KanawatTH

Investment Thesis

After robust performance through FY23 and into FY24, global markets led by the U.S. have delivered substantial gains for investors since the markets bottomed in late 2022. Interest rate hikes in most developed countries are on hold as the reserve banks of sovereign nations assess the growth outlook of their countries versus their respective inflation projections. Most recently, the U.S. Federal Reserve announced their projections last week that they continue to expect three rate cuts this year, with the ECB echoing similar sentiments earlier this month.

Such rate-cut projections are productive for the outlook on stock markets the world over, as lower rates spur growth once again. Investors looking to diversify away from the U.S. stock markets, which by some valuation measures are starting to look expensive, have many areas in global markets to allocate their capital. For those investors looking to gain broad exposure to global markets, the iShares MSCI ACWI fund (NASDAQ:ACWI) is one such ETF that offers investors the opportunity to invest capital in a broad range of global stocks.

The balanced approach that ACWI offers looks appealing to me, but the deep diversification of stocks combined with the relative underperformance of this fund makes the prospects of the ACWI ETF look unattractive to me. For reasons outlined in the post below, I will rate this as a Hold for now.

About the ACWI ETF

The iShares MSCI ACWI ETF is managed by BlackRock’s ETF arm, iShares. The fund offers investors a simplified portfolio construction process by providing exposure to a wide range of stock markets in countries all around the world across developed as well as emerging market economies, while minimizing any rebalancing needs in the process. The fund’s prospectus suggests that the ACWI ETF should be used to “diversify internationally and seek long-term growth in your portfolio,” so it might appeal to only those investors who want access to global markets but have a long-term horizon.

The ACWI ETF achieves its investment objective by tracking the investment results of the U.S. dollar-denominated MSCI ACWI Index. The index is composed of large and mid-cap developed and emerging market equities spread across two dozen Emerging Market economies and a similar number of Developed Market economies. The index tracks over 2000 components, so I can expect a similar level of deep diversification in the ACWI ETF as well.

