Capuski/E+ via Getty Images

I discovered this stock around the time of Charlie Munger’s passing and it reminded me of one of his investment philosophies. He is said to have famously remarked, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

But as I dived deeper into this company, I saw that its business model not only qualifies as wonderful but the business also presents itself at an incredibly wonderful price. Let me explain.

A wonderful company

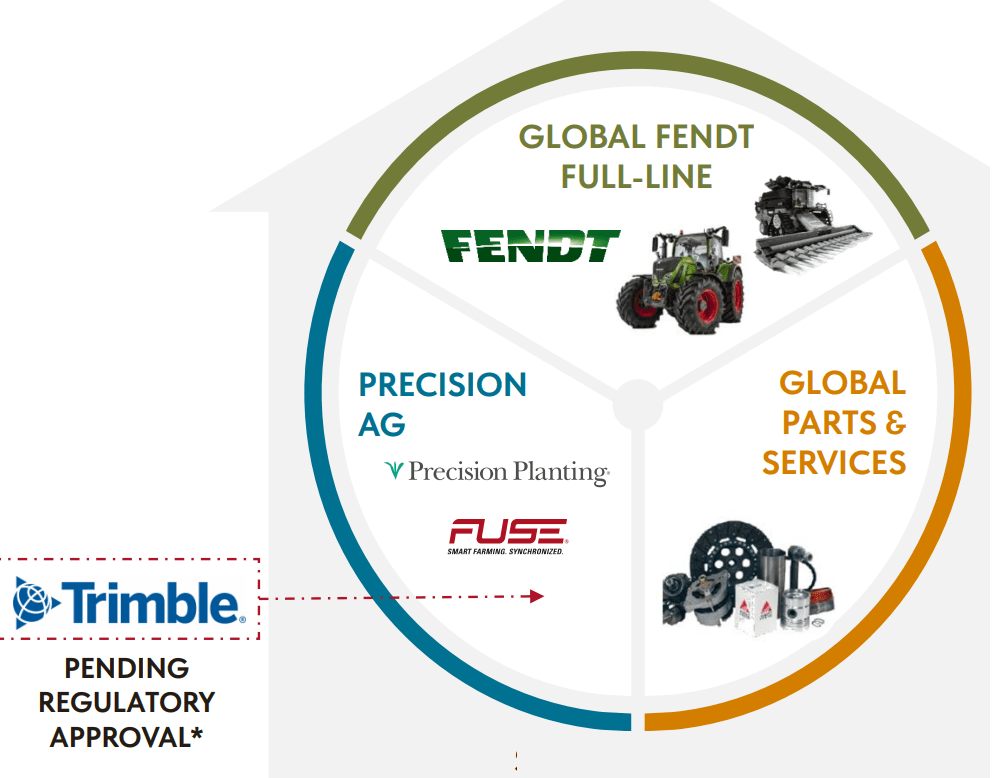

AGCO Corporation’s (NYSE:AGCO) business model revolves around delivering high-quality agricultural equipment and services to customers worldwide, supported by a robust distribution network and support for its products.

Product Portfolio: The company offers a comprehensive range of agricultural equipment, including tractors, combines, sprayers, hay and forage machinery, seeding and tillage equipment, and grain storage solutions. They have a history of continuous innovation and continue to update its product offerings to meet the evolving needs of farmers and agricultural businesses worldwide.

Portfolio (Investor Presentation)

Their business not only brings revenues from the initial sale of equipment but also revenues from the entire lifecycle of the equipment (Supplying spare parts, support, maintenance, repairs, and technical assistance).

Presence: Their brands operate in over 100 countries, serving a diverse customer base of farmers, agricultural contractors, and agricultural machinery dealers. The company’s global footprint enables it to capitalize on opportunities in various regions and adapt its product offerings to local market preferences and regulatory requirements. The company also uses a multi-channel distribution model, comprising a network of independent dealers, distributors, and company-owned outlets. This extensive distribution network ensures broad market coverage and facilitates the efficient delivery of products and lifecycle support to customers.

