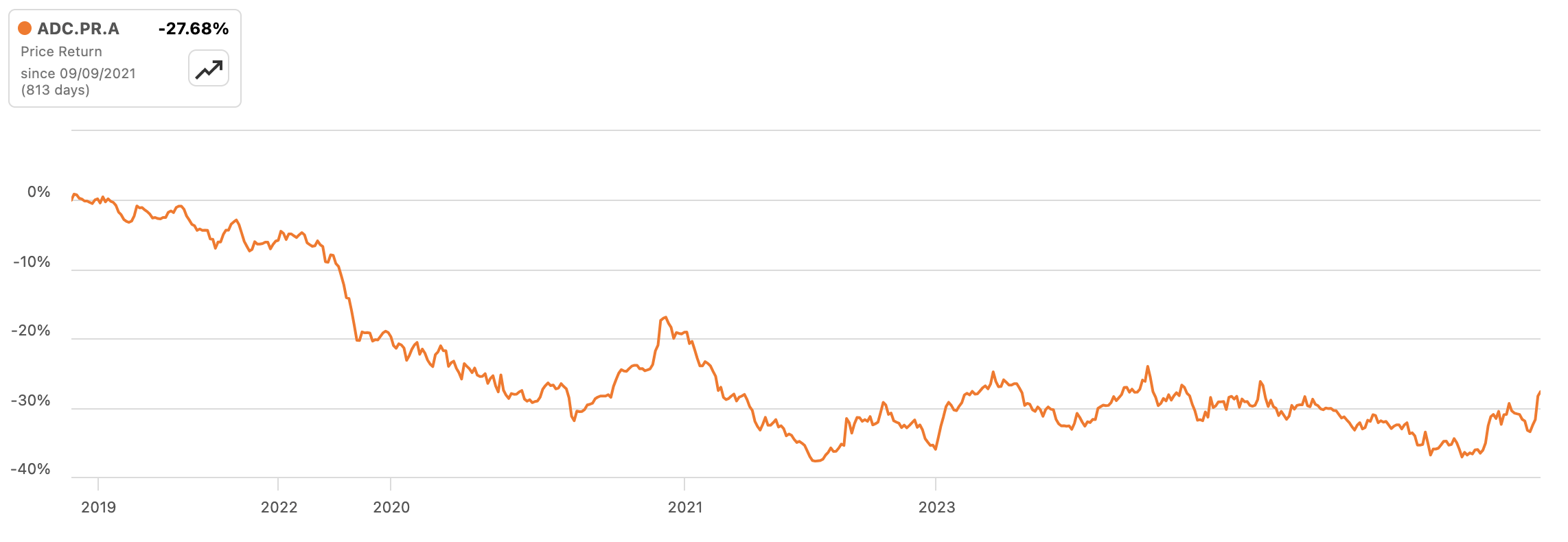

I’ve so far been buying Agree Realty 4.250% Series A Preferred Shares (NYSE:ADC.PR.A). These offer a $1.0625 annual coupon for what currently works out to be a 5.83% yield on cost, around 90 basis points more than the commons. The coupon is also distributed monthly on the first day of the month. Whilst the preferreds will have less upside than the commons, the appeal is their current discount to par. These are currently trading hands for $18.21 per share, a roughly 27% discount to their $25 per share par value. Hence, there is around $6.79 in potential capital gains upside to be captured on a gradual drift back up to par if inflation continues to fall back to the Fed’s 2% target to set the backdrop for rate cuts.

Seeking Alpha

They’re coming up for redemption just under 3 years from now on 17 September 2026 with the yield to redemption at 15.6%. ADC has no other outstanding preferred shares with the Series A issued in 2021 when ZIRP was still in vogue and inflation was meant to be transitory. Hence, redemption would likely only happen on the back of a return to ZIRP. Interest rates would also likely have to dip below the headline coupon rate for the preferreds to proceed back to par fully. I’m rating both securities as a buy and will start to build a position in the commons later this month.

Q2 2024 Earnings Call Transcript")