coldsnowstorm

I upgraded AGNC Investment (NASDAQ:AGNC) back in June, saying that with the Fed tightening cycle likely coming to an end now was the time to start accumulating shares. Including dividends, the stock has generated an over 5% return since then. Let’s catch up on the name after its recent earnings report.

Company Profile

As a refresher, AGNC is mortgage REIT that primarily derives its income from the spread between the interest it earns on the mortgage-backed securities (MBS) it holds and its borrowing costs. The firm will also use leverage to increase its return.

It primarily invests in MBS backed by Fannie Mae, Freddie Mac, and Ginnie Mae, which come with essentially no credit risk, as these agencies backstop the mortgages. Non-agency residential mortgage backed securities (RMBS), commercial mortgage backed securities (CMBS), and credit risk transfer (CRT) securities represent a small portion of its portfolio.

At the end of Q3 2023, AGNC’s investment portfolio was valued at $60.2 billion, with $58.3 billion of that in Agency MBS and $5.4 billion in TBA (to be announced) securities. Nearly 94% of its portfolio was in 30-year fixed rate MBS and TBA securities at quarter end.

The Turn Begins

The main story throughout much of 2022 and 2023 for AGNC and other mortgage REITs was the continued pressure on tangible book value (“TBV”). This was caused by a combination of increasing interest rates, as well as the spread between Treasuries and MBS increasing. As new MBS are issued at high coupons, this causes the older MBS in a mortgage REITs’ portfolios to be repriced lower in order for the yields to be similar to that of current issued MBS.

