Scott Olson

I have a past with adidas (OTCQX:ADDYY) (OTCQX:ADDDF). Back in 2015, I wrote about adidas because the underperformance relative to Nike (NKE) had caught my eye. Here is the chart from that analysis.

Google Finance

This trend was not only a deviation from its historical averages but also reflective of broader market dynamics.

Author’s computations

A critical factor in this underperformance was the geopolitical tension arising from the Crimea invasion. My hypothesis posited that the market had preemptively factored in the performance dip, anticipating a recovery and eventual market reassessment in favor of adidas. This prediction materialized, leading to a strategic exit from my adidas position following the onset of the second Ukraine invasion in 2022, a decision informed by the market’s previous response to similar geopolitical events.

Currently, a review suggests a potential repetition of this pattern, albeit compounded by additional challenges, such as the Yeezi collaboration’s shortcomings. This situation warrants a nuanced examination of adidas.

Seeking Alpha

Recent results

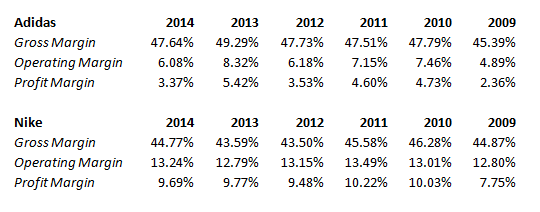

adidas’ financial performance in 2023 presented a mixed yet cautiously optimistic picture. The company’s currency-neutral revenues remained stable year-over-year, outperforming its initial projections of a slight decline. This stability is commendable, given the myriad challenges Adidas faced, including the termination of the Yeezy line, which was anticipated to negatively impact revenue. In reported terms, however, sales saw a 5% decrease to €21,427 million (USD 23,355 million) from €22,511 million (USD 24,537 million) in 2022, illustrating the tangible impact of these challenges.

The discontinuation of the Yeezy partnership was a significant drag on Adidas’ revenue, estimated at around €500 million (USD 545 million). Nonetheless, the release of two Yeezy products in 2023 partially offset this loss, contributing €750 million (USD 817 million) to net sales, albeit lower than the €1,200 million (USD 1,308 million) generated in 2022. Excluding the fluctuating Yeezy revenues, Adidas’ core business exhibited resilience, with a 2% growth in currency-neutral revenues, underscoring the underlying strength and adaptability of the brand.

Gross margin performance slightly improved by 0.2 percentage points to 47.5% in 2023, a testament to adidas’ strategic cost management and pricing mechanisms, especially noteworthy amidst substantial currency volatility. Operating profit, though significantly reduced to €268 million (USD 292 million) from €669 million (USD 729 million) in 2022, surpassed expectations by avoiding the forecasted operating loss, attributed to a robust Q4 performance and a strategic shift in handling the Yeezy inventory. Contrary to the anticipated write-off of approximately €300 million (USD 327 million), the actual figure was markedly lower, in the low double-digit million range. This decision not only mitigated the financial impact but also laid the groundwork for potentially recuperating value from the Yeezy stock in 2024 by selling these products at least at cost.

Problems and challenges

The recent leadership transition within adidas’ North American business, marked by the resignation of the President at the end of October and the subsequent appointment of a Board member as an interim leader, signifies a critical juncture for the company. This change comes amidst significant operational challenges in the American market, notably the issue of elevated inventory levels. Both retail and adidas’s own stock have been affected, exerting a pronounced negative impact on sales and profit margins.

A considerable portion of these difficulties can be attributed to the fallout from the Yeezy brand discontinuation. The termination of this partnership with Kanye West has not only led to a considerable revenue shortfall, but also contributed to the inventory challenges. The Yeezy line, once a major revenue driver for adidas, has left a void that the company now struggles to fill, exacerbating existing market challenges.

This leadership change, therefore, is not merely a personnel adjustment but a strategic pivot at a time when adidas needs to address and mitigate the compounded effects of inventory mismanagement and the loss of a high-profile collaboration. The new leadership’s ability to navigate these issues will be pivotal in stabilizing adidas’s North American operations and setting a course for recovery. The situation underscores the necessity for a robust strategy to manage inventory levels effectively and to find new avenues for growth and profitability in the wake of the Yeezy discontinuation.