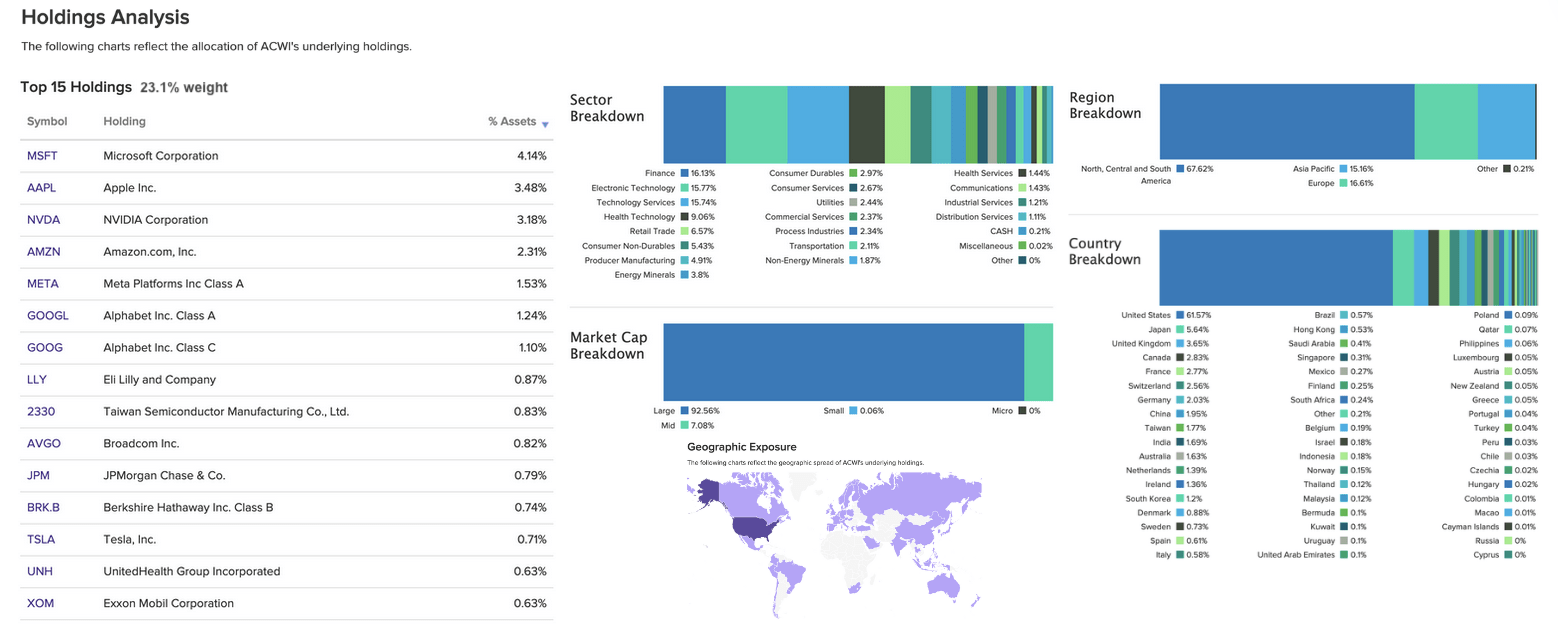

Here is a chart that shows the Top 15 Holdings vs. the Constitution of ACWI’s Funds by categories.

MSCI ACWI ETF’s holdings illustrated in charts (etfdb)

Peer comparison

Here is how ACWI ETF compares with some of its peers. The list below is ordered by largest-to-smallest fund in terms of Assets Managed.

MSCI ACWI ETF vs its Peers. Note that ACWI ETF’s dividend payout is semiannual. (sa)

Both the ACWI fund and its largest peer by assets managed, Vanguard Total World Stock Index Fund ETF (VT), are relatively newer as compared to the SPDR Global Dow ETF (DGT), which has been around since the start of this century. Now, comparing ACWI with VT, I see that it costs investors 25 cents more for every $100 of capital to stay invested in ACWI. On top of that, the trailing dividend yield difference of 0.32% does not make the ACWI as appealing. However, ACWI does outperform VT marginally for every time period, except for the 10 year period, where it outperforms VT by 4.2%. Also note that ACWI’s dividend payout is semiannual.

Moreover, the DGT fund also appears to be more appealing despite its 0.5% expense fee, which is 0.18% higher than ACWI. I believe this relative appeal will be important to investors because DGT’s trailing dividend yield is 0.64% higher than ACWI.

