Jeremy Poland

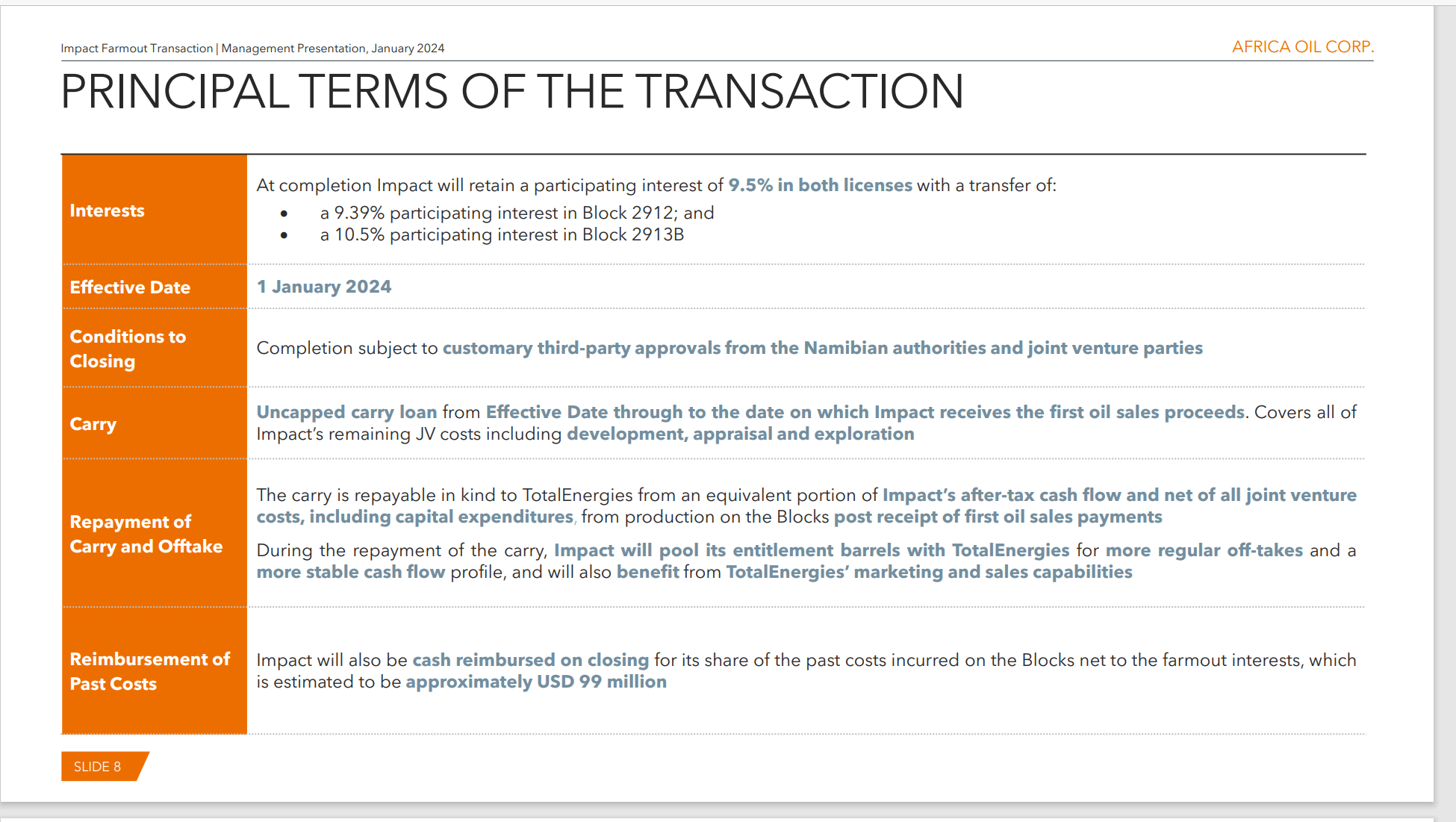

Africa Oil Corp. (OTCPK:AOIFF) is a major shareholder of Impact. That subsidiary has no income but has a major share in the discovery known as Venus where Total is the shareholder. Impact management recently sold a significant portion of its interest in this discovery in exchange for an end to the financing needs that typically plague a company with no revenue. TotalEnergies SE (TTE), the operator has agreed to essentially carry Impact to first commercial production with the terms listed in the referenced agreement. There will likely be something formal filed in the future for shareholders to review. This allows shareholders to participate in the considerable upside of a world-class discovery without the repeated capital raises that would have occurred until production. (Below: source)

Africa Oil Details Of Impact Farmout Agreement For Venus (Africa Oil Corporate Presentation Of Impact Agreement)

This will also significantly reduce the financing needed for major shareholders in Impact. Africa Oil itself can therefore devote its cash flow to considerable opportunities (that range from lower risk than this to higher risk) that could likewise raise shareholder value.