Solutions: India, China and Saudi Arabia

adidas is at a pivotal juncture, necessitating a strategic overhaul of its marketing approaches and a comprehensive refresh of its product offerings to enhance its market appeal globally. The imperative to align more closely with American tastes and trends has led to the establishment of a dedicated office in Los Angeles, with a focus on tapping into American street culture and basketball. This initiative, aimed at fostering collaborations and projects resonant with street culture, signifies adidas’s commitment to embedding itself within the fabric of American cultural preferences.

However, adidas’s strategy extends beyond the U.S., recognizing the importance of diversifying growth avenues. The company’s foray into the Indian market, particularly with cricket merchandise, has borne fruit, exemplified by the sale of over half a million jerseys of the Indian national cricket team. This achievement is bolstered by the team’s performance in international tournaments, with sales momentum expected to surge in anticipation of the World Cup final.

Expansion efforts have also reached the Middle Eastern market, with the opening of an office in Saudi Arabia. This move reflects an understanding of Saudi Arabia’s growing engagement with sports, from hosting international events to enhancing its sports leagues. adidas anticipates leveraging the country’s increasing investment in sports as a strategic opportunity for growth.

In China, adidas is recalibrating its focus to meet local market demands, particularly in basketball. By bringing basketball stars to China and reviving grassroots programs, adidas aims to underscore basketball’s cultural significance. The company plans to introduce competitively priced basketball products, challenging local brands and catering to diverse consumer segments. This strategy underscores adidas’s vision of becoming a dominant sports brand in China, supported by significant investments and the establishment of a state-of-the-art distribution center.

Valuation & Risks

adidas’s preliminary outcomes for 2023 depict a company adeptly navigating the aftermath of discontinuing a significant product line, with management exceeding operational forecasts and making strategic inventory decisions, particularly concerning the Yeezy stock. This demonstrates a potential acceleration in resolving its challenges. The strategy to liquidate the remaining Yeezy inventory at cost in 2024 is pivotal, expected to influence financial metrics significantly.

For 2024, adidas’s forecast suggests a moderate growth trajectory in currency-neutral sales, inclusive of a planned contribution from selling the Yeezy inventory at cost, estimated to boost sales. Excluding this one-off, the company’s core business is expected to exhibit stronger growth, with an operating profit projection of around €500 million (USD 545 million). This outlook, juxtaposed with the company’s recent performance, mirrors the resilience adidas demonstrated in 2014 amidst geopolitical tensions and marketing missteps.

Seeking Alpha

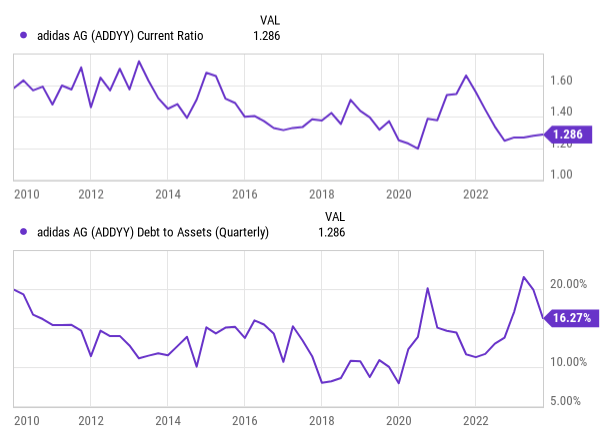

The financial structure of adidas, characterized by robust liquidity and manageable debt levels, remains stable, presenting a solid foundation for operational flexibility and strategic initiatives.

