adventtr

The Simplify Aggregate Bond ETF (NYSEARCA:AGGH) is an actively managed, investment-grade bond ETF. It is aggressively actively managed, with high turnover rates and the use of derivatives. AGGH’s strategy has been moderately successful in the past, with the fund outperforming its closest benchmark, but not all relevant indexes or peers. AGGH’s 9.6% dividend yield is quite high but seems somewhat unsustainable. Although there is nothing significantly wrong with the fund, I can’t say that I find its strategy or performance all that compelling. As such, I would not be investing in the fund.

AGGH – Basics

- Investment Manager: Simplify

- Distribution Yield: 9.64%

- Expense Ratio: 0.33%

AGGH – Strategy and Portfolio

AGGH is an actively managed, investment-grade bond ETF. The fund intends to focus on other investment-grade bond ETFs and hedge the credit risk. It seems to do neither, as it focuses on individual treasuries and treasury futures while selling calls on some of its holdings. A fellow author says AGGH is not the bond fund advertised, and I am inclined to agree.

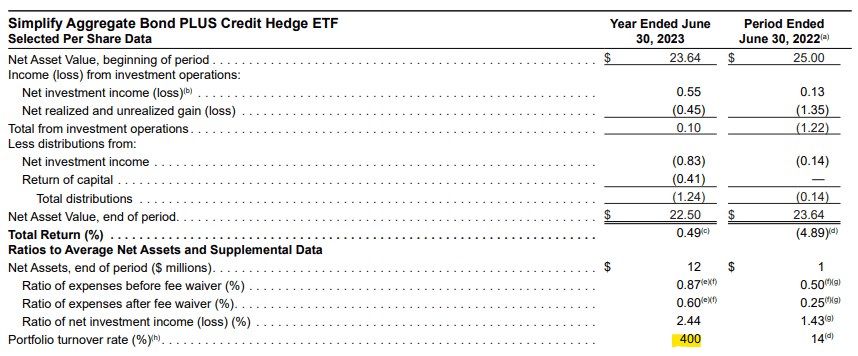

AGGH is actively managed, and it seems to be aggressively actively managed, with a whopping 400% turnover rate, several option strategies, trades, leverage, and shifts in positioning. Turnover rates probably overstate actual portfolio turnover, as the fund holds a lot of short-term securities, which are rolled over through time.

AGGH

Right now, the fund focuses on short-term inflation-protected treasuries and 10Y treasuries. Seems like a recent position, as per prior coverage. AGGH used to invest quite heavily in short-term inflation-protected securities but seems to have sold/refused to roll over most of these securities.

Right now, the fund sells calls on some of its holdings. Premiums from these are used to boost the fund’s distributions. It is impossible for me to even attempt to quantify these.

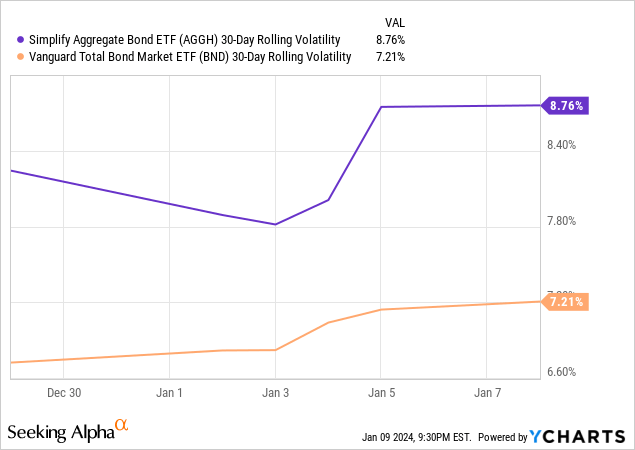

Options and futures are generally implicitly leveraged. Nevertheless, the fund does not perform as a leveraged bond fund would, with only slightly higher volatility than bond index funds.