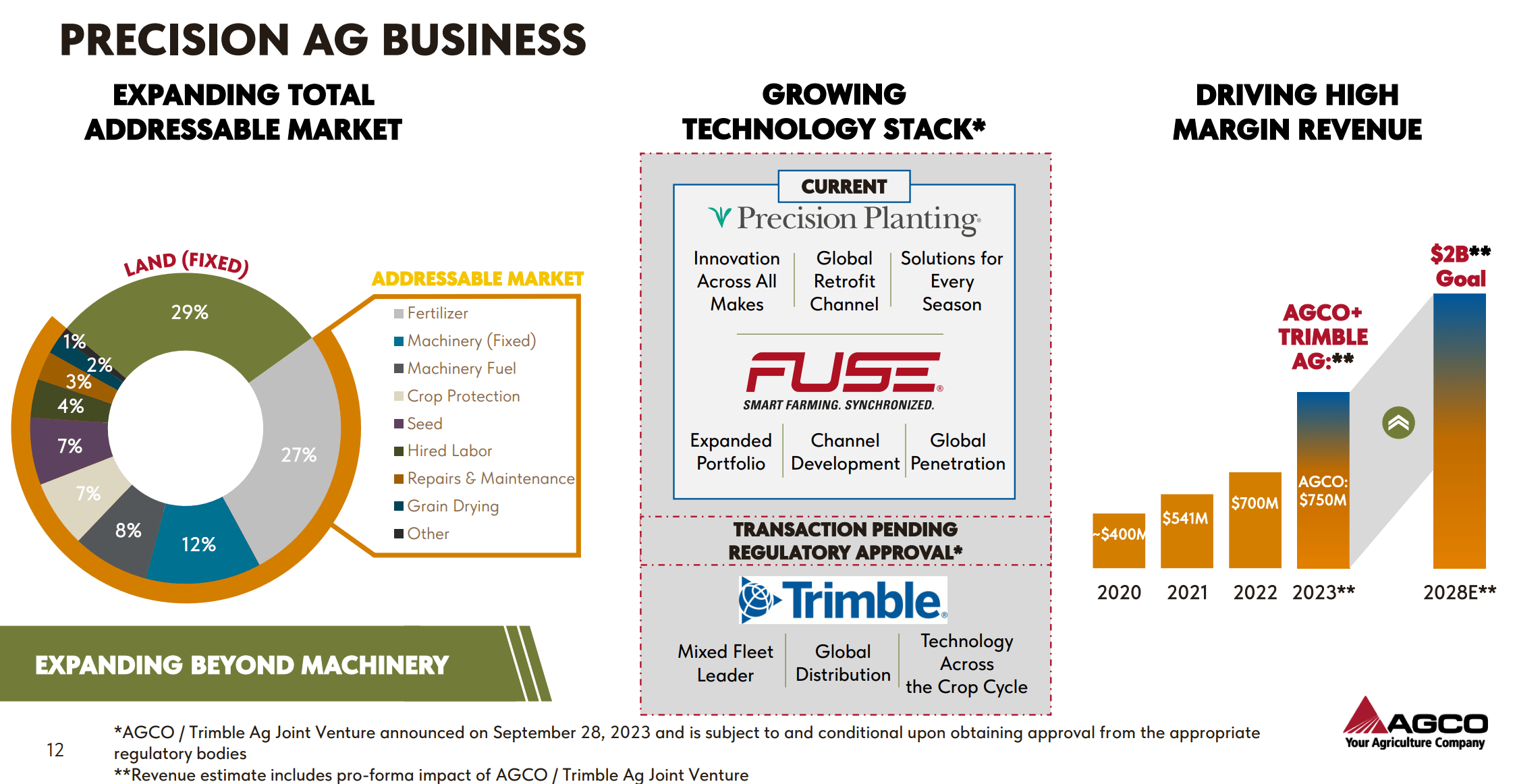

Current Strategy and Approach

Market (Investor Presentation)

Looking at their latest earnings call, AGCO Corporation’s current strategy is centered around its Farmer-First Strategy, which involves growing its Precision Ag business, further globalizing its Fendt branded products, and further expanding its parts and service business.

AGCO’s focus on high-margin, high-growth segments centered around its technology stack would align with its goal of outperforming the industry. Additionally, as mentioned earlier, AGCO is working on joint ventures, like the one with Trimble, to enhance its offerings and drive growth.

The company’s strategy includes leveraging technology to improve product performance and efficiency and positioning itself as a trusted partner for smart farming solutions. I think by focusing on key growth levers such as globalization, parts business expansion, and Precision Ag, AGCO could potentially surpass industry growth rates.