Long-term appeal does not seem interesting on a relative basis

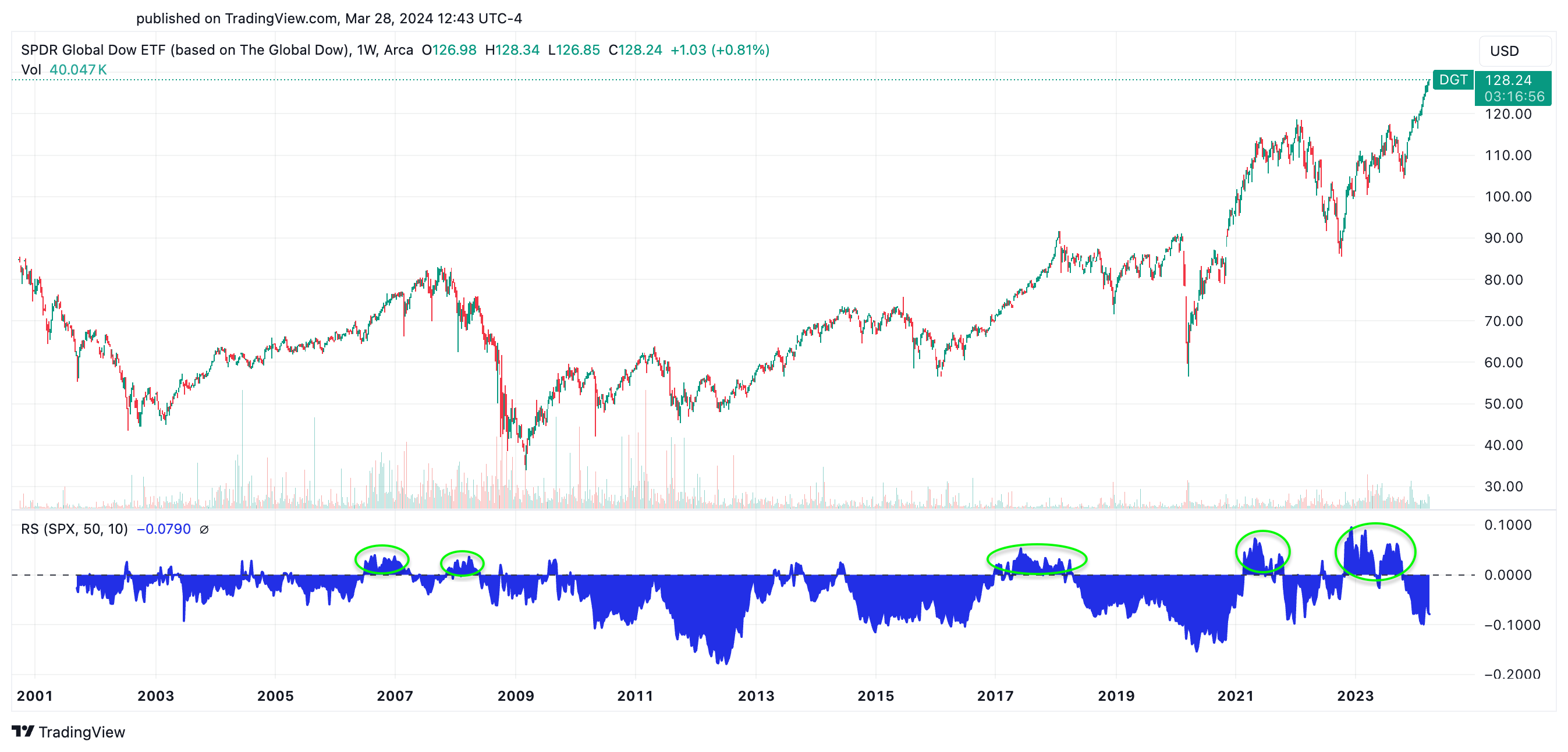

Most global broad-market ETFs set expectations to have long-term horizons with their ETFs, as I had pointed out earlier in the About section above in ACWI’s case. To compare the relative performance of global broad-market ETFs vs. the S&P 500 Index, I looked at DGT’s past performance vs. the S&P 500. Since DGT was an older fund, it made sense to look at that first.

DGT underperforms S&P 500 (TradingView)