Company Presentation

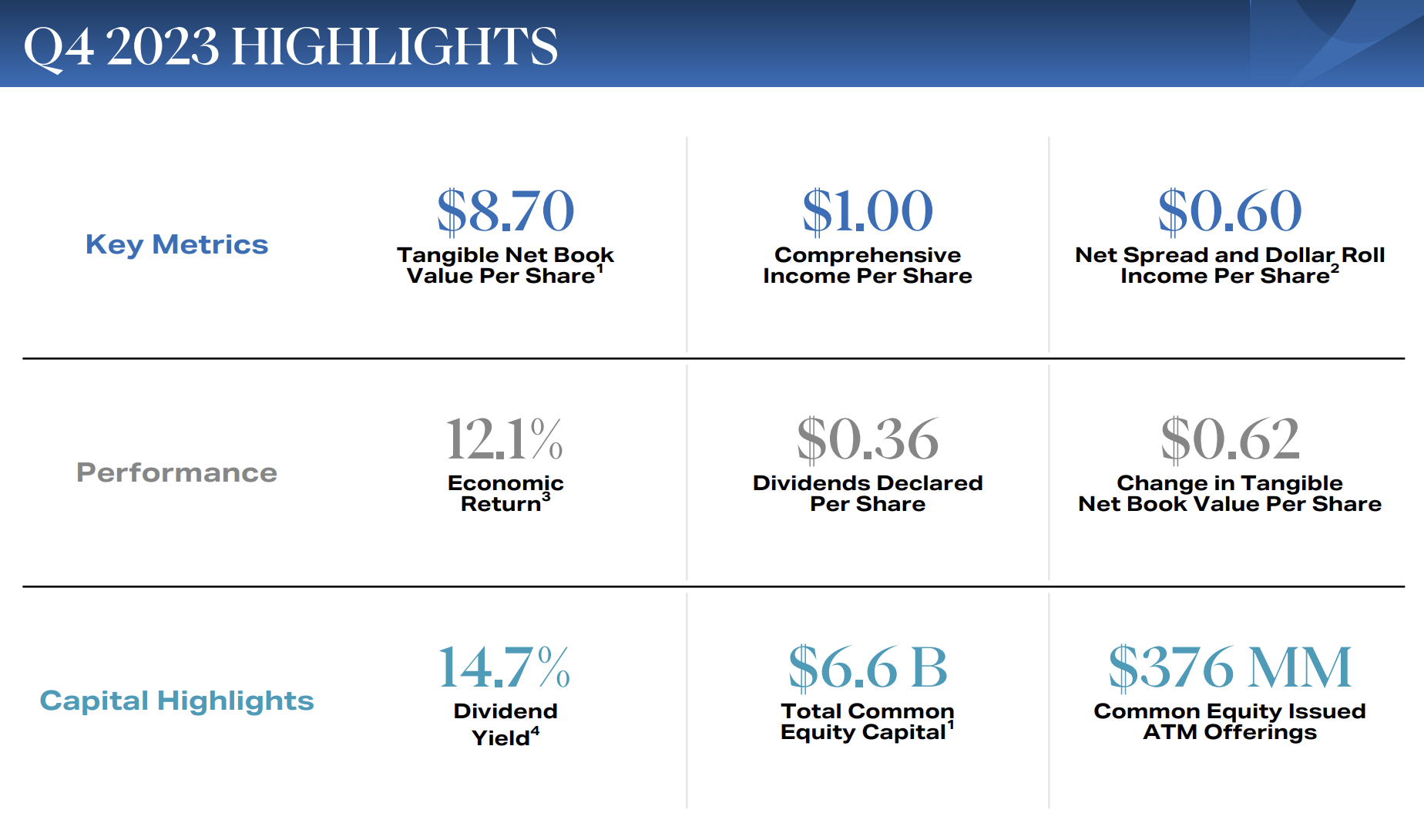

As a result of this pressure, AGNC saw its TBV go from $15.75 at the start of 2022 down to $8.08 at the end of Q3 2023. That was a massive -49% drop. Given that mortgage REITs generally trade at a multiple to their TBV, it is no surprise that the AGNC’s stock has had a difficult two years.

With the Fed signaling in December that it will shift policy and look to cut interest rates three times in 2024, however, the rates for mortgages began to decline. As a result, AGNC saw its TBV increase nearly 8% sequentially to $8.70 from $8.08.

Notably, AGNC issued $376 million in common stock during the quarter through its ATM program. While issuing stock is dilutive and generally viewed as a negative for most industries, when a mortgage REIT issues equity above book value it actually helps increase its book value. AGNC was able to issue the shares when its stock was trading well above TBV per share.

Meanwhile, AGNC was able to continue to get solid spreads in Q4. It had a 3.08% average net interest spread in the quarter. That compares to 3.06% a year ago and 3.03% in Q3. Two years ago its average net interest spread was 2.74%. So on that front, AGNC has been doing a great job, highlighted by its hedging, which has been able to keep its funding costs down. This is one area where AGNC continues to shine.

Overall, AGNC generated 60 cents per share in net spread and dollar roll income. It generated a 12.1% economic return of its tangible common equity, with its TBV rising 62 cents per share and it paying out 36 cents in dividends during the quarter.

AGNC ended the quarter with 7.0x tangible net book value “at risk” leverage. That compares to 7.4x at the end of 2022 and 7.9x at the end of Q3.

Not surprisingly, AGNC management was much more bullish on its Q4 earrings call than it has been over the past couple of year. On its call, CEO Peter Federico said:

“As we begin 2024, we believe the investment outlook for Agency MBS is decidedly more favorable than the previous 2 years. This positive outlook is supported by historically attractive valuation levels on both an absolute and relative basis. Low mortgage origination volumes, declining interest rate volatility, a less inverted yield curve and most importantly, a more investor-friendly monetary policy stance by the Federal Reserve. Our favorable outlook for Agency MBS is further supported by several important developments. First, in the fourth quarter, the Fed adopted a more neutral monetary policy stance as inflation measures continue to show progress toward the Fed’s long-run target. More significantly, at the December meeting, the Fed also indicated that multiple rate cuts were possible in 2024, assuming inflation measures continue to improve as expected. Second, interest rate volatility is poised to decline. Over the last 2 years, the distribution of potential interest rate path has been exceedingly wide, due to the many uncertainties associated with inflation, the economy, regional banks, fiscal policy, geopolitical events and of course, the Fed’s unprecedented dual-track approach to monetary policy tightening. Not surprisingly, these major uncertainties led to a meaningful increase in interest rate volatility.”

Overall, AGNC put up one of its best quarters in the past two years. The firm has done a great job expanding it net income spread, and it finally saw a nice reversal in TBV. The former is fueled by AGNC management, which has been masters at hedging. In the quarter, the company’s Treasury-based hedges outperformed traditional swap-based hedges, helping its strong performance.

Valuation

For mortgage REITs, I usually look at a price to book as the best way to value them. On that front, AGNC trades at 1.12x.

AGNC was the first MREIT to report its Q4 results, so I don’t have end of year values for the other firms. Based on Q3 book value, though, Annaly (NLY) trades at 1.07x book while ARMOUR (ARR) is at 0.90x. Two Harbors (TWO) trades 0.87x.

AGNC trades at a premium to other MREITs, but this has been well earned given its hedging prowess and overall management over the years. I’d also note that trading above book does have some advantages, as discussed above, as it allows firms to issue shares to buy more MBS and it increases book value at the same time.

Where TBV ends up will depend on interest rates, leverage, and where Treasury-to-MBS spreads head, but I don’t think $11 is out of the question given the expected three cuts. Place a 1.1x multiple on that, and you have a $12 stock.

Conclusion

The tide has turned for agency-backed mortgage REITs, and now is the time to get into AGNC if you haven’t already. The current interest rate cycle has peaked, and a Fed rate-cutting campaign will drive rates lower and TBV higher. At the same time, expect spreads to Treasuries to also narrow, which should help TBV as well.

The combination of a nearly 15% yield together with rising TBV, should be a driver for AGNC in the coming year. AGNC is not a buy and hold forever stock, but this is the cycle you want to own it in. I rate the stock a “Buy” with a $12 target.

Q2 2024 Earnings Call Transcript")