Partnerships

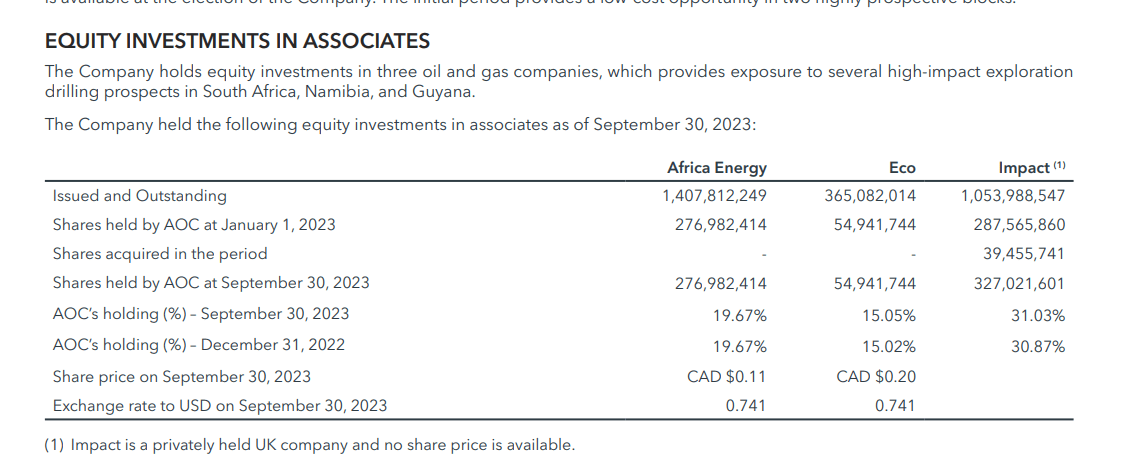

Africa Oil has considerable interests in companies that are for all intents and purposes partnerships. None of these partnerships produce income. Therefore, with each capital call from these companies, the partners can decide whether to move forward or retain a diluted interest.

Africa Oil Interests In Other Companies (Africa Oil Third Quarter 2023, Financial Statement)

Two of these companies, Africa Energy Corp. (OTCPK:HPMCF) and Eco (Atlantic) Oil & Gas Ltd. (OTCPK:ECAOF) are publicly traded Canadian companies that like Africa Oil, report in United States dollars. Impact is private. Depending upon the future course of drilling success offshore, there could be considerable cash requirements generated by these interests.

Currently, investing through these largely speculative projects through Africa Oil has the advantage of Africa Oil having cash flow and management that can decide whether or not to continue to add cash to any of the subsidiaries for the projects in each portfolio. Sometimes, as in the case of some African acreage, Africa Oil itself owns an interest in the project as well.

The key is that oftentimes, the management of Africa Oil is in a much better position to determine the cash needs of the subsidiaries than the average shareholder. Besides, Africa Oil usually has the cash to maintain its interests. Individual shareholders can be diluted significantly before first production arrives (if it ever arrives at all).

Risk

There is always the risk that any or all of the projects fail to meet expectations.

Africa Oil is a relatively small offshore player that could have cash needs that exceed the ability of management to raise that cash needed. This could have material adverse effects on company prospects.

Growth from offshore projects will occur on an irregular basis. Investors can expect large jumps at one time with probably years between those jumps. Smaller companies like this rarely grow each year because of the size of the projects.

Africa itself has been a cash drain on oil and gas companies for years. While that period appears to be ending there is no assurance that is the case.

The governments in the area where Africa Oil is the main source of cash flow are not known for its effectiveness. Other areas with upside potential are not known for their stability. The fact that the business is offshore mitigates much of the effect but cannot eliminate it.

As a result, this has to be considered a speculative idea before you even consider typical risks like commodity price and loss of key personnel.