Hallmarks of a quality business

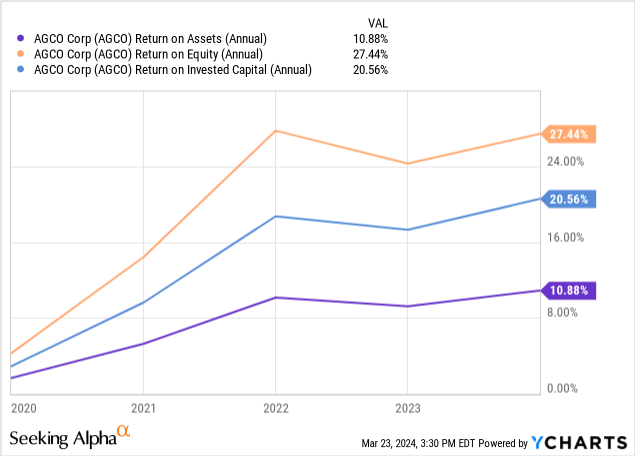

1. The three pillars of a quality business for me are Return on Equity, Return on Assets, and Return on Invested Capital and all of them have been on an uptrend in the last few years.

The positive growth rates over the past few years indicate that AGCO effectively utilizes its capital to generate profits and return capital to shareholders.

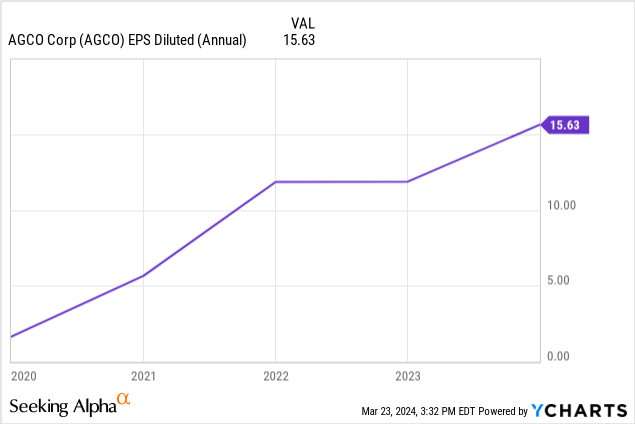

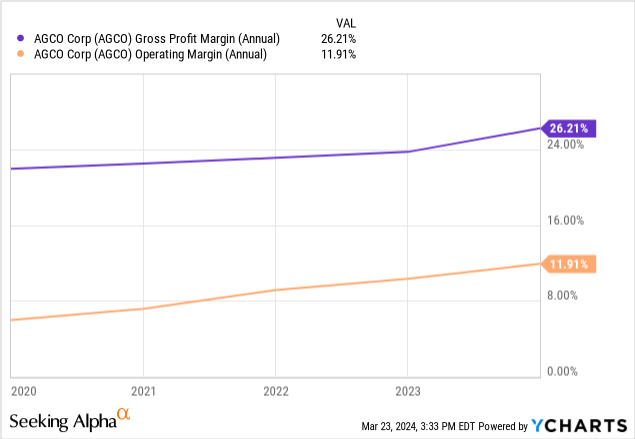

2. It is no secret that ROE, ROA, and ROC usually come on the back of impressive top and bottom-line growth. In terms of revenue growth, the company has achieved a Compound Annual Growth Rate (CAGR) of 14.5% over the past three years, indicating a strong upward trajectory. EPS has also seen an impressive upward trend and most of this can be credited due big improvements in margins.

3. The company’s upward trajectory came entirely from improving business prospects and debt or dilution was no factor. Its debt-to-equity ratio from close to 50% to less than 30% over the past five years. Its operational cashflows have also shown an upward trajectory and the debt is well covered by its OCF. Its free cash flow has also seen an increase of 30% to $450M for 2023 compared to 2022.

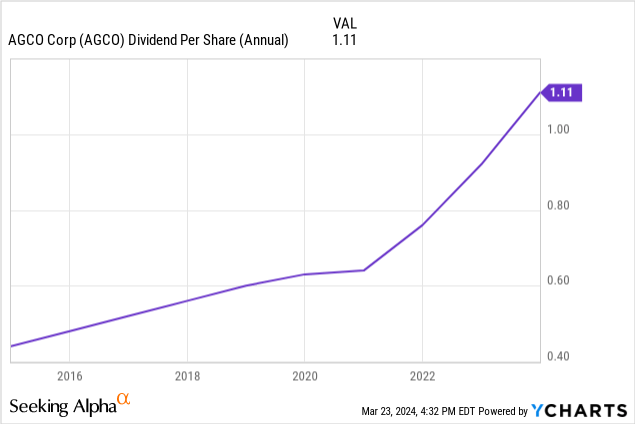

Rounding up all this is the fact that the company has a dividend program that is attractive and sustainable.