Data by YCharts

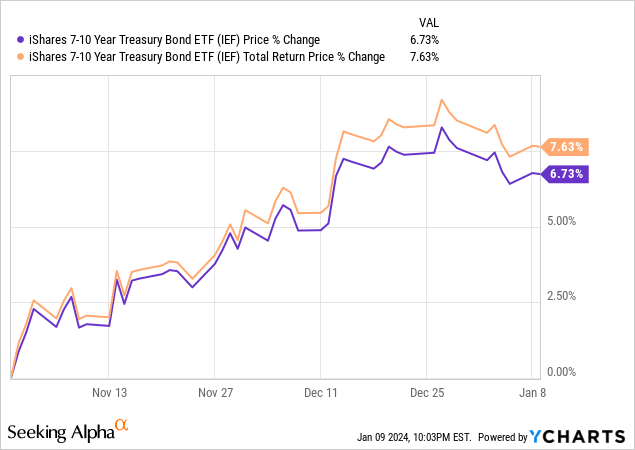

As should be evident from the above, there are aspects of AGGH which are not all that clear to me, due to the fund’s high turnover rate and unclear/outdated information. What is clear to me is that the fund is an investment-grade bond ETF and that its active management strategy is instrumental to its characteristics, performance, and distributions. Shifting to 10Y treasuries in late October 2023 would have led to sizable gains:

Data by YCharts

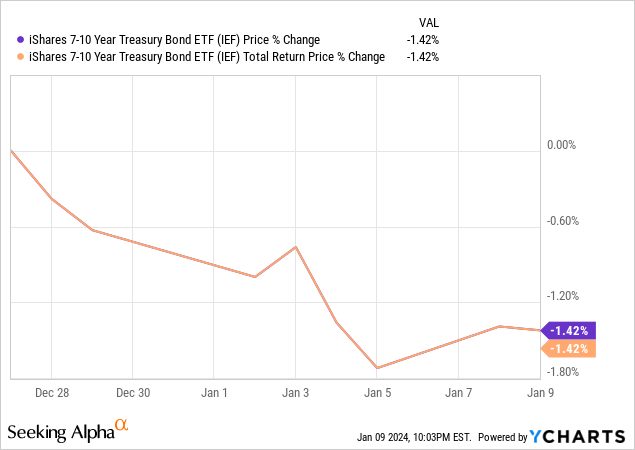

Investing in late December would have led to slight losses:

Data by YCharts

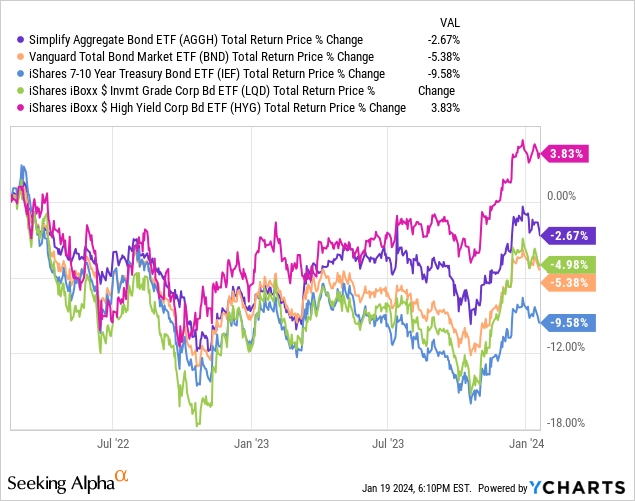

The same is true of the fund’s other investments and strategies. Importantly, it is not true for most bond funds, at least not to the same extent. A fund like the iShares 7-10 Year Treasury Bond ETF (IEF) is always invested in treasuries and sees very little portfolio turnover or shifts in positioning. IEF can’t really outperform treasuries due to active management, unlike AGGH.