Areas Of Operation

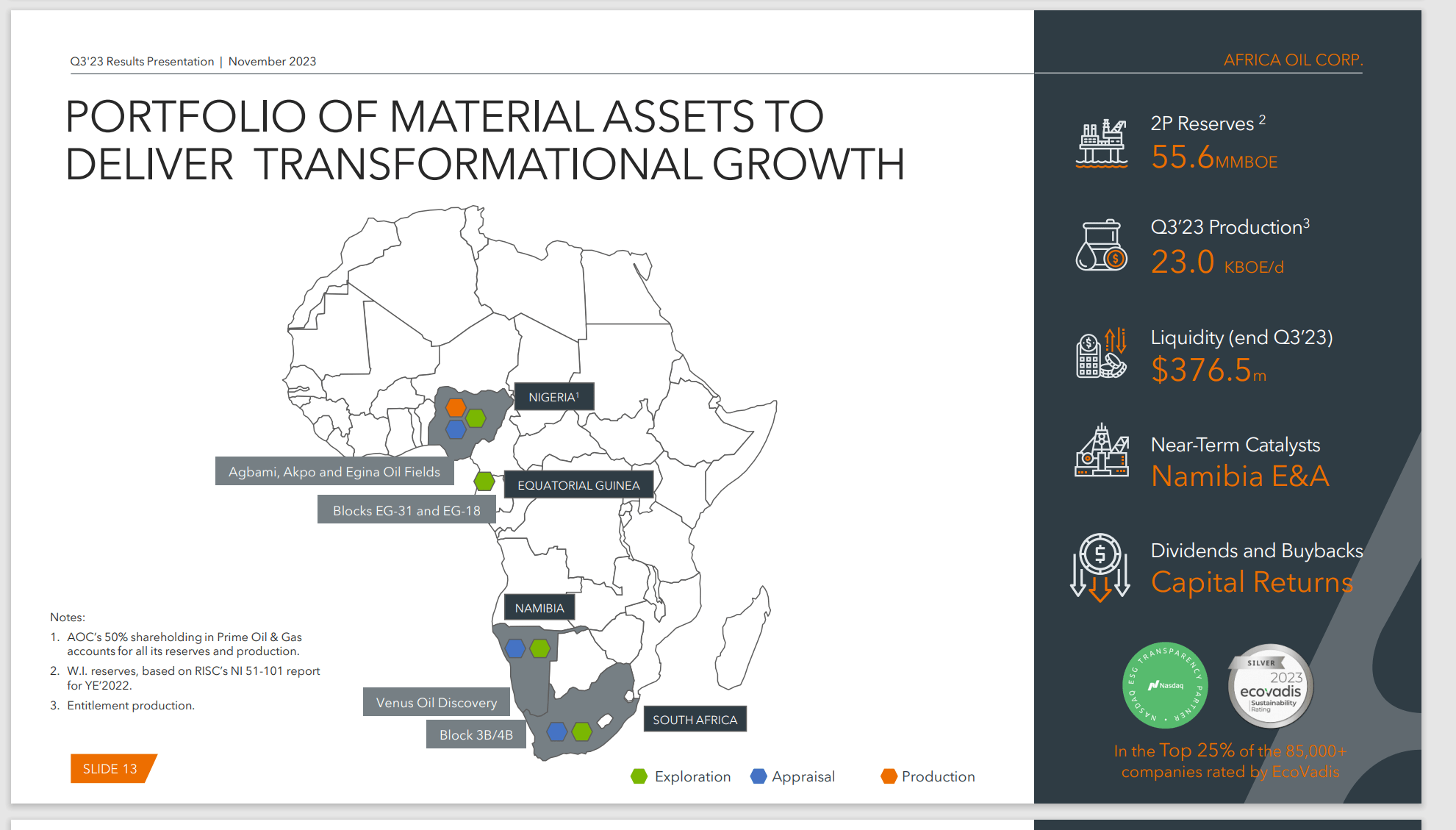

The company does have an interest in Guyana through its interest in Eco Atlantic. But the cash flow and much of the upside potential is in Africa at the current time.

Africa Oil Map Of Operations And General Status Of Projects (Africa Oil Corporate Presentation Third Quarter 2023)

The current production reported is solely from Nigeria. However, future production is likely to come from both South Africa and Namibia. Both of those countries are far more stable with modern supporting infrastructure than is typical of the continent. The result is that Africa Oil may well have some more reliable income sources.

In fact, the South Africa venture in which Total is the operator also has submitted a request for a production permit that is likely now being reviewed. That particular request is through Africa Energy.

Finances

Africa Oil, the company itself is debt-free and has a considerable cash balance. However, there are some obligations from its ownership in Prime which does carry some debt. That debt has climbed in the current fiscal year as Prime has participated in some development and exploratory drilling located offshore Nigeria. This is expected to at least maintain and probably increase production (net to Prime).

Therefore, that debt is likely to be quickly repaid. Africa Oil is completely dependent upon dividends from Prime to run its own operations. Those dividends are paid on an irregular basis. Therefore, Africa Oil needs a significant cash balance to keep other projects in its portfolio adequately financed as needed.

The Nigerian projects are likewise operated by major oil companies. This somewhat reduces the risk of operating offshore Nigeria.

What This Means To Investors

Africa Oil has been doing share repurchases as well as paying a dividend to shareholders. However, the balance sheet strength is paramount as is the growth in production in the future. Therefore, this company is best looked at as an upstream variable dividend entity with some very large projects on its plate.

Management, through its actions, is demonstrating that the company is undervalued. However, that undervaluation comes with considerable risks that some other undervalued companies I follow do not have.

Therefore, while this company remains a strong buy. The risks that this company has in its line of business (and preferred location for that business) may well discourage all but the more venturesome investors.

There are some excellent projects that could change the current scenario in the future. But any position in this company should be a small position as part of a basket of companies. Project delays for any number of reasons should be expected whenever a small company like this tackles large projects. The larger companies that operate these projects give this company credibility the few companies of a similar size have.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")