- The dividend payout has been stable and increasing over the past several years

- The payments are well covered by its earnings (low payout ratio)

A wonderful price

This is where I believe things start to get even juicier.

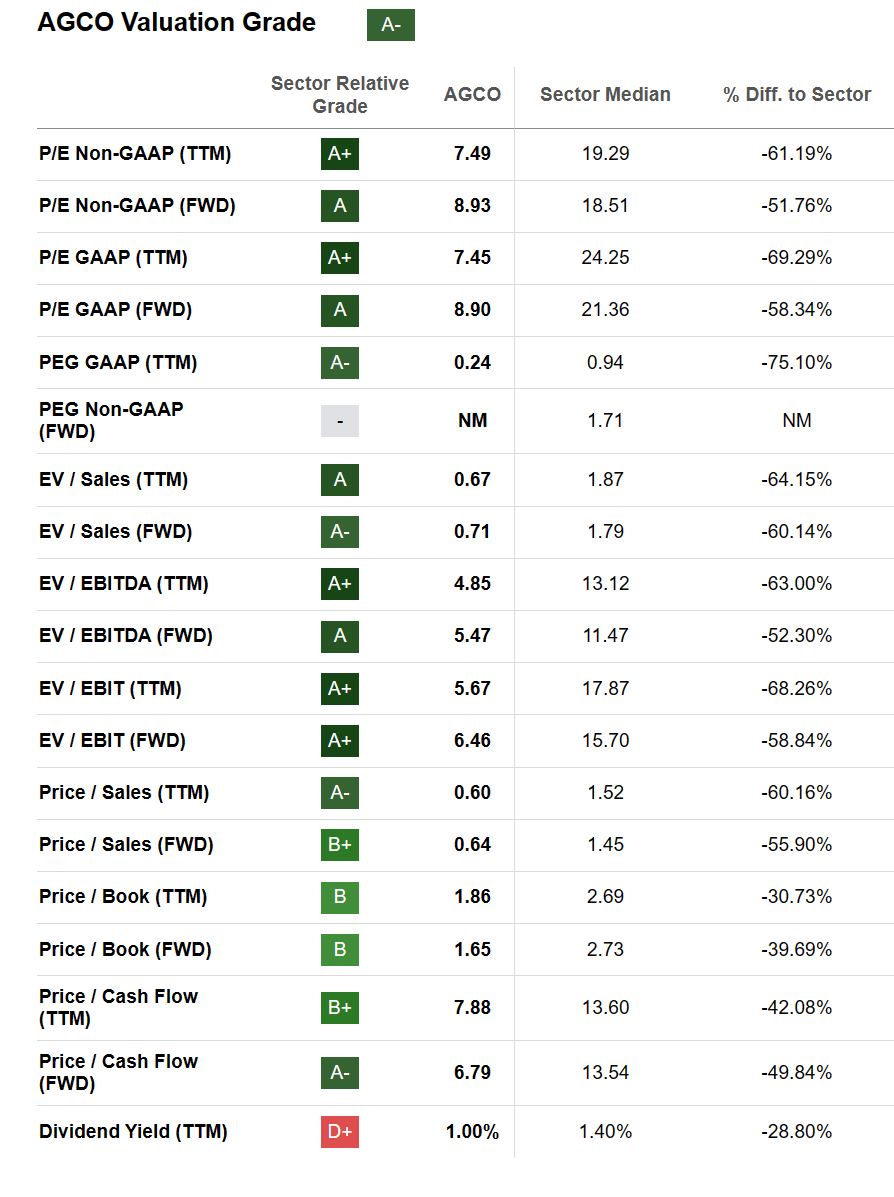

1. The company trades at a current Price-to-earnings multiple of 7.5x and as we saw, its earnings growth has been so impressive, which results in a low PEG ratio of 0.24. In fact, across the board, the company’s multiples are extremely low when compared to the sector multiples.