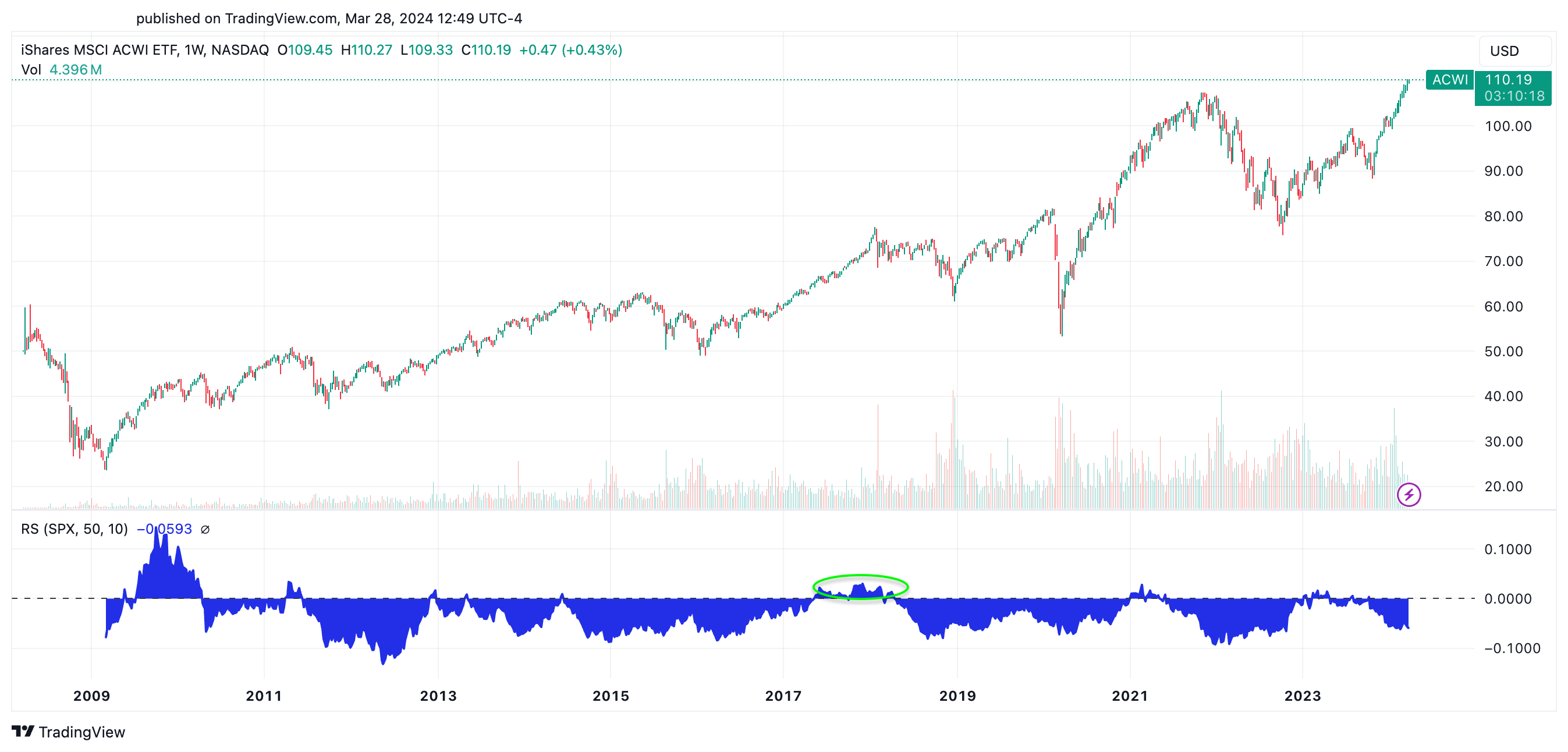

From the chart above, I have circled out areas of relative outperformance of the DGT versus the S&P 500 index. This shows that broad-market index ETFs like DGT have few instances of outperformance compared to the S&P 500 index. Those instances of underperformance look even more pronounced when comparing ACWI’s relative performance versus the S&P 500, as seen below.

ACWI underperforms S&P 500 more as compared to DGT in earlier charts (TradingView)

In my view, global broad-market ETFs don’t offer that much appeal when comparing DGT’s relative history. Still, if investors prefer international diversification funds like DGT and VT, they would be better choices as compared to ACWI.

Moreover, the ACWI fund trades at a rich valuation as compared to some of its peers. To arrive at the relative valuation, I looked at the forward valuation that the underlying indices are at. The MSCI ACWI Index, which the ACWI fund tracks, trades at a forward valuation of 17.4x forward earnings, which is significantly higher than the DGT fund’s forward valuation of 12.9. Given this outlook, I remain neutral on the ACWI fund.

Risks and other factors to consider

In 2024, one of the biggest factors to consider is that many countries the world over have upcoming election cycles this year. Elections can impact the outcome of global stocks in both ways, which may create volatility in stock markets, affecting the outlook of these stocks.

In addition, interest rate environments have so far offered stable conditions for businesses to operate, but if reserve banks, including the U.S. Federal Reserve, are compelled to raise interest rates, this could create headwinds in global markets, including stocks in the ACWI.

Takeaways

After a thorough review of ACWI, I believe that ACWI’s value proposition is not appealing enough for investors at the current moment, given the relative performance of its peers. Long-term investors may continue to stay invested, but its peers like DGT and VT funds offer better risk/reward. For reasons pointed out in this post, I believe a Hold rating would be appropriate at the moment for the ACWI fund.

Q2 2024 Earnings Call Transcript")