YCharts

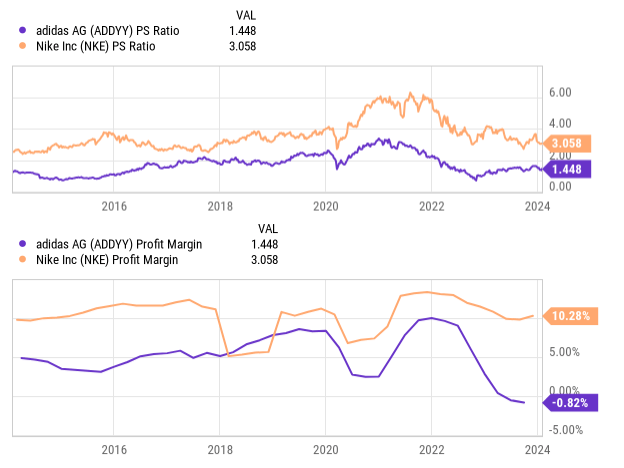

When we look at valuation, the comparison with Nike highlights a historical undervaluation of adidas, attributed to Nike’s superior profit margins. Despite this, a mean reversion to adidas’ historical sales multiple suggests potential for a valuation uplift, contingent on operational improvements.

YCharts

Marketing strategies reliant on celebrity endorsements present inherent risks, particularly in an era of heightened public scrutiny and the amplification of controversies via social media. The challenge for adidas and similar brands lies in navigating these risks while maintaining the allure and relevance of their endorsements. This necessitates a strategic reevaluation of celebrity partnerships to mitigate potential brand damage.

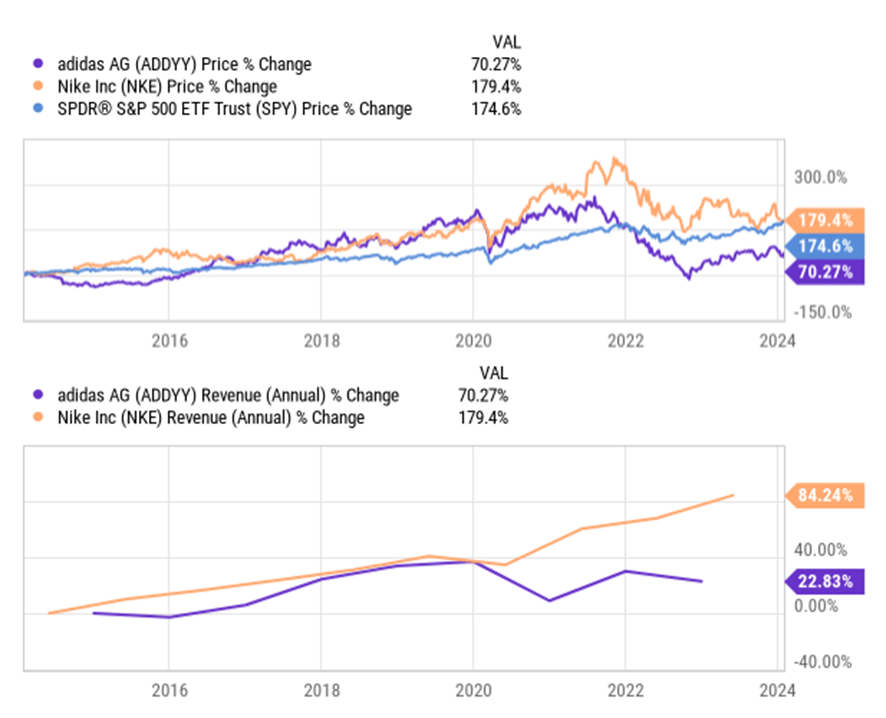

The enduring appeal of adidas, absent a significant market disruptor, suggests a resilient brand position. However, the historical comparison with Nike underscores a persistent performance gap, underscoring the importance of strategic clarity for adidas to enhance its market standing and financial performance.

In summary, while adidas shows promise for a valuation rebound and operational normalization, caution is warranted given the competitive landscape and the intricacies of celebrity-driven marketing strategies. The potential for growth and a return to form exists, but the need for a coherent growth strategy is paramount. Therefore, despite the attractiveness of adidas’ current valuation and its prospects for recovery, a watchful stance is advised until clearer growth indicators emerge, particularly in contrast to alternatives like Nike, which may offer more immediate clarity and growth potential.

YCharts

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")