Overall, I dislike AGGH’s strategy, as it is incredibly uncertain, somewhat complicated, and a bit risky. I’m not sure what exactly it is that I am buying, or if it will perform all that well moving forward. These are not deal-breakers, but definitely negatives.

For a fund like AGGH, potential outperformance is the key selling point. Let’s have a closer look at the fund’s performance.

AGGH – Performance Analysis

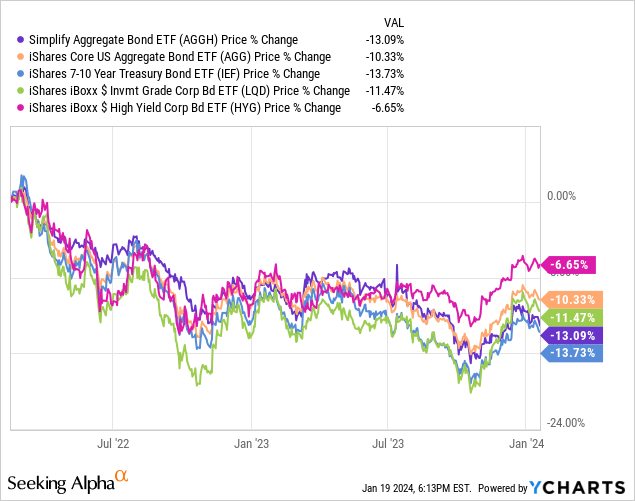

AGGH’s overall performance track record seems reasonably good, although nothing out of the ordinary. The fund has slightly outperformed most bonds, investment-grade bonds, and treasuries since its inception in early 2022. Outperformance was concentrated in mid-2023. Drawdowns and volatility seem about average.

Although AGGH has outperformed most of its peers since its inception, a few negative issues stand out.

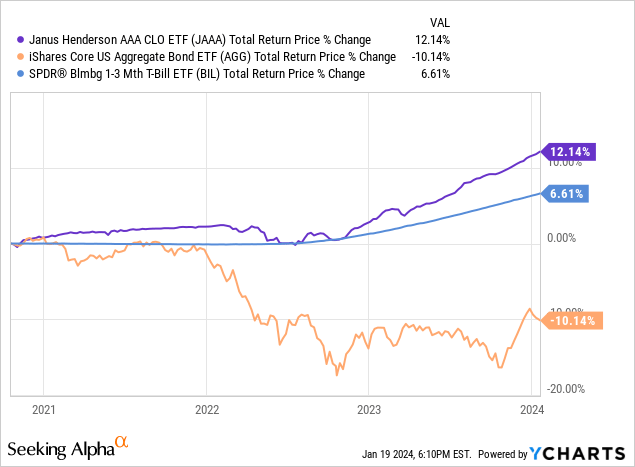

First, the fund’s outperformance was slight and inconsistent. AGGH’s strategy does seem to be working, but the excess returns do not look that significant. The best fixed-income funds outperform much more consistently and significantly, including the Janus Henderson AAA CLO ETF (JAAA):

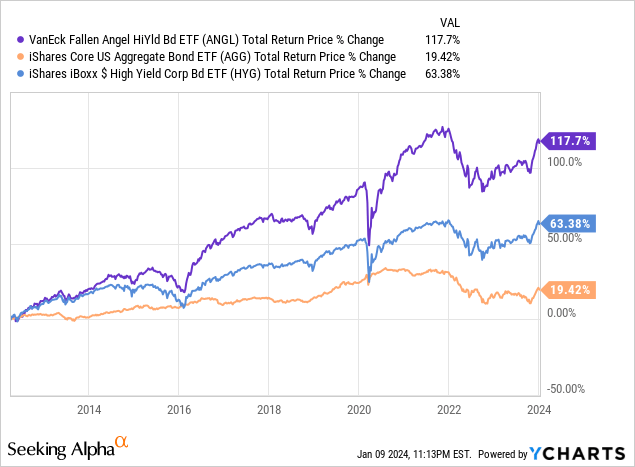

Second, the fund’s performance track record is not all that long. Two years seems enough to have an idea of the fund’s effectiveness, but not to be certain. AGGH’s strategy might not work all that well as rates start to decline, for instance. For reference, fallen angels have a decades-long track record of outperformance, as does the VanEck Fallen Angel High Yield Bond ETF (ANGL):