SA

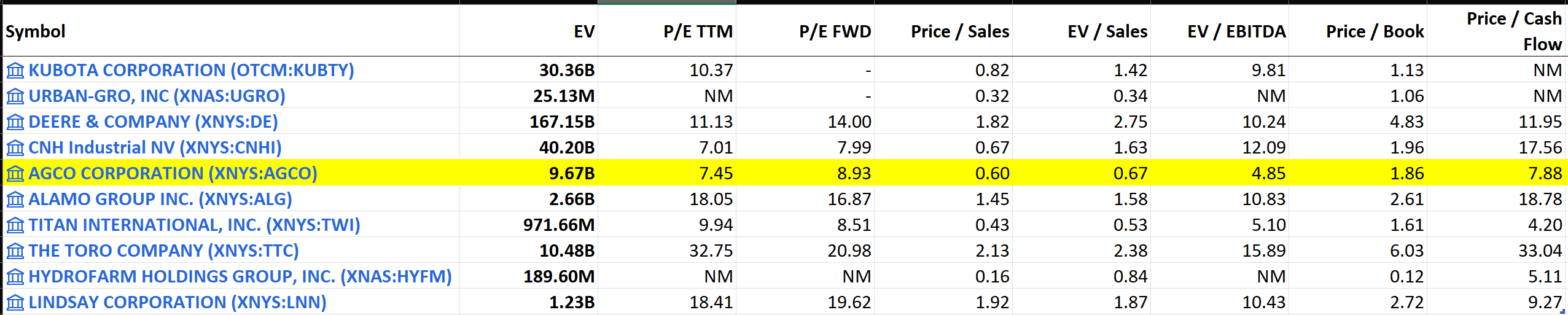

2. The company has also provided its outlook for 2024 with net sales of $13.6B and EPS of $13.15 which is 16% lower than the 2023 full-year EPS. This slightly inflates our ratios but it is still lower against its comparables. Looking at the “Agricultural and Farm Machinery” industry components, we see that there are 10 stocks and the company ranks quite well across the board against the other components in the industry.

Industry comps (SA)