Data by YCharts

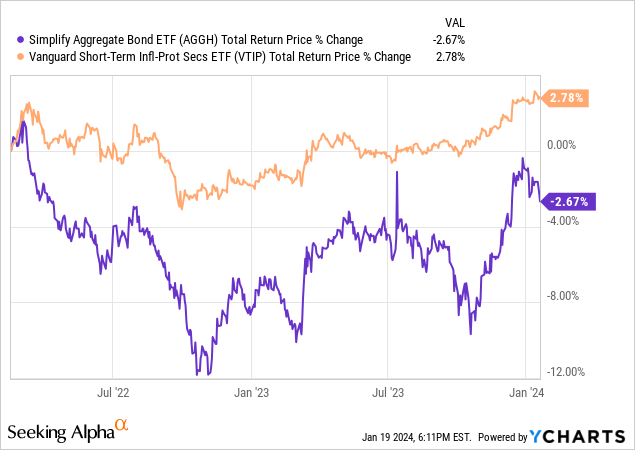

Third, the fund does not compare all that well to short-term inflation-protected treasuries, which accounted for a significant portion of its portfolio in the past. One could argue that overweighting these securities was a good choice, one could also argue that the fund should be benchmarked against these.

Overall, AGGH’s performance track record does seem reasonably good, but definitely not outstanding.

AGGH – Distribution Analysis

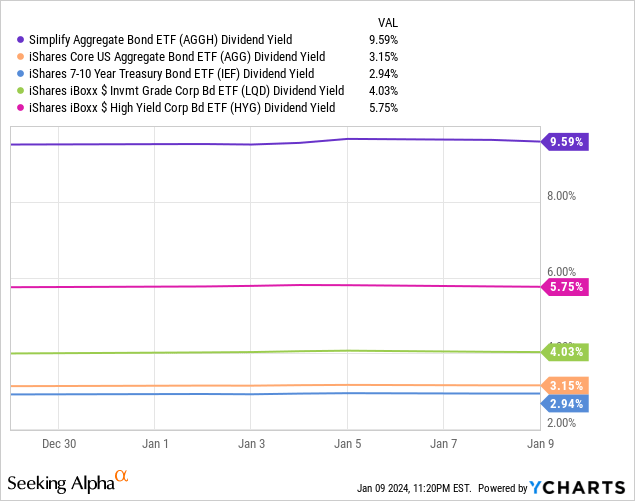

AGGH currently sports a 9.6% distribution yield. It is an incredibly strong yield on an absolute basis, and much higher than that of most bonds and bond sub-asset classes.

Data by YCharts

Ideally, AGGH’s distributions would be covered by the underlying generation of income, including coupon payments from its bond portfolio and option premiums from selling calls. It is unclear to me if this is the case. The fund’s share price has declined since inception, consistent with uncovered, unsustainable distributions, but this seems to have mostly been due to higher interest rates.

Overall, I find the fund’s strong distributions to be a net positive, but there are issues regarding their sustainability. For an aggressive actively managed fund like AGGH it seems better to focus on total returns, in my opinion at least.

AGGH’s strong distributions and above-average performance track record make for a reasonably compelling investment thesis. Not compelling enough to overcome uncertainty about the fund’s holdings, strategy, and performance, for me at least.

AGGH – Conclusion

AGGH is an actively managed, investment-grade bond ETF. Although there is nothing significantly wrong with the fund, I can’t say that I find its strategy or performance all that compelling. As such, I would not be investing in the fund.

Q2 2024 Earnings Call Transcript")