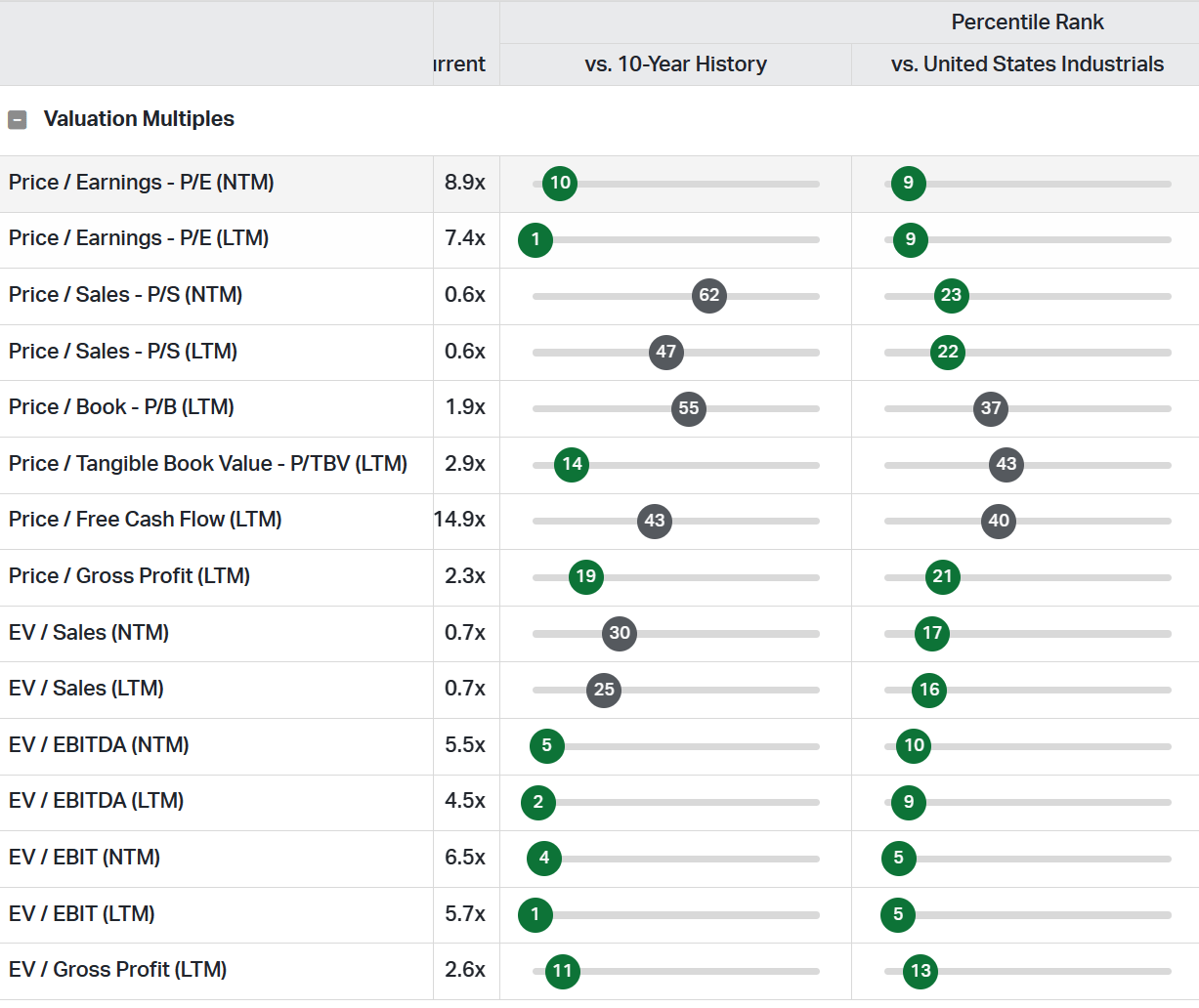

3. Yet, another way to look at its valuation would be to see how well it fares against its own history. PS and P/FCF are trading close to their mid-point but outside of this every valuation metric is trading at its lows (This rank is observed both across its 10Y history and against the sector).

Valuation Percentile Rank (Koyfin)

4. Even with inflated forward ratios, I believe the stock is trading at least 30% below its fair value when we combine the information from its sector, industry, and its own historical valuation.

Risks to this thesis

This naturally begs the question. With such a fantastic business model, and consistent growth how is this trading so low? What could the market’s reasons be for not piling on this opportunity? One reason could be that this industry is heavily exposed to the commodity business. Commodities can be notoriously difficult to predict. The industry is cyclically influenced by weather and supply and demand. Fluctuations in commodity prices can affect farmers’ income and their ability to invest in new machinery. Lower commodity prices can lead to reduced spending on equipment, impacting the revenue of farm machinery companies. Specifically, for a company such as AGCO with an international presence, these factors can get country/region specific which can start to show in the topline. In fact, in the latest quarter, there is already some evidence for this statement, and the company is predicting a slowdown in 2024.

Investor Presentation Investor Presentation

The company experienced a 2.5% decrease in net sales and a 1.6% decline in operating margins year-over-year. Strong performance in Europe and North America helped offset the overall slowdown in market demand, particularly a significant increase in competitive retail activity in Brazil. This was also coupled with a sharp decrease in demand and substantial retail incentives, which impacted the results.

Expectations for 2024 anticipate more challenging global market conditions, attributed to declining commodity prices and slightly reduced farmer income projections which means lower sales for 2024.

Final Call

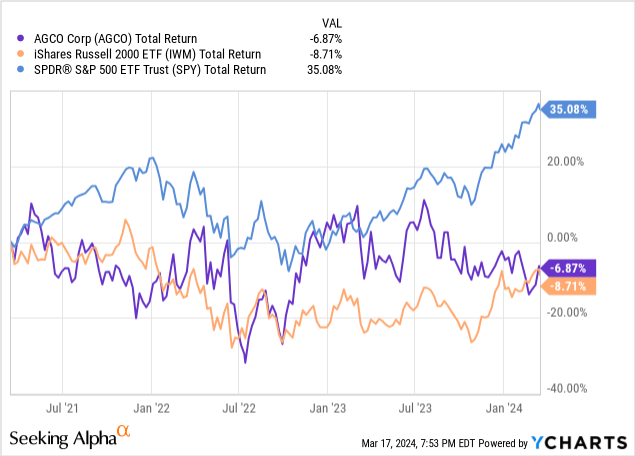

I rate this company as a Strong Buy and I already own stocks in this company. The outlook for 2024 may be lower and the market could be pessimistic about the company’s prospects over the short term. The stock has underperformed the S&P index but this doesn’t really surprise me. It is well known that returns in the stock market have been skewed by the Technology mega-caps and tech concentration has become a major driver in the performance.

For me, the business shows promise, trading at an attractive price and fundamentally I believe this belongs in a long-term buy-and-hold portfolio and the market is giving me an opportunity to buy at this level.

Q2 2024 Earnings Call